I’ve had a bit of a relapse in my recovery and seem set to spend much of this week doing little more than lying on the sofa reading something not too taxing. There are plenty of things I’d like to comment on substantively, but for now it won’t happen.

The Reserve Bank released its (latest – third in three years) final LVR decision on Monday. To no one’s surprise, after a sham consultation, they confirmed the Governor’s original plans, albeit with some curious refinements to the exemptions – curious, that is, if one thinks that decisions on such things should be based on considerations – the statutory ones – around the soundness and efficiency of the financial system.

And although the lawgiver has now descended from the mountain and issued his unilateral decrees, which have the force of law, there is still no sign of a regulatory impact assessment. There is talk in the summary of submissions that one is forthcoming, but really……when the regulatory impact assessment is published only some time after all the decisions have been made, it reveals quite how little weight the Governor seems to put on good processes. And it is not as if the initial consultation document was sufficiently extensive and robust to cover the ground – recall the “cost-benefit” analysis that consisted of a questionable list of pros and cons with no attempts to quantify any of them.

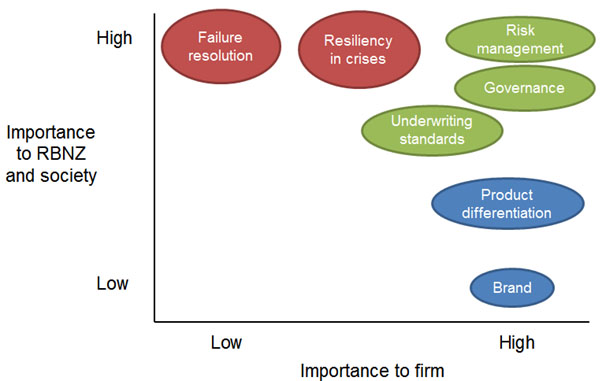

One of the other things I had hoped to comment on in more depth was a speech given last week by Toby Fiennes, the Reserve Bank’s Head of Prudential Supervision. on the Bank’s regulatory philosophy and supervisory practices. It included this nice chart, outlining various aspects of financial institutions’ operations and how much, in the Bank’s judgement, they mattered to the “RBNZ and society” (as if these were the same thing) and how much they mattered to the institutions themselves.

Figure 1: Selected interests of the RBNZ, society and financial institutions

Fiennes went on to note that the blue areas aren’t of much interest to the Bank (and don’t therefore attract much regulatory interest), while the red area are typically quite heavily and directly regulated.

But in this context, it was the comments on the green areas that caught my eye

Some things – like risk management and underwriting standards (in green) – are of strong interest to both the Reserve Bank and firms. Here we tend to use market and self-discipline. Examples of some of our supervisory practices in this area are:

- Disclosure of credit risks;

- Mandatory credit ratings;

- Governance requirements; and

- Publicly disclosed attestations by the board that key risks are being managed.

Now I know that the Bank’s prudential supervisors have never been keen on LVR restrictions, and that they are devised in a different department, but……..all controls are imposed under the same legislation – indeed the same part of the legislation – and by the same Governor. And when housing loans are the biggest single component of banks’ credit exposure – and banks have most to lose if things go wrong – and yet when the Bank has imposed three sets of direct controls on housing LVRs in three years, imposing its own judgements on underwriting standards, you might have hoped that practice and “philosophy” might have been better reconciled, or the gaps smoothed over in a speech by the Head of Prudential Supervision.

As regular readers know, I’ve been pushing to get submissions on Reserve Bank regulatory proposals routinely published. Such publication is common practice in other areas of government, including submissions to parliamentary select committees. If you make a submission seeking to influence public policy, that submission should generally be public as matter of course – it should be one of the hallmarks of an open society.

Some progress has been made with the Reserve Bank. If someone asks, they will now typically release submissions made by anyone who isn’t a regulated institution. I asked for all the submissions on the latest LVR “proposal” to be released, and – as expected – the Bank has released all those not made by banks (the regulated institutions in this proposal). Anyone interested can find those submissions here. I have three remaining areas of concern.

The first is that release of submissions should be a routine part of the process for all consultations, not just when someone makes the effort (remembers) to ask. The second is that on this occasion they have withheld the names of four private submitters. As I noted, if you want to influence lawmaking, you should be prepared to have your name disclosed. How can citizens have confidence in the integrity of lawmaking processes if they don’t know who the Bank is receiving submissions from, and what interests they may represent? (Of course, since one of the anonymous submitters appears to have views very similar to my own, we can safely assume that that person’s views will have had no influence on the Bank.)

And the third concern is that the Reserve Bank is still consistently keeping secret the views of regulated entities (the banks in this case). When the regulated lobby the regulator it is particularly important that citizens are able to see what arguments are being made, to ensure that the process remains robust and that the regulators are not being “captured” by their closeness to the regulated – bearing in mind that the Bank is supposed to be regulating in the public interest, not that of banks. As I’ve noted before, the Bank justifies withholding bank submissions on the grounds of section 105 of the Reserve Bank Act – which they argue compels them to withhold such material. In fact, that section of the Act gives no hint of a distinction between material received from banks and that from other parties, If section 105 applies to submissions on proposed regulatory changes, the Bank is obliged to keep secret all submissions, not just those from banks. As I’ve noted before, there is a good case for a small amendment to the Reserve Bank Act to make it clear that the section 105 protections do not apply to submissions on regulatory proposals and hence that banks should expect their submissions to the Reserve Bank on regulatory initiatives to be published, in just the same way that bank submissions to parliamentary select committees will generally be published.

I have appealed to the Ombudsman the Bank’s decision to withhold the bank submissions, in effect seeking greater legal clarity on what the section 105 restrictions actually apply to. In the meantime, of course, if the banks have nothing to hide – and I don’t imagine they really do – they could chose to publish their submissions. According to the Summary of Submissions “a few respondents urged tighter LVR restrictions on investors than proposed”, so perhaps the ANZ really did follow up on their CEO’s newspaper op-ed and advocate more far-reaching restrictions. If so, citizens should have the right to know (customers might be interested to, but that is their affair).

Is there really no RIS?

I could understand if some small Ministry struggled with them but my experience of the big ones – Treasury, Inland Revenue, MBIE, DIA all take them very seriously and do the best job they can with the timescales and the information they hold. I would have expected RBNZ as one of the ‘big guys’ to do an equally professional job.

LikeLike

One will “follow shortly” according to the Summary of Submissions. The Bank has never taken RISs terribly seriously and had no arms-length internal review even when they did produce a document.

LikeLike

Surprising that they haven’t done the regulatory impact assessment yet…

From the Reserve Bank of New Zealand Act 1989:

162AB Assessment of regulatory impacts of policies

(1) The Bank must—

(a) assess the expected regulatory impacts of any policy that it intends to adopt under Part 5, Parts 5B and 5C, and under the Non-bank Deposit Takers Act 2013 and the Insurance (Prudential Supervision) Act 2010; and

(b) assess the regulatory impacts of the policies adopted and applied under Part 5, Parts 5B and 5C, and under the Non-bank Deposit Takers Act 2013 and the Insurance (Prudential Supervision) Act 2010 at intervals appropriate to the nature of the policy being assessed; and

(c) give reports on the assessments to the Minister.

(2) Subsection (1) does not apply in respect of any policy that is of a minor or technical nature.

(3) The Bank may provide reports on the assessments of regulatory impacts to the Minister—

(a) as part of an accountability document or other report; or

(b) as a stand-alone report prepared following a request by the Minister or on the Bank’s own initiative.

(4) The Bank must publish every report on the assessment of regulatory impacts on an Internet site maintained by, or on behalf of, the Bank.

LikeLike

Regulatory Impact Statement by the RB in 2007 to 2009 should read as follows. Raised OCR to 9% and pushed bank interest rates to 10% and decimated the NZ economy. Wrecked the entire building industry, decimated 61 finance companies with a loss of $6 billion in investor funds and forced a long and deep recession on previously a strong and booming NZ economy.

LikeLike