In yesterday’s post I outlined some of my concerns about the government’s Budget, from a macroeconomic perspective. Not only did it seem to be built on rather optimistic medium-term economic assumptions, but several years out – on current policy advised to it by the government – The Treasury still expects a fairly significant cyclically-adjusted primary deficit (which means, once finance costs are added in, a larger-still overall cyclically-adjusted deficit).

There was a good case for such deficits last year, and perhaps even in the year that ends next month. But there is no obvious macroeconomic reason for running larger deficits in this coming year, and still having cyclically-adjusted deficits four years hence (by which time The Treasury numbers project a non-trivial positive output gap). It is now simply a splurge – a government that, unnecessarily, is simply choosing to take on more debt to fund its new spending, rather than fund core operating spending with taxes. In a climate when risks abound.

And all this is an environment where fiscal policy now appears to be unanchored by any specific fiscal goals a government is committing itself too.

I’ve never been one of those who put huge weight on the Fiscal Responsibility Act 1994, now (as amended) incorporated as Part 2 of the Public Finance Act. There are some good aspects to the legislation but I was never really convinced that asking governments to set out their specific short and long-term fiscal objectives, or articulating in statute “principles of responsible fiscal management” would make much difference to anything that mattered about the conduct of fiscal policy. (Here is a post on the 30th anniversary of the Public Finance Act critiquing some rather over the top claims then made for the framework.) In my take, there was a shared commitment across the main parties to balanced budgets (in normal times) and low debt, and the legislation reflected that rather than driving it.

And I guess I take this year’s Budget as vindication of that stance. There was a shared commitment to such things, and now it appears there is not. And the legislation still sits on the books, lonely and overlooked. Check out the requirements of Part 2 of the Public Finance Act, and then compare it with this year’s Budget documents. In particular, have a look at the statutory principles for responsible fiscal management, and the requirements that a Fiscal Strategy Report brought down on Budget day has to contain outlining both short-term and long-term fiscal objectives.

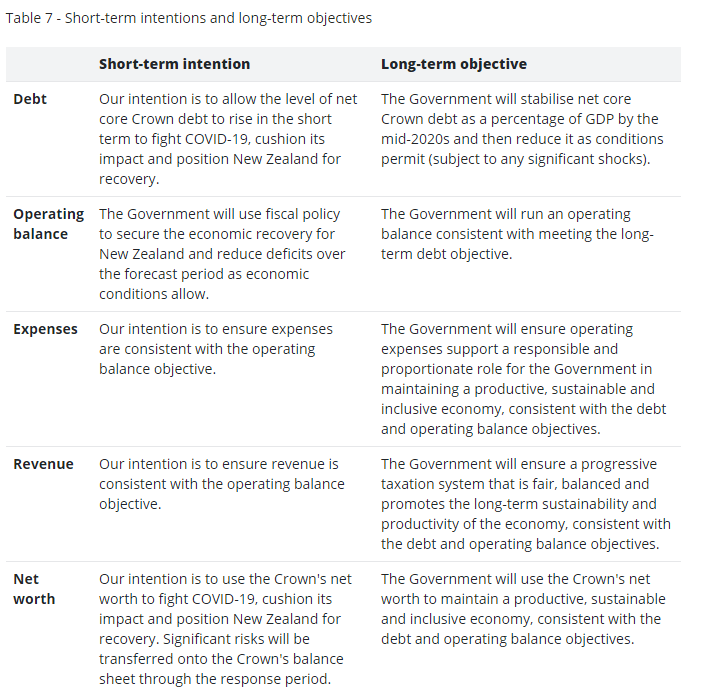

And then go and check out the vestigial thing the Fiscal Strategy Report appears to have become. Here is the statement of the government’s fiscal intentions.

Take the long-term intentions first (if you can find them). For debt, the government offers no numbers at all – either as to the level they aim to first stabilise the debt at or the longer-term level they would aim to then reduce it to (not even whether that level is higher or lower than the current level). Not even anything conditional on, say, us avoiding future Covid outbreaks and new lockdowns.

And then what about the operating balance? Well, they assure us they will run an operating balance consistent with the long-term debt objective, but (a) isn’t that obvious?, and (b) it tells us nothing at all, since they give us no medium to long term debt objective. And all the rest of it is equally or more vacuous. Now, sure, the Act does not formally require the government to put numbers on their objectives in these areas, but I’m pretty sure the drafters of the Act – the Parliament that passed it – did not think that simply stating “we’ll do whatever we like to pursue our political objectives” (all that “productive, sustainable and inclusive economy” mantra) would meet the bill. The whole section of the Act is rendered empty and futile.

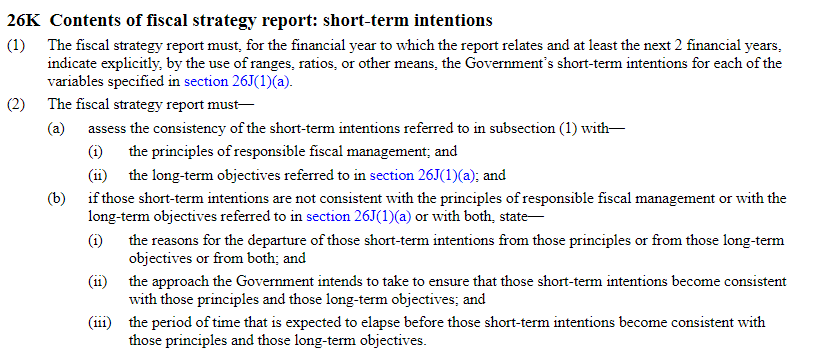

It is even worse when we get to the short-term intentions. The Act is somewhat more prescriptive there

And there is simply none of that content at all. No objectives, no serious discussion reconciling with the (non-existent) long-term objectives, and just this explanation for why the government is (for now anyway) abandoning the statutory principles for responsible fiscal management

Doing so in this case for the short-term operating balance intention is the right thing to do, given the unprecedented size of the global economic shock caused by COVID-19 and the need for the Government to provide a strong ongoing fiscal response to protect lives and livelihoods in New Zealand as we secure the economic recovery.

But as I suggested yesterday, that argument probably made sense (at least the first half) at the time of last year’s Budget and FSR. It doesn’t today when New Zealand’s unemployment rate is under 5 per cent.

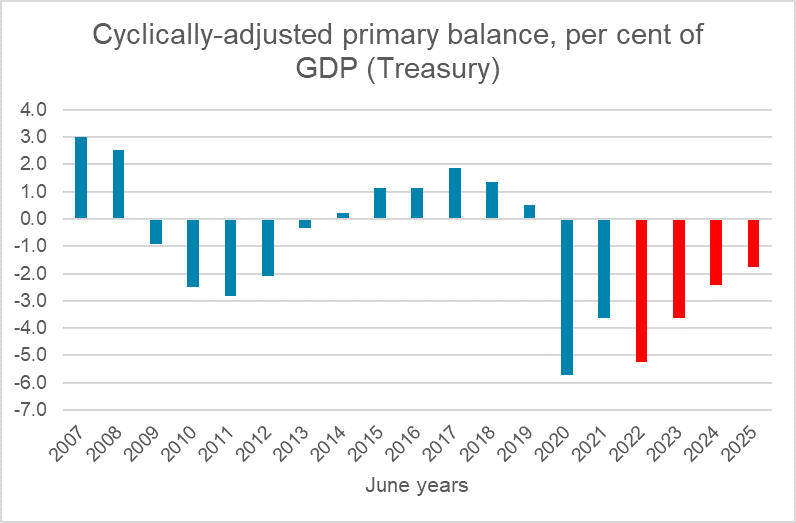

There is no rationale – grounded in the Act – no analysis, and no short or medium goals. Simply structural deficits for years to come (see first chart above) – discretionary deficits actively chosen by today’s government larger than any such cyclically-adjusted deficits run in New Zealand at any time since at least the end of World War Two. It hasn’t been the New Zealand way. But it appears to be so now.

As I noted yesterday, maybe it will all come right. Maybe Robertson and Ardern really are at heart a bit more responsible than this Budget suggests and future new spending splurges (which are, I guess, what one expects from a party whose MPs and leader have now taken to openly calling themselves “socialists”) will be funded by persuading the electorate to stump up with increased taxes.

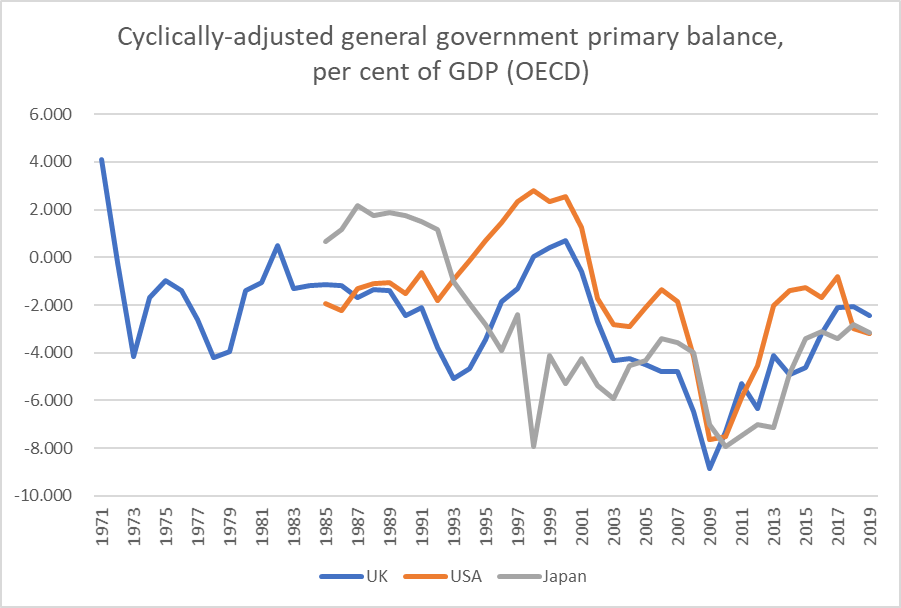

But bad fiscal outcomes – high debt, and little obvious prospect of reversals – don’t arise overnight. And the sort of thing that concerns me is what has happened in some other advanced countries. Here are the cyclically-adjusted primary balances for the US, the UK, and Japan. Remember, a positive number should be a bare minimum for prudent fiscal management (higher the higher are your accumulated debts and the prevailing real interest rate).

30 years each had relatively low levels of government debt (OECD data for net general government liabilities as per cent of GDP), the UK and Japan in particular. And now they are all among the OECD countries with the highest levels of (net) public debt.

It can happen here too. And if those on the left are celebrating this week their own government “breaking free” of the shackles, they need to remember that political fortunes come and go. The other parties will form governments again, and the precedent this government is setting may guide them in how constrained they feel about increasing spending or cutting taxes or whatever (see the US as an example). In a floating exchange rate economy the disciplines on fiscal policy are more political than market in nature. If your party believes in bigger government, that’s a choice but then insist that bigger government means higher taxes. If your party believes in much lower taxes, that too is a choice, but then insist that smaller revenue have to mean much lower spending. But don’t toss out the window a hard-won consensus around balanced budgets and low public debt – one of the few real achievements of the last 30 years – and substitute for it feel-good politics (whether from the left or right) that avoids confronting choices about who will pay.

I’m still reluctant to believe that Robertson is quite as reckless as this Budget suggests, but for now at least the evidence is tilting against my optimistic prior. And, disconcertingly, there isn’t much sign of the Opposition calling him out.

This, incidentally, is the sort of analysis and discussion that a Fiscal Council provides in many countries.

It might be instructive to compare and contrast New Zealand and Australia. One source of the thinking on this from across the Tasman is the traditional address by Secretary Kennedy to the Australian Business Economists. https://treasury.gov.au/sites/default/files/2021-05/210518-drkennedy-abeaddress.docx. Ideally we would use comparisons of cyclically adjusted balance – but this is made more challenging by the different measurement approaches of the measures in NZ vs Australia.

2020 2021 2022 2023 2024 2025

New Zealand OBEGAL -7.3 -4.5 -5.3 -2.6 -1.4 -0.6

Australia (cash balance) -4.3 -7.8 -5 -4.6 -3.5 -2.4

Australia (fiscal balance) -4.9 -7.9 -4.8 -4.6 -3.5 -2.7

LikeLike

Thanks. I’m not sure it makes the NZ govt’s strategy look any more appropriate, including because Australia’s was the pre-election splurge Budget. Bottom line: there is little or no credible case for unfunded operating spending (cyclical influences aside).

LikeLike

Incidentally while it is an interesting speech (and we have nothing comparable from ministers or officials here) much seems to rest on this line:

“Monetary policy has provided important support during the pandemic, despite the cash rate reaching the zero lower bound.

But there are limitations on how much more support monetary policy can provide. “

When what he really means is that the RBA board on which the Secretary is a full voting member refuses to cut policy rates further. Mercifully we do not face the same self-imposed constraint.

LikeLike

Hi,

Timber has gone up twice this year. I will make an adjustment to reflect the timber ingrease.

Thanks,

John Cooney.

LikeLike

With the cost of borrowing so low perhaps now is the time to borrow for capital / infrastructure investment. Core expenditure should be financed by taxes but capital can be financed by borrowings. The fact that borrowings go up as a percentage of GDP is of academic interest only, the real issue is what is the cost of borrowings in relation to the anticipated contribution to the economy of the infrastructure that they financed .

A meaningful number is the annual cost of borrowings as a percentage of the annual tax take.

LikeLike

Yes, can be fine to borrow for capex altho sadly quite a lot of govt capex is not robustly evaluated in the first place.

LikeLike

Given that the risk free rate ie usually the Treasury Bond rate is so low, most Capex projects should pass the usual evaluation threshold for NPV. Sadly NZ is so corrupt that even building a children’s park can have a budget blowout by 43%.

“Parliament’s new playground is a monument to extravagance and waste with revelations it cost $572,000 and went 43 per cent over budget.”

https://www.scoop.co.nz/stories/PA2006/S00147/parliament-playground-blows-budget.htm

LikeLike

It is not the project evaluation for Capex which is the problem. The problem is the corruption rampant in our government projects and services. As long as it is labelled a variation it makes it all so conveniently legal.

LikeLike

There are plenty of projects undertaken that did not stack up on a proper initial project evaluation, even with a weighted average cost of capital of 6 or 7 per cent.

LikeLike

The entire premise of the Australian budget seems different- better (with better targeted assistance for both business and social spending):

“Job creation was a key theme of this year’s Budget with benefits expected to flow to businesses across the sectors broadly via income tax relief, support for apprentices and trainees and business tax breaks targeting investment, along with significant spending in specific areas. Aged care, mental health and disability services will be major beneficiaries, while infrastructure will also receive a top-up”

(https://westpaciq.westpac.com.au/Article/48076/35806/)

LikeLike

Sounds right. I tried to avoid comment on the individual policy specifics of the NZ Budget – I don’t like most of them but then I’m not a “socialist” – to keep the focus on the bigger picture (deficits and the PFA).

LikeLike

Hi great rreading your post

LikeLike