Take a scenario, just as a thought experiment for now.

A new government gets elected, amid a lot of rhetoric about excessive increases in government spending and public service numbers. They pretty quickly move to require government departments – typically funded by Parliament through annual appropriations – to cut their spending. Typically these agencies were being expected to make cuts of 6.5 per cent or 7.5 per cent.

You are part of the governance structure – Board member, CEO, perhaps other top tier managers – of a powerful public agency, one that doesn’t really do “frontline services” types of stuff, but also one that isn’t directly funded by Parliament. Instead, by law every few years your agency agrees with the Minister of Finance how much you can spend for each of the following few years. When the government changes there is still a little more than 18 months to run on your latest agreement – itself in fact a variation agreement made just a few months earlier, just before the election, that had substantially increased how much your agency could spend over the remainder of the agreement period.

How would you react in such a situation? (How do you like to think you would have reacted?)

One other big agency in New Zealand, not directly funded by Parliament either and not directly subject to the new government’s savings target, early on decided that they really needed to move with the spirit of the new environment. They (Board and CE presumably) adopted a 6.5 per cent cut themselves, telling the media that while they weren’t within the formal government plans “there’s a very clear expectation that we’ll make material cost saving”.

It is the sort of way I hope I’d have behaved had I been in their shoes.

Of course, there is another approach. After all, under the law governing this agency, they get to set their own annual budget. Remember that there is an agreement with the Minister, but actually there is nothing in law that forces them to actually spend in line with that agreement, and no direct consequences if they fail to do so.

So, another possibility, knowing that your agreement has 18 months or so to run, is simply to ramp up your organisation’s budget for the final year of that old agreement – perhaps to levels well above what is approved in the agreement – and then when it comes time to negotiate with the Minister of Finance on spending levels for the following five years, you simply offer up a 7.5 per cent saving from the hugely increased budget you yourself had set just a couple of months previously (all while shuffling a few more costs into the out-of-scope category to reduce even further the extent of the proposed “savings”).

And that, readers, is the story of what Adrian Orr, Neil Quigley, and the Reserve Bank’s Board did. It was simply extraordinary. Quite shameless really. Longstanding readers will know I have not been a fan of the Orr/Quigley stewardship of the Bank but…..I wouldn’t have guessed, without seeing it in writing, that their approach would be quite so openly shameless.

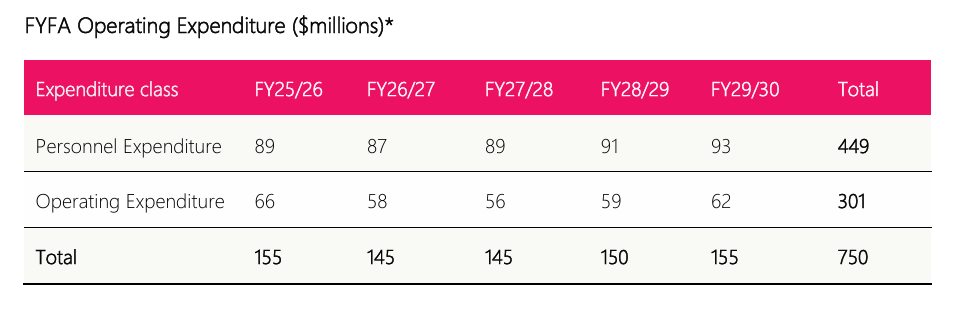

I wrote about the Bank’s new Funding Agreement quite a bit last month. The final and most comprehensive post was here. There are still lots of unanswered questions, but in early May – just before I headed off to PNG – the Bank released on its website a redacted version of the initial bid they had put in to Treasury, as adviser to the Minister of Finance, in September 2024 (NB: Thanks to the RB comms person who got in touch to draw my attention to this document.) This was the bid for $1 billion or so ($981 million opex and $50 million capex, both over five years), for things that would be covered by the Funding Agreement (quite a lot wouldn’t). I only got back to reading it this week.

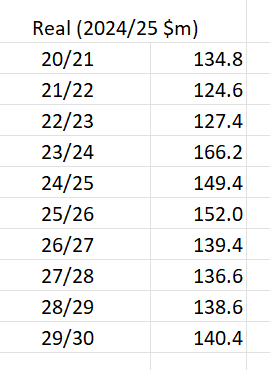

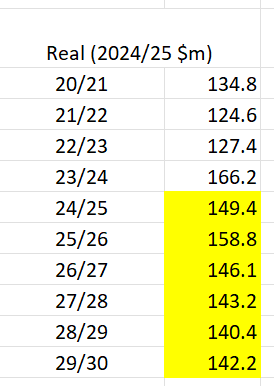

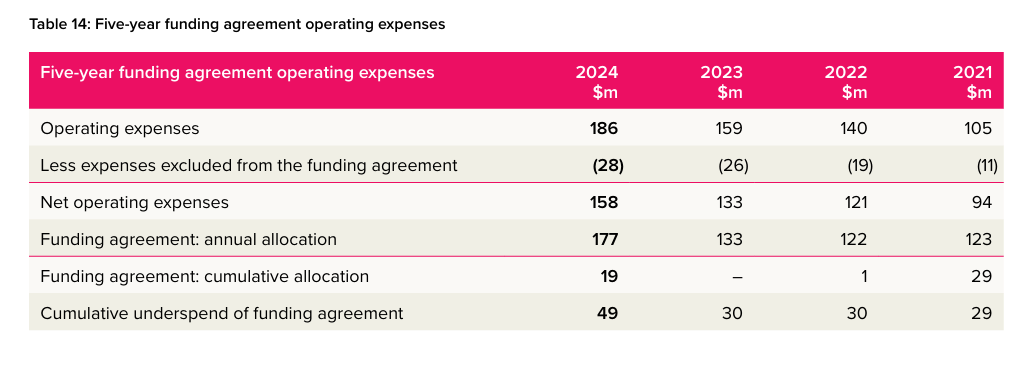

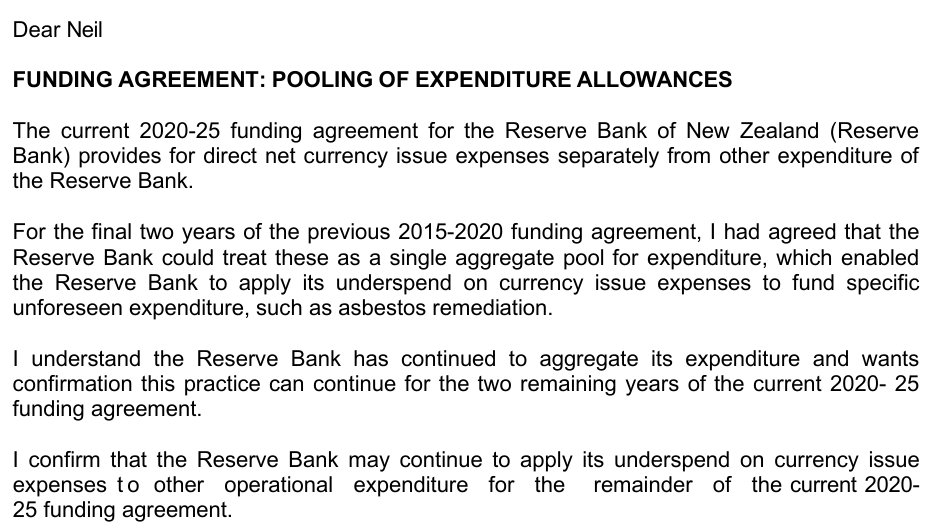

To recap, in September 2023 Grant Robertson had agreed to a (further) increase in the Bank’s Funding Agreement spending for the last two years of the 2020-2025 agreement. For the year to 30 June 2025, the amount of core operational spending Robertson had approved was $149.44 million. In that previous funding agreement there was also a separate line item for direct currency issue expenses and Robertson agreed that if they underspent that they could use the balance for general operating expenses. That gave them perhaps another $5 million.

So as the Bank’s Board and management approached the setting of the 2024/25 Budget those were the parameters they were supposed to be working within. But they also had information from the Minister of Finance about future intentions. On 3 April she had sent the Board her annual Letter of Expectation, which contained these points

In the general

And the specific

A responsible Board member would surely then have read the times and concluded that (a) they really needed to ensure that the 2024/25 Budget was, at worst, no higher than what Grant Robertson had allowed (bearing in mind that most agencies were getting those 6.5 to 7.5 per cuts even in 2024/25) and b) that any bids for the new 2025-30 Funding Agreement should be kept no higher (whether in real or nominal terms) than the 2024/25 approved level of spending. The focus was clearly intended to be reprioritisation, not further increases (in an organisation whose operating spending and staff numbers had already increased massively in recent years).

That is what a responsible Board member, looking to the public interest etc, would have done.

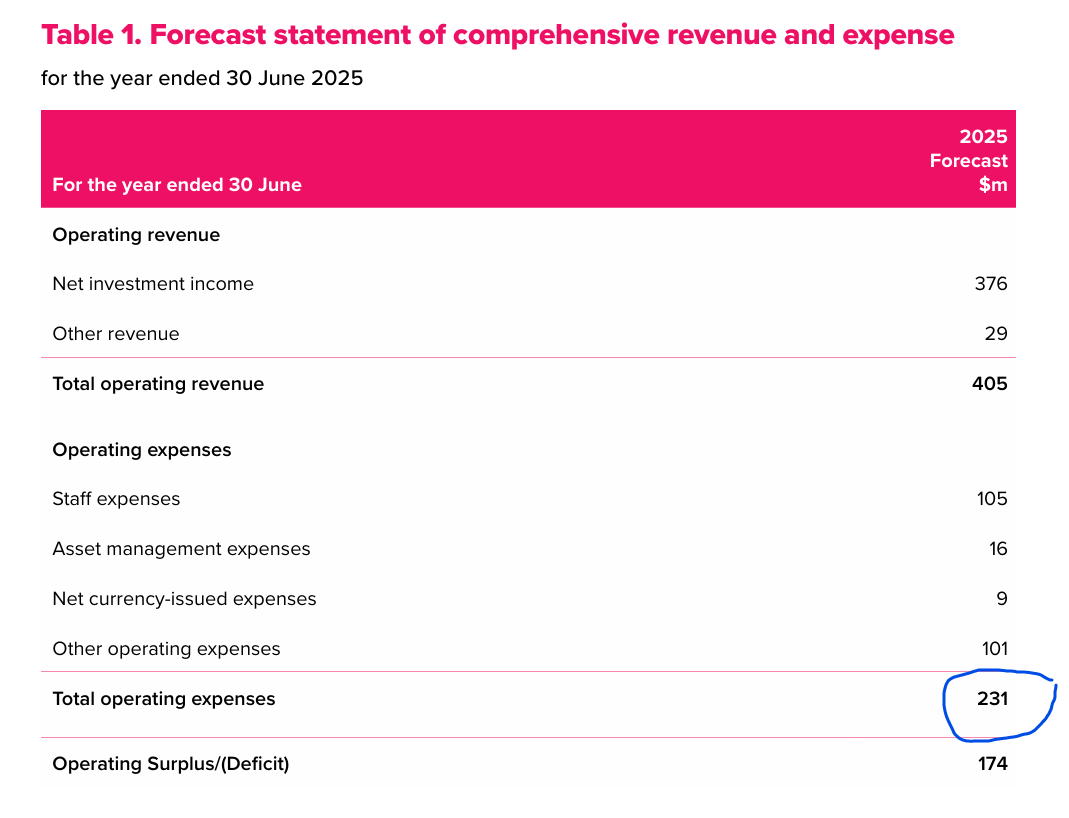

It wasn’t what the actual Board and senior management did. Instead, they adopted and published a budget for operating spending (captured by the Funding Agreement) of $191 million for 2024/25. Recall the spending that Grant Robertson – Mr Big Spender himself as Minister of Finance – had allowed the Bank for 24/25: $149.44m plus (on their budget) $5.5m from the underspend of their direct currency expenses allowance. The approved budget for 24/25, on items covered by the Funding Agreement, was 23 per cent in excess of what Robertson had allowed them, having already had those counsels of restraint from the Minister of Finance in her April letter. (As I noted in earlier post, there are mysteries around whether the Minister raised any objection at the time – she had to be consulted – which maybe an outstanding OIA will shed some light on, but that isn’t the focus of this post.)

That Budget was approved in June 2024 and in late August the Board approved the Funding Agreement bid (note that the current “temporary Governor” while not then a full Board member himself was in attendance throughout the relevant Board meeting). It was sent off to the acting Secretary to the Treasury, signed by both Orr and Quigley, on 13 September. And here from the second page of the covering letter (with a 40+ page document) was how their bid was sold, in blaring headline

In the body of the document it is repeated: “this approach would achieve savings of 7.5 per cent from our baseline operating expenditure, as requested by the Minister of Finance” [a footnote here refers the reader to the 3 April Letter of Expectation].

Ramp up the budget to 23 per cent above (previous Minister’s) authorised levels…..and then graciously offer a 7.5 per cent “cut” from that level. Really quite breathtaking… In fact in the previous paragraph they carefully noted that they had “had regard” to the Minister’s stance in her Letter of Expectation. Read, thought about, and then ignored would seem a more accurate description, all while attempting to spin Treasury and the Minister of Finance (nowhere in the document do they claim, for example, that the previous Funding Agreement levels were inadequate and needed to be increased. They simply take their own budget as the starting point, claim to have heeded the Minister, and end up “offering” a level of spending well above (in real and nominal terms) what even Grant Robertson had approved.

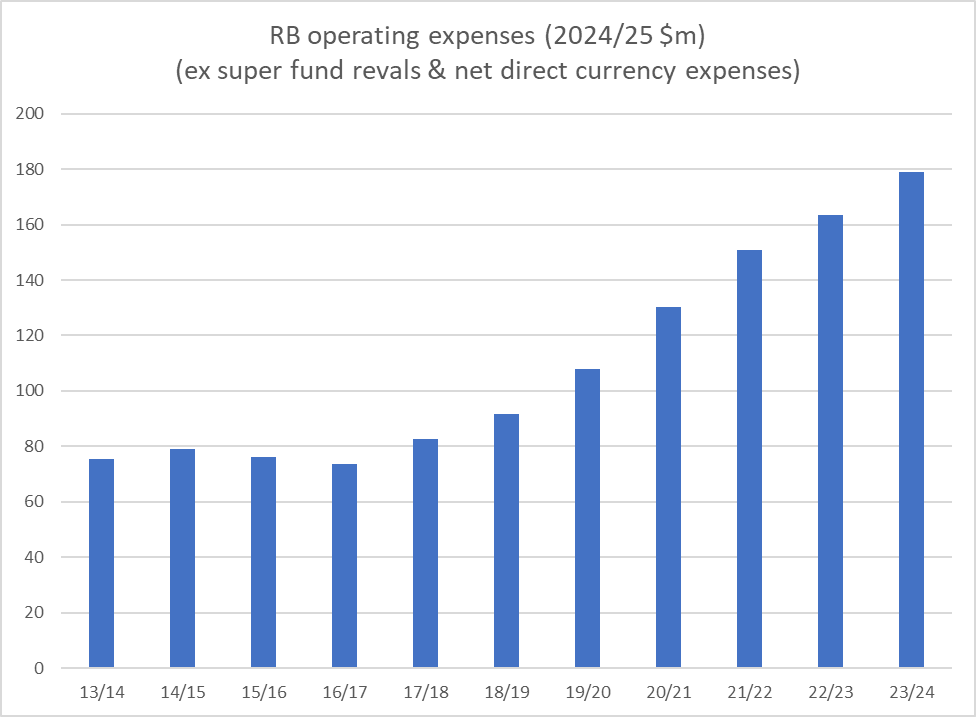

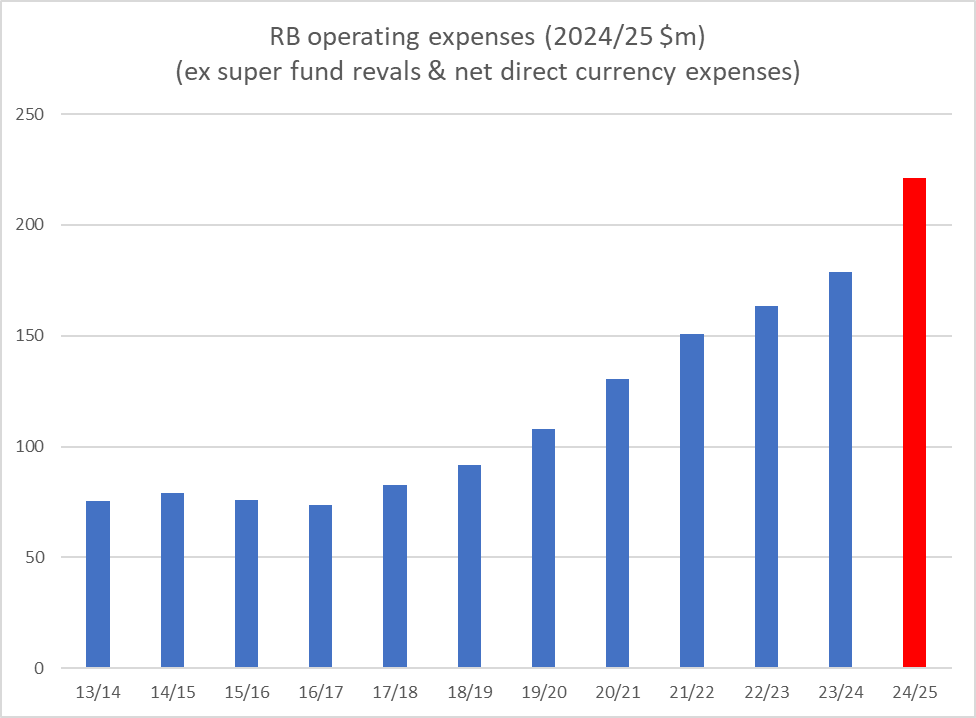

There is more sleight of hand when it comes to staff numbers. The government had seemed to be looking for agencies to be slimming staff numbers. In the year to June 2024 the Bank had increased staff numbers by 18 per cent (another 90 people), and in their Funding Agreement bid you get the sense that the “current headcount” was, in their view, roughly adequate for the things they had to do. And in fact later in the document they suggest that their preferred option would involve a net headcount reduction of 19 people. But what they didn’t point out to Treasury (or thus to the Minister) is that at the very same time they were handwaving about potential savings, they were going hell-for-leather to further increase staff numbers. We know this because the paper the Minister of Finance finally took to Cabinet in March tells us that the Bank increased staff numbers from the 601 at the end of June 2024 to 660 (FTE) by the end of January 2025. So they had no intention of actually cutting staff numbers, just of slightly slowing the rapid further increase they were already recruiting for. Now, sure, acute readers must have realised that such a huge operating budget increase in 2024/25 must have involved further increases in staff numbers, but….they were left to work it out for themselves. In a political and public spending climate in which Orr and Quigley and all the rest of them were only too well aware of sensitivities around rising staff numbers.

It is all pretty disreputable, shabby, and borderline dishonest (I didn’t spot an actual verifiable lie in the document; it was all in the self-serving misleading framing). Among the ongoing mysteries is why, when Treasury received this bid, they didn’t take a quick look and send it straight back with a demand that the Board revise the starting point back to (say) the previously approved (by Robertson) level of opex, not the Board’s own inflated budget which bore no relation to what the previous Minister of Finance had approved them spending. It wasn’t until March this year, after Orr’s departure, that there was finally a revised (much lower) submission.

And although the Orr/Quigley initial submission had strongly suggested that the Bank needed every one of the proposed billion dollars to function, reality seems to disagree. Just a couple of weeks ago the “temporary Governor” completed a restructuring of his top tier, in which the number of (very expensive) roles was reduced from about nine to four. Not hard to economise when you try (when the Minister’s choices finally compelled it). The Governor has gone of course (he’ll eventually be replaced), as have Assistant Governors Smith (finance), Kolich (data), Robbers (strategy, governance, and sustainability), Strategic Adviser Prince, and the grapevine reports that another of the Orr hires, Assistant Governor Owen (risk and legal) has also resigned. It is really only a start, since Board chair Neil Quigley and all the board members who approved and endorsed this egregious funding bid are still there (although the terms of two expire next month). And are we really to believe that all along the Deputy Governor, Hawkesby, hadn’t been endorsing the approach?

And then, of course, there is the lack of transparency. In that Funding Agreement bid they explicitly told Treasury that once a new agreement was reached “our intent is to publish the final version of our Funding Proposal on our website”. Which sounds quite good, but…. the new Funding Agreement was published on 16 April. It is now 20 May, and although they have published a redacted version of the first proposal (which is a start) there is no sign of the final revised March bid. In fact, I have an OIA request in for it

Just yesterday I heard back from the Bank

Of these:

- the first relates to the question of whether the Minister ever pushed back on the proposed 24/25 budget

- the second covers two specific and easily identified documents (the first now released – see above), and

- the third is to shed light on whether the Board pushed back at all on what management was proposing (is the final version different in any material extent to what went to Treasury.

None of these documents will take any particular effort to find, and at least one they promised Treasury nine months ago they’d publish. But…..in the way of public sector obstructionism, they’ve just taken another six weeks to respond to a fairly straightforward request. Isn’t that convenient for them.

It really is staggering that a government-appointed Board chair could try it on quite as egregiously as Quigley did (in league with Orr) and still hold his very well-paid role ($200000 for a part-time role), including leading the process of selecting a nominee to be the next Governor.