It was one too many mentions of Equatorial Guinea that prompted me to pull together this very quick follow-up to my post yesterday showing some snippets from the newly-released IMF WEO.

For my tastes, these comparisons of forecast growth in real GDP per capita for New Zealand and the group of advanced countries are most useful and enlightening

But it was easy enough to download the data for both GDP and GDP per capita (both in constant price – “real” – terms) for all the countries and territories in the Fund’s database (roughly 190 of them, depending on the precise variable and year). I did it for both variables and for the three years, 2022, 2023, and 2024. The forecasts are annual not quarterly, so (for example) the growth rate for 2023 is GDP generated in the whole of this year relative to that in the whole of last year.

Take real GDP growth first:

In 2022, New Zealand is shown as having 2.2 per cent growth. That put us 130th of 192 countries (in case you are wondering, and to no one’s surprise surely, Ukraine did worst).

In 2023, the Fund expects real GDP growth here of 1.1 per cent. That would put us 152nd of 190 countries (Sudan doing worst).

In 2024 – and for these forecasts the Fund basically assumes constant policy – the Fund forecasts that New Zealand’s real GDP growth will be 1.0 per cent, 180th of 190 countries (and here Equatorial Guinea really is last).

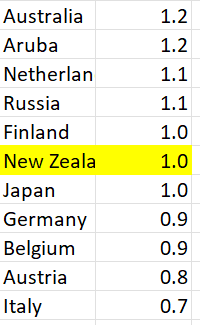

As context, here are the five countries either side of New Zealand for 2024

But headline GDP isn’t even close to a measure of economic wellbeing. Some countries have rising populations and some falling populations. New Zealand’s population has tended to rise faster than most advanced countries, particularly so right now. Real GDP per capita data/forecasts are typically more useful, as being a bit closer to the average experience of an individual in a country.

How does the IMF see New Zealand doing on that count?

In 2022 the IMF shows us as having had growth in real per capita GDP of 2.2 per cent, 98th of 192 countries/territories (Macao did worst)

In 2023 the IMF expects that New Zealand will have had real per capita GDP growth of -0.1 per cent, ranking us 156th of 190 countries (Timor-Leste did worst).

And in 2024 the IMF forecasts that New Zealand will have real per capita GDP growth of 0.0 per cent, ranking us 177th of 190 countries (and there Equatorial Guinea is projected to be worst).

Here are the five countries/territories either side of us this year (an eclectic mix it would be fair to say)

and here is the same snippet for the 2024 forecasts

To repeat, macroeconomic forecasters aren’t very good, and the IMF is no better than most of the others. But these are consistently compiled numbers, and for 2022 the numbers are reasonably firm and for 2023 almost three-quarters of the year had gone when the numbers were finalised.

The IMF released its latest World Economic Outlook and associated forecast tables overnight. There is no reason to think the IMF is any better as a forecaster than anyone else (ie not very good at all) but they do look at a bunch of advanced countries all at the same time, against a common global backdrop, so it is still worth looking at how they see things here relative to those other advanced countries. A few charts follow.

(Here, as in various recent posts, I remove from the IMF advanced countries Andorra and San Marino (as too small to matter) and Hong Kong, Macao, and Puerto Rico (as not countries at all), and add in Poland and Hungary, both of which are OECD member countries and performing similarly economically to various central and eastern European countries the IMF includes in their advanced country grouping. That leaves a group of 38 countries, including New Zealand.)

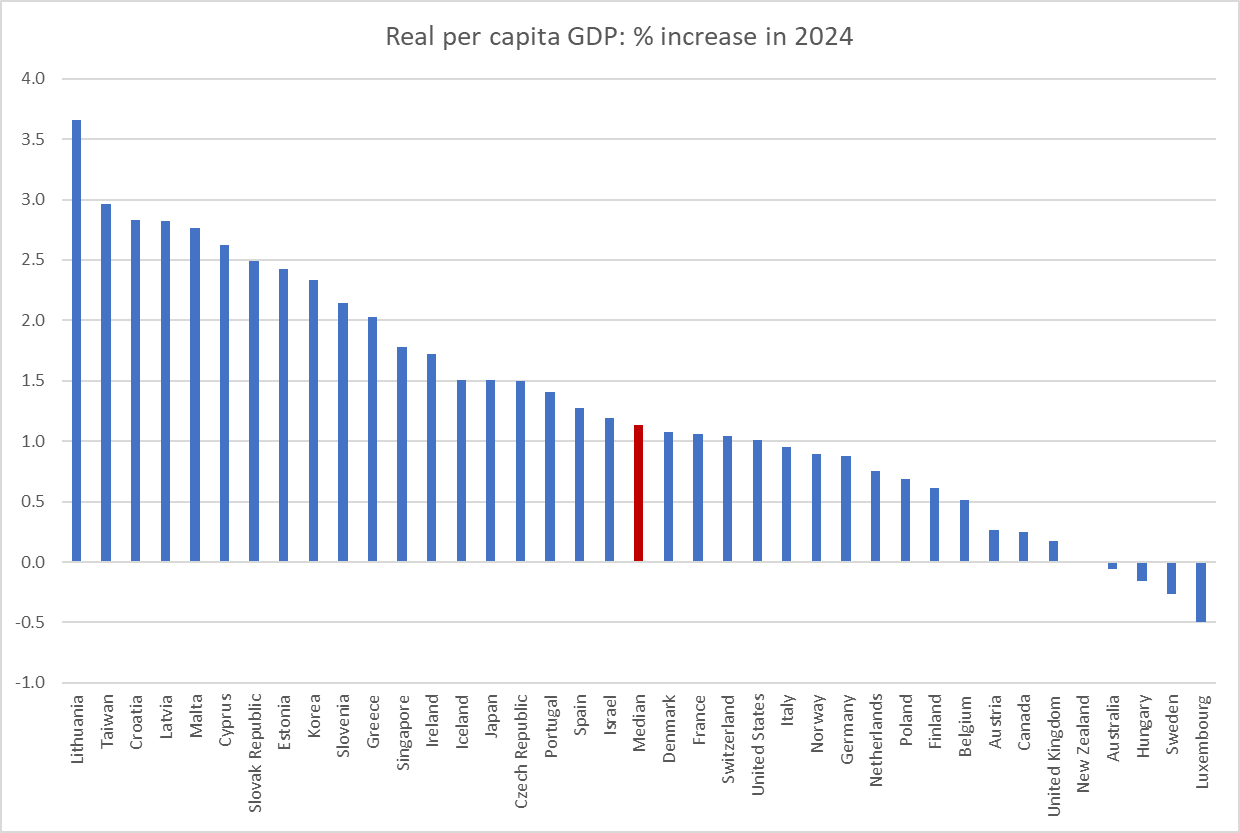

First, we look at the Fund’s forecasts for real per capita GDP growth.

In calendar 2023

and calendar 2024 (I can’t highlight New Zealand – zero growth – but we are fifth from the right)

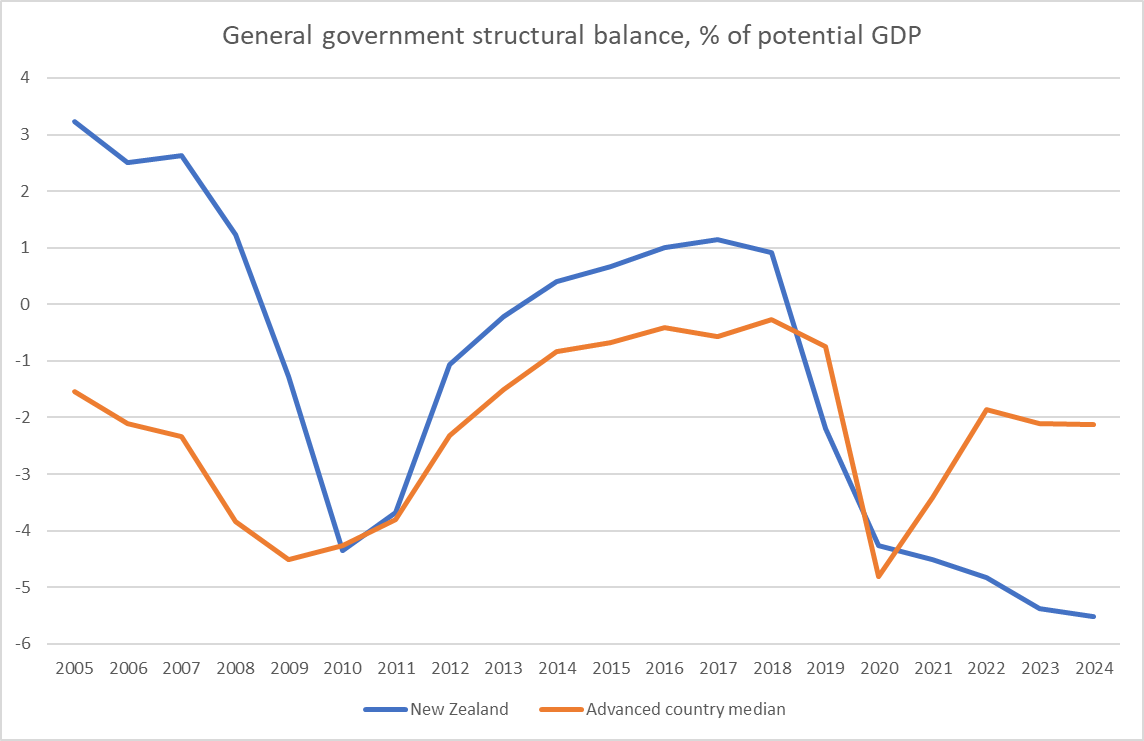

What about fiscal policy? The IMF has actuals and forecasts for the general government structural balance. We used to be better than most advanced countries. But that was then.

For calendar 2024 alone (for 2023 we are a couple of places less bad). These numbers seem very consistent with the IMF cyclically-adjusted primary deficit estimates in their recent Article IV review of New Zealand.

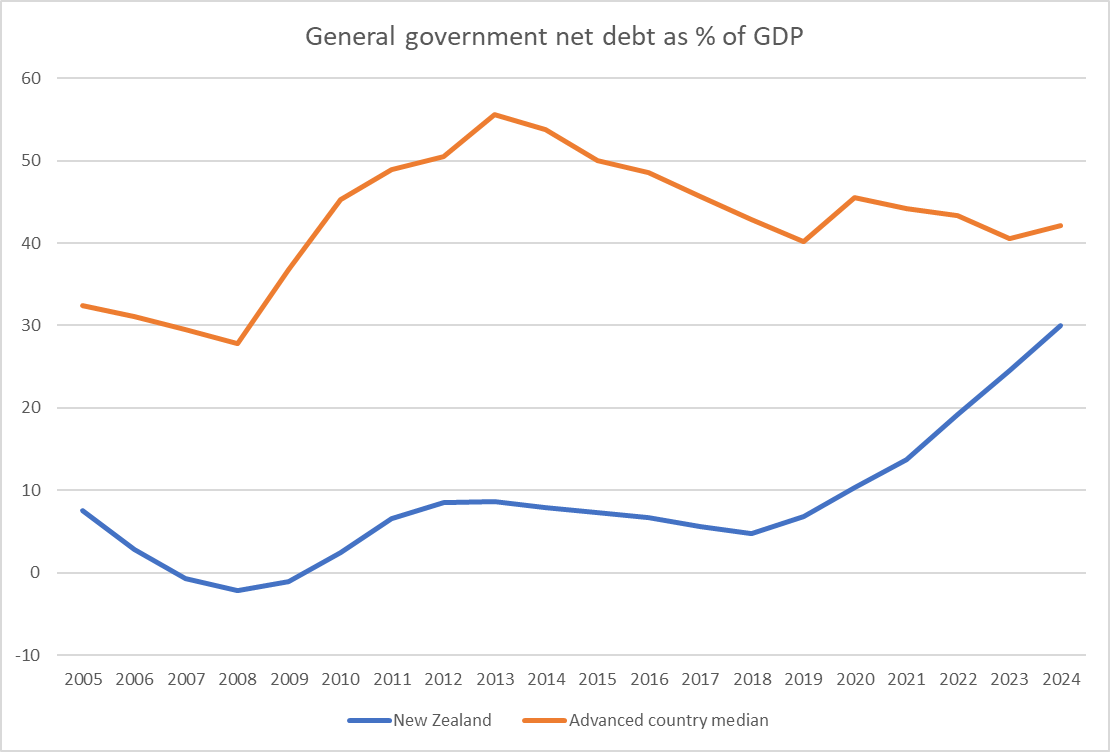

What of net general government debt?

We do still have government debt as a share of GDP less than the median advanced country, but that gap is closing fast. You’ve heard a lot in this election campaign about the pandemic: other countries had one too.

And what of the current account deficit? There is no right or wrong number for a current account deficit. Huge surpluses or huge deficits can both be symptoms of things going right or wrong. Context matters. In a country with rapid productivity growth and lots of business investment, catching up with the rest of world, really large deficits make sense. That was Singapore and South Korea in their earlier development phases, or 19th century New Zealand.

In 2023, New Zealand doesn’t have the largest deficit as a share of GDP, but it is close. (We had the third largest deficit last year and are still forecast to be second largest next year.)

All in all, it didn’t really make encouraging reading.

The topic may not be of much interest to core or regular readers of this blog, but this is about seeing an issue through to the end.

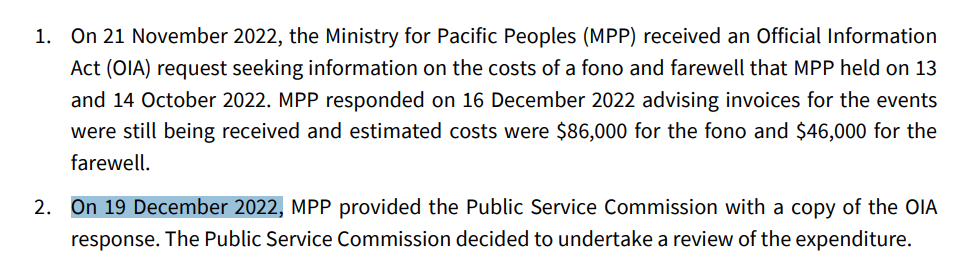

My post on Saturday highlighted how the Public Service Commission seems to keep just making stuff up in defence of (a) themselves, and (b) the Commissioner’s protege, Mr Leauanae formerly of the Ministry for Pacific Peoples and now CE of the Ministry for Culture and Heritage. They tell it the way it isn’t or wasn’t, but perhaps the way they would prefer it to have been. It is simply dishonest, and discredits the institution (and the government that is responsible for the Commission). Leauanae did not pay back money for months after he had inappropriately received benefits, and never took any pro-active steps, and PSC’s report did not criticise Leauanae for having recused himself from involvement in planning for his farewell, let alone call it out “clearly and strongly, and [..] on the public record”.

But yesterday I had another OIA response from PSC. I’d asked about all and any contact (written or otherwise) with ministers or their offices about the MPP/Leauanae affair. And it prompted me to stand back a little.

First, in case you were wondering about advice to ministers, this is the full response on that point.

In other words, over the eight months from start to finish of this investigation and review, into what was revealed to be grossly inappropriate spending in a public service department, including considerable personal benefit for a senior public servant, PSC never once provided anything in writing to the Minister for the Public Service (when the process started that was still Hipkins), or to any of the portfolio ministers of the departments Leauanae had been (MPP) or was (MCH) chief executive of. Had some journalists asked the Minister for the Public Service in, say, early January about this issue/investigation, we are to suppose he would not even have been aware of the matter. Doesn’t seem very much in line with “no surprises”.

There was also the question of when PSC was first aware. I’ve already noted how odd it was – or would be if PSC had been doing its job, and some culture of excess and entitlement had not apparently taken hold in parts of the public service – that PSC itself seemed not to know about any of this until (mid December) two months after the events and spending in question (last October). According to the PSC report released in August, things got underway this way.

Perhaps. But this latest release contains quite a bit of material from 21 December, starting with an email from a person whose entire email address is blacked out to four people with parliament.govt.nz email addresses (almost certainly people in one or more ministerial office, including that of the Minister for Pacific Peoples), but including Christina Connolly, the private secretary in the office of the Minister for the Public Service. Here is the relevant page from the release (there is a whole other paragraph withheld from that final email). Connolly sends it on to one of the PSC Deputy Commissioners, one responsible for communications and public affairs.

Mr Sio, then Minister for Pacific Peoples, is on record – his ministerial diary – as having attended and spoken at this lavish farewell, but it is apparently only two months later, confronted with the actual numbers (of the expenditure), that his staff appear to think there might perhaps be a bit of an issue. And there is no sign at this point that the PSC secondee in the Minister for the Public Service’s office is even aware there is an issue. It wasn’t perhaps an ideal day for some of this to come to light, as it was the day PSC had announced the appointment of a new head of MPP.

Anyway, whatever PSC knew by then, they first seemed to think that some public statement might be in order. Because there are several emails about a proposed “Statement from Public Service Commissioner Peter Hughes” in which it was intended to indicate that the spending had come to his attention and “I have decided to look into this matter to understand the extent to which that guidance was adhered to”. This work was to be completed by February 2023 (ie in fairly short order, given that this was being discussed on 21 December). For whatever reason, that statement was never issued and the wider public wasn’t aware there even was an issue until the final report finally came out in August,

The next document is from 7 June: an email from the PSC Deputy Commissioner to the secondee in the Minister’s office, advising that PSC is envisaging releasing their final report the following week (and providing a bullet point summary of what was known to them then).

We don’t know why this investigation took months longer than PSC had initially envisaged. But we’ve known for a while that up to this point (early June) PSC knew nothing at all about the inappropriate spending (by MPP) on Leauanae’s family members’ travel to his welcome ceremony at MCH. Something of that must have come to light in the days after 7 June, and the enquiry is then reopened and is only finally published in August (Leauanae – who simply has to have known all along that this was inappropriate spending for personal benefit – having very belatedly paid that money back by then). There is no way it would not have come to light earlier if either MPP or Leauanae himself had been at all proactive, and inclined to bend over backwards to think about anything that might have been raising questions re these events in October last year.

The final document in the bundle is an email from 4 August, shortly before the report is finally released, to the secondee in the office of the Minister for the Public Service asking her to pass the final material along to the offices of Edmonds (now Minister for Pacific Peoples) and Sepuloni (primarily responsible for MCH). But just as one ministerial services staffer to others. Nothing at all from the Commissioner to these ministers.

No one emerges well from this affair:

Not the Public Service Commission (or Commissioner) as regards the original matter and investigation itself. How did a department they oversee come to exemplify such a culture of excess in the first place? How did the (bloated) Commission have no idea of the lavish farewell and gifts for two months after the event, apparently reliant entirely on a member of the public’s OIA which – after it had gone out – finally ended up on their desks. Why did the initial inquiry take six months, not the two initially envisaged, and why did they not ask sufficient questions that would have led them to the MCH-welcome travel expenditure until they had almost all wrapped up and were ready to publish. How did the Commissioner in his press release go beyond the facts and actively mislead the public about Mr Leauanae’s part in all this, particularly the speed (or otherwise, more to the point) with which the money was repaid?

Not the Ministry for Pacific Peoples which arranged the lavish event in the first place, in clear breach of public sector standards (the written ones, but who knows if they were the lived ones), and then must have been not overly cooperative and proactive in the PSC inquiry, or otherwise it would not have taken until June before PSC finally became aware of the spending on Leauanae’s family travel. Shouldn’t PSC have asked early on, and MPP proferred it early on even if PSC didn’t ask, about all expenditure on or for Mr Leauanae and/or his family in (say) the preceding six months. You cast the net wide to be sure of capturing everything relevant. Unless you don’t care greatly, want to protect your former boss, and just want to do the bare minimum.

Not the several relevant ministers of the Crown.As noted already, Mr Sio, the Minister for Pacific Peoples, had attended and spoken at the farewell. There is no evidence he raised concerns with either MPP or PSC. What sense of public expenditure restraint and appropriate spending on a public servant changing jobs did he have? Any at all? And there is no sign, at any point early or late, of any serious expressions of concern from Hipkins (then Minister for the Public Service) or Edmonds or Sepuloni, or Andrew Little (currently Minister for the Public Service).

Not Mr Leauanae, whose lists of faults and failings, revealing someone simply unfit to be a government department CEO, is long. In earlier posts, I’d noted that he could and should have ensured reimbursements to MPP within days of the event taking place, and should have immediately recognised how inappropriate his receipt of those benefits was. There is no evidence that he ever had that moment of recognition. A point that hadn’t occurred to me until I wrote my post on Saturday was that a slack but honourable CE (one whose subordinates – appointed by him- had badly stuffed up with this lavish and inappropriate expenditure) would have been on the phone to Peter Hughes the very next day, deeply embarrassed and apologetic, suggesting that an PSC investigation was probably warranted, pledging cooperation, and indicating that he had already taken steps to return the money and benefit he himself had inappropriately received. He did nothing of the sort, and the case against him is only strengthened by his failure even in March, when he returned the gifts and money he’d received at the farewell, to have drawn PSC’s attention to the spending on his family travel, or to have taken immediate steps even then (very belatedly) to have returned that money promptly. That he is still a government CE is a disgraceful reflection on the management of the public sector by Hughes and by the various relevant ministers.

And then finally, not the Public Service Commission (and the Commissioner) who have simply not been straight with the public even when their initial defence of their protege has been revealed to be threadbare. The lack of straightforward integrity is staggering.

A quick Google of “Public Service Commission values” brings up a list that includes this item among the list of things PSC say “are how New Zealand expects public servants to behave”

If walking that sort of talk meant anything you might suppose it would mean that when the Public Service Commissioner himself issued a press release it would be clear and straightforward, free of any intent or effect of misleading the press and public. And that if, perchance, the Commissioner once fell short of the high standard he himself had laid out then contrition and correction – with a dose of humility thrown in -would follow quickly.

Instead, we are dealing with Peter Hughes and the Hughes-led PSC.

Two months ago Peter Hughes released a report into the excessive and inappropriate spending by the Ministry for Pacific Peoples on the farewell to its outgoing chief executive as he moved down the road to head a bigger government department (MCH). The spending was lavish and inappropriate, something the report rightly (if belatedly) called out. But the second element of it all was the lavish taxpayer-funded gifts given to the outgoing CE, Mr Leauanae, and the spending by MPP of taxpayer money on travel for members of his family for his welcome to MCH. With the report there was a covering press release (the report document itself is linked to in the press release). In the press release in particular Hughes went out of his way to play down Leauanae’s culpability, with this culminating line

I thank Mr Leauanae for putting the matter right at the first opportunity

Except that Mr Leauanae did nothing of the sort. There had been no dates at all in the press release and none of the relevant ones were in the 11 page report either. Casual readers might reasonably have supposed it had all been sorted out within days, not months later.

But OIA requests finally got confirmation from PSC (and MPP) that despite this inappropriate spending having occurred in October last year, the money was not returned until March (in respect of the gifts) and July (in respect of the travel). And not from any belated sense of compunction on Mr Leauanae’s part. I wrote about this in a post a few weeks ago.

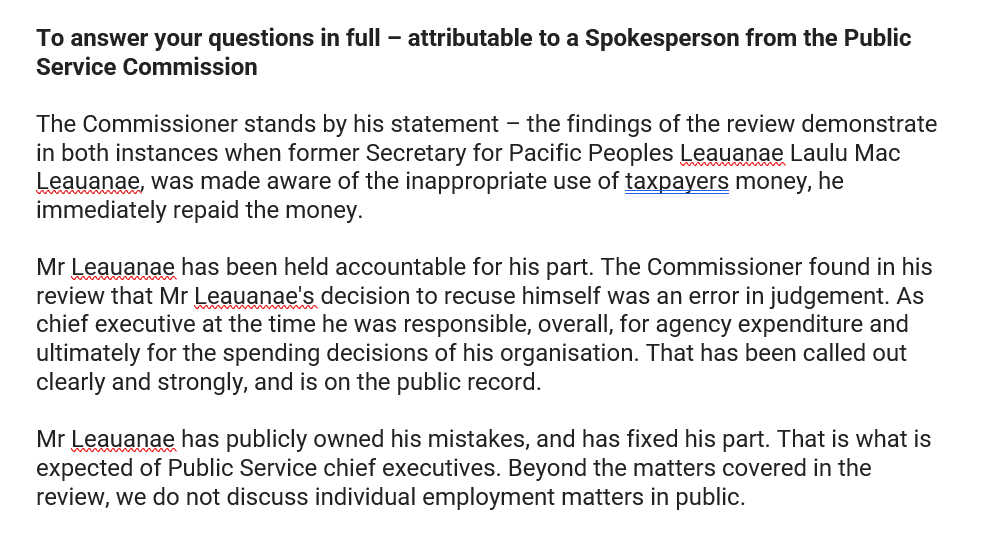

Which is by way of prelude to Andrea Vance’s article on the issue in The Post this morning. She had drawn on the OIAs and my post and had asked PSC some follow up questions, including asking why the Commissioner had said that the money had been paid back at the first opportunity when the documents – from PSC itself – had clearly shown otherwise. Vance was kind enough to share the statement from PSC with me. These are the relevant paragraphs

There are multiple problems with this.

Any public servant – notably any very senior public servant – would have known immediately that it was not appropriate to receive lavish farewell gifts (no matter what the mix of private and taxpayer funding) and even more so to have received public money from his previous employer to pay for travel for family for his welcome into a new role down the road. (He should also immediately have recognised that the lavish farewell itself was in breach of all public service standards and have immediately alerted Hughes to the mistake by his underlings (on his watch)). On timing from my previous post.

The PSC statements seem to rely entirely on the point that it was not until the day or two before the money was paid back that he knew exactly how much each item had cost. He hadn’t asked, not even once, in all the previous months. It simply wasn’t sorted out “at the first opportunity”

And while Leauanae did eventually put out an apologetic statement, it was only the day after the Commissioner’s statement, when the issue started to get some media coverage. And we know there is no written apology to PSC or MPP because my OIAs covered all communications with Leauanae on these matters, and none of them included either an apology from him (or any reprimand by the senior PSC officials dealing with the matter – and PSC did not say there were any documents they were withholding on the grounds of, say, personal privacy).

But then notice that middle paragraph of the PSC statement, which followed a comment that Leauanae had not been involved in decisions at MPP about the scope, nature and expense of the farewell

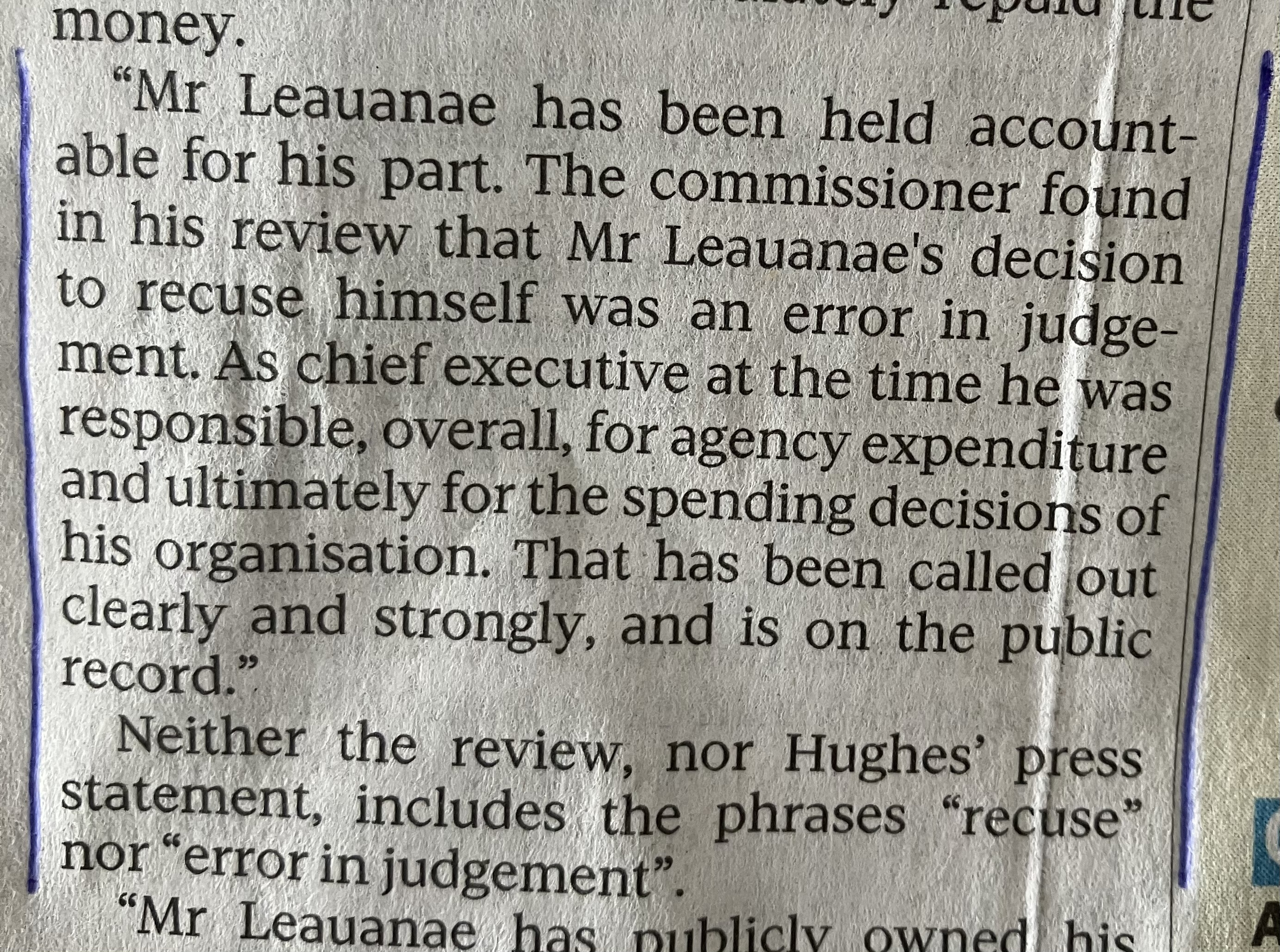

The Commissioner found in his review that Mr Leauanae’s decision to recuse himself was an error in judgement. As chief executive at the time he was responsible, overall, for agency expenditure and ultimately for the spending decisions of his organisation. That has been called out clearly and strongly, and is on the public record.

which sounds fair enough I guess. Or would if it were true. When Vance sent me this statement yesterday I went back and checked the report. From Vance’s article

There is simply no statement along those lines in the report or the press release. Did Hughes and his comms guy really suppose no one would check? Or did they just not care?

Not only are the specific words not there, but neither is anything along those lines. Read the documents yourself if you doubt me (I had to twice, because I couldn’t quite believe we were just being lied to). The press release will take you 2 minutes, and the report not that much longer. The report simply notes that even if he formally or informally recused himself, Leauanae was still chief executive and was responsible (which is not in dispute, but is very different from what the PSC statement yesterday said).

There are a lot of other points that could be repeated from my previous post, including about how PSC’s oversight of the public service was so lax that it was months after the event before they knew (or claim to have known) about any of this lavish spending, despite two of their staff being there, another CE being a speaker, and the relevant government minister also having been a speaker. But you can read the previous post for that.

I’m just going to end where this post started. Hughes and the PSC proclaim the importance of the value of trustworthiness, integrity etc. Little or nothing of that has been on display around the public side of this investigation into serious misjudgements (and, it appears, weak management and/or a sense of entitlement) by someone (Leauanae) who appears to be a Hughes protege. Never less so that in the follow up statement to Andrea Vance yesterday.

On the evidence of this affair, PSC appears to serve PSC’s interests and those of its chosen. That is, of course, the tendency that economic analysis would tend to predict. But it is a very long way from the guff that Hughes likes to spout about the public interest and public trust.

A few weeks ago, just before I went away for 10 days holiday, the latest in the saga of the Reserve Bank MPC, and the blackball on external experts when the first MPC appointments were made, appeared in the Herald.

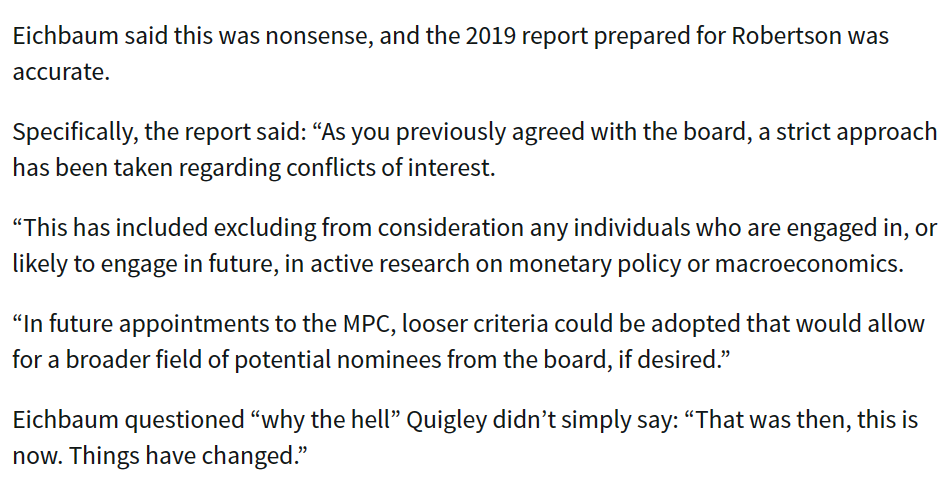

You’ll recall that it was widely understood that there had been such a blackball, put in place by the Bank’s Board and agreed by the Minister of Finance. It was widely understood by pretty much everyone – the Minister, Treasury and Reserve Bank staff, former senior Reserve Bank figures, (quite probably even MPC members themselves), a former senior adviser to the Minister, and Bank spokespeople – and was widely reported, and not denied, once the news got out formally with an OIA release from the Minister to me back in 2019, which had included a procedural papers from Treasury’s appointments and governance manager, handling the formal side of the appointment process, which described the blackball. Lines in that paper – that they were being particularly cautious but that a more relaxed approach might be adopted in future appointments – had been echoed in later comments by people speaking for the Bank. All this had come on top of the person, with macro-specific expertise, who back in 2018 had enquired about the MPC roles and been told by the Board’s recruitment firm that there was a blackball on research expertise, and who had then gone to the Board chair (Neil Quigley) himself to check, and had been told face to face that indeed there was such a ban. I wrote about it all here.

The reason I (and others) were still writing about it was that a few months ago, when forthcoming MPC vacancies were first advertised, it became apparent that the blackball had been lifted, and in this round people with research expertise and possible future research activity in areas of macroeconomics and monetary policy would not be barred from consideration by the Bank’s Board. That was, and is, good news (cynics might suggest that the Board is simply likely to fall back on adopting a slightly different test, barring anyone who might prove awkward for the Governor, but leave that issue for later). But then Treasury, backed by the Minister, issued a statement to the Herald claiming there had never been a blackball, it had all been a sad misunderstanding, and tossed one of their own former mid-level staffers under a bus by suggesting that when she’d written that memo to the Minister, she’d simply got the wrong end of the stick. And, so OIAs revealed, they made this comment – without any serious scrutiny or testing (including asking the person concerned) – because Neil Quigley had, on two occasions, this year told them so. The Treasury official had simply got things wrong, and all that had happened is that some academic who was interviewed for the role had refused to commit to not commenting publicly if appointed, and so that person had not been taken any further. Or so Quigley said.

In that post last month I outlined why this simply wasn’t a credible story, and that either Quigley was simply and deliberately misrepresenting things, or – years on – was suffering from a faulty memory, and had conflated two quite different things. Either way, his claim now that there had never been a blackball simply did not stack up, and Treasury should not have been uncritically making statements based on it, perhaps particularly when it involved throwing one of their own former managers (and managers at Treasury aren’t junior people) under a bus. Treasury should now be rather annoyed at Quigley, for putting them in a situation where taking him at his word – a senior government appointee – had left them with egg on their face (I have an OIA in on how, if at all, they have dealt with this subsequently).

Anyway, that is all prelude to the Herald’s story on 12 September. In my posts I had noted that among the many reasons for scepticism about the Quigley story was former Board member Chris Eichbaum. I knew he used to read my stuff (he told me so one day when I ran into him) and had not been backward in coming forward, commenting in replies on Twitter when he thought I’d got it wrong or been unfair about the Board and its role/performance. Not once had he objected to my characterisations of the existence of a blackball (this back before he left Twitter).

The Herald’s Jenee Tibshraeny got in touch with Eichbaum to see if he had anything to say now. He did. In fact, her story opens with an Eichbaum expletive.

Asked specifically about the 2023 Treasury denial, which had channelled Quigley, this was Eichbaum’s response

Well indeed.

He’d added

noting that today’s Board might not be as “risk-averse” as the old Board was.

Here it is worth noting that Eichbaum was not just any Board member, but was one of the small interview panel (him, Orr, and Quigley) for these MPC roles back then.

I also understand that Eichbaum regards the Herald article as having fairly and accurately represented his views/comments.

That might have seemed fairly open and shut. There are suggestions there is no love lost between Eichbaum and Quigley (one of the left, one of the right, and Quigley had been a former senior manager at Victoria University where Eichbaum taught – and comments on Quigley from people at Vic then often seem to have quite an edge to them), but it all seemed pretty clear. There was an expertise blackball, as everyone else had believed until Quigley belatedly sought to deny it.

But there were some more Eichbaum comments in the post, on a slightly different strand of what seems to have gone in 2018/19.

Which seems to give support to what outsiders have supposed all along (anyone awkward for management, especially the Governor, wasn’t going to be welcome), but is also consistent with that “consensus collegial” model of MPC decisionmaking which the Minister went along with (but which is not practiced in the best practice MPCs globally). The Bank had actually wanted to ban external MPC members from giving speeches or interviews at all, but the Minister didn’t go along with that…..and the practical solution seems to have been to appoint people who had neither the interest, inclination or ability to give speeches or serious interviews (despite being responsible, supposedly actually accountable, statutory appointees and decisionmakers).

But it also points to what Quigley may have been remembering when he falsely claimed there had never been a general blackball. There clearly was – as Eichbaum says – but it looks as though they may have also turned down one person who got as far as an interview because he/she wanted to be freer to speak. That wasn’t a wider general ban, but specific to an individual and the limitations of the model the Bank wanted around MPC. There was still a wider ban on people with actual/future macro research expertise etc.

But focus on that final para of Eichbaum. In open and transparent central banks – Bank of England, Fed, Riksbank – individual MPC members often give speeches or interviews, sometimes based on their own research, often drawing on their own analysis, outlining their thinking on issues, risks, and outlooks, including policy outlooks. It is quite normal, not at all problematic, and quite consistent with the inevitable huge uncertainty around any view on the outlook and likely required future stance of monetary policy. But we don’t want any of that sort of openness in the Robertson/Orr/Quigley Reserve Bank……and they’ve delivered. We’ve heard nothing of substance – research or not – from any of them.

And that might have been that, but on the same morning the Herald article Newsroom published a column on the MPC blackball issue by Eric Crampton, who has had many of the same views as me on the issue.

And one Chris Eichbaum left a comment.

This is the same person quoted in the Herald saying Treasury’s description of the blackball had been quite right, and it was only a shame Quigley hadn’t just said so and said they’d now moved on.

But this comment, if it is to be interpreted consistently with this comments to the Herald, must also be about that desire to ensure that no external MPC members were speaking in public at all, at least never articulating any views of their own. That is a different issues than the macro research expertise blackball – not much more defensible in substance, but at least with some precedents (notably in the RBA model that the Bank wanted to model its committee on – more ornamental than substantive).

What of that second paragraph? I am not aware of anyone who thought they had a “claim on MPC membership” – and Eichbaum seems to have no evidence for his claim – but a really large number of people, economists and not, many of whom would not have wanted to touch an Orr RB MPC with a barge pole, were nonetheless seriously disconcerted that our MPC was to be the only one in the world where formal expertise in the subject was a disqualifying factor. As it clearly was, as Eichbaum acknowledged to the Herald. And recall that the story did not break in the first place because some aggrieved academic went to the press but because a citizen used the OIA and the Minister of Finance complied with the law and released the relevant material.

In the Newsroom comments column Eric Crampton responded to Eichbaum. Here were some relevant bits of Eichbaum’s reply.

It is interesting in its way, but what it seems to confirm is the conflation of two quite separate events by Quigley. The block put on an individual at the interview stage seems to have been specific to one person’s desire to be free to communicate publically while in office.

But that is very different from the message conveyed by the Board’s recruitment firm – confirmed face to face by Quigley – that no one with active or future research interests in and around monetary policy would be considered (would even be longlisted), let alone interviewed or appointed.

There is no real doubt that happened. The person who recounted their experience to me is someone whose integrity and honesty I have never had any reason to doubt. The fact of that blackball also squares with what the record of a Board meeting discussion in 2018 suggested (copy in earlier posts).

But I realised that when the Bank had responded to my OIA request in 2019 re MPC appointments it had left out a lot of material that as clearly covered by the wording of my request. So I lodged a few weeks ago a further request – noting the prior omission – asking for all dealings with the recruitment firm around that first round of appointments. The Bank is slowwalking that request too – citing the need for “consultations”, about events 4-5 years ago – but before long we should have those answers too.

(Interestingly, I had another OIA back from the Minister of Finance last week re any discussions/advice this year re the blackball and its removal. It appears he was not involved at all (which I have no particular problem with, although one might perhaps have hoped for a more proactive approach).

Some of you will be wondering why any of this matters. To me it is a matter of two things. First, a really bad decision was made in 2018/19, which got the MPC off to a very poor start. But at least as importantly, because honesty and integity matters, or should do, in public life, and particularly in and around powerful independent agencies. We’ve simply not seen that from Neil Quigley (and here I am clear that his responsibility is personal: the Governor and management have not weighed in to support his, clearly wrong, story).

But it does bring us to today. In the papers I got from the Bank a month or so back there was a lot of material about the process that is underway to fill the two MPC external vacancies next year. It is a quite unsatisfactory situation. The Board – appointed entirely by the current Minister of Finance, few of whom have any relevat expertise – have not only advertised to fill the MPC vacancies, have had their recruitment firm tell at least one qualified person that they simply won’t be considered, but were on schedule to have conducted final interviews last month, positioned to deliver recommendations to the Minister of Finance once a new government is formed.

Perhaps that would be no great problem if a Labour-led government were to be returned – his friends and appointees on the Board will be delivering names consistent with the last few years’ model of the Reserve Bank. But it is highly unsatisfactory if there is a new government, especially in light of the concerns both National and ACT have expressed about the Governor and the Bank’s stewardship. If Nicola Willis is appointed Minister of Finance, she should start the process from scratch, making clear to the Board the sort of people, and sort of model (hopefully both more expert and more open) that she wants, opening the process to people who might be more interested in serving under such a model, even if Orr is still in place. The first vacancy is not until 1 April next year. It is very difficult to get rid of the Governor himself – and thus Willis has made a virtue of necessity in ruling it out – but if a new government is at all serious about change it has to start with a keen focus on all vacancies, MPC and Board, as they arise. Whether they are really serious – I’m sceptical – I guess only time will tell.

It is election season, and since the performance of the economy enables (or disables) so much of what political parties want to do, or to spend, it is worth having a look at a few charts. There have been plenty on inflation this year, and plenty of fiscal policy in just the last few weeks.

I had an op-ed in The Post and The Press the other day, which touched on some of the old and new economic challenges, the greatest of which – and longest running of which – is the dismal productivity performance of the economy.

I had in mind this, from a post a few weeks ago

I’d wondered how New Zealand had done over just the last 10 years – half spent under National governments and half under Labour governments.

We’ve dropped six ranking places in a club of only 37 members in just a decade. It took me a little bit by surprise, and I think partly because the New Zealand debate (such as it is) rarely focuses on the countries that are now most similar to us in productivity terms.

And for those wanting to play crude National vs Labour partisan games on this one, probably best not. Here is our quarterly data up to Q2 this year, with a simple linear trend through the data. The last few years have been a lot noisier, as you might expect, between (a) Covid disruptions, and (b) the fact that recent data are somewhat provisional and will keep getting revised for the next few years. Note that whatever influence political parties’ policies and practices have on economywide productivity, outcomes don’t just change the day a different party takes office.

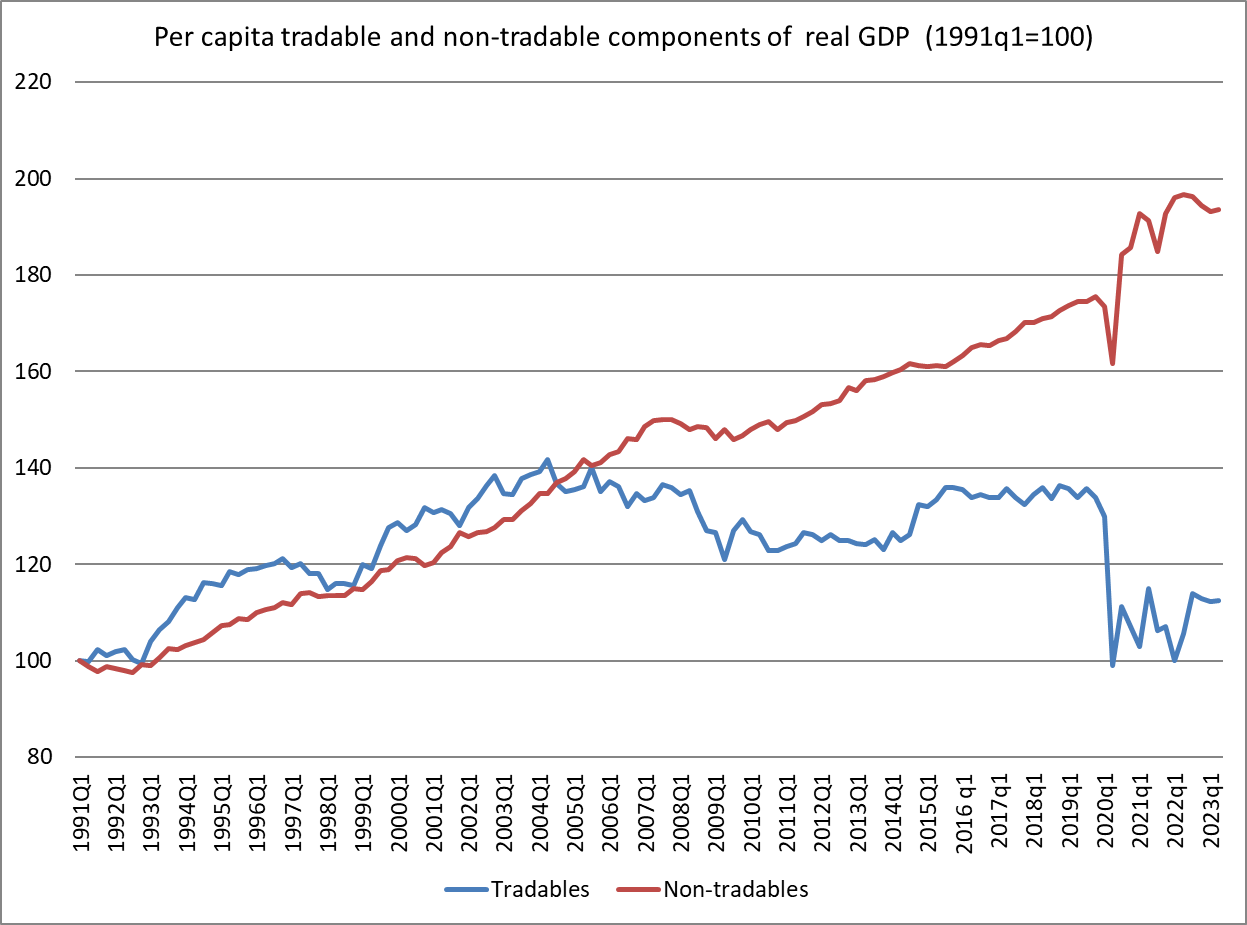

A line I’ve banged on about quite a bit over the years is the unbalanced nature of the New Zealand economy, in which growth in production in the tradables sectors has tended to lag behind that in the non-tradables sectors, going back at least 20 years, and the opposite to what one might expect to see in a successful economy gaining ground on other countries it had dropped behind.

Here is the latest version of the summary chart I’ve used for that purpose.

Tradables sector output, per capita, is about where it was 30 years ago. Even if tourism magically quickly recovered to pre-Covid levels, the pre-Covid picture wasn’t really much more encouraging.

In last week’s column I noted

Productivity isn’t primarily about individuals working harder. It is mostly about having an economy where more firms find it attractive to invest in producing new and better products, to produce old products in better ways, tapping new markets, and by doing so supporting higher incomes across the board. But business investment here has been weak, as a share of GDP, for a long time. Nowhere near enough firms are finding anywhere near enough opportunities to enable New Zealand to reverse its sustained relative economic decline.

I hadn’t checked the comparative business investment numbers for a while but I did this morning

Sure enough, in a country which has had much faster population growth than most OECD countries – and high labour force participation – business investment has been lower as a share of GDP than in most advanced economies. That isn’t what you’d expect to see in a country making any progress at all in reversing the decades of decline. It is, however, consistent with New Zealand’s own dismal record.

And while for a decade or so we managed to support growth in living standards on the back of a rising terms of trade, that was almost a decade ago now. The terms of trade haven’t gone consistently backwards, but they aren’t supporting any further growth in material purchasing power (or the tax base)

I also touched on house prices in that op-ed, observing

House prices are rising again, from levels that are still punishingly high. In real terms they are materially higher now than when the current government took office, a pattern we’ve seen with successive governments for decades. Political parties talk about improving housing affordability, but market prices speak louder than politicians’ words.

What I had in mind was this chart, drawn from the BIS cross-country database of real house prices, going back many decades (in our case to 1970). Assuming Labour loses office this month we won’t have the final data for their term for a while yet, but I’ve allowed another 2.5 per cent real drop from the last published value for the March quarter this year.

Terms of government differ (3, 6, and 9 years) and of course background economic circumstances differ a lot. Often within terms of government there have been both periods of flat or falling real prices and ones of quite material increases. But for more than 30 years, real prices have been rising……really for no other reason than the combination of regulatory and structural policy choices successive governments have made. Parties approaching office like to suggest they have some sort of answers, but they haven’t delivered…..and current market prices (remember, houses are asset prices, trading on all information about the expected future) don’t suggest the likely next government is likely to be much different. Land prices in peripheral areas around our cities certainly aren’t collapsing. (And all this latterly after the steepest quick increase in interest rates for many decades – probably since 1984/85.)

Which brings us back to productivity. Neither main party – one of which will lead the next government – seems to have any serious idea or policies (not even an underlying narrative) that might turn things around and offer a much better (relative to the other countries we increasingly lag behind) tomorrow for our children. Judging by how little the words (“productivity”) or ideas have appeared in debates, manifestos, campaign appearances, it isn’t obvious they really care much. Squabbling over which baubles to offer the voters, and how to pay for them (at a time when the budget is deep in deficit) seems to be where the game is at.

Probably like most people I’d got a bit tired of the foreign buyers’ tax revenue estimates issue. At best I can tell, something like the estimates we produced seem more plausible than National’s numbers. In the grand macroeconomic scheme of things, the differences are fairly second order (0.1 per cent of GDP vs the 2.7 per cent of GDP gap between revenue and expenses this year in the PREFU). But it has not been reassuring that National has simply refused to release their modelling/calculations or authorise the release of the modelling said to have been done for them by Castalia. It is an evasiveness that doesn’t speak well of a party that has come out in support of a state Policy Costing Office, and whose leader just this morning is reported to have championed an overhaul of the OIA (presumably to encourage more transparency/accessibility). No one can make them publish, but if they don’t we can draw our own conclusions. As a straw in the wind on that point, I saw National’s recent responses to questions on this issue from one media organisation, in which Willis seemed more interested in casting doubt on our independence, than in elaborating on their own work. (My earlier two posts are here (including the underlying paper) and here.)

Much as I quite liked the modelling exercise we did, in some ways I took at least as much comfort from what I could learn of the Canadian experience, most notably the revenue numbers from their foreign buyers’ tax in British Columbia – Vancouver having been a magnet for (in particular) Chinese purchases, and the tax having been applied at all price points. But I hadn’t made much effort to look more broadly, not really being that familiar with the data sources in other countries.

But this afternoon someone sent me a link to an Australian Tax Office insight note, with data, on foreign purchases and sales of residential real estate. Under the Australian system (accessible summary here) foreigners other than New Zealand citizens need FIRB approval to buy a house in Australia (this includes people on temporary work visas, but not permanent residents).

The report has data for four (June) years, to June 2021. The numbers appear to be for those classes of people who require FIRB (ie ex NZ purchases).

You might be inclined to discount 2019/20 and 2020/21 a bit, having been disrupted by Covid, including the border closures for much of those periods. But even if one starts from the 2018/19 numbers, it is a total of 7679 sales of dwelling (new and existing) in a full year, at all price points. Around 80 per cent of all sales (by number) were at price points under A$1m (this will include the vacant land sales, but they only make up about 20 per cent of the total).

The total value of foreign purchases in 2020/21 was A$4.2 billion. In 2018/19 – when the volume was higher – the value of sales in total was A$7.5bn. (Interestingly, whereas foreign purchases have been dropping, sales of such properties by foreigners – a much smaller number – were rising over this period.)

Had a 15 per cent tax been applied to that 2018/19 higher level of sales it would have raised only just over A$1.1bn even in 2018/19. Australia is, of course, five times the size of New Zealand (and the proposed tax here will exclude Australian – and Singaporean – buyers, as New Zealand buyers are excluded from the Australia numbers), so if it were really a like for like comparison this would be consistent with not much more than about $200m of annual revenue here. On the assumption that – unlike National’s proposal – purchases at all price points were covered.

However, this is not a clean comparison. The Australian land transfer market is riddled with complexity and costs. Not only does the FIRB process appear more constraining (especially on non-resident purchasers of other than investment properties – as distinct, say, from people living in Australia on work and study visas) than what National is proposing for properties selling for more than $2m, but there are stamp duties and the like. In Victoria, for example, foreign buyers in this period faced this additional transfer duty

All of which means I would not put too much weight on this report – comprehensive as it is in the Australian context – for insights on prospects for New Zealand if National’s policy were to be implemented. But in the grand scheme of things, Sydney and Melbourne are rather more “global cities” than Auckland (and about as expensive, in price/income terms), and Australia has – per capita – about as many migrants as we do. And what none of us know with any certainty is how many of the houses being bought by foreigners before our ban – outside Queenstown, small in the overall scheme of things for non-Australian buyers – were bought by people living here at least part of the time, as distinct from holiday homes

The most I would say is that it is just one more straw in the wind – but no more – that the National revenue estimates still seem implausibly high.

But perhaps things would look different if we saw National’s own or Castalia’s modelling.

I have become increasingly concerned about the declining standards in New Zealand public life, where things that come close to corruption get justified or excused, with very little attention from main Opposition political parties or the media. Labour has been in government for the last six years, so many or most recent examples have featured Labour ministers or appointees (eg the Public Service Commissioner simply lying to the public, one of his proteges (who would not still be in office if ministers took standards seriously) who took lavish taxpayer-funded gifts etc when changing government jobs and was very slow to pay back the money when concerns started coming to light, a senior minister attempting to pressure Radio New Zealand re the employment of someone close to her (and then refusing all attempts to get the text of her remarks released), or Cabinet ministers left in office by the PM even as their spouses are soliciting business contracts from agencies the relevant minister has responsibility for – contracts that, by the nature of marriage, they are direct personal financial beneficiaries from). And so on.

But as the prospect of a change of government has increased, so has my level of concern that the leadership of the National Party has made fairly little of such episodes and tendencies, and in particular has refused to take a strong stance making clear that such behaviours would be dismissable offences under a National government and its Prime Minister. I am generally reluctant to quite concede Matthew Hooton’s suggestion that each MMP government is worse than the one before it, but when it comes to standards in public life it is increasingly hard not to think he is right (although whatever United Front interests/individuals are now going to be in Parliament I suppose we should be grateful there is no one quite as egregious as Jian Yang now in prospect).

I have also been on record for years being concerned about former senior ministers and Prime Ministers moving effortlessly from politics into highly-paid private sector positions. I’d rather we paid retiring senior politicians a decent pension than to never be quite sure that people were not governing with a view to their next appointment. Being Prime Minister should be a stepping-stone to….retirement, the grandkids, and perhaps doing good and charitable deeds.

This post was prompted by an article in The Post this morning, a feature interview with John Key about campaigning, the election, Christopher Luxon etc. It highlights another area of risk/threat, which I hope gets some scrutiny.

Were John Key simply a retired former Prime Minister now tending his garden, his golf or his helicopter (it gets a mention in the article) it would be no problem at all. He has real campaign experience and can offer some potentially useful insights on the man, campaigning and so on. Especially when we learn (to no one’s surprise) that

But John Key is also chairman of New Zealand’s largest bank, ANZ, something which features prominently and deliberately in the article.

and lest there was any doubt (could, just possibly, this be a personal office that just happened to be in the ANZ building)

It is the ANZ chairman’s office. Key could easily have arranged to have the interview over lunch in a restaurant, at home, almost anywhere really…..but he chose to have it in the office of the chair of the biggest bank in the country. His office, in that Bank.

Now, if one were an ANZ customer (I am as it happens) it might or might not bother one to have the chair of one’s bank so openly aligned with the (likely) incoming Prime Minister and his party. There is certainly no sign that Key has become an uncontroversial non-partisan figure in his late middle age. Personally, that aspect doesn’t really bother me.

What I’m concerned about is that big banks are heavily regulated entities (far too heavily in my view, but what is is), and – most importantly – entities where there is a very strong expectation that if they get into trouble governments will bail them out one way or the other. Bail-out decisions aren’t a matter for central banks but (and rightly) for elected governments (no one more so than the Prime Minister and the Minister of Finance). Not only that, but although much of the implementation of regulation is done at arms-length (Reserve Bank and FMA) much of the policy-authorisation requires ministerial say-so. Plus, of course, ministers appoint the boards of both the Reserve Bank and the FMA.

And so in a few weeks it seems we will have chairing the board of our biggest bank someone who describes himself (quite credibly from all else we’ve seen and heard over the years) as “quite close” to the new Prime Minister, with the new Minister of Finance one of his own former staff.

It is a really serious conflict, and one of those where even if all the individuals involved actually act honourably, always and everywhere, neither they (unconscious bias, subconscious motivations etc) nor the rest of us can be confident that would be so, most especially in times of stress and crisis.

Banks being run by close affiliates of senior political figures are a well-recognised risk in the banking regulation/supervision area. The risks here may be a bit different from those in some deeply corrupt developing countries – not, eg, a matter of soft loans to the politicians etc – but that doesn’t mean they don’t exist. Public confidence in our system relies on the public having good grounds for being sure that only the public interest is shaping major policy and regulatory interventions. No might how honourable the individuals concerned here might be (I am making no observation on that), we simply cannot be that confident when a close confidante of the (probable) incoming PM and MoF – and former leader of their own party – is chairing the biggest bank in the system. That is so in the stress events I most worry about, but it is also so around the more fevered politicised debate about bank profits and whether anything should be done about them.

I would note that this is not one of those problems that is either inevitable everywhere, or innate to a fairly small country like New Zealand. It is also a different issue than ones around wholly state-owned banks (dubious as the appointments of Bolger and Cullen to NZ Post/Kiwibank were). The issue is also not about whether Key might have some pre-politics expertise that otherwise equips him for an ANZ role.

If you check the main boards of the big Australian banks by contrast you will find no former Australian politicians on any of them (although Key is also on the main ANZ Board). And, as it happens, the ANZ main board also has on it a New Zealand citizen (albeit resident in Melbourne) – a long time ago even a Treasury official – with much more banking experience, and no obvious political party affiliations. The other big banks in New Zealand manage without such political figures in prominent Board positions.

I hope National has thought seriously about this looming issue (not really an issue while they were in Opposition) and has plans for how to handle it. Other political parties and the media should be asking questions now, because voters deserve to know (both on the specific, but also on the more general approach to standards in public life an incoming government would propose to take). The best we can hope for is high enunciated standards now, as things tend to corrode under the actual pressure of office.

It isn’t obvious what the solution should be from National’s end. The Prime Minister and Minister of Finance can hardly stand aside from bank crisis resolution issues, not just because potentially huge amounts of money will be at stake, but also because resolution is likely to be highly political and involve high-level haggling with the Australian government. Nor does recusing themselves from bank regulatory issues really work – some junior minister might get to make the formal decision, but junior ministers are ambitious to be senior ministers. Perhaps – yes this tongue in cheek – Winston Peters might have to be delegated that specific power, as I’m sure there is no love lost between him and Key.

Key could of course resolve the issue, and if he were to do so it would prove him to be an honourable person, by stepping aside from his ANZ roles if National is elected, recognising that otherwise the appearance of conflict will never go away, and neither he nor Willis/Luxon, nor the ANZ will ever be free of either controversy or suspicion. Even if all acted otherwise honourably in the presence of such a conflict.

But it needs to be addressed now.

UPDATE (2/10). Thinking about this issue a bit further, while it might not be a fully adequate solution one step Luxon and Willis could take is to cut ties with Key (no meetings, no texts, no nothing), for as long as he is chair of ANZ. That would be an indication that they took actual and perceived conflicts seriously.

For those still doubting there is an issue it was reported this morning that in an interview with Mike Hosking Luxon had made these comments. Much of it is probably empty pre-election rhetoric, but they are his own words…..”constantly monitoring” a bank chaired by his mentor, close adviser etc, about matters which aren’t delegated to independent agencies. Again, no matter how honourably all involved believed they were individually behaving, no one (including the people concerned) could really be verifiably confident of that. Hard lines have to be drawn when monitoring (in this case of politicians/private business figures etc) is impossible and the issues/entities not small.

National’s “fiscal plan” came out this afternoon. To no one’s great surprise I guess, we didn’t learn much from it. The big National numbers had been in the Back Pocket Boost package a few weeks ago, combined with the statement from Willis last week that National would get back to an OBEGAL surplus no sooner than Labour was suggesting it would (in PREFU, and in its own fiscal plan). Oh, and they paid some economic consultants to say much the same as Labour got their economic consultants to say: the promises listed added up to less than the future operating allowances the two parties had indicated. As I noted in my post the other day, Labour’s consultants (Infometrics) noted that they hadn’t had much time. But then, having splurged in the previous two budgets, Labour is going into this election with fewer and smaller promises. National’s Castalia is reported to have done a bit more work on a couple of items, but we are still left totally in the dark about the numbers behind the foreign buyers’ tax revenue estimate: neither National’s nor Castalia’s modelling has been released, and there is no official agency estimate to use as a starting point.

The National “plan” is unambitious, depressingly so if you care about fiscal responsibility, or even about easing pressure on monetary policy when (core) inflation – which National has (rightly) been quite strident about – is still coming down slowly if at all.

If you are wondering where that 0.7 per cent of GDP in the title of this post comes from that is how much lower net government debt is estimated (by National themselves) to be lower than the PREFU numbers by 2027/28 – a year so far out it isn’t even in the main PREFU forecast numbers (which run only to 2026/27), and which involves budgets set after the next election, when who knows which constellation of parties will be in office. In the final year of the forecast period – and the final year for which any new government elected next month will set the Budget – the difference is 0.4 per cent of GDP. The differences are derisorily small (and totally swamped by margins of errors around each parties’ plans, let alone uncertainty about denominators (what happens to the economy, and recall that Treasury’s PREFU forecasts were taken by many economists as veering towards the optimistic side)).

Now, I’ve seen Willis and Luxon quoted as saying “ah yes, but no one should believe that Labour can deliver on its plans” (the ones included in the PREFU, including future operating allowances). “Look at their track record, of consistently overshooting those lines in the shifting sands, announced intended future operating allowances.”

And I’d have some sympathy with that line, as no doubt would The Treasury, whose own lightly-coded comments in the PREFU were really rather sceptical (for a government agency in public), highlighting the tough choices and tradeoffs that would be required. At best, the fiscal numbers (recent “cuts” and future operating allowances) behind PREFU are statements of current high-level intent only. Achieving them against the backdrop of ongoing cost pressures – and temporary windfalls from surprise inflation that will not persist – will be challenging to say the least.

But the problem for National with this argument is that they will face all those same pressures, and instead of approaching this election with a serious stance of austerity, emphasising the size and unjustified nature of the current government’s deficits, they are playing much the same game as Labour has over the last year or two, competing to see who can give out the most electorally attractive baubles, and funding those handouts with either the same new distortionary tax Labour is championing (depreciation on non-residential buildings), even as they claim to the party of business and growth, or with a tax (foreign buyers) that is not only unprincipled and inconsistent with much of the rest of their messaging (“supply is what matters”, “foreign investment should be championed), but where the revenue estimates command no confidence whatever beyond the halls of the National Party wing of Parliament.

Now, I for one do have some confidence that National will be better at cutting, or restraining, spending in the next few years. They’ll be cutting stuff the other side did so won’t have the same attachment Labour ministers would have had. But……they need to be better at cutting just to get the same fiscal bottom lines as Labour, because their fiscal plans – bottom lines oh so little from Labour’s – already rely on much larger cuts than the numbers Labour themselves have already talked of (neither side offering any specifics at this point). And for all the talk of spending restraint, and even of a pre-Christmas “mini-budget”. today’s numbers seem to involve no change at all, relative to PREFU, to 2023/24’s spending levels.

And National has its own future fiscal vulnerabilities. Not only will there be pressure to bring down the 39 per cent income tax rate (ruled out only for the first term) but in the Back Pocket Boost package there was this

It isn’t a promise to adjust, but it is a promise to review, and it will be hard to resist the pressure for some adjustment in the 2026 Budget, running into the next election.

It is simply unserious from a party that has banged on – quite reasonably – about Labour fiscal excess in the last few years, and now seems to be slipping (predictably but sadly) into me-too mode, advertising themselves as just a little less bad than the current lot, offering a different set of baubles (ones that seem more electorally appealing at present, but have much the same macro effects).

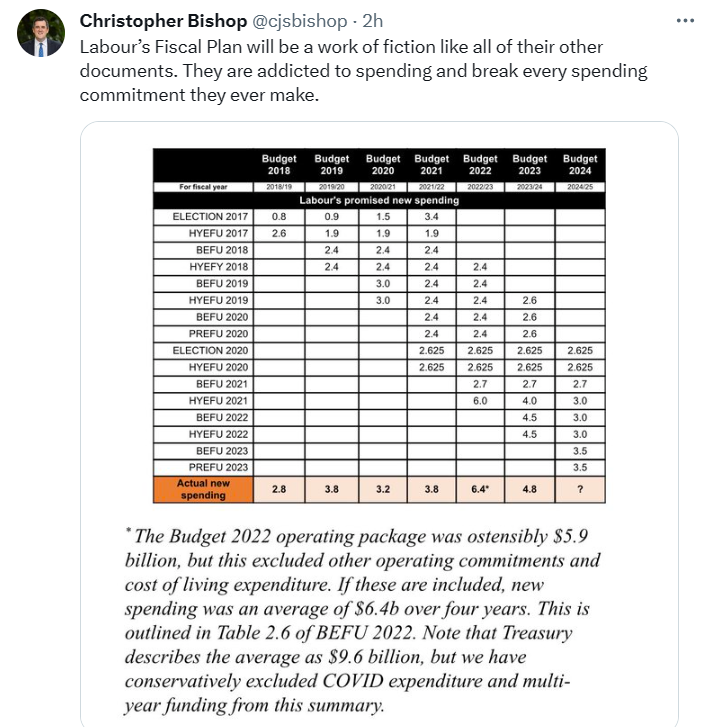

One telling point (which I owe to Eric Crampton) is to compare what Labour planned to be spending in the medium-term before Covid hit and compare it to what National plans to spend (years down the track) in the medium-term, as (ostensibly) the smaller government party, the party of tough spending discipline. In fact, the one that won’t cut any serious programmes, and only wants to add a few more.

Here, it is only fair to focus on primary spending (National inherits the debt Labour ran up, and it has to be serviced for now). In the HYEFU at the end of 2019 core Crown spending excluding finance costs for 2023/24 was projected (on Labour stated plans) to be 27.1 per cent of GDP. We don’t have detailed tables from National, but there is a line in the plan stating that they intend core Crown spending will be 31 per cent of GDP in 2027/28. Adjust for finance costs (from the PREFU, adjusted for small changes in National’s plan from slightly lower debt late in the period) gives 29 per cent of GDP. That is almost two full percentage points of GDP higher than Labour’s medium-term number.

(Some of that will be because of the ageing population, but that only highlights that National’s plans include not even starting on raising the NZS age for another 20 years. 20 years…….)

Finally, National asserts that their policy will be less inflationary than Labour’s.

That looks fine on paper, but (a) any effect is tiny ($300m), less than 0.1% of GDP, utterly lost in the rounding of any inflation forecasting model, and (b) it ignores quite a lot. That line attributed to the Treasury may be valid in a very general broad-brush sense, but here we need to think about concrete proposals. Thus, even if National’s foreign buyer tax revenue estimates were to be roughly right – and Willis’s latest answers to questions on this point advance things not at all – the money will mostly be coming from income not earned in New Zealand (thus representing no drag on demand) to fund tax cuts pretty much across the board, to a household sector with a high marginal propensity to consume. But reading through the plan, I was struck by a couple of other points. The removal of the regional fuel tax for example (while it will temporarily slightly lower headline, but not core, inflation) puts more money in the hands of Auckland householders, without any immediate identified replacement, and National says they think reserves will enable the Auckland local authorities to keep spending. Net, that is a near-term inflationary effect. They also seem to propose to pay to councils an extra $25000 for each house built above a five year average, funded by discontinuing various other things, one of which is a Kainga Ora land acquisition programme. My point here is not about the merits of the policy, but a policy which stops asset purchases and instead gives councils more spending money is also likely to be inflationary at the margin.

I do not want to overstate this point. All these effects are small, individually and even in total. But there is just no serious basis for National’s claim that their fiscal approach will be less inflationary than Labour’s. And Labour’s added a lot to demand this year, when inflation is still a serious problem.

Finally, for all those – probably mostly on Twitter – who have spent the last few weeks bemoaning my bias (in their eyes) towards either Labour or National, I’m told that at the Mood of the Boardroom event in Auckland this morning both Robertson and Willis were each at pains to suggest that I was no friend or fan of either of them.

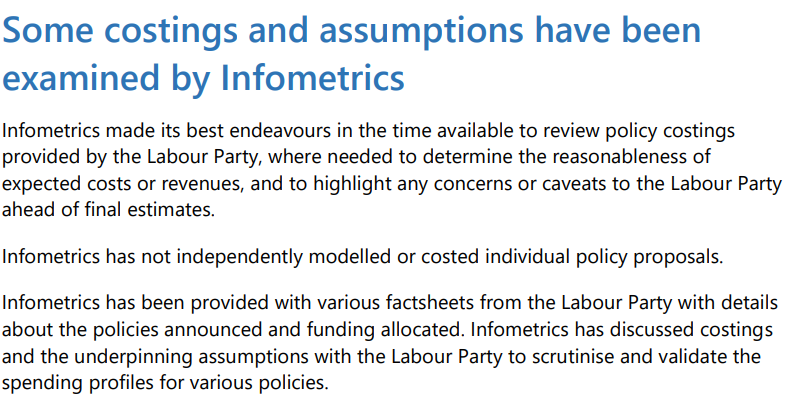

The Labour Party this morning released “Labour’s fiscal plan” together with a document reviewing that plan and prepared for the Labour Party by Brad Olsen of Infometrics. Both documents can be found here.

I suppose it is good that they have put out such a document – I’m not sure parties in office always have previously – but it adds almost nothing to our state of knowledge as at the PREFU a couple of weeks ago.

And so here, again, is the text and charts from my post after PREFU, where I suggested it was really a case of “pretend fiscal policy”. After that text, I’ll add a few charts on today’s release.

This morning’s post previewed PREFU at a high level, pointing out that both main parties had been in practice endorsing expansionary fiscal policy, and that the likely operating balance surplus that would be shown in the PREFU would really reflect nothing more solid than aspiration, even after the numbers had been gamed. Neither party seemed to have a concrete fiscal strategy or plan to actually close the deficit, a deficit which the IMF estimated a few weeks ago was one of the largest among advanced countries as a share of GDP.

As far as I can see there are no great surprises in the PREFU fiscal numbers. There is a small surplus in 2026/27, using the numbers the government told Treasury to use for its future spending plans. Anyone can plonk down a number. Delivering it is another thing.

There isn’t going to be lots of fresh analysis in this post, mostly (at least for fiscals) a series of charts I’ve shown on Twitter.

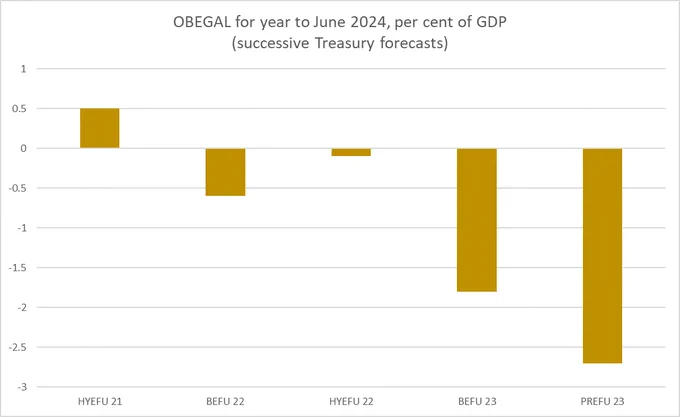

For example, here is how Treasury’s forecast of the operating balance (OBEGAL) as a share of GDP for the year we are now in has evolved just over the last 20 months.

The deterioration since the Budget this year is despite the economic position and capacity pressures (the output gap) being a bit less negative. This is a year for which the spending has now been appropriated, the taxes put in place etc.

What about the following year?

We aren’t anywhere that year yet, but the forecasts have already revised down massively.

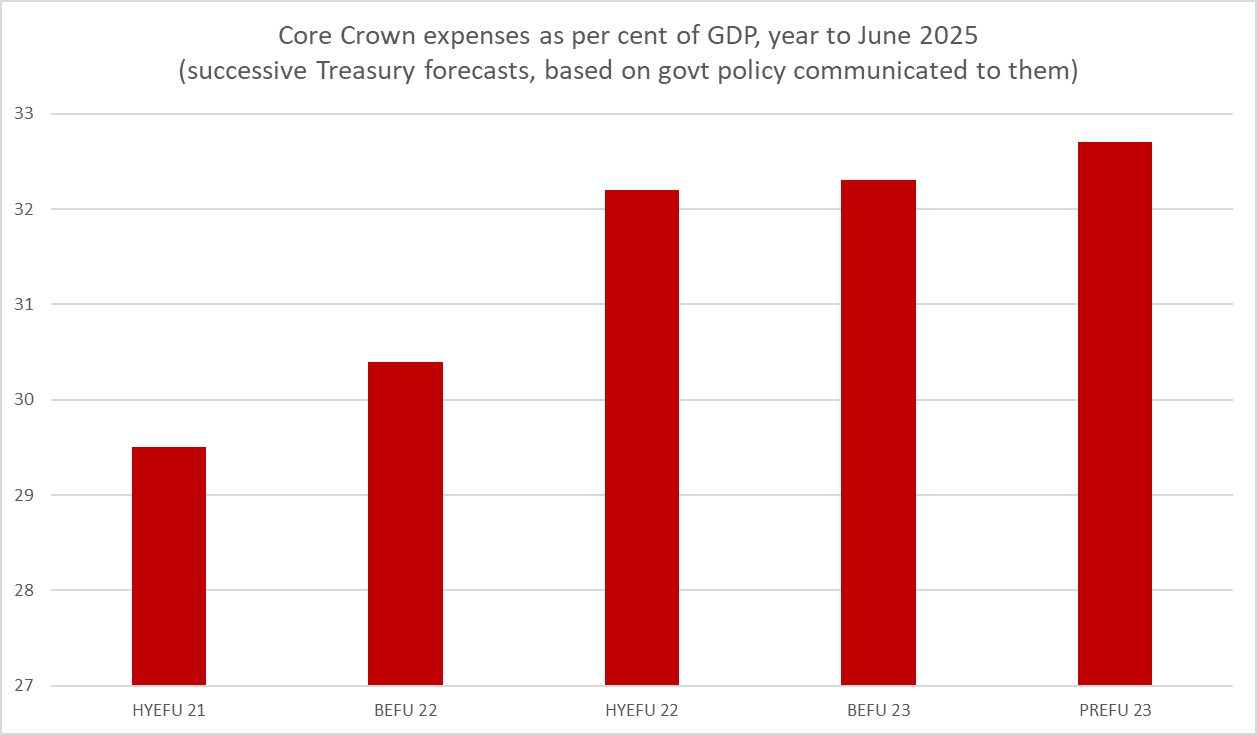

And despite recent talk of renewed fiscal discipline and spending restraint, here are the projections for core Crown spending as a share of GDP, again for the next Budget year. The PREFU forecast share is higher again than the BEFU one. And this is before Ministers actually have to confront drawing up next year’s Budget.

The political parties want us to believe that we are on a track back to surplus. We aren’t. Instead, the Secretary has been given some numbers to be consistent with a surplus by the end of the period, and for anything else…..well, we just have to wait for successive Budgets under whichever government holds office.

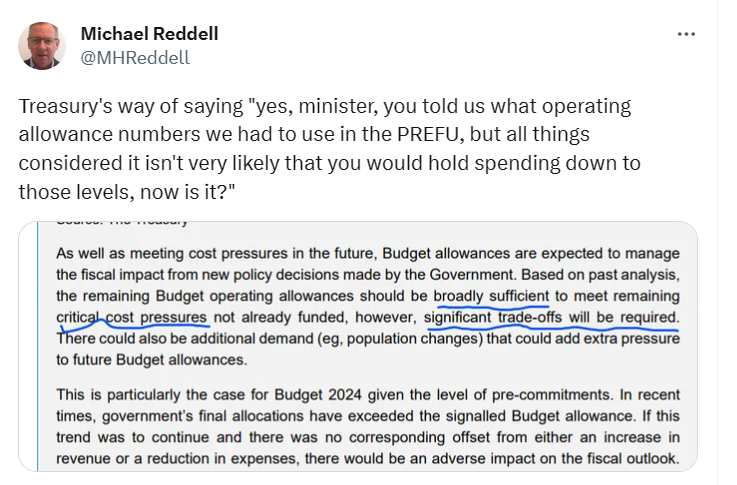

As for Treasury, they have to be a little diplomatic, but here is their text about spending and operating allowances, and my summary commentary

The medium-term numbers in the PREFU are just not a serious contribution to anything much. They distract more than they clarify or reveal.

Whichever party forms the government they face tough choices over years if they were actually to be serious about getting back not to surplus, or even balance. If they aren’t serious then net debt will continue to rise as a share of GDP and within a few years we will have higher net debt as a share of GDP than the median advanced country.

27 September material here again:

Setting aside the outright political spin one might expect in any such document or the deceit by omission (no mention of how fiscal policy in the last couple of years is adding to inflation pressures, or that while the median advanced country now has stable ratios of net debt to GDP, here that ratio is rising rapidly (albeit still at a level a little lower than the median advanced country)), what we have in today’s release isn’t much more than a statement showing that the specific operating spending items Labour has already committed to, as government or as party, do not add to more than the operating allowances Labour in government set a few weeks ago.

I guess that is welcome but (a) it is hardly a surprise (they set the operating allowance knowing at least in outline their election campaign approach, and (b) it isn’t enlightening because there is very little serious analysis of underlying cost pressures (eg are teachers really going to be stuck with a permanent real wage cut?), past track records (National is touting a nice table out showing how actual spending has consistently exceeded signalled future operating allowances) and nothing at all of substance on what is going to be cut to deliver on the sudden arbitrary scope for savings the government claimed to identifiy (and got in the PREFU numbers) a few weeks ago.

The publication of the Olsen report is also welcome. But it is very limited indeed.

They don’t seem to have had much time

and they explicitly reiterate that Treasury line I quoted above that “significant trade-offs will be required”.

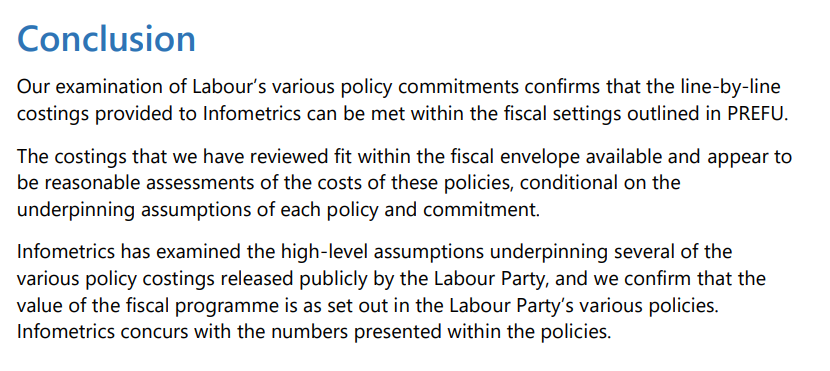

Here is the conclusion

It is a mechanical exercise not a behavioural one. Do things add up to less than the announced operating allowance? As far as they can tell, yes they do. It is good to know, but (again) isn’t telling us much.

Meanwhile we are still waiting for the National fiscal plan (let alone publication of the modelling their reviewer is said to have done for items in the earlier tax and spending package). Today’s document will up the pressure on them, at least a little, perhaps including in tonight’s leaders debate.

The bottom line, however, is likely to be that Labour had its irresponsible splurge in the last two Budgets (when Covid was simply not a material consideration, the economy was overheating, and domestic inflation was miles above target) and in this campaign there isn’t really much of a fresh bout (although one could mount a good argument that now is not the time for giveaways no matter the party). National, sadly, seems to think it should have its turn to splurge – and to further distort the tax system with the same anti business investment depreciation provisions Labour is also promising. It is no time for tax cuts, even if somehow they were (locally) fully funded and the revenue estimates stacked up. It is no time for substantial cyclically-adjusted fiscal deficits, which don’t fix themselves. Labour offers no credible story for how they will close them – just drew a line on a graph saying they will and that now they are the reformed drunkard not the drinker still on a binge.

Will National offer anything better re overall fiscal management? On the evidence to date – including comments from Willis citing Key/English, who were still running net expansionary budgets as late as 2010, before any quakes – it is difficult to be optimistic. One day we will see their plan.