I don’t want to comment extensively on yesterday’s Reserve Bank announcement. It may prove to be the right call (or not), but in the data hiatus – 2.5 months since the last CPI, two months since the latest HLFS – they are to some extent flying blind (New Zealand really needs more frequent and timely key official macro data), and it would have been better to have rescheduled the announcements (adding one) as suggested in my post the other day. And the very brief, almost passing, mention of having considered a 75 basis point increase – which would have made a lot of sense this time last year – highlights again just how non-transparent and non-accountable New Zealand’s MPC is, We don’t know whether, in the end, any of the members actually favoured a 75 basis point increase, or did the Committee just toy with the idea briefly so that they could put a hawkish reference in the minutes? In places like the UK, Sweden, and the US we would have much greater clarity, and potential accountability – and potential accountability focuses the minds of decisionmakers who can, under the New Zealand system, collect their fee, turn up for lunch, and never have to do or say anything.

But looking for some other data I remembered an email from the Reserve Bank statistics group a few weeks ago indicating that they were finally going to publish some of the new data from the Survey of Expectations that they have been collecting for the last couple of years.

The survey has long asked about expected near-term policy rates (previously the 90-day bill rate as proxy, more recently the OCR) but in 2020 they added two new questions, asking respondents where they thought the OCR would be in 10 years’ time (describing that as a proxy for a neutral rate), and what they thought the average OCR would be over the next 10 years. I thought they – and especially the first question – were good additions to the survey (if we could get individual MPC members to give us their numbers, akin to the Fed’s dot-plot it would be even better).

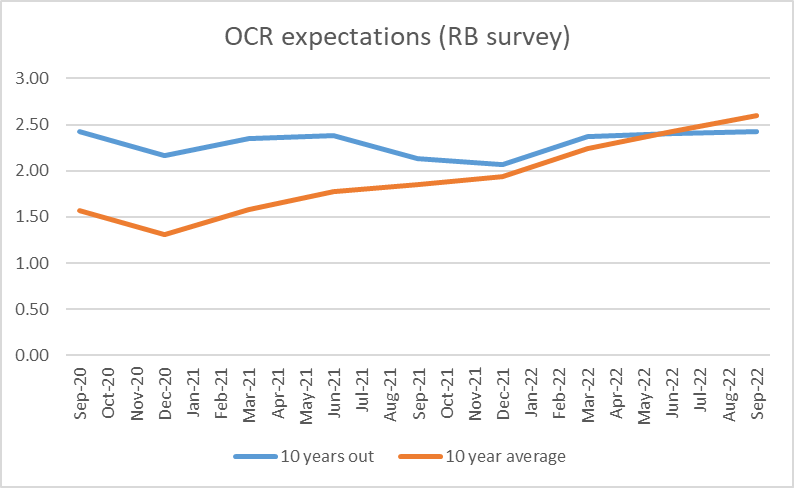

Anyway, here are the results (despite the extraneous labels Excel added in these are quarterly data, beginning with the Sept 2020 quarter)

The blue line (expectations for the neutral nominal rate) really took me by surprise. The first observation would have been captured around the end of July 2020 (I filled mine in on 20 July), and the second three months later, about the time long-term bond yields reached their all-time lows (and talk was of a possible negative OCR in 2021). And yet responses in the last couple of surveys aren’t much different – 2.42 per cent in the September 2022 quarter and 2.43 per cent in the September 2022 quarter. If you’d asked me to guess before the question was instituted, I’d have expected a much more cyclical series of responses (consistent with the variability we see in implied forward bond yields). And since the question is about nominal rates I wouldn’t have been very surprised now to have seen expected future nominal rates rising even if the real rates respondents had in mind weren’t changing much (core inflation undershot the target midpoint for the last decade, but perhaps it won’t in future).

The orange line is much less surprising. Back in 2020 there was a general expectation that the OCR would be very low for several years. As it became apparent that wouldn’t be the case, naturally the average expected over the subsequent 10 years tend to rise (and the intense pandemic period passes out of the 10-year window too).

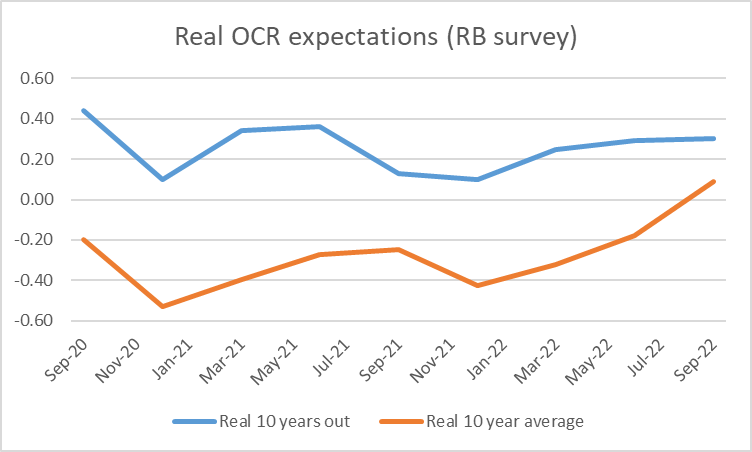

Both questions are about nominal rates. But the same respondents are also asked about their inflation expectations for periods one, two, five and ten years ahead. In this chart, I’ve taken the nominal responses (previous chart) and adjusted them for respondents’ inflation expectations: the 10 year ahead expectation for the blue line, and the average of the two, five, and 10 year ahead expectations for the orange line.

For what it is worth, this group of respondents still think the longer-term neutral real OCR is just barely positive, and their view has hardly changed since near the worst of the Covid shock (first observation), despite the recent huge upsurge in (core) inflation. Average expected real OCRs have increased this year as the OCR has been raised much more rapidly than was expected a year ago.

I don’t have a strong view on whether respondents are right or not (and, on checking, my own responses to the survey questions haven’t been consistently different from the average).

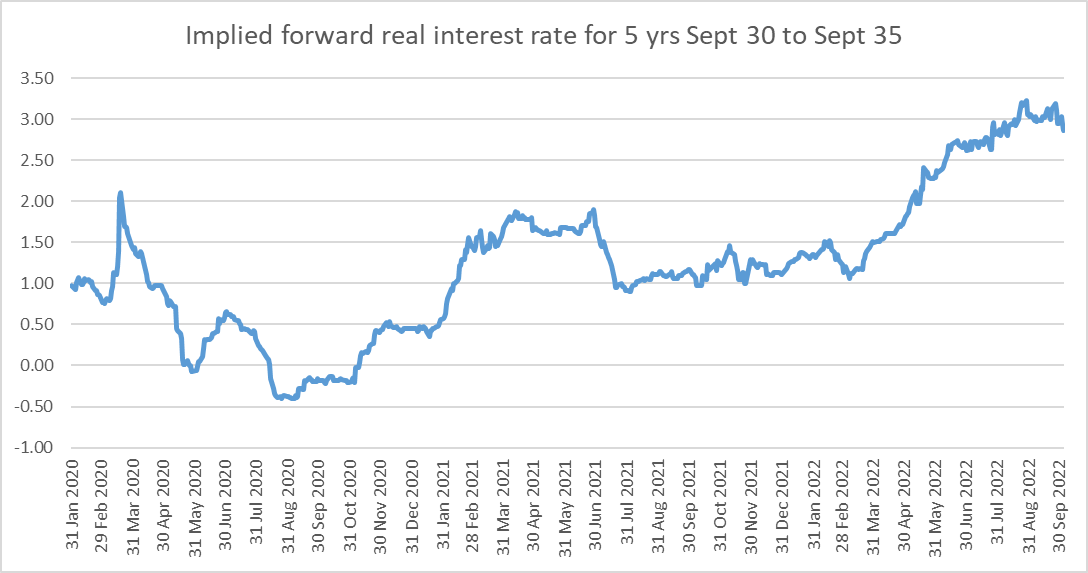

But…..these survey respondents seem to have very different views from the future rates implied by market prices.

In this chart I’ve taken the yields on the Sept 2030 and Sept 2035 government indexed bonds and backed out the implied real rate for the five year period between Sept 30 and Sept 35 – a period which encompasses the 10 years ahead OCR question for the period the Bank has been running the survey.

At the time of the most recent survey, respondents thought the real OCR 10 years hence would be about 0.3 per cent. At around the same time, the market prices suggested an implied future five year real bond rate of around 2.75 per cent. Sure there would usually be a term premium between OCR and a five year rate, but it wouldn’t typically be anywhere near that large. And our indexed bond markets aren’t the most liquid in the world, but the implied future rates in the chart don’t seem particularly out of line with (for example) implied future nominal government bond rates (using the May 2031, May 32, and Apr 33 bonds all currently yielding a little above 4 per cent), suggesting implied future nominal rates much higher than the 2.4 per cent (or thereabouts) survey respondents expect for the OCR 10 years hence.

I don’t have any answers to offer as to who is going to be proved right – most probably neither (there will be cycles next decade too, as well as whatever structural shocks might unfold) – but it is interesting to see such large gaps between survey responses and market prices. And kudos to the Reserve Bank for collecting (and belatedly publishing) the survey data.

I was always a bit ambivalent on the idea of a public holiday to mark the death (and life) of Her Late Majesty: there were (and are) better, cheaper, and more enduring things that could (have) been done. And the more so when the day chosen seems less to do with Queen Elizabeth (whose funeral and burial were a week ago) and more to do with the Prime Minister’s schedule. But here we are.

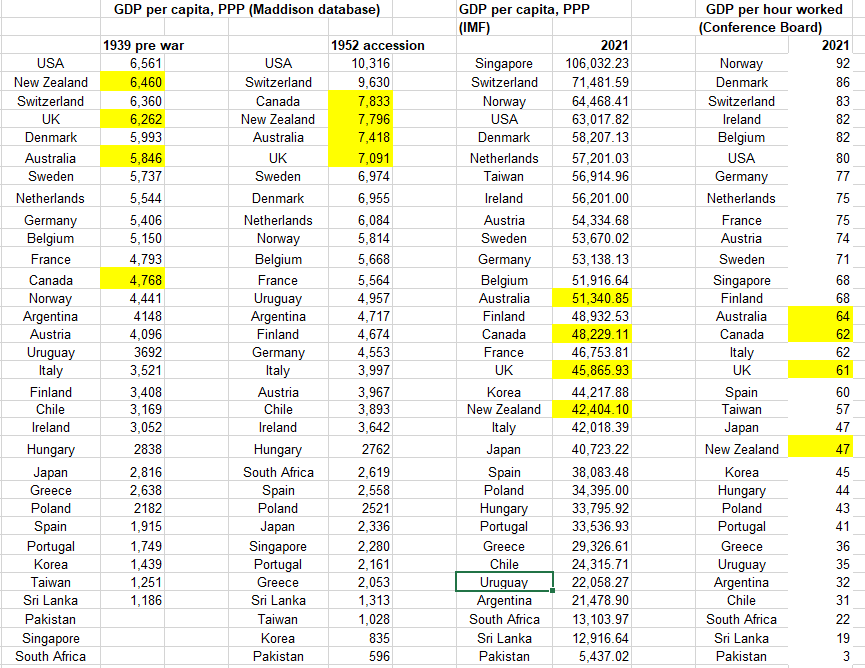

It seemed like a good day to potter in the old data and see how things went, in terms of relative economic performance, for the independent countries of which the Queen was monarch throughout her reign – the United Kingdom, Canada, Australia and New Zealand. Back in 1952 there were a few others – South Africa, Pakistan, and (as it then was) Ceylon. The other current realms (PNG, the Solomons, Belize, and so on) were not independent until later.

In the table below I started with Angus Maddison’s collation of historical GDP and GDP per capita (in purchasing power parity terms) estimates. I used the Western Europe and “offshoots” (NZ, Australia, Canada and the US), the east Asian countries that are now very prosperous (Singapore, Taiwan, Japan, and (South) Korea), included a few representative central European and South American countries, and included the other 1952 realms (South Africa, Pakistan, and Ceylon).

My main interest was comparing rankings from 1952 to those now. But if one starts from 1952, some people will make (not entirely unreasonable) objections about it being just after the war, and so the numbers may flatter countries that had little or destruction in World War Two, so I’ve also included 1939 numbers where (most cases) Maddison had them available. And for the most recent period I’ve included rankings for both GDP per capita and (my preferred focus) GDP per hour worked.

(UPDATE: This table replaces the original one in which I had inadvertently given Uruguay’s the US’s 2021 GDP and vice versa)

There are all sorts of extended essays one could write about relative growth performance over the decades/centuries for different groups of countries, but here my main interest is just in the four Anglo countries of which the Queen was monarch from 1952 until a couple of weeks ago. That picture is not a pretty one. 70 years ago all four countries were in the very top grouping, and these days not one of them is. Not in any way the fault of Her Late Majesty of course: she and her Governors-General act only on the advice of respective sets of ministers in each country, but a poor reflection on the countries concerned, and their successive respective governments nonetheless. New Zealand, sadly, has been by some margin the worst of them.

If I were inclined to be particularly gloomy – okay, I am – one could even note that the extent of the drop down the league tables for these stable democratic rule-of-law countries, isn’t materially different to the drop experienced by Uruguay, Argentina, and Chile, none of which enjoyed uninterrupted democratic governance over those decades. South Africa has had a similar drop down the league tables too.

I have my own stories about why most of the seven countries (Anglo and South American) have done poorly, but I don’t claim to have any particularly compelling tale about the UK and the extent of its continuing relative decline.

A couple of weeks ago I did the first couple of posts in a series looking at the Reserve Bank’s stewardship of monetary policy since the start of 2020 (and the start of Covid). That proved to be too much for my intermittent (at best) post-Covid energy levels, and although I will come back and complete the series that won’t be this week either.

But I was glancing at the Reserve Bank’s page of selected OIA releases (always interesting to see what others have asked) when I found this release last Friday under the heading “Growth of RBNZ”. The Bank appears to have adopted a new strategy where the OIA request responses it chooses to release on the website are released there on the same day the requester themselves gets the information (a strategy often intended to reduce the payoff to the effort involved in actually devising and lodging an OIA request – it has been more normal over the years to put releases on the website at least a few days after providing the information to the requester.)

Actually on checking again, I find that there were three releases on Friday, quite possibly to the same person. First was “RBNZ Brand and Design” (which request appeared to be in response to a Bank advert a couple of months ago for a brand manager), second was “Growth of RBNZ”, and third was “RBNZ media inquiries”. There is the odd amusing snippet in the first, including

and

In the third release, the answers aren’t very interesting (which media interviews the Bank did), but there were several questions with potentially interesting answers which the Bank claimed were dealt with in (long) documents on Parliament’s website as part of the Bank’s Annual Review last year.

But what really caught my eye was the “Growth of RBNZ” request/answers, where the requester had asked for breakdowns of staff numbers over the last 10 years. They didn’t really need to go back that far – all the 200 FTE growth in staff numbers has occurred since Orr took office (up from 255 then to 454 on 30 June 2022) but it was interesting nonetheless. One gets a very clear sense of the bloat. Here for example

(I can recall a time, 35 years ago, when the numbers were probably larger but (a) total staff numbers were even larger than Orr levels), and (b) most counted the slimming down as something much more appropriate, and appropriately concerned with a restrained approach to public spending.)

The Bank’s functions haven’t changed but – like too many public agencies – the number of “communications” staff has increased hugely

An OIA I’d lodged a couple of years ago (and written about here) gives a bit more background on that function (although numbers have grown more since).

We know there has been senior management bloat – a whole new lawyer of second tier appointees (Assistant Governors) most of whom seem to have little subject expertise to offer)

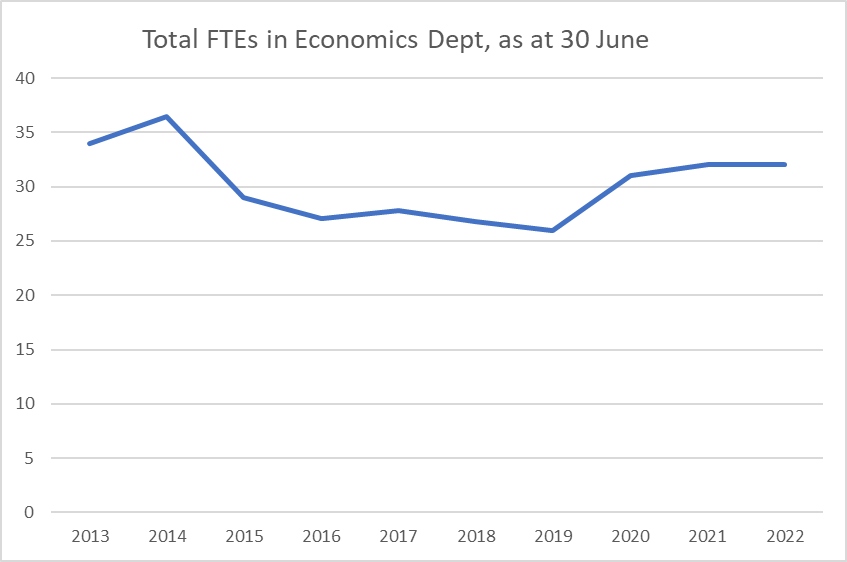

On the other hand, there are the Bank’s core economics functions. Until very recently, monetary policy was by statute the primary function of the Bank. That has changed (reasonably enough) but it is still a key core function. But here are staff numbers in the Economics Department

There are no self-evidently right or wrong answers as to how big a central bank Economics Department should be but there are few/no economies of scale, the Bank has been publishing very little serious research (or even revealing analysis) in recent years, and….inflation is through the roof. It doesn’t have the feel of an appropriate level of spending, especially when the Minister of Finance is throwing money at the Bank (all those hugely increased “support” functions above). But it is consistent with the stories one hears, at second hand but from inside the institution, suggesting that the Governor has little interest in monetary policy or the supporting macroeconomics. The Bank also released some salary data by function and it is striking that in 2021/22 the total salary spend on the Economics Department was almost 10 per cent lower than it had been in 2012/13.

The Financial Markets Department has usually been seen primarily as an element of the Bank’s monetary policy function (implementation etc), so it looks somewhat odd to see a huge increase in staff numbers there even as the economics function has been flat or falling. These were the operational people who, on the Governor’s instructions, lost the taxpayer billions and billions of dollars through the LSAP (so it isn’t even as if market functions were paying for themselves).

The other obvious area of growth – but harder to illustrate given the changing definitions/structures, so that numbers for the earlier period aren’t readily comparable to those now – is around the Bank’s financial stability functions. Some will welcome this growth, citing recommendations from the (fellow supervisors who did the) IMF’s FSAP a few years ago. Count me sceptical. For example, as at 30 June 2022 the Bank now has 38 people doing “Prudential Policy”, which feels large not just by historical Bank standards (there was a time 20 years ago when, perhaps going through the other extreme, all the prudential functions, not just policy, had about 10 people) but by comparisons with the policy functions for specific areas of policy in other ministries. It is, for example, more than the total staffing in the Economics Department. Oh, and they also have 22 staff doing “Financial Stability Assessment and Strategy” and yet the Bank publishes nothing particularly insightful and no research relevant to the prudential or financial stability functions. As best I can tell from this release, total staff numbers in the financial stability functions have more than doubled since 2018 when Orr took office.

Orr has long had something of a reputation as an empire-builder, and in his first four years at the Bank that seems to have been amply warranted again. This is scarce taxpayers’ money and yet Orr (facilitated by the Minister and the Board) flings it round with gay abandon……without even the consolation of better quality research, analysis, policy design, let alone policy outcomes. But it has been a windfall for HR people and former journalists.

I will resume my series of posts reviewing Covid monetary policy next week.

This post will be primarily of interest to former Reserve Bank staff, although may also interest those who are now, or were previously, charged with monitoring and holding to account the Reserve Bank. Most regular readers of the blog are likely to want to stop reading here.

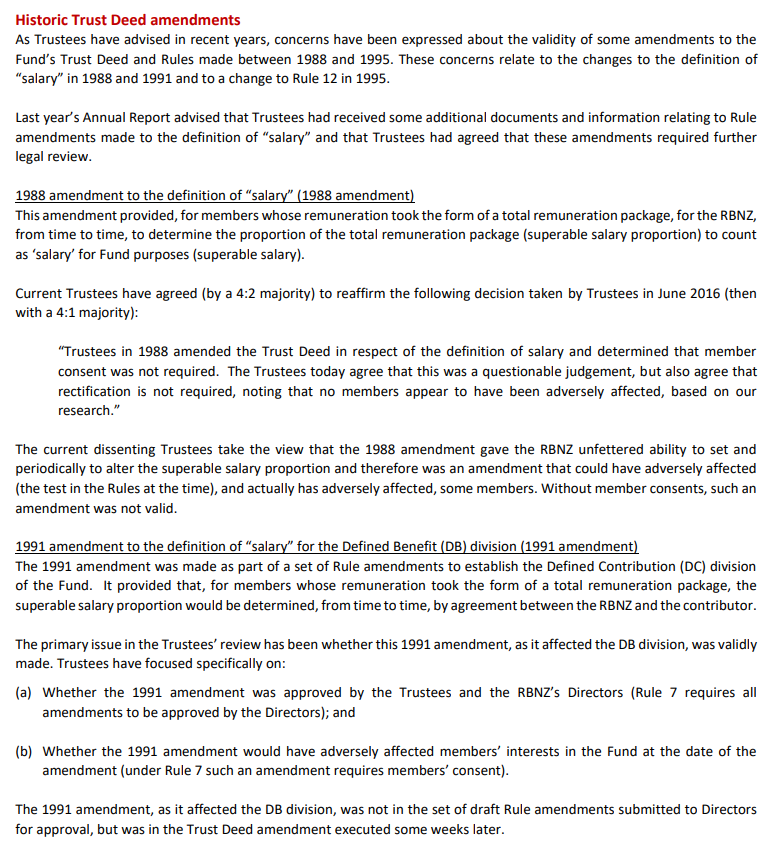

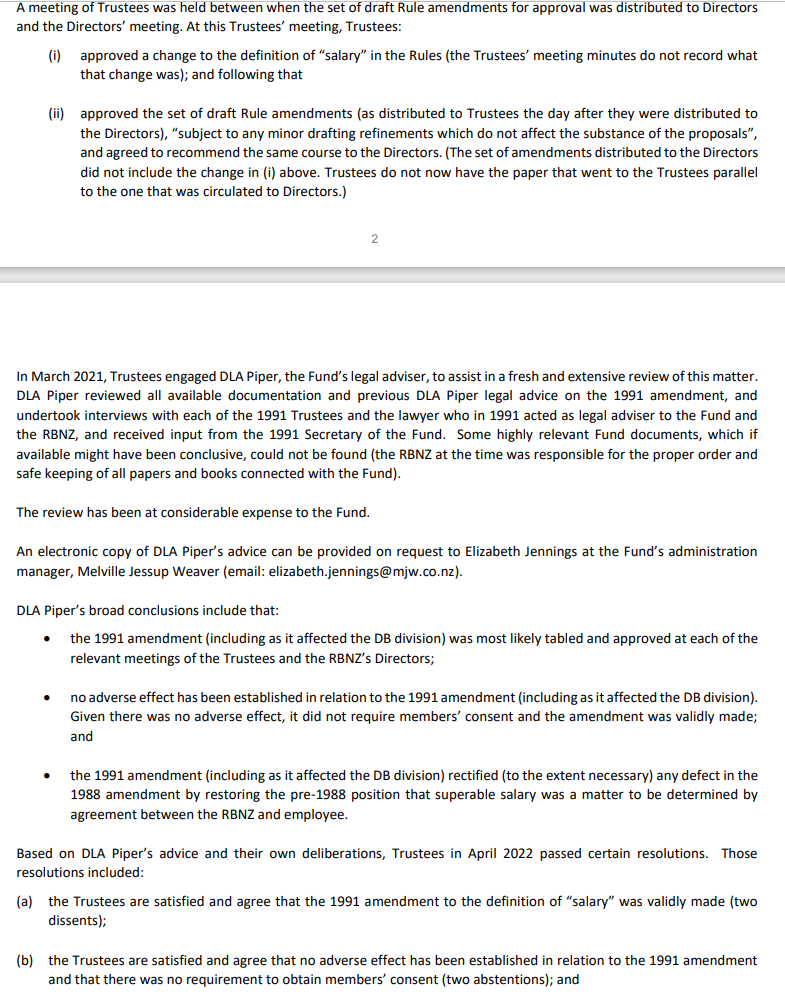

I have set out below, without further comment, a significant chunk of the latest Annual Report of the Reserve Bank of New Zealand Staff Superannuation and Provident Fund. I am both a member and a long-serving trustee of the scheme. The report is now in the hands of members, but is also a public document (readily available on the Disclose register at the Companies Office). The material in the extracts below may also be of interest and relevance to former staff who were once members of the scheme but are so no longer, and whose financial interests may have been affected by (contested) rule changes made some considerable time ago.

The Minister of Finance yesterday afternoon finally announced the rest of the members of the new Reserve Bank Board that takes office, under its new authorising legislation, today. In my post earlier this week, I highlighted a number of weaknesses in the legislation around the (dis) qualifications of the Governor and other Board members. None of the appointments to the Board appear to be in breach of the Act, but several are questionable on various counts, and taken together (and one should think about the composition of the Board as a whole) the new Board represents a poor, and grossly inadequate, start to the new regime. It could have been a great opportunity for a really impressive fresh start for the governance of the Bank. Instead, the Orr-Robertson degrading of the Bank continues.

As one gets older, rose-tinted glasses about aspects of the past are a risk. I do recall a time when the Reserve Bank Board had some really impressive people on it (mostly credit to Roger Douglas). But the dominant story over the almost 90 years the Bank has existed hasn’t been of impressive people being appointed to non-executive roles on the Board. In making appointments, at least since the government took full ownership of the Bank in 1936, political debts have always been paid or political loyalties rewarded – at times, past, present, and future overtly political figures have been appointed (and I even found one member who’d been a Communist Party donor), and the general quality has ebbed and flowed. One member I’m aware of – whom I gather turned out to make a reasonable contribution – was appointed mostly to spite a then Governor who vehemently objected to an economist the Minister wanted to appoint. There have been a handful of people with relevant subject expertise, some people good at asking (awkward) questions, and the time-servers and middling sorts who populate the myriad of boards and committees governments have to fill.

But – and it is an important but – none of them ever mattered very much. From the late 30s to 1990 it was clear that if the Board was the governing authority of the Bank as an entity (“the Board was the Bank” was used to say), most everything that really mattered about what the Bank did was decided – quite properly under the then-legislation – by the Minister of Finance and/or the Cabinet. That included policy, implementation, and key personnel (Governor and Deputy Governor). No doubt there were plenty of things for the board to do in that era – administration, buildings, staff etc – but it wasn’t the stuff we set up the central bank for. And from 1990 to yesterday, the Board had little say over anything much (not even the pay and rations stuff) but established as an monitoring and accountability body almost exclusively. It wasn’t quite that narrow, in that a person could only be appointed or reappointed as Governor if recommended by the Board.

As the overhaul of the legislation got underway, more recently people could only be appointed to the MPC on the recommendation of the Board, but OIA documents show that when the MPC was established they did not recommend names to the Minister but presented a list and said to Robertson “you pick”. This was the same Board that had got together with the Governor and Minister and put in place a blackball on the appointment to non-executive positions of anyone with actual hard expertise in monetary policy.

What of the new legislation. There have already been attempts at spin.

Thus, we have this from the Minister of Finance

The Board’s remit does not cover monetary policy, which remains solely the role of the Monetary Policy Committee.

And it is certainly true that the Board members do not get to set the OCR or publish projections. But as the Bank now points out on its website. “collective duties of the Board” now include

reviewing the performance of the Monetary Policy Committee and its members.

And it is the Board that has to recommend a person to be appointed (or reappointed) as Governor, and has to recommend appointees for the Monetary Policy Committee. It also has the responsibility to recommend removal of these people if they are not adequately doing their jobs.

In the Bank’s Annual Report (sec 240) they are specifically required to include

(m) a statement as to whether, in the board’s opinion, the MPC and the members of the MPC have adequately discharged their respective responsibilities during the financial year (seesection 99); and

(n) a description of how the board has assessed the matter under paragraph (m)

And that is just monetary policy. The Board also now has all the powers the Governor previously had on prudential regulatory matters (mostly banks, but including non-bank deposit-takers, insurers, payment system infrastructures), New Zealand’s physical currency, a large balance sheet. And there are a number of grey areas in the Act of matters which in my view really should be matters for the MPC, but seem to be matters for the Board. You will recall the big disputes a few years ago about the Governor’s ambitions to dramatically increase capital ratios: such things are now the responsibility of the Board. And recall that the whole point of the new Board model was to reduce the single-person risks inherent in the previous legislation (so don’t anyone think about running a “oh, none of this matters as the Governor runs things” response).

So lets look at the make-up of the Board.

Take the Governor first (and note the oddity of the new legislation where on paper the Governor is a totally dominant figure on monetary policy, but just another board member on the Bank’s other major policy/regulatory functions). With the best will in the world, no one would argue that Adrian Orr is a leading figure in either monetary policy or financial stability functions. With a really really impressive chief executive, the rest of the Board can matter a little less – but the best people need hard and informed questioning. All the signs suggest an undisciplined and petulant figure who just isn’t overly interested in the core responsibilities of the Bank – and that would be consistent with his record of speeches over his four years in office.

Then we have the chair, Neil Quigley, who was an economics academic and is now Vice-Chancellor of Waikato University. Quigley has been on the Board for more than a decade, has been chair since 2016 (and thus presumably bears the greatest responsibility for Orr, and what followed). But as I discussed yesterday in all those years on the Board there has been little sign of serious and hard challenge and scrutiny, and despite Quigley’s academic background there isn’t much sign these days of someone devoting a lot of time to keeping abreast of the literature on financial stability and regulation. How could he? Most would have thought a university vice-chancellor role in these difficult times would itself be at least a fulltime job. Quigley’s appointment appears to be a transitional one (to 30 June 2024), and his replacement would be a key opportunity for any new government taking office after next year’s election that was serious about restoring the authority, reputation etc of the Bank.

It is downhill from there with the rest of the Board. Taking them in alphabetical order

All laudable no doubt, but not a shred of a sign of suitability to be a board member of New Zealand’s prudential regulator or to be choosing appointees to the MPC and evaluating the performance of the MPC.

I’ve discussed Finlay previously. We can be relieved that his terms as NZ Post chair (owning Kiwibank and Kiwi Wealth) ended yesterday. He should never have been actively involved in Reserve Bank affairs while chairing the owner of a major bank. But that is now over, and we are left with someone who looks like a pretty generic professional director and accountant. Perhaps, and despite his past (what ethics does he display in having accepted the RB/NZ Post conflict), he could be a perfectly adequate director of yet another government body. But it isn’t evident there is any expertise or experience in monetary policy, prudential regulation, financial stability etc.

Higgins appears to be wholly and solely a diversity hire. Her background is all very interesting, perhaps even laudable, but…..this is the central bank and prudential regulatory agency, and there is not a shred of relevant background or qualifications – any more than a professor of Latin and university bureaucrat would typically have.

Paterson is another carryover from the old board. Perhaps she is just excellent (but remember all those questions we didn’t find in the Board minutes to now) but she is a pharmacist turned generic company director. There is a place for such people, perhaps even a couple on a central bank board, but subject matter expertise and energy on such matters seems less than evident.

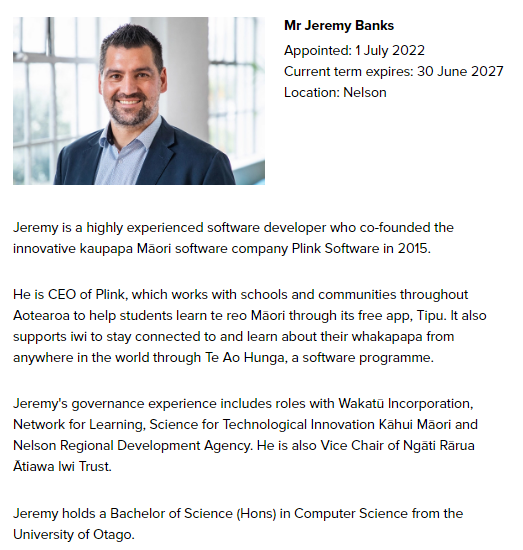

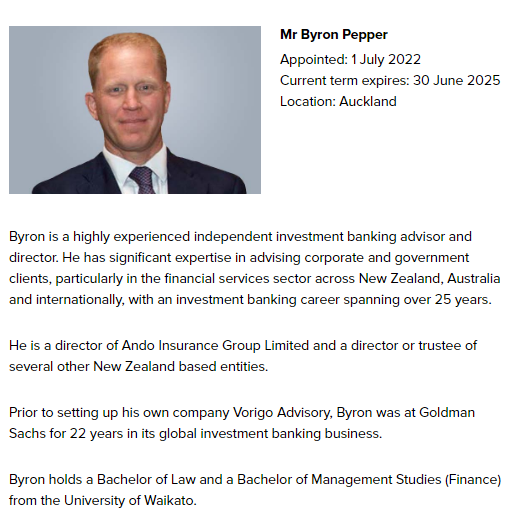

Pepper seems to be the only appointee with recent practical exposure to financial markets. On paper he looks like he could be quite a reasonable appointment to the FMA Board (perhaps a swap with Professor Prasanna Gai who is on the FMA but has expertise and experience that would be very valuable on the Bank’s Board or MPC). But the Bank’s Board is more about financial institutions than about wholesale markets and it isn’t evident he has much knowledge about institutions, the sort of risks that threaten them, or about financial regulatory policy – let alone being particularly fit for evaluating MPC members.

And then there is that insurance company he recently became a director of. According to the Minister

Mr Pepper is a director at Ando Insurance Group Ltd, but that role is not expected to create a conflict of interest as Ando is a non-regulated company.

The problem is that when you look up that company it is described as almost 40 per cent owned by a foreign insurer which is regulated by the Reserve Bank, and Ando describes itself as writing its insurance business for that regulated company. I don’t know either the business or the law enough to know why Ando itself is not regulated by the Reserve Bank, but on what we do know the appointment, while lawful, seems pretty questionable, and not (especially after Finlay) a great way to start a shiny new Board and governance model. One wonders what Treasury made of it when they provided advice to the Minister on appointees. (Or, indeed, the other political parties when, as the law now requires, they were consulted.)

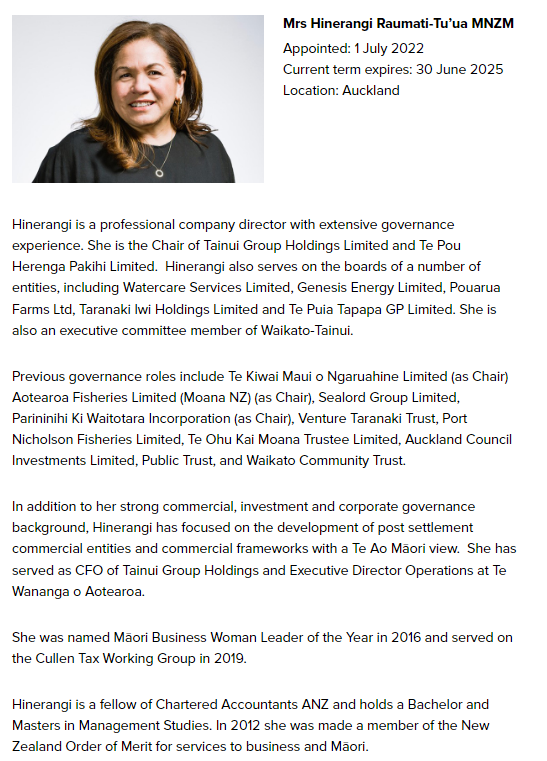

Raumati-Tu’ua (who seems to be a qualified accountant) is another of those generic professional directors. As I said earlier, there is a place for a couple of them on the Board, but there is no relevant subject matter expertise at all.

For the most part I am not suggesting that as individuals these people are unsuited to being on a mixed Board (although Higgins appears utterly unqualified, and Pepper questionable on ethical grounds), but what you end up with is a Board that is deeply unimpressive and really unfit for anything like the role the legislation envisages for the Board of the Reserve Bank. There is no one with any real expertise or authority in banking, no one with any real expertise on financial regulatory matters, no one who really seems fit (or ready) to be holding the MPC to account or making good choices about who should go on the MPC in future. And, perhaps a little surprisingly given the limited pool of expertise locally and the risks of too inward loking an approach, there is no one from abroad. As a group – however nice, and perhaps able they each are in their own fields – they simply aren’t up to what the job should entail, and that against the background on an inexperienced and underqualified senior management team. One can only imagine the Australian Prudential Regulatory Authority people reading of these appointments with some mix of despair and bewilderment while – condescendingly, but as they are prone to – suggesting that fortunately it doesn’t matter too much as APRA does the prudential supervision that really counts for New Zealand. That model – wind up and turn things over to APRA – was rejected (and rightly) by Michael Cullen almost 20 years ago, but his successor seems to be going for the worst of all worlds -a a bloated and expensive central bank of our own, led by people who do not warrant any great level of confidence in their individual or collective capabilities in the role they have taken up.

If there is a National/ACT government after the election it will have to make it a matter of priority to begin a far-reaching overhaul of the Reserve Bank (management and governance) to reverse the increasingly embarrassing spectacle of sustained institutional decline.

Meanwhile, of course, under the new law, the Minister of Finance was required to consult with other political parties on proposed appointees. It is a relatively unusual provision which Labour chose to put in the law, presumably intended to single their seriousness about a high quality Board that was broadly not too unacceptable across party lines (consistent with that, these appointees do not serve at will and can be removed only for cause – not including being ill-qualified in the first place). One wonders what National and ACT (in particular) said when the Minister consulted? Perhaps there were worse names on an original list. Perhaps the parties never bothered objecting, or perhaps they did object and Robertson just pushed on through anyway. Perhaps the relevant spokespeople could tell us?

I have lodged a series of OIA requests with the Minister, The Treasury, and the Reserve Bank to get a better insight on the process leading to those appointments, including the consultation with other parties.

My last short post was a month ago. At that stage post-Covid it was seriously taxing to read anything more demanding than Trollope, let alone even think about writing anything.

But with time, things improve. I had even harboured thoughts of a serious post this week – the one I’d like to write is about how we assess the culpability of central banks for the current and prospective inflation outcomes.

But….I had a commitment to write a 1000 word book review for a publication I write for. I did a draft of that yesterday, and doing so so badly knocked me back I won’t be trying anything similar for a while yet.

The gist of the post would have been:

Based on the information, understanding, and risks at the time, interest rate cuts in early 2020 were well-warranted.

(Core) inflation outcomes (globally) are largely the outcome of monetary policy choices 12-18 months previously.

12-18 months previously no one was forecasting inflation (or unemployment) outcomes akin to what we actually now see (check RB forecasts, NZ private sector forecasts, or overseas official or private forecasts).

That was a huge forecasting/understanding error, but……it is hard to hold central banks very culpable when no one much else saw the outlook any better (even if it is their specific job).

There is much more culpability about sluggish policy responses (or lack of them) from about a year ago, as the upside risks became increasingly apparent. Central banks took a punt, which hasn’t worked out, and we are all paying the price (in NZ it wasn’t until February that the OCR got to pre-Covid levels and the Funding for lending crisis programme is still running).

Serious scrutiny of central bank policymakers is now warranted, with a presumption against reappointment (but here two were just reappointed).

Oh, and the massive losses to the taxpayer from the bond buying programmes – purchases often occurring well after it was clear worst-case downside outcomes were no longer likely – are something central bankers are entirely culpable for.

And the book? Two Hundred Years of Muddling Through: The Surprising Story of the British Economy by UK journalist Duncan Weldon. It is short (300 pages), accessible (even chatty), judicious, informed by the literature, and strongly recommended (especially for the period up to about 1950) for anyone who wants to know a bit more economic and economic policymaking history. I’ve read a lot in that area, and so probably didn’t learn a lot new, but was interested to learn that on the eve of World War One, not only was the UK “the dominant manufacturer of exported goods, the centre of international finance” but also “the world’s largest net energy exporter” (that was the coal).

Three weeks ago I last wrote here, in a blithely optimistic tone

No posts last week between some mix of the war news (including related economics and financial markets news) being more interesting, and Covid – in our house that is. Not being too sick, but not being entirely well either I wasn’t concentrating very hard for very long. Fortunately, the isolation is now half over and no one’s health is particularly concerning. So back to some domestic economics and policy.

When our isolation began I’d picked off the bookshelves the first of the six of Anthony Trollope’s Palliser novels. Having been on the shelves for almost 20 years it seemed like a good opportunity to make a start on the series.

Unfortunately, although the whole family got Covid to one degree or other and all of them recovered fully, I – quite a bit the oldest, and perhaps previously prone to slow recoveries – did not.

And this morning I’ve just finished the last of the six Palliser novels (an enjoyable read if, perhaps, not as good as his Barsetshire novels).

As those who follow me on Twitter will know, it is not as if I have lost all interest in economic policy etc, but have just lost the ability to concentrate on anything more taxing than Trollope for more than perhaps 10 minutes without feeling really quite unwell and needing to lie down. Reading one 8 page memo bright and early yesterday morning completely did me in for the day.

There are many people much less well positioned than I am (including that I have an ample supply of novels etc on the shelves), so this is really just an advisory that it seems likely to be a few weeks at least before there are any other posts here. Which is a shame, as interesting issues abound (should, for example, the MPC consider a 75 or even a 100 basis point increase in the OCR next month?), but for now it is the way things are.

The National Party, in particular, has been seeking to make the rate of inflation a key line of attack on the government. Headline annual CPI inflation was 5.9 per cent in the most recent release, and National has been running a line that government spending is to blame. It is never clear how much they think it is to blame – or even in what sense – but it must be to a considerable extent, assuming (as I do) that they are addressing the issue honestly.

I’ve seen quite a bit of talk that government spending (core Crown expenses) is estimated to have risen by 68 per cent from the June 2017 year (last full year of the previous government) to the June 2022 year – numbers from the HYEFU published last December. That is quite a lot: in the previous five years, this measure of spending rose by only 11 per cent. Of course, what you won’t see mentioned is that government spending is forecast to drop by 6 per cent in the year to June 2023, consistent with the fact that there were large one-off outlays on account of lockdowns (2020 and 2021), not (forecast) to be repeated.

But there is no question but that government spending now accounts for a larger share of the economy than it did. Since inflation was just struggling to get up towards target pre-Covid, and I’m not really into partisan points-scoring, lets focus on the changes from the June 2019 year (last full pre-Covid period). Core Crown expenses were 28 per cent of GDP that year, and are projected to be 35.3 per cent this year, and 30.5 per cent in the year to June 2023 (nominal GDP is growing quite a bit). That isn’t a tiny change, but…..it is quite a lot smaller than the drop in government spending as a share of GDP from 2012 to 2017. I haven’t heard National MPs suggesting their government’s (lack of) spending was responsible for inflation undershooting over much of that decade – and nor should they because (a) fiscal plans are pretty transparent in New Zealand and (b) it is the responsibility of the Reserve Bank to respond to forecast spending (public and private) in a way that keeps inflation near target. The government is responsible for the Bank, of course, but the Bank is responsible for (the persistent bits of) inflation.

The genesis of this post was yesterday morning when my wife came upstairs and told me I was being quoted on Morning Report. The interviewer was pushing back on Luxon’s claim that government spending was to blame for high inflation, suggesting that I – who (words to the effect of) “wasn’t exactly a big fan of the government” – disagreed and believed that monetary policy was responsible. I presume the interviewer had in mind my post from a couple of weeks back, and I then tweeted out this extract

I haven’t taken a strong view on which factors contributed to the demand stimulus, but have been keen to stress the responsibility that falls on monetary policy to manage (core, systematic) inflation pressures, wherever they initially arise from. If there was a (macroeconomic policy) mistake, it rests – almost by definition, by statute – with the forecasting and policy setting of the Reserve Bank’s Monetary Policy Committee.

I haven’t seen any compelling piece of analysis from anyone (but most notably the Bank, whose job it is) unpicking the relative contributions of monetary and fiscal policy in getting us to the point where core inflation was so high and there was a consensus monetary policy adjustment was required. Nor, I think, has there been any really good analysis of why things that were widely expected in 2020 just never came to pass (eg personally I’m still surprised that amid the huge uncertainty around Covid, the border etc, business investment has held up as much as it has). Were the forecasts the government had available to it in 2020 from The Treasury and the Reserve Bank simply incompetently done or the best that could realistically have been done at the time?

Standard analytical indicators often don’t help much. This, for example, is the fiscal impulse measure from the HYEFU, which shows huge year to year fluctuations over the Covid and (assumed) aftermath period. Did fiscal policy go crazy in the year to June 2020? Well, not really, but we had huge wage subsidy outlays in the last few months of that year – despite which (and desirably as a matter of Covid policy at the time) GDP fell sharply. What was happening was income replacement for people unable to work because of the effects of the lockdowns. And no one much – certainly not the National Party – thinks that was a mistake. In the year to June 2021, a big negative fiscal impulse shows, simply because in contrast to the previous year there were no big lockdowns and associated huge outlays. And then we had late 2021’s lockdowns. And for 2022/23 no such events are forecast.

One can’t really say – in much of a meaningful way – that fiscal policy swung from being highly inflationary to highly disinflationary, wash and repeat. Instead, some mix of the virus, public reactions to it, and the policy restrictions periodically materially impeded the economy’s capacity to supply (to some unknowable extent even in the lightest restrictions period potential real GDP per capita is probably lower than otherwise too). The government provided partial income replacement, such that incomes fell by less than potential output. As the restrictions came off, the supply restrictions abated – and the government was no longer pumping out income support – but effective demand (itself constrained in the restrictions period) bounced back even more strongly.

Now, not all of the additional government spending has been of that fairly-uncontroversial type. Or even the things – running MIQ, vaccine rollouts – that were integral to the Covid response itself And we can all cite examples of wasteful spending, or things done under a Covid logo that really had nothing whatever to do with Covid responses. But most, in the scheme of things, were relatively small.

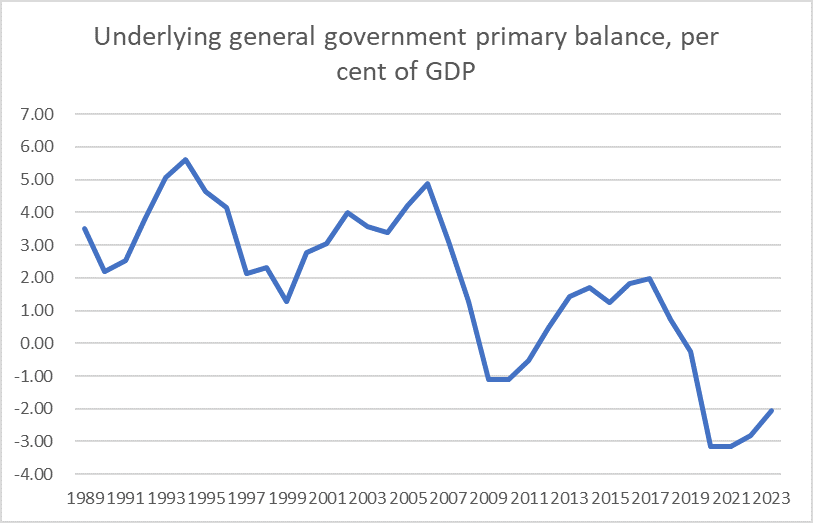

This chart shows The Treasury’s latest attempt at a structural balance estimate (the dotted line).

In the scheme of things (a) the deficits are pretty small, and (b) they don’t move around that much. If big and persistent structural deficits were your concern then – if this estimation is even roughly right – the first half of last decade was a much bigger issues. And recall that the persistent increase in government spending wasn’t that large by historical standards, wasn’t badly-telegraphed (to the Bank), and should have been something the Bank was readily able to have handled (keeping core inflation inside the target range).

The bottom line is that there was a forecasting mistake: not by ministers or the Labour Party, but by (a) The Treasury, and (b) the Reserve Bank and its monetary policy committee. Go back and check the macro forecasts in late 2020. The forecasters at the official agencies basically knew what fiscal policy was, even recognised the possibility of future lockdowns (and future income support), and they got the inflation and unemployment outlook quite wrong. They had lots of resources and so should have done better, but their forecasts weren’t extreme outliers (and they didn’t then seem wildly implausible to me). They knew about the supply constraints, they knew about the income support, they even knew that the world economy was going to be grappling with Covid for some time. Consistent with that, for much of 2020 inflation expectations – market prices or surveys – had been falling, even though people knew a fair amount about what monetary and fiscal policy were doing. In real terms, through much of that year, the OCR had barely fallen at all. It was all known, but the experts got things wrong.

Quite why they did still isn’t sufficiently clear. But, and it is only fair to recognise this, the (large) mistake made here seems to have been one repeated in a bunch of other countries, where resource pressures (and core inflation) have become evident much more strongly and quickly than most serious analysts had thought likely (or, looking at market prices, than markets themselves had expected). Some of that mistake was welcome – getting unemployment back down again was a great success, and inflation in too many countries had been below target for too long – so central banks had some buffer. But it has become most unwelcome, and central banks have been too slow to pivot and to reverse themselves.

Not only have the Opposition parties here been trying to blame government spending, but they have been trying to tie it to the 5.9 per cent headline inflation outcome. I suppose I understand the short-term politics of that, and if you are polling as badly as National was, perhaps you need some quick wins, any wins. But it doesn’t make much analytical sense, and actually enables the government to push back more than they really should be able to. Because no serious analyst thinks that either the government or the Reserve Bank is “to blame” for the full 5.9 per cent – the supply chain disruption effects etc are real, and to the extent they raise prices it is pretty basic economics for monetary policy to “look through” such exogenous factors. It seems unlikely those particular factors will be in play when we turn out to vote next year.

Core inflation not so much – indeed, the Bank’s sectoral core factor model measure is designed to look for the persistent components across the whole range of price increases, filtering out the high profile but idiosyncratic changes. Those measures have also risen strongly and now are above the top of the target range. That inflation is what NZ macro policy can, and should, do something about. But based on those measures – and their forecasts – the Reserve Bank has been too slow to act: the OCR today is still below where it was before Covid struck, even as core inflation and inflation expectations are way higher. Conventional measures of monetary policy stimulus suggest more fuel thrown on the fire now than was the case two years ago.

When I thought about writing this post, I thought about unpicking a series of parliamentary questions and answers from yesterday on inflation. I won’t, but suffice to say neither the Minister of Finance, the Prime Minister, the Leader of the Opposition, or Simon Bridges or David Seymour emerged with much credit – at least for the evident command of the analytical and policy issues. There was simply no mention of monetary policy, of the Reserve Bank, of the Monetary Policy Committee, or (notably) the government’s legal responsibility to ensure that the Bank has been doing its job. It clearly hasn’t (or core inflation would not have gotten away on them to the extent it has). I suppose it is awkward for the politicians – who wants to be seen championing higher interest rates? – and yet that is the route to getting inflation back down, and the sooner action is taken the less the total action required is likely to be. With (core) inflation bursting out the top of the range, perhaps with further to go, the Bank haemorrhaging senior staff, the recent recruitment of a deputy chief executive for macro and monetary policy with no experience, expertise, or credibility in that area, it would seem a pretty open line of attack. Geeky? For sure? But it is where the real responsibility rests – with the Bank, and with the man to whom they are accountable, who appoints the Board and MPC members? There is some real government responsibility here, but it isn’t mainly about fiscal policy (wasteful as some spending items are, inefficient as some tax grabs are), but about institutional decline, and (core) inflation outcomes that have become quite troubling.

Since I started writing this post, an interview by Bloomberg with Luxon has appeared. In that interview Luxon declares that a National government would amend the Act to reinstate a single focus on price stability. I don’t particularly support that proposal – it was a concern of National in 2018 – but it is of no substantive relevance. Even the Governor has gone on record saying that in the environment of the last couple of years – when they forecast both inflation and employment to be very weak – he didn’t think monetary policy was run any differently than it would have been under the old mandate. That too is pretty basic macroeconomics. It is good that the Leader of the Opposition has begun to talk a bit about monetary policy, but he needs to train his fire where it belongs – on the Governor – not, as he did before Christmas, forcing Simon Bridges to walk back a comment casting doubt on whether National would support Orr being reappointed next year. In normal times, you would hope politicians wouldn’t need to comment much on central bankers at all. But the macro outcomes (notably inflation), and Orr’s approach on a whole manner of issues (including the ever-mounting LSAP losses) suggest these are far from normal times. Core inflation could and should be in the target range. It is a failure of the Reserve Bank that it is not, and that – to date – nothing energetic has been done in response.

On 7 February 1952, New Zealanders woke and – whether they turned on the radio or picked up the morning newspaper – only then did most learn that the previous afternoon King George VI had died, and that his daughter Princess Elizabeth was now our queen, Queen Elizabeth II. 70 years ago, before most of us were even alive.

To look at today’s New Zealand media one might suppose that some decades ago New Zealand had angrily tossed out the monarchy. There has been barely any mention of the 70th anniversary of the accession of New Zealand’s Head of State and what coverage there has been seems determined to treat it as British news, not as news about our own Head of State – she holds that office by laws passed by New Zealand’s Parliament, and polls suggest that today’s New Zealander’s still favour the system of constitutional monarchy that we share with the UK, Australia, Canada, and a variety of other countries. Much as a significant chunk of the media class might lament it, Elizabeth is our Queen, and has been for 70 years now. Whether as Queen of New Zealand or of her other realms and territories, her reign is now one of the very longest ever in recorded history. If one dates modern New Zealand from some time in 1840, she has been our head of state for almost 40 per cent of our history. A remarkable life of service.

(And, in fairness, while the media have preferred to play down any sense of Elizabeth as our Queen, the Prime Minister did put out a gracious and fitting statement.)

Anyway, I got a bit curious about how the accession of the Queen, 70 years ago, had been marked in New Zealand and recorded in the New Zealand media. Papers Past is a wonderful resource although of the major city papers sadly only the Press is available for 1952.

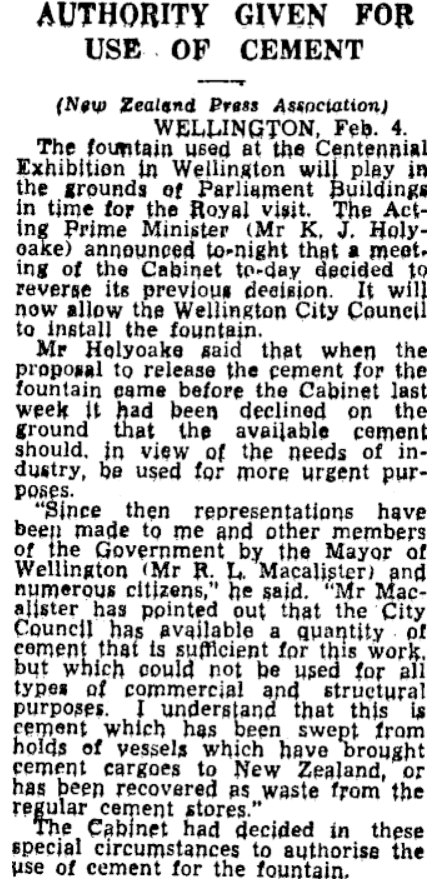

I started with the edition of Tuesday 5 February. In that paper it was reported that preparations were well underway for the planned visit to New Zealand in May of Princess Elizabeth and Prince Philip – undertaking the tour that the King himself had originally hoped to do. The Assistant Comptroller of the Royal Household had arrived on the 4th “to discuss final details and matters of etiquette. The economist is me could not, however, help noticing this element of the story.

It was a different time indeed, when the Cabinet was allocating cement.

The arrival of the Princess and her husband at the Kenyan lodge, where she was receive the grim news of the death of her father, was recorded in another story in which it was noted that the Queen and the Duke had attended Evensong at the small local church where “she spoke to the man who alone laid every stone of the church”.

What of Wednesday 6 February? It was a normal working day in New Zealand (and, as far as I can see from the table of contents there were no stories about the Treaty of Waitangi or the like). The Prime Minister – Sid Holland – was in Paris. Back here there were further reports of the forthcoming royal visit, including a push to keep handshakes to a minimum, and stories from the visit to Kenya. It was mid-summer and in Dunedin the touring West Indies cricket team had just beaten Otago.

King George VI died at Sandringham in the early hours of 6 February (New Zealand time being 12 hours ahead of that in the UK). The news was announced to be public at 11am (UK time).

In those days, the front pages of newspapers still seemed to be devoted to classified advertisements. It was no different in the Press of 7 February 1952. The news of the King’s death, and of the accession of Queen Elizabeth, appeared on page 5. This appears to be the editorial, and these were the first few sentences.

The Cabinet had met as soon as our government received the news, and the acting Prime Minister (Keith Holyoake) issued a statement in the early hours of the morning.

Despite the late hour – and presumably only for later editions – there are large numbers of stories, and photos (including one of the new heir to the throne, Prince Charles) over two pages (even managing to note that the forthcoming visit to New Zealand was now cancelled). There was an article about the visit by the then Duke and Duchess of York to New Zealand – and Christchurch in particular – in 1927 (among many other details, the Duke had had dinner with Labour leader Harry Holland in Westport).

The death of the King was marked immediately by the closure of all New Zealand schools on 7 February, and the closure of all government departments (other than essential services) for the afternoon of 7 February. No doubt there were many statements by local dignitaries around the country, but this was the statement by the (Labour) mayor of Christchurch.

In Greymouth, the mayor had requested that the bell of the local Catholic church be tolled 15 times (soon after the news first came through), once for each year of the King’s reign.

By the next issue of the newspaper – that for Friday 8 February – we still got through a great deal of other news first (the cricket test began that day in Christchurch) before the best part of three pages of coverage of the royal news.

There was a thoughtful editorial, even if it was a little wide of the mark with its suggestion “many [ in New Zealand] will never see her”, given the huge crowds for her first tour of New Zealand two years later. There was news of the forthcoming New Zealand official proclamation of the accession of the Queen, to occur the following Monday (more details here from the next day’s paper). The article is well-worth clicking through to for the details of official mourning, for the suggestion that employees should as far as possible be given time off on that Monday to attend local ceremonies marking the accession. This is just one snippet

Tributes from all manner of individuals and bodies – here and abroad – flowed in, and find a place in the pages of the Press. Here is an account of official American tributes and observances. And preparations for the funeral. From the next day’s paper, many resolutions of sympathy and loyalty.

By Monday 11 February, plans were in place. The King’s funeral was to be held that Friday (the Queen had requested that the day not be a public holiday). And the Prime Minister – who had been visiting West Germany when the King died – made a broadcast to New Zealand from London. In the same article it was reported that Mr Holland would be received by the Queen on Wednesday. Meanwhile back here the Governor-General, the Cabinet, and other dignitaries had attended a memorial service at (now Old) St Paul’s in Wellington. There were reports too of the special services in the churches of many denominations. If you wanted legal detail on the accession process, the Press had it covered.

In the Press of the 12th, you could read the (quite lengthy) account of the Christchurch civic proclamation of accession ceremony held the previous day – several thousand attended that ceremony, and there were similar smaller occasions in the boroughs around the city.

On the 13th we read that both the Prime Minister and the Leader of the Opposition (Walter Nash), both of whom had already been in London, would represent New Zealand at the funeral for the King. We also read of the Queen’s own declaration in taking her oath.

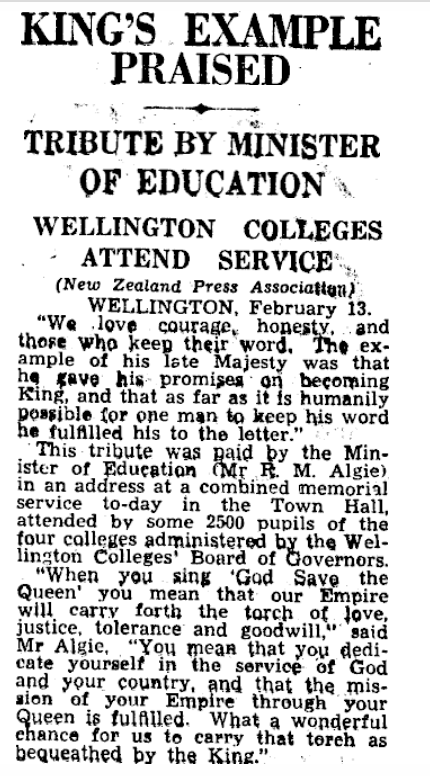

Back in New Zealand, in the following day’s paper we read some remarks made by the Minister of Education at a combined (four schools) memorial service in Wellington Town Hall.

The next day’s paper was full of articles about the funeral, but also carried this report of the Prime Minister’s meeting with the Queen, including this snippet.

And on the 16th, we read of the two minutes silence in memory of the King, and of great bell in Christchurch Cathedral tolling 56 times, once for each year of the King’s life, and so much more.

It was another age in many ways, but these surely were the monarchs of New Zealand, not by force or coercion but by the free consent, and loyalty of people, high and low, of all races and religions up and down New Zealand.

“Elizabeth the Second, by the Grace of God Queen of New Zealand and Her Other Realms and Territories, Head of the Commonwealth, Defender of the Faith—”

We shall not see her like again, whether in New Zealand or in her other realms and territories. But the 70th anniversary of her accession, to our throne, should very much have been New Zealand news.

The OECD’s latest Economic Outlook came out a few days ago. As always with the OECD, the value is rarely in the analysis or policy prescriptions, but mostly in the vast collection of more-or-less comparable tables, collating data for a wide range of advanced economies (and a few diversity hires).

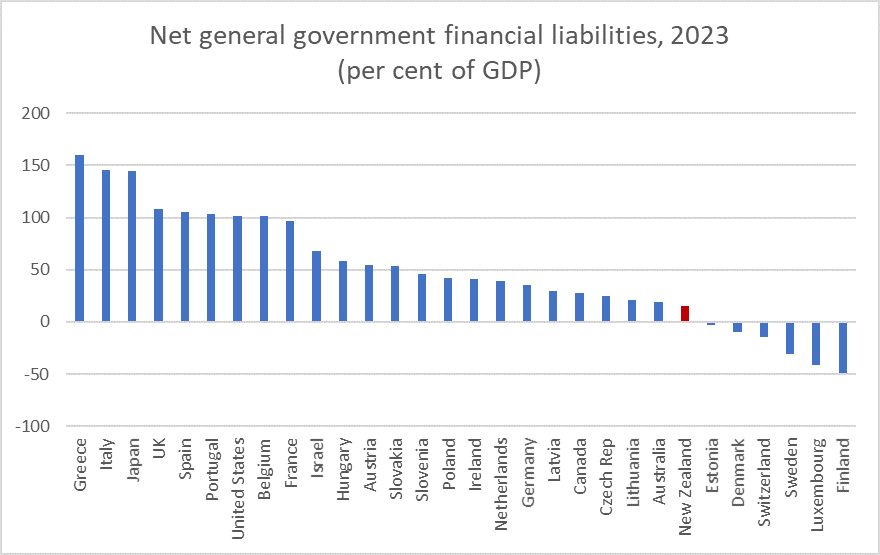

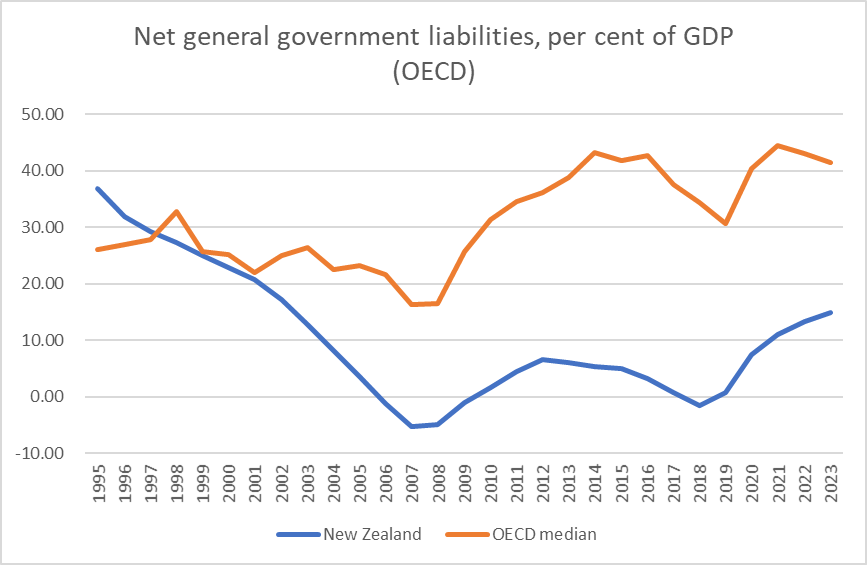

Take public debt as an example. Next week our Treasury will be out with their HYEFU and more-detailed New Zealand numbers for central government. But there is no easy way of comparing Treasury’s New Zealand numbers with those for other countries. And so I tend to focus most often on the OECD series of “net general government financial liabilities”, which includes all layers of government, and doesn’t exclude things that particular national governments find it convenient to exclude (in New Zealand’s case, all the assets in the Crown’s hedge fund, the NZSF).

The OECD’s forecasts only a couple of years ahead, but that is probably about the most that is useful anyway, Here are their recent forecasts for net general government liabilities as a per cent of GDP (for the 30 countries they do these numbers for).

For New Zealand, the 2023 number is 14.82 per cent of GDP and on these forecasts we’d be 7th lowest of (these) OECD countries. There isn’t a forecast for Norway for 2023, but they have net financial assets of about 350 per cent of GDP, so call it 8th.

Going into the pandemic, our net general government liabilities as a per cent of GDP in 2019 was 0.8 per cent. (Including Norway) we were 8th lowest of these OECD countries.

That is a not-insignificant increase in net debt as a per cent of GDP. Between 2007 and 2012 – serious recession and the earthquakes – net general government financial liabilities were increased by about 12 percentage points of GDP. But, and on the other hand, in five good-times years (from 2002 to 2007) net general government liabilities as a share of GDP dropped by 23 percentage points of GDP.

Here is the cross-country comparison over time

I’m not suggesting we should be totally comfortable about that picture, but our net public debt is forecast to remain (a) low, and (b) much lower than the typical advanced country.

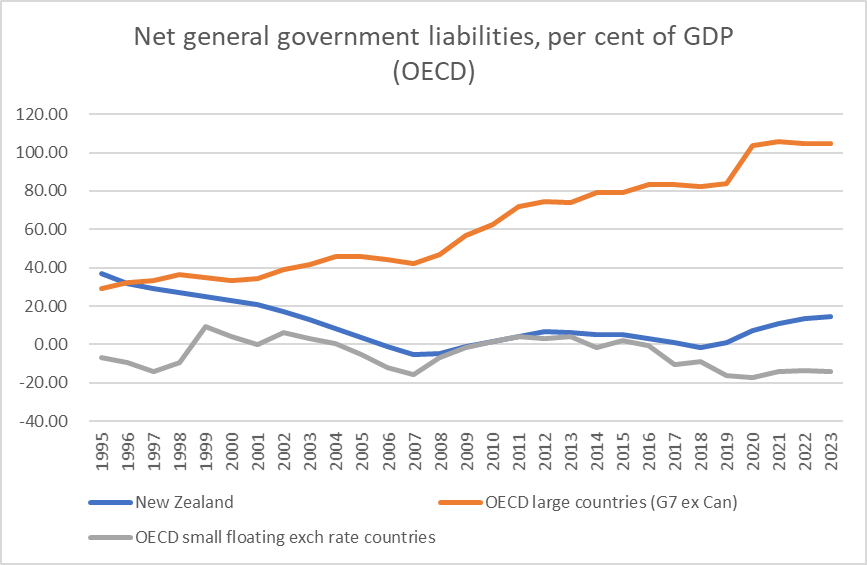

What if we break out the countries. Some argue (I’m not really convinced) that big countries, at least those with a history of reasonable government etc, can comfortably ran higher ratios of public debt than smaller countries. And, on the other hand, perhaps the countries most like New Zealand are the fairly-small places with their own central bank and floating exchange rate. Here are the relevant comparisions over time (medians in both cases).

The big countries – Germany excepted – really have been on a rising debt path. I’m not one who believes crisis and/or default is looming (generally – Italy remains a wild card) but were I a voter in one of those countries I’d be seriously uneasy. Were I involved in an opposition political party, I hope the high and rising debt would be made a salient political issue.

But – and generally – the small advanced countries have done pretty well (true on this sample of countries, or if one uses all the small countries – including those in the euro – in the database), and there has been (and is) nothing startling or particularly impressive about the New Zealand performance. If anything, one might note the widening gap at the end of the period.

Of course, none of this includes the fiscal challenges imposed by the rising NZS fiscal burden from maintaining the age of eligibility at 65 (although it is now a decade since baby boomers started turning 65) and the expected trend increase in public health expenditure….but I really can’t see public debt itself being a particularly salient issue in 2023.

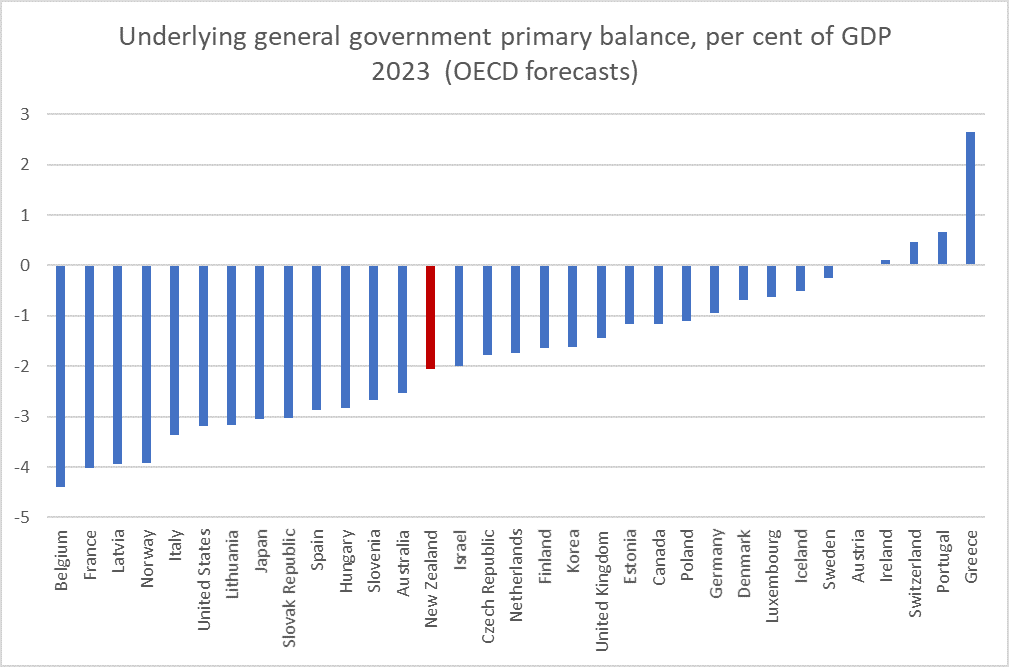

But what about deficits? No one argues the government should have been running a balanced budget last year, and perhaps not even this year (given the renewed lockdowns and big output losses the government left itself open to), but why not 2023? These are the OECD’s projections – the primary balance excludes financing costs, and a common rule of thumb is that even a small primary surplus is consistent with keeping debt in check. “Underlying” captures cyclical-adjustment.

In 2023, with the economy projected to be fully-employed (a reasonably significantly positive output gap), with a strong terms of trade, and (as ever) with some of the highest real interest rates anywhere in the advanced world, the OECD estimates that the government’s fiscal policy will see us in 2023 with a large primary deficit, a bit worse than the median OECD country. (Norway’s primary deficit is much larger, but remember that they have big net earnings (finance receipts) on the government’s huge net asset position.

Were one confident that spending initiatives were being ruthlessly scrutinised to keep waste to an absolute minimum, perhaps one might be a little less worried – although small structural surpluses, where spending is funded by taxes remains a good rule of thumb – but does anyone suppose that describes current New Zealand approaches to public spending.

I don’t suppose Ardern and Robertson are likely to let things get really out of hand. They seem oriented enough towards broad macro stability – in the traditions of all New Zealand governments of recent decades – even as they too watch our real economic performance decline, but at present the structural deficit picture (as the OECD interprets our data and policies) isn’t looking that good.

There should be considerable scrutiny on the government’s plans in the forthcoming Budget Policy Statement, and the Treasury’s HYEFU projections.