As far as I can see reaction to last week’s Budget seems to be split between those on the government side who thought it was great – in some cases just a start – and on the other side of politics those noting that there was no sign of any sort of plan or set of policies that might lift the economy’s productivity performance, and in turn lift the capacity – whether or individuals or governments – to spend on personal or collective priorities. Those critics are, of course, right.

But what I really wanted to focus on in this post is the size of the deficit the government is choosing to run.

Little more than four years ago the Labour and Green parties published the Budget Responsibility Rules that, they told us, would guide them should they take office (I wrote about them here). They were seeking to persuade us that in office they would prove to be responsible macroeconomic and fiscal managers.

The first of the rules they offered up was this one.

Note especially that second sentence: they expected to be in surplus every year “unless there is a significant natural event or a major economic shock of crisis”. Pursuing other policy priorities wasn’t going to be an excuse either: if they thought they needed to spend more on this or that, they’d fund it by taxes.

It sounded pretty good.

Even before Covid, if they were sticking to their own “rules” it is was a pretty close run thing. In the HYEFU for December 2019, for example, the total Crown OBEGAL measure in (very) slightly in deficit was for 2019/20 and exactly in balance in 2020/21. The same set of forecasts showed the economy running just a bit above potential in those two years. It wasn’t exactly the spirit of the Budget Responsibility Rules.

And then, of course, Covid came along. I don’t think anyone is going to dispute the idea that deficits (even large deficits) made sense for much of last calendar year, particularly to support the incomes of those unable to work because of lockdowns etc, Not many people are disputing the case for the wage subsidy, and of course when people couldn’t work and businesses couldn’t trade tax revenue was also going to be down. You’ll recall that the worst of all that was in the March and June quarters of last year (part of the fiscal year 2019/20). Consistent with that core Crown expenses in 2019/20 was 34.4 per cent GDP, compared with 28 per cent the year previously. Whichever deficit measure you prefer, the 2019/20 deficit was large. And few will quibble about much of that.

Right now we are coming to the end of the fiscal year 2020/21. Wage subsidies and similar measures have been used at very stages, especially early in year.

But as everyone also knows, the economy has bounced back more strongly that most (including me) had expected – notably, much faster than the official agencies had forecast. It is, of course, entirely right to note that the borders are still largely closed, global supply chains are disrupted, and prospects in parts of the wider world still look pretty shaky. On the other hand, the terms of trade are doing really well. In total, Treasury does the forecasts, and they reckon that when we finally get the nominal GDP data for the year to June 2021 it won’t be much different in total than they had thought back in late 2019 pre-Covid. The comparison is a little unfair, since there were some historical SNZ base revisions, but they also reckoned (when they did the forecasts in late March and early April) that the June quarter unemployment rate this year would be less than 1 percentage point higher than they’d been forecasting for that date back in late 2019.

That’s great, something to celebrate. But it doesn’t have the look or feel of a “major economic shock or crisis” – Labour’s 2017 words. There was one, especially in the first half of last year, but from a whole economy perspective it has an increasingly been a stretch to make such a case as 2020/21 drew on. And yet core Crown expenses in 2020/21 are expected to have been 33.1 per cent of GDP, not much lower than in the previous year, and more big deficits have been racked up.

But 2020/21 is really water under the bridge now. There is only five weeks of that year to go, and the Budget is about policy for 2021/22 (in particular) and beyond.

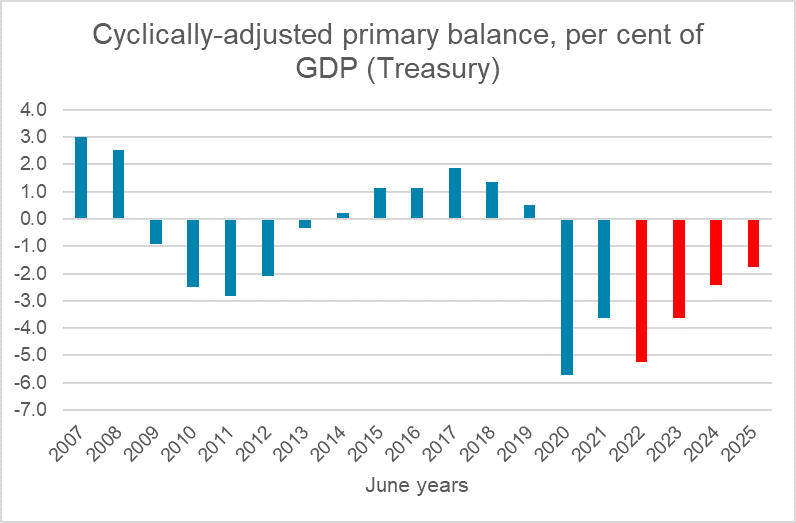

And in 2021/22 not only is the government planning to run large deficits but ones that even larger than those for 2020/21. The Budget documents this year were rather light on the analytical material that Treasury usually publishes, but they put in this year a chart of the cyclically-adjusted primary balance.

Cyclical-adjustment here involves Treasury adjusting for the state of the economic cycle (recessions dampen tax revenue quite a bit and raise spending a bit, as the automatic stabilisers play out). In this chart, the Treasury also exclude the EQC/Southern Response Canterbury earthquake costs. And the primary balance excludes finance costs – it is a standard measure used in fiscal analysis, with a common rule of thumb being that if your primary balance is positive, at least you aren’t borrowing simply to pay the interest on the accumulated debt. Labour’s 2017 commitment re surpluses would have implied running positive primary balances almost every year.

There were significant cyclically-adjusted primary deficits in the years following the 2008/09 recession – the twin consequence of the fiscal splurge at the end of the previous Labour government’s term and the unexpected (by Treasury, whose forecasts governments use) shortfall in potential output. But those cyclically-adjusted deficits over 2010-2012 look small by comparison with the deficit the current government plans to run in 2021/22 (and still smaller than what they are planning for next year).

Perhaps you might think the state of the economy in some sense warrants this, but (a) recall that these are cyclically-adjusted numbers, and (b) check out the state of the economy in the two periods. Over the coming year Treasury expects an average output gap of 1.7 per cent of GDP, coming back to zero in 2022/23. They expect the unemployment rate to be about 5 per cent next June, dropping to around (their view of the NAIRU) 4.4 per cent the following June. By contrast, Treasury now estimates that the output gaps in the 2012/13 and 2013/14 years were each around 1.5 per cent, and the unemployment rate in both years was also higher than they expect in the next two years.

What about some longer-term perspectives? I can’t see a Treasury version of this series going further back but (a) the OECD publishes estimates of the cyclically-adjusted primary balance at a general government level, and (b) the Treasury has primary balance (not cyclically adjusted) back to 1972. Neither series is fully comparable – the OECD numbers aren’t done on an accrual basis, and include local government (but it is small in New Zealand), and the older Treasury numbers aren’t cyclically adjusted. But together they can still create a useful picture.

Here is the OECD chart, back to 1989

Cyclically-adjusted primary surpluses have been the New Zealand norm in modern times – even (a propaganda line Grant Robertson could have chosen to use, but preferred not to for obvious reasons) in 1990.

And here is the not cyclically-adjusted primary balance numbers back to the year to March 1972, using the data from the Treasury’s long-term fiscal time series.

Note that although these numbers are not cyclically-adjusted, even in quite severe recessions the cyclical-adjustment procedure Treasury uses makes a difference of less than 2 percentage points of GDP.

So, one might reasonably note that over the next couple of years when, on Treasury’s numbers, the economy will be running increasingly close to full employment, the government is choosing – wholly as a matter of discretionary policy – to run a primary deficit bigger than any that have been run in the past 50 years, with the exception only of the accrual effect of the government’s EQC obligations post-Christchurch, obligations that were not discretionary or voluntary at that point. To be pointed, one might reasonably note that the primary deficits are (far) larger than any run under Robert Muldoon’s stewardship (the first two years on the chart, as well as 1976-84), and are in contrast to the primary surpluses run in every single year of the Lange/Palmer/Douglas and Clark/Cullen eras.

(What about those big Muldoon era deficits you keep reading about? Actually, a huge chunk of that was interest costs, and much of that was just inflation – real interest rates themselves were often quite low. Another way of looking at the issue is an inflation-adjustment to the deficits.)

It seems like pretty irresponsible opportunistic fiscal policy to me. It is certainly inconsistent with those mostly-admirable Budget Responsibility Rules Labour campaigned on – since not only are they running large deficits with no macroeconomic crisis, but debt is above their own targets.

Of course, from supporters of the government I expect there will be two responses.

The first might be to celebrate – Robertson and Ardern have thrown off the shackles, scrapping (as they formally have) any references to surpluses or balances budgets now or in the future. What is not to like, surpluses or balanced budgets being things for people like Clark, Cullen, Kirk, and Rowling, but not for our brave new leaders. After all, don’t we know that interest rates are low – even if long-term rates now are no lower than they were pre-Covid. If so, it is a dangerous path they are treading: their cyclically-adjusted primary balance outlook now looks a lot more like the sort of ill-disciplined approach to fiscal management we’ve seen in places like the UK, the US, and Japan over recent years. That was already underway with the various permanent fiscal measures the government put in place as early as last March (under the guise of a Covid package) and has continued since.

The second, more moderate, stance might be to acknowledge my point but to argue that (a) the economy is only doing as well as it is because of macroeconomic stimulus, and (b) better fiscal policy than monetary policy. I’m not going to dispute that policy stimulus is likely to have helped achieve the welcome economic rebound, and (more specifically) if the government had taken steps in this Budget to (say) cut the cyclically-adjusted primary deficit to 2 per cent of GDP in 2021/22, closing to zero the following year (while reserving the need for possible fresh intervention if Covid got loose here), the economic outlook would – all else equal – be worse than is portrayed in The Treasury’s forecasts.

But all is not equal. The primary tool for macroeconomic stabilisation is monetary policy. A tighter fiscal policy – getting back to balance quickly now that last year’s shock has passed – would naturally and normally be offset by monetary policy, doing its job. The Bank stuffed up going into Covid and wasn’t then able to take the OCR negative (or so it claimed), but even they tell us that is an issue no longer. For those who believe in the potency of the LSAP – and I think all the evidence is against it – there is that tool too. And the beauty of monetary policy is threefold:

- it costs the taxpayer precisely nothing (relative price shift instead and those best placed to respond do),

- it can be adjusted very quickly as the outlook and circumstances change, and

- using monetary policy tends to lower the exchange rate while reliance on fiscal policy feeds an overvalued exchange rate, skewing the economy further inwards.

Monetary policy is, of course, no good at income relief. That is what fiscal policy did so well last year. But that was last year’s need not – as Treasury’s forecasts – the need now or for the next couple of years.

My unease about the Budget is not helped when I dug into some of the macroeconomic numbers.

For example, The Treasury’s forecasts for growth in the population of working age show expected growth in the five years to June 2024 exactly the same now as in the projections for the 2019 HYEFU. Perhaps, but it seems a bit of a stretch, when we know – from Customs data – that there has been a significant net outflow of people (migrants, tourists, New Zealanders, foreigners) over the last 17 months.

And then there are the Treasury’s productivity growth assumptions that seem heroic at best.

And this even though their text explicitly refers to some degree of permanent “scarring” as a result of Covid. Perhaps they could enlighten us as to what about the economic environment or economic policy framework is likely to generate such strong productivity growth (by New Zealand standards) in the next few years? Covid isn’t something the government can do much about, but nothing else in their policy programme now or in recent years seems likely to begin to reverse the lamentable New Zealand productivity performance. Without that productivity growth, future revenue growth would also be weaker than this Budget is built on.

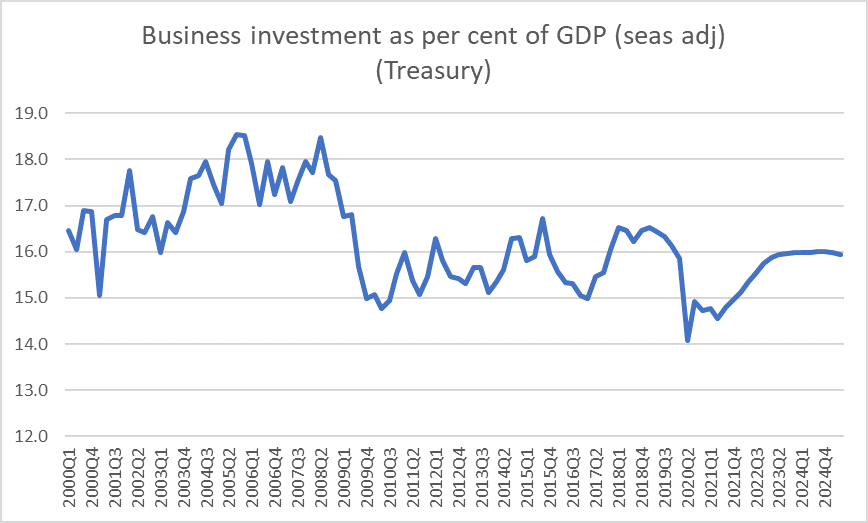

It isn’t as if The Treasury expect business investment to soar. At best The Treasury seems to think we limp back to the rates of business investment seen in the previous half decade (when the Governor of the Reserve Bank was exhorting firms to invest more, as if he knew better than them where the profit opportunities lay).

And then there is one of my favourite, but sad, charts

Exports and import shares of GDP both rebound, of course, but only to settle at even lower levels than we’ve seen in New Zealand for decades. Successful economies tend to be ones that are exporting successfully lots of stuff to the rest of world and importing lots of stuff from the rest of the world. That isn’t New Zealand. But then we haven’t been a successful economy for a long time now.

Perhaps fiscal policy will come out okay in the end. But when the government isn’t expecting to be back in cyclically-adjusted primary surplus even by 2025, and when the medium-term economic projections seem to rest on some rather rosy assumptions (these and others), it is difficult to be optimistic. Thirty years of sound fiscal management – one of the few real successes New Zealand economic managers could claim – looks to be at risk. And yet the grim fiscal outlook seems to have had astonishingly little coverage, as if last year’s (appropriate) mega-deficit numbers have disoriented people so far that they’ve lost interest in the hard slog of delivering balanced (cyclically-adjusted) budgets. The appropriate size of government – perhaps even the appropriate degree of dependence on government – is rightly the stuff of political debate, but what is spent should be paid for, not simply grabbed from the population – reducing their future spending options – without the normal political conversations around what tax rates are tolerable and acceptable.

Something something “recovery” something I believe was the answer to your question “What about some longer-term perspectives?”

Treasury’s productivity predictions should be publicly shamed for their persistent wrong-ness. They’re making economists look bad.

LikeLiked by 1 person

“Making economists look bad”

… now that takes some doing!

LikeLike

The Wage subsidy was a $13 billion spend up which covered the loss of the spend by International tourists and international student was $15 billion a year in NZ. If you add in other government spending from the RBNZ $61 billion Treasury bond buying activity which pushed up overall government debt to an extra $41 billion, And not to forget Kiwis that are not travelling who do spend as much as $8 billion outside of NZ it is no wonder the NZ economy was a rather smooth sailing over troubled Covid 19 lockdowns.

The problem is this year and subsequent years with the slow roll out of the vaccine and the slow border re-opening. That loss of $15 billion annual spending by tourists and international students will start to bite will only have cover from the Kiwis not travelling of $8 billion. Thats a net loss of approx $7 billion and the roll on effect could mean $12 billion loss from the NZ economy. Thats a serious recession in any economists books.

LikeLike

Nice commentary Michael.

I think when economic historians revisit this period post-GFC they will be appalled at the succession of bad decisions made by our policymakers. Focus seems to be entirely on the income statements/flows with no serious thought given to balance sheets/stocks and long run dynamics.

I note The Treasury intended to publish its long term fiscal projections in March 2020 but this was now pushed out to September 2021. Why?

Wellington was disrupted by COVID for two months last year but the disruption there has long been over. I think Grant owes us an explanation as to this:

“The Treasury now intends to publish the 2020 Statement before the end of September 2021.” – New Zealand Treasury

LikeLike

I’m generally quite sceptical on the value of the long-term fiscal statement (this was a post looking forward to the scheduled March 2020 one https://croakingcassandra.com/2019/11/07/long-term-fiscal-choices/ ) but there is probably a defensible case that we are better off getting a statement this year – when there has been some time to assess where we stand post-Covid, than having put out something largely based on pre-Covid (and thus low debt) starting point. GIven that fiscal policy is now unanchored – no debt target, no surplus target – it will be interesting to see what they come up with.

LikeLike

Thanks Mike I reckon your analysis proves my theory that Politicians & Bureacrats know nothing and understand less.

LikeLike

Not too sure that Jacinda Ardern knows nothing because it was quite clear that just last week that she was very definitely a democratic socialist in her speech. What was surprising was then a few days later the Chinese Premier Li Keqiang spelled out that the Chinese government is Socialist with Chinese characteristics. No doubts NZ and China are the very best socialist mates

“We must rally more closely around the Party Central Committee with Comrade Xi Jinping at its core, uphold socialism with Chinese characteristics, and follow the guidance of Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era.”

https://news.cgtn.com/news/2020-05-22/Full-text-Premier-Li-s-speech-at-the-third-session-of-the-13th-NPC-QHaP1FpB8k/index.html

LikeLike

Does your chart of ‘Exports and Import shares of GDP’ showing low expectations simply reflect the planners guess that international tourism will not recover?

LikeLike

Probably some of that and some extrapolation of the trend, given they expect the exchange rate to stay high.

LikeLike