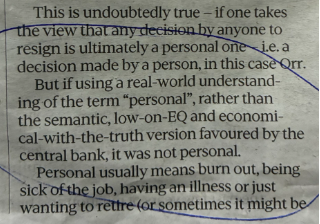

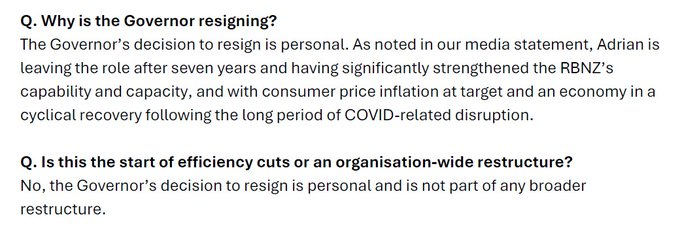

There are still lots of outstanding questions around the sudden departure of the Reserve Bank Governor, and the handling of those events by the board and the Minister. But, even amid ongoing OIA obstructionism – the Bank simply ignoring the substance of specific requests, in a flagrantly illegal way – some more bits and pieces have emerged.

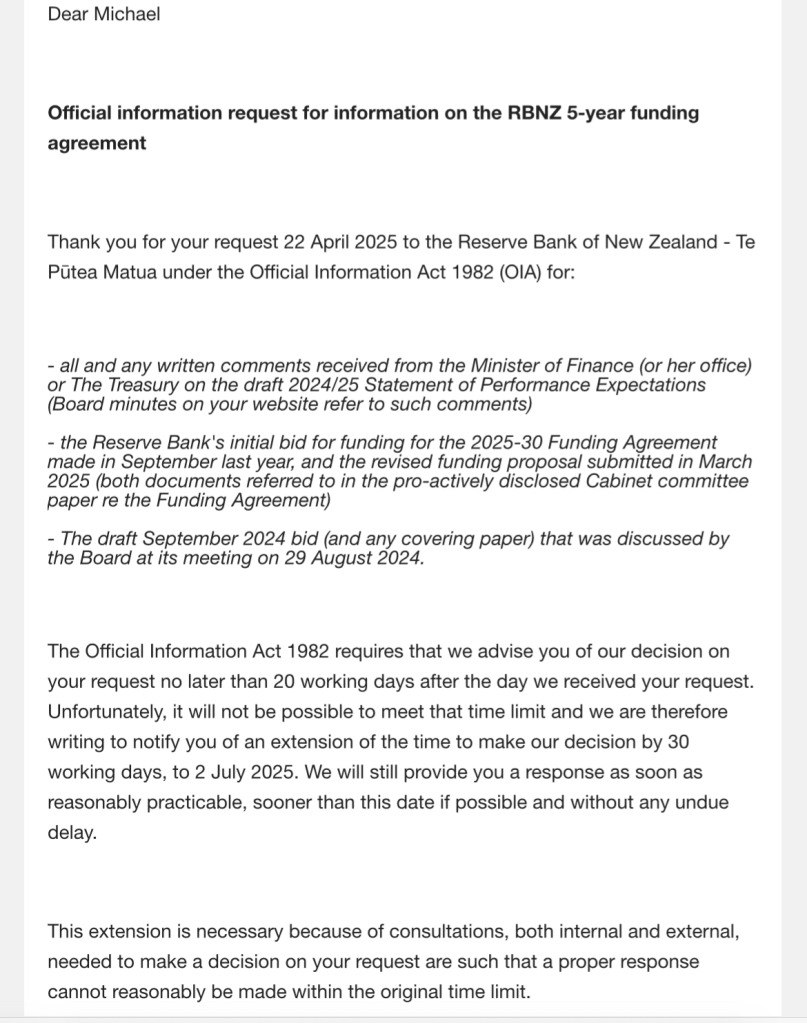

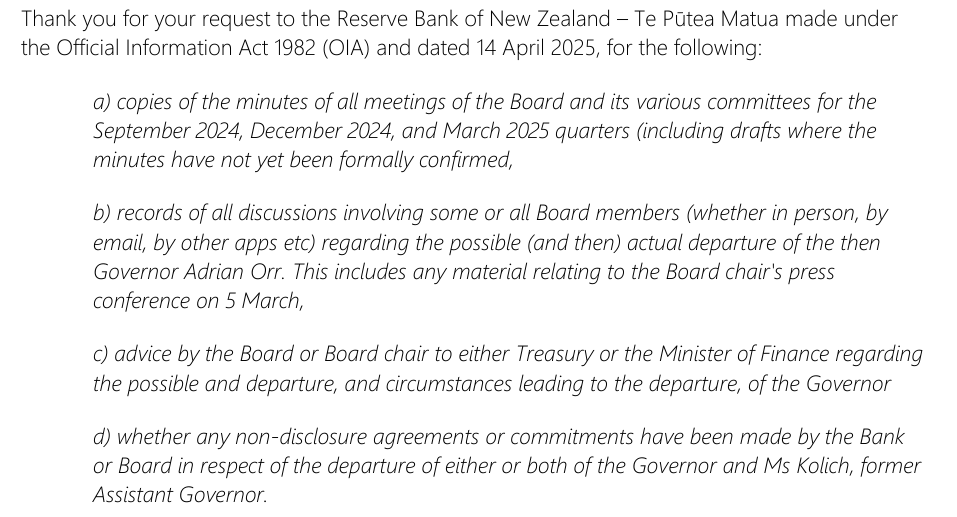

Back in April I lodged these requests

The Bank finally got round to responding on 30 June.

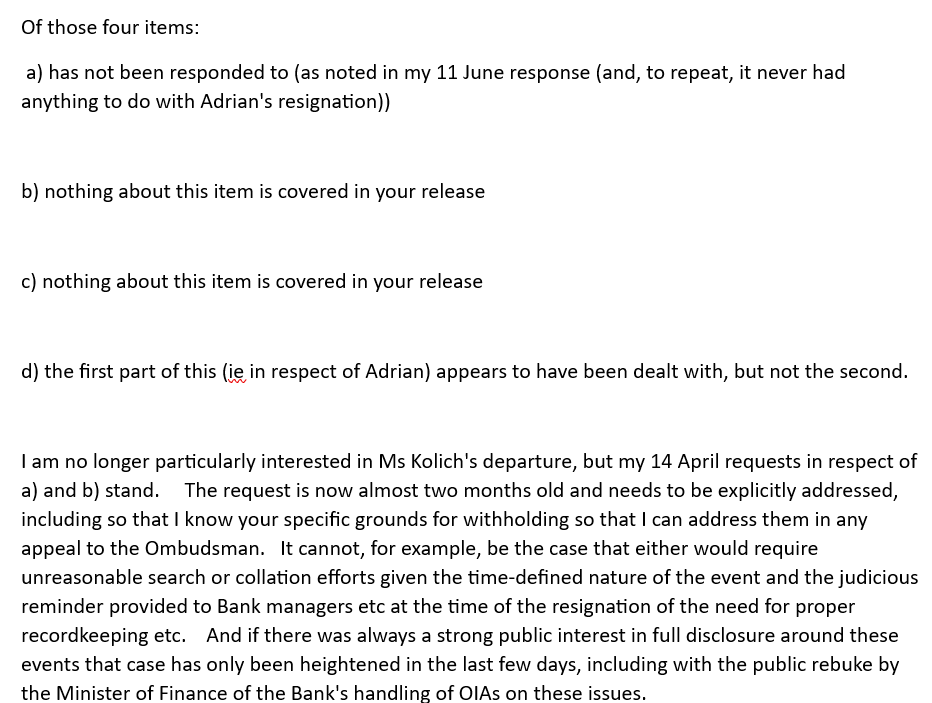

Of those, item a) wasn’t primarily about Orr’s departure (for unrelated reasons I wanted to see how their board committees work). Nonetheless, the response was interesting because although they sent me the committee minutes (with redactions), they didn’t even address the request for the minutes of actual Board meetings. As it happens, the Bank periodically (normally quarterly) releases rather limited and selective minutes of regularly scheduled Board meetings (you can find them here) and I’d lodged the request mostly because by 14 April they hadn’t released any for six months). They’ve since put up more recent ones. The Bank’s usual approach when someone requests something that is already on a website by the time the reply goes out is to point requesters to a link to those documents and then decline the specific request because the document is already publicly available (legitimate grounds for denial). This time, however, there is no mention in the response of the board minutes at all (only a mention that the committee minutes were attached, as they were).

This suggests an (illegal) effort to avoid addressing the specific request. One possible reason might be because it is almost certain that there will have been short-notice board meetings in and immediately around Orr’s resignation, which they don’t want to either acknowledge or disclose the records of. How could it have been otherwise? The Governor tells the board chair he’s thinking of resigning, and the Board does nothing, never meets, never authorises an exit package with gag agreements? Even for an apparently supine board like that of the Reserve Bank it seems very very unlikely. And when the Governor actually resigns – recall it was brought forward at the last minute by several days – there is no short notice Zoom board meeting to discuss what next? Yeah, right. (I’ll come back later to some interesting points in the minutes of the scheduled board meetings).

Another reason to believe that might be the explanation is the Bank’s response to my second item (above). This was it

That is a reference to the belated bulk release (available here), apparently designed to shape how we should think about Orr’s departure. But…..that response to my request by the Bank simply does not address my specific request, because the 11 June release contained precisely nothing about discussions among board members and nothing about the chair’s press conference later on the afternoon of Orr’s resignation (and nothing about any short-notice board meetings). Of course there will have been discussion among board members, and there might be even be some OIA grounds to withhold some of that specifically (in which cases such withholding needs to be justified specifically, item by item), but this response seeks to pretend answers have been provided when in fact the whole issue has been avoided.

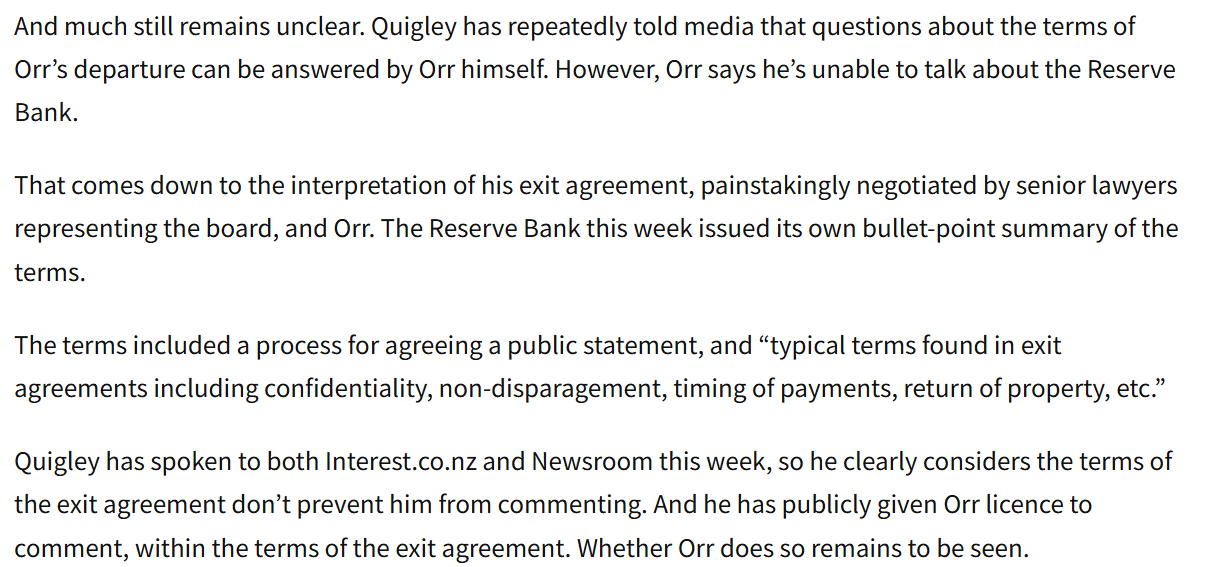

Item d) of my request was overtaken by events. I was no longer particularly interested in Kolich’s departure (and the 11 June release suggested it was in train before Orr left), and the 11 June release did tell us there was an NDA with Orr (although we still have no idea what the nature of the gagging provisions were, or why they were imposed or accepted by the Board, or the Minister – you’ll recall from previous posts that a Governor’s resignation is addressed to the Minister not the Board).

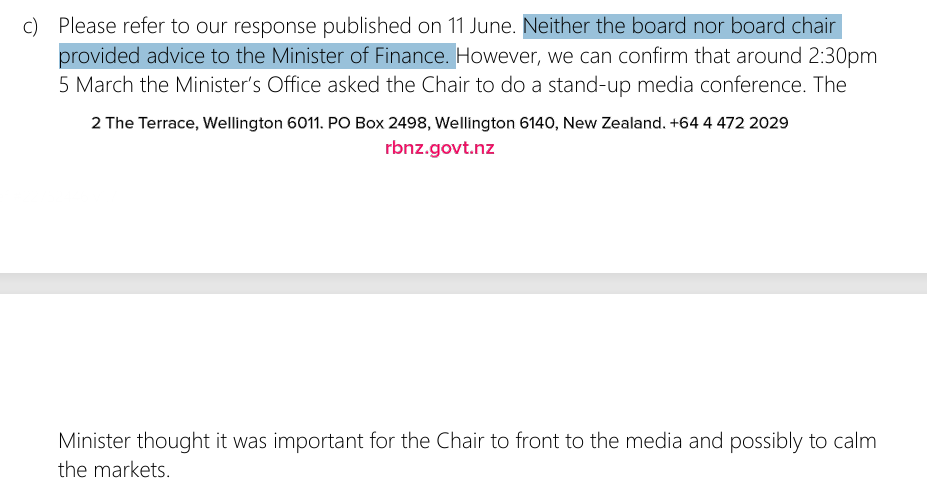

But then there was item c) (above). There is a typo in the request, but the Bank seems to have understood it as intended (about possible and actual departure). This was their response

It is quite extraordinary really. Things had run so far off the rails that the Governor was first talking of resigning then actually planning to resign – partly, the 11 June release tells us, because effective future working relations were so impaired, in the context of the funding agreement disagreements – and neither the Board nor the Board chair initiated any (direct) contact with the Minister of Finance at all; no meetings, no texts, no calls, no written advice, no nothing. If true, and I guess we must assume it is so, it is extraordinary, and something of a dereliction of duty, given that the Board governs the Bank, monitors the Governor etc all on behalf of the Minister, who not only has general responsibility for the Bank but specific responsibility for hiring, firing, and (in this case) receiving a Governor’s resignation. (Other releases show that Quigley had alerted Iain Rennie to what was going on, who’d mentioned it to the Minister). I usually word such requests quite carefully to specifically include “or the minister’s office” and failed to do so this time. I guess it is possible they are hiding behind that and there was contact by Quigley and the Board with senior advisers to the Minister, but on this occasion I doubt that is so because of the final two sentences in that response. It was nice of them to tell me about that but since it was from the Minister, conveyed via her office, it wasn’t specifically within the scope of my request (but one is left wondering why it wasn’t disclosed in the 11 June release).

It just seems astonishing. And not least because of how the Board just seems to assume the freedom to negotiate gag orders with Orr, when a) his resignation had to be made to the Minister not to them, and b) when there would inevitably be intense public questioning and scrutiny of what was going on, and they were proposing even to tie the Minister’s hand without consulting her.

And then the only contact is the ill-judged (as it turned out) request from the Minister’s office for the Board chair to do a press conference. I don’t disagree that both the Board chair and the Minister owed us answers (which we still don’t have) but Quigley is singularly bad at fronting when dealing with challenging questions, and his responses in that press conference ended up raising more questions than answers, at times apparently actively misleading journalists and the public, all while there were no evident market ructions to calm. More questions for the Minister I guess: does she even now know the terms of the gagging agreements entered into? If not, why not? If so, how and why does she defend or justify them?

I noted earlier that the March quarter Board minutes (released on 18 June, conveniently after the 11 June release) had some interesting content (and some telling omissions).

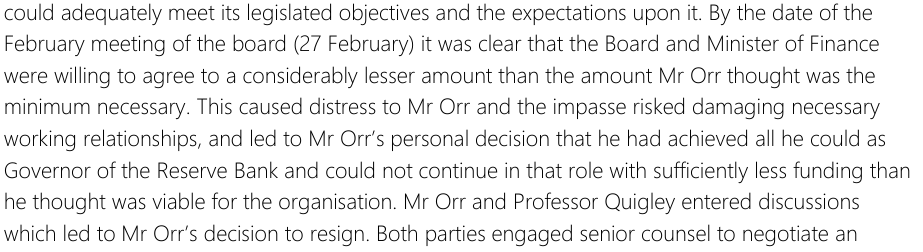

There were records of two meetings. The first was on 27 February (which reports the Board approved minutes of a 14 February special meeting, minutes of which – not disclosed – were clearly within scope of my request). This was the meeting – we were told in the 11 June release – where things crystallised

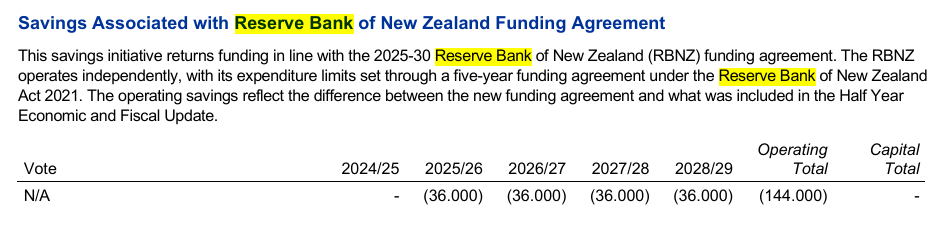

with the Board taking one view on the future Funding Agreement (bowing to reality) and the Governor refusing to do so. You have to imagine there was quite an extensive and tense discussion. But here is what the Board minutes have to say about discussion of the Funding Agreement and associated negotiations.

That’s right. Precisely nothing. And it is not as if some very sensitive material has been withheld on legitimate OIA grounds (hard to see what now that so much is a) finalised and b) in the public domain). It is just that there is no mention of the Funding Agreement in the 10 pages of minutes of a seven hour meeting.

It is extremely dubious, because it appears like an active effort to mislead readers (of these proactively released documents) and, unless there are secret shadow minutes, a breach of the Public Records Act, which requires public agencies to maintain proper records, including of such consequential meetings and discussions. It seems likely that much of the discussion will have occurred in item 6.2 “Board Only Time”, where nothing is disclosed (or withheld), although even then how plausible is it that all the discussion of the Funding Agreement, where there were major differences, occurred without any other senior management present (CFO or that person’s boss, or the Deputy Governor)? It really is a classic example of minutes theatre: it is good that the Board releases proactively what they do, but this example illustrates again just how selective (and thus dishonest) their approach is.

The next meeting for which they published minutes was on 27 March, three weeks after Orr had resigned. This time there is a short note that “The Five Year Funding Agreement negotiations have neared completion”. On this occasion there were quite a few interesting snippets.

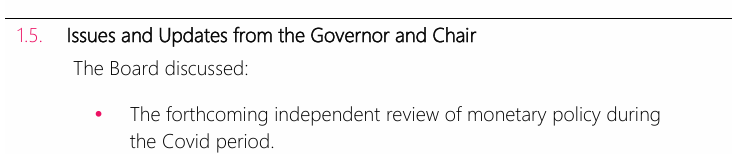

The first was this

This one took me quite by surprise. When in Opposition, Willis used to promise an independent review pretty much as soon as she took office. Nothing had been heard of it since they did take office. Nothing else has found its way into the public domain since 27 March. What review then? Who will be conducting it? What will the terms of reference be? How does it fit with the Royal Commission which did a – poor, once-over-lightly, channelling officialdom – chapter on economic policy in its Stage 1 report? Who, if anyone, will be invited to submit? And (frankly) at this late date what really is the point – unless, I guess, it asks hard questions of Christian Hawkesby, assuming he has applied to be Governor, about his responsibility for the costly mistakes and bad calls (as deputy chief executive then responsible for macro and monetary policy). But I do hope some journalist with access to the Minister will ask about the review.

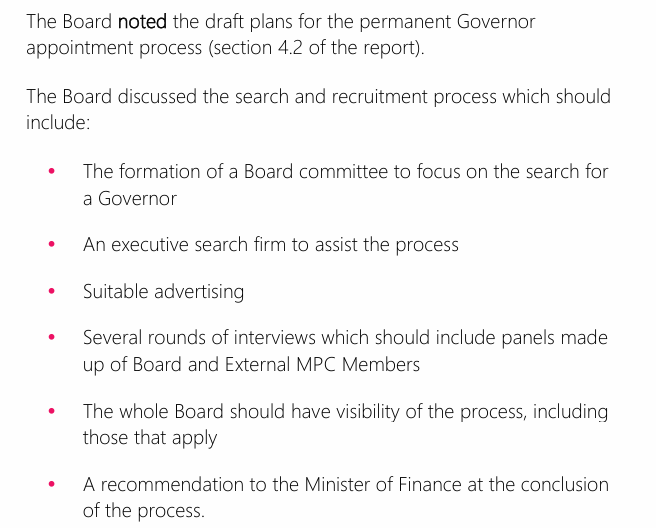

The second was more forward looking.

That sounds sensible enough, even if it remains egregious that Neil Quigley is driving the process, having been chair through the Orr years, policy failures, culture of excess, messy departure of the CE and all. But for some, still inexplicable, reason that appears not to bother the Minister.

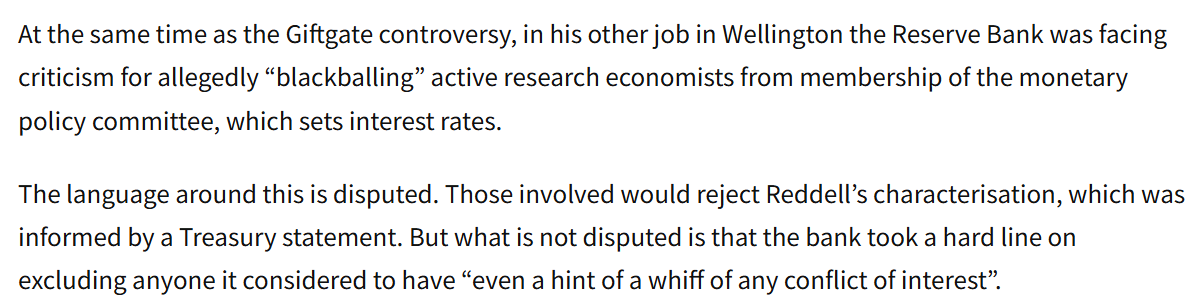

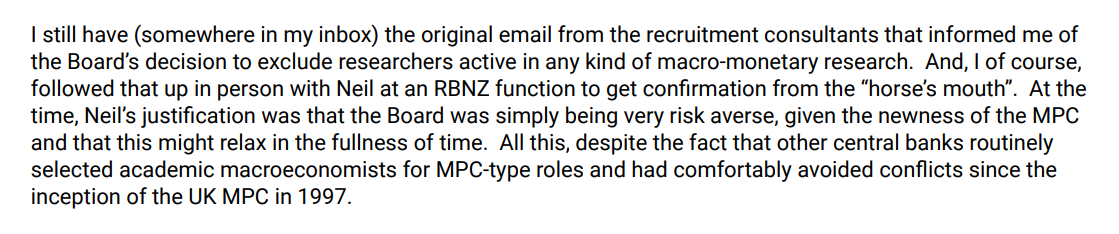

One of my big concerns about the new governance structure created by the 2021 Act has been that the Board had major responsibilities around the appointment of MPC members, including the Governor, but members had little or no expertise or background to making those calls (including reviewing performance on monetary policy matters, something they are also charged with). Two things partly allay those concerns. The first is the appointment of a couple of new board members with an economics background: Professor Philip Vermeulen and the former Deputy Governor and chief economist Grant Spencer. And the second, at least in principle, is involving external MPC members in the interview process. I say “in principle” because of the three externals, one is 80 and coming to the end of six years on the MPC where he shares responsibility for the very costly mistakes and is not on record as having made any distinctive contribution, and another – Prasanna Gai – is thought in some circles to be interested in becoming Governor himself. It does rather narrow the value of such an external panel.

Note, however, that one of Bank’s main roles is bank (and related) supervision and regulation. The Bank’s policies there have been quite contentious – including apparently with the Minister – and yet there is no one on the board with a strong banking or banking regulation background other than Spencer, and he tended to be a status quo figure in his last decade in the Bank when responsible for those functions. It just isn’t obvious where the intellectual vigour and fresh perspectives will be coming from (and it is interesting that, contrary to the practice for many top public sector jobs these days, there is no suggestion of having a respected outsider or two on an interview panel).

It is difficult to be optimistic about the process. There are no obvious ideal candidates, and the Board remains led by the same chair who gave us Orr in the first place, appointed and reappointed. But……fingers crossed I guess.