The IMF released its latest World Economic Outlook and associated forecast tables overnight. There is no reason to think the IMF is any better as a forecaster than anyone else (ie not very good at all) but they do look at a bunch of advanced countries all at the same time, against a common global backdrop, so it is still worth looking at how they see things here relative to those other advanced countries. A few charts follow.

(Here, as in various recent posts, I remove from the IMF advanced countries Andorra and San Marino (as too small to matter) and Hong Kong, Macao, and Puerto Rico (as not countries at all), and add in Poland and Hungary, both of which are OECD member countries and performing similarly economically to various central and eastern European countries the IMF includes in their advanced country grouping. That leaves a group of 38 countries, including New Zealand.)

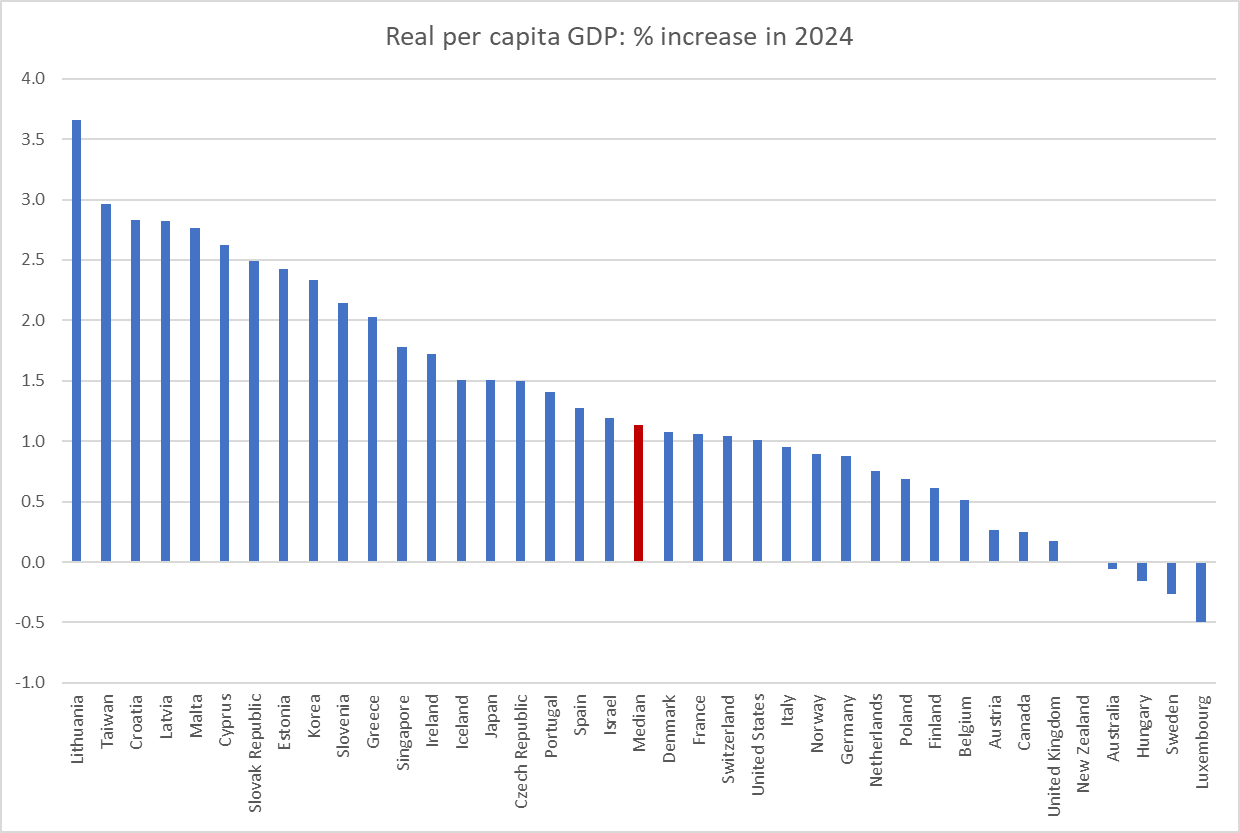

First, we look at the Fund’s forecasts for real per capita GDP growth.

In calendar 2023

and calendar 2024 (I can’t highlight New Zealand – zero growth – but we are fifth from the right)

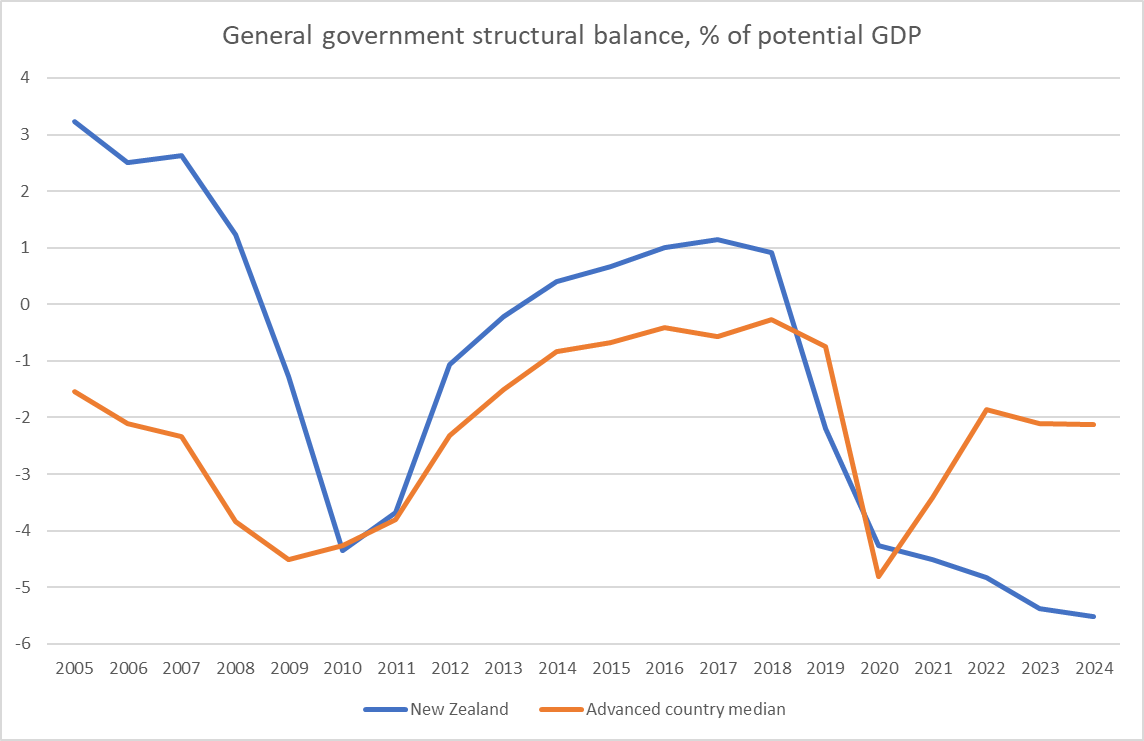

What about fiscal policy? The IMF has actuals and forecasts for the general government structural balance. We used to be better than most advanced countries. But that was then.

For calendar 2024 alone (for 2023 we are a couple of places less bad). These numbers seem very consistent with the IMF cyclically-adjusted primary deficit estimates in their recent Article IV review of New Zealand.

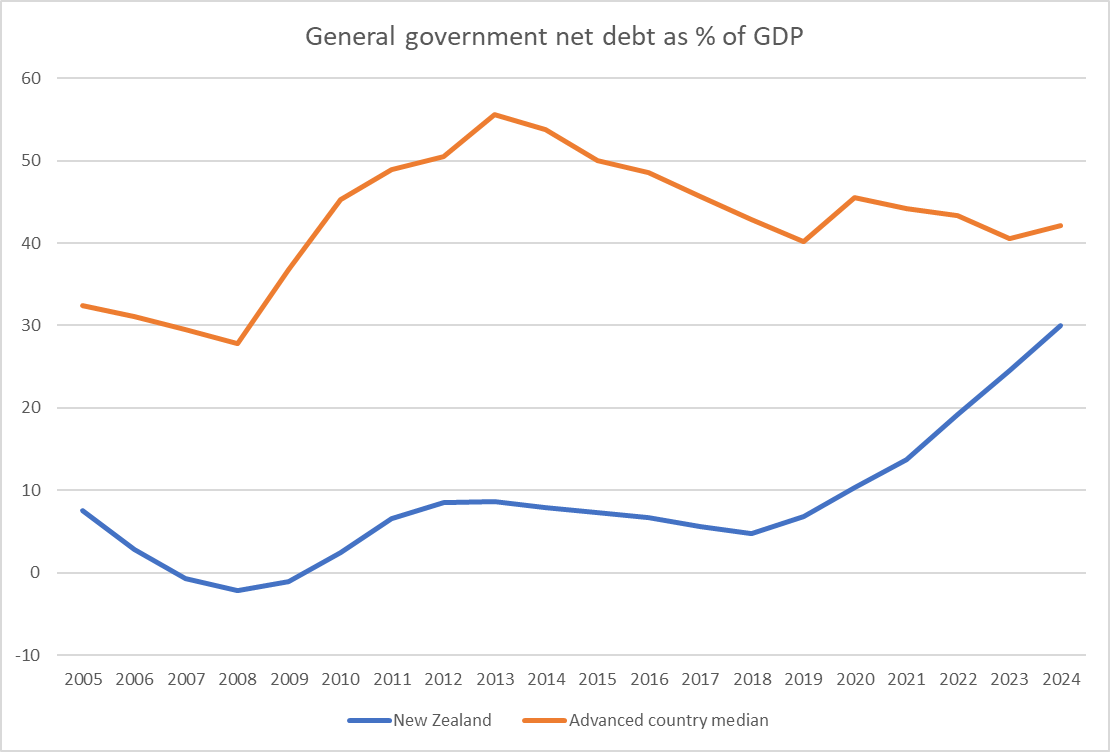

What of net general government debt?

We do still have government debt as a share of GDP less than the median advanced country, but that gap is closing fast. You’ve heard a lot in this election campaign about the pandemic: other countries had one too.

And what of the current account deficit? There is no right or wrong number for a current account deficit. Huge surpluses or huge deficits can both be symptoms of things going right or wrong. Context matters. In a country with rapid productivity growth and lots of business investment, catching up with the rest of world, really large deficits make sense. That was Singapore and South Korea in their earlier development phases, or 19th century New Zealand.

In 2023, New Zealand doesn’t have the largest deficit as a share of GDP, but it is close. (We had the third largest deficit last year and are still forecast to be second largest next year.)

All in all, it didn’t really make encouraging reading.

Where do we look for some comparative figures for China?

LikeLike

https://www.imf.org/en/Publications/WEO/weo-database/2023/October

In the same database

LikeLike