As a a key regulator of components of the New Zealand banking and financial system, and an institution which puts a great deal of emphasis in its regulatory philosophy (expounded again in a speech given only last night) on strong governance systems and protocols and the importance of directors taking very seriously their legal and other responsibilities, you might have supposed that the Reserve Bank would be punctilious in observing canons of good governance, to the limits of the legal requirements and beyond, for any institutions they themselves, and key managers, were associated with. After all, that respect for the law, for boundaries, for the appropriate management of potential and actual conflicts of interest for example, would surely be second nature. And, even if it weren’t, they would surely want to set a good example, and be whiter than white so that if questions even arose there would no doubt that the Reserve Bank was operating fully consistently with the best of the sorts of standards they espouse for (and often impose on) regulated institutions.

Unfortunately, if that had been your supposition, you would be quite wrong.

I’m a trustee of the Reserve Bank of New Zealand Staff Superannuation and Provident Fund. The long-standing fund, long since closed to new members, is established and operates under its under trust deed. It is a separate legal entity, with its own governance structures, lawyers,auditors, and is subject to the Superannuation Schemes Act, soon to transition to the Financial Market Conduct Act. The Reserve Bank is a party to the deed that establishes the fund, but neither the Reserve Bank, nor its Board of Directors (nor for that matter the Minister of Finance) has any powers in respect of the Fund. It cannot direct the trustees on their investments, or how to apply the rules, and nor has it any rights to demand information from the trustees. The Bank has obligations to the Fund under the trust deed, but no specific rights or powers in respect of it. By law – common law and statute – all trustees must operate in the best interests of the members of the Fund. The Fund, in essence, exists for members, in effect holding some of their remuneration in a savings vehicle and then paying out pensions and other benefits, under the rules, in due course.

On paper, the governance model is quite elegant. The Governor is a trustee. The Bank’s Board appoints one of its members as a trustee, and they also appoint one member of the scheme as a trustee (although both these appointees serve at the pleasure of the Board, and appointments can be revoked at any time if those trustees get difficult). And there are two trustees elected by the members for five year terms. I’m one of those members’ trustees. Most members are now retired, so typically members’ trustees also are (although I’ve been a trustee since 2008).

But whoever appoints the trustees, none of us serves as delegates or representatives of those who appoint us. We are all – equally – subject to the same legal responsibility that in conducting the affairs of the Fund, we must serve the best interests of members. If there is any (actual or potential) conflict between the interests of members, those conflicts need to be identified, but it is the interests of members that must be paramount. For material conflicts, conflicted trustees should absent themselves from involvement in the matters where conflicts arise.

This isn’t novel stuff. And it has long been recognized that when senior managers (or directors) of sponsoring organisations serve as trustees of superannuation funds, there is a particularly serious risk of conflicts of interest arising, between the duties those individuals owe to their employer, and those they owe to the members of the superannuation scheme. In the United Kingdom, the Pensions Regulator some years ago published a very useful and substantial guide to managing conflicts of interest in the context of superannuation schemes.

Management of these issues at the Reserve Bank scheme has been shockingly bad over the years. From meeting to meeting, there often aren’t material conflicts, but when the conflicts do arise there has been no evidence that the Governor (or, typically, his alternate – since the Governor consistently claims to unavailable for meetings, even when scheduled a year in advance) has managed those conflicts in ways consistent with their overriding legal obligation, when acting as trustees, to act in the best interests of members. I’m a bit of a starry-eyed optimist at heart, so have been constantly surprised at how indifferent to these responsibilities trustees who are senior Bank managers have been. Mostly, I don’t even think it is willful – but sheer indifference, or failure to appreciate the importance of appropriately managing conflicts of interest, are almost as bad. Perhaps especially in an institution that is a key financial regulator.

I could give you lots of boring detail about examples. This is a troubled scheme, against which complaints have now been made to the Financial Markets Authority (regulator of such superannuation schemes). But for now, those are issues for us, and many of them are very complex.

But this morning one of the issues has been put in the public domain by the trustees as a whole, acting under duress. This morning, the trustees made their first ever press statement (stories here and here) . And so since the matter is in the public domain, I feel free to give you some context.

On Wednesday last week, in the face of media coverage of some of the investments of the State Services Retirement Savings Scheme, I suggested to trustees that we should check with our investment managers on whether we had any similar exposures, about which questions might be raised. As I noted then, I wasn’t particularly concerned for the fund itself – a private body, and closed to new members – but recognized that there might be some reputational questions for the Bank, and that we should probably be aware of any such exposures. Our regularly quarterly meeting was to be held the next day, which would provide a good opportunity to discuss the matter (albeit, we already had a full agenda).

Our administration managers arranged to get the relevant information, at least at a high initial level, identifying that in one passive offshore equity fund we had holdings of, some of the underlying shares were those of firms associated with what might be considered “controversial weapons”.

The next day we held a meeting of trustees. It was long and difficult one dealing with several other issues. The Reserve Bank’s Deputy Governor, Geoff Bascand, is the Governor’s alternate (when the Governor is unavailable to attend) and also chairs the meeting. He made no effort to raise the “ethical investment” issue, and when he tried to adjourn the meeting I pointed out that we had still not discussed this issue. Geoff insisted he had another meeting, and rather than (say) handing over the chairmanship to another member, he simply refused to have a discussion, made no effort to schedule one even by email (we only meet quarterly) and ended the meeting and left. Curiously, as he left the meeting he signed, as chair, a revised Statement of Investment Performance and Objectives (SIPO), a document all superannuation schemes need to have, that reaffirmed our existing investment approach, including (explicitly) the holdings in the offshore index fund that had the small “controversial weapons” exposures.

We heard nothing more until late on Monday when Geoff emailed trustees about a written parliamentary question that the Minister of Finance had received. Predictably, questions had been raised about the holdings of the Reserve Bank superannuation scheme. As is customary, the Minister’s office had referred the PQ to the Reserve Bank for advice on a draft answer. The people who handle PQs etc in the Reserve Bank work to Geoff, as Deputy Governor.

It wasn’t clear to me what business it was of the Minister of Finance. The Minister has no ministerial responsibility for the Reserve Bank superannuation fund (structure and governance as above) although he no doubt does have responsibility for the actions of the Reserve Bank (including vis-à-vis the Fund). How the Minister chose to answer was, and is, up to him. However, the information requested in the PQ belonged to the trustees, and no one else (in this context, the Reserve Bank or the Minister) had any legal right to demand it from us. It was our information, and our members’ money.

In a well-governed institution, Geoff would have passed on the PQ to trustees and invited trustees themselves to consider how the Fund should respond. If the Bank had wanted us to provide the information so that, in its interests, it could pass it on to the Minister, a proper request, cognizant of the legal responsibilities of the trustees, could have been made to the trustees. And given the potential for the interests of the Bank and the trustees to diverge, Geoff would wisely have taken no further role in the discussions on the matter by the trustees.

But this was the Reserve Bank. By the time, late on Monday afternoon, that trustees were even made aware of the issue, Geoff had already emailed our investment managers and got the detailed information that was being sought in the PQ. In fact, he had known about the request since mid-afternoon on the previous Friday. And when he emailed the investment managers, he didn’t keep the information to the trustees (or their own administration managers), he copied in Bank staff who had nothing whatever to do with the superannuation scheme. Emails went back and forth on Sunday and Monday, every single one was copied to other Bank staff, and the trustees had still not been made aware of the issue. To the extent that Geoff Bascand had a right to the information on the Fund’s investment, it was solely as an (alternate) trustee, not as Deputy Governor of the Bank, and he had no right at all to use that information himself for Bank purposes or to share that information with Bank staff, without the prior authorization of the trustees as a whole.

That made the whole exercise a fait accompli. Whatever the attitude of trustees, the Bank now had our information and was free to use it as it chose. Geoff’s email to the trustees late on Monday afternoon said “we have to supply information” – but it wasn’t clear, at all, who “we” were. The trustees were certainly under no legal obligation to do so.

As the first trustee to respond to Geoff, I noted that the Minister had no power over, or ministerial responsibility for, the Fund, noted that we needed to obey any laws constraining our specific investments, noted that shifting the portfolio in response to Bank reputational concerns could be costly so the Bank might need to consider reimbursing the Fund, and also highlighted the importance of ensuring that conflicts of interest were appropriately managed in handling this issue.

There was never of any sign of that. The Bank – having obtained our information without authorization – simply advised us, via emails from Geoff (never clear from them whether acting as a trustee or as Deputy Governor) that the Bank would pass on our information to the Minister, would advise the Minister to answer the question fully, and would advise the Minister to say that the Bank would be seeking to encourage us to adopt an “ethical” investment policy. Continuing his glaring inability to recognize the different interests of the Fund and the Bank, he urged trustees not to approach the Minister’s office directly “as the Bank was handling that”. The Bank, of course, was not required – or expected – to operate in the best interests of members (or trustees).

We gravitated towards the idea of putting out our own public statement – while Geoff continued to act as conduit for the Bank in telling us what the Bank “insisted” had to be in such a statement. At one point, I explicitly asked Geoff, acting as trustee, what course of action he thought we should take, acting (as legally required) in the best interests of members. He simply refused to answer directly, responding with the following extraordinary comment

Now I accept that this may reflect the Bank’s interests more than that of Trustees per se, but the reality is that a Bank director, the Governor and a bank employee are trustees (with me as alternate and chair).

All these people are legally required to act in the best interests of members. For several years, I was an employee and a trustee, and I hope I always sought to do so.

Fighting something of a rear-guard action, I argued that if we were giving the information about these exposures to anyone, we should at very least provide it to members of the scheme before we provide it to the Minister of Finance, let alone the public. It is, after all, their money, and if there are to be any changes in investments as a result of a distaste for particular types of exposures, members’ preferences should presumably be the ones that count. That request got nowhere either, with Geoff apparently much more interested in his day job as Deputy Governor. We finally got a grudging statement that the information would be sent to members shortly after our public press release went out at 10am this morning. It went out, baldly, with no context or background. Frankly, it is the sort of process that treats members with disdain. I can only apologise to our members for that.

There has been a suggestion that even a passive interest in cluster munitions firms, through a very broad-based index-linked fund – we held one that mirrored the MSCI World ex Australia index – was illegal under New Zealand law. There is a range of views on that issue apparently, and reallocating any fund’s investment involves (potentially quite material) transactions costs, but even when it was suggested that we should consult our own lawyers, or the legal opinions of industry bodies, Bascand has little or no interest. The best interests of members didn’t seem to matter, but the “reputation” of the Reserve Bank did. I have no particular problem with the Reserve Bank managing its own reputational risks – recall, I was the first person among trustees to even raise the issues – but for a Reserve Bank senior manager to abuse his position to force through the Bank’s interests is quite another matter.

In the press release it states that

Trustees will act expeditiously to eliminate our exposure to these firms.

In fact, when I pointed out yesterday that if we were going to say this, we really should have some sort of process in place to effect the change (eg formally request options and costs from our investment managers), I was simply ignored. Trustees have not commissioned any such process yet. I guess what mattered more to the Bank was to (have the trustees) be seen to say it.

The press release goes on.

The Bank has requested that Trustees adopt a socially responsible investment policy and we will consider the matter at our next meeting.

At the time this press release was agreed there had been no such request at all. When I asked again last night, shouldn’t we actually have a written request from the Bank if we were going to say there was such a request, one finally came through at 8.24 this morning. Interestingly, it came from the Bank’s Communications Manager, highlighting the extent to which this is mostly a Bank PR management issue. Graciously, the Bank sent through a version of their “socially responsible investment policy”, expressing their “surprise” that the trustees did not have such a policy and commending to us the example of theirs. This blatant attempt to seize the high moral ground was somewhat undermined (in addition to the fact that the Governor himself is a – absentee – trustee) by the fact that their own ‘responsible investment’ policy document does not apply to international ventures the Reserve Bank is party to, or to any specific countries. Which is convenient because, as I used to point out as an insider, it allowed the Bank to invest New Zealand taxpayers’ money in Chinese government bonds, do swap deals with the Chinese central bank, even though China remains one of the greatest human rights abusers of modern times, as well as an aggressively expansionist power. Maybe that is just fine, in the interests of international relations, but don’t try claiming the moral ground Governor. Perhaps its just me, but $15000 of passive indirect holdings in companies that may be making cluster bombs, bother me much less than the Bank funding the butchers of Beijing. Tastes on that will differ – but the Reserve Bank’s assets are public money, and the superannuation scheme’s assets are not.

So let’s summarise:

- as recently as last Thursday, this issue didn’t bother Bascand – or his boss, who could have turned up to a trustees meeting – enough to even have a discussion at a long-scheduled meeting. Despite the points I’ve noted here, had they done so, I’d have suggested we get a prompt legal opinion, get out of such exposures expeditiously if they were illegal, and if not would have been happy to have agreed to restructure the portfolio if the Bank had covered the transactions costs etc of doing so.

- But once the PQ was asked, the Bank panicked. Good governance processes were over-ridden and in exchange after exchange, Geoff Bascand – a man generally regarded as ambitious to become the next Governor – prioritized the interests of the Bank over the interests of members of the superannuation fund. That wasn’t just bad form, it was in breach of the fundamental duty of trustees.

- When an institution communicates with an associated institution, that is only a email away, primarily by press release, you know that what is going on is mostly about spin and PR.

Does it really matter? On the specific issue, perhaps not overly, and the final outcome might well have been the same anyway. After all, I’d raised the issue before the MP did. But as the old saying had it “take care of the pennies and the pounds will take care of themselves”. It applies as much to doing the small stuff well, and having good and disciplined processes in place, and observed. The Reserve Bank would surely expect no less from the institutions it regulates/supervises. And when small stuff is done badly – as it was here – it often points to some rather serious problems in the institution concerned. .

I don’t know how the Minister of Finance will eventually choose to respond to the original parliamentary question. I’ll watch with some interest, conscious that it will be one of those days when an Opposition MP can take heart. That MP will have made a difference.

In the course of all this, it became clear that most dealings of the superannuation scheme, and all the email traffic over this issue, is captured by the Official Information Act (since two trustees are Reserve Bank employees, using Reserve Bank computers and email addresses) and thus the material is “held” by the Reserve Bank. I wouldn’t necessarily encourage it, but anyone interested could seek the whole gruesome paper trail.

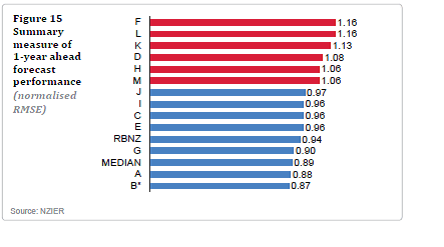

The median forecaster is between forecasters J and D. Again, the Reserve Bank looks no better (or worse) than the group of forecasters clustered near the median forecaster.

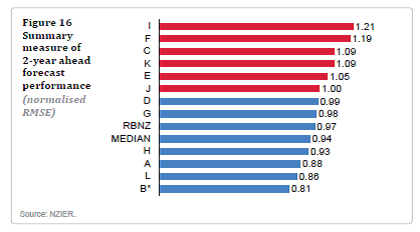

The median forecaster is between forecasters J and D. Again, the Reserve Bank looks no better (or worse) than the group of forecasters clustered near the median forecaster.