The Governor of the Reserve Bank is always keen to tell us what an important contribution the Reserve Bank is making through its large-scale asset purchase programme (LSAP). Recall that the Bank cut the OCR by 75 basis points and then gave up on using conventional monetary policy – promising (in one of the weirdest pledges in the history of modern monetary policy) to do no more for 12 months, come what may – in favour of buying lots of (mostly) government bonds. At present, the MPC has authorised the Bank to buy up to $60 billion of bonds, and there is speculation from some banks that that total may even be raised further at the next Monetary Policy Statement in August. The Bank claims – as it did in the MPS last week and at its appearance at FEC the next day – to be making a big difference, but it is mostly a smoke and mirrors show. There are big numbers involved, but the differences being made to things that might matter economically are really rather small.

Sadly, it seems to suit our very conservative and risk-averse Minister of Finance to believe – or acts as if he believes – the Bank’s story, even if by doing so he aids and abets an insuffficient macro policy response to the savage recession that is upon us. The macro consequences of his indifference probably won’t show up before the election, but even beyond that horizon in his entire term in office he has been remarkably deferential towards the Bank. It is if he is scared of doing what the economy needs.

It is fair to say that there has been an active debate over quite what these asset purchase programmes have achieved ever since they were launched. While I was still at the Reserve Bank I recall a couple of visits from Dan Thornton, then a senior researcher from the St Louis Fed, who presented versions of papers arguing that the Fed’s various asset purchase programmes really hadn’t made much sustained difference to anything. I was never fully convinced but if you’d asked me a year ago I’d have said that my summary impression was that earliest Fed programme – in the midst of the financial crisis – probably added some value, but that the later ones didn’t achieve much at all, perhaps beyond some announcement signalling. (The issues in Europe were a bit different, since breakup risk was in play). Long-term interest rates in the US, for example, hadn’t seemed to have fallen more, relative to the change in the policy rate, than we’d seen in New Zealand or Australia (which, to then, had not resorted to asset purchase programmes).

In truth that didn’t seem very different to the approach being taken by the Reserve Bank’s chief economist only two months ago. This was reported in the Herald on 13 March

That sounded – sounds in fact – about right to me. It isn’t, of course, the line that either Ha or his boss are running now. Instead, we get repeated suggestions – never quite pinned down with hard estimates or illustrations – that what the Bank is doing with the LSAP is some sort of fully adequate substitute for the sort of scale of OCR adjustment we’ve had in past serious recession (recessions which, it might be added, it has often taken years for the unenemployment rate to drop back acceptably).

Strangely, the Governor has found some supporters among the local bank economists. I presume they really believe what they are saying, but I still don’t find it very persuasive at all.

Much has been made of the claimed impact of the bond purchase programme on wholesale interest rates. But even there, the story isn’t particularly persuasive.

Typically, the biggest influence on longer-term interest rates is the expected future path of short-term interest rates. Why? Because, in principle at least, someone holding a 10 year bond has as an alternative investing in a series of 40 day 90 day bills. If the market thinks the short-term rates wil rise or fall materially over the life of the bond, that will influence bond yields themselves.

Sometimes, there is a serious recession, involving significant cuts in the OCR, but where the effect is expected to be quite shortlived; before long it is expected that the Reserve Bank will be raising the OCR again. If so, bond yields might not fall much, and in particular the implied forward interest rates (eg the second five years of a 10 year bond, backed out using yields for five and ten year maturities). That was more or less exactly how markets reacted in 2008/09.

It took a couple of years for markets to really begin to appreciate that future policy rates were likely to be low for some considerable time. This New Zealand experience wasn’t that unusual. In fact, it took a while for the Reserve Bank to learn – they’d actually started tightening in mid 2010.

But what about this recession? I’ve not seen a single serious commentator here or abroad – I’ll set aside the columnists who reckon we are now on an inexorable path towards Venezuela – who think there is any material chance of policy rates being raised any time in the foreseeable future (several years at least). By contrast, just a few months ago people were beginning about the possibility of OCR increases perhaps later this year or next year.

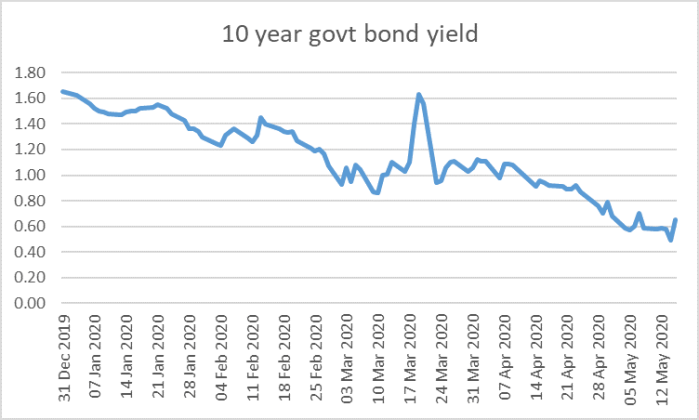

And yet even with all that Reserve Bank bond buying – actual and promised – the implied five year forward government bond rate hasn’t really fallen that much at all. It is down 80-90 since the middle of last year and 60 points since January. It just isn’t very much – look at the size of some of the past movements even just in the period of this chart – and all this against a backdrop of a 70-80 basis point fall in medium-term inflation expectations (whether one uses survey measures or market prices). Unfortunately, long-term historical swaps data isn’t readily available, but for the more recent period the picture is much the same: implied forward rates haven’t fallen very much relative to history, relative to the scale of the economic shock, or relative to the fall in inflation expectations. And yet it was this fall in swaps rates on which the Bank seems to pin its claims.

Ah, but what about the counterfactual? What would have happened if the Reserve Bank had not launched and then expanded the Large Scale Asset Purchase programme? The only fully honest answer of course is that we do not know.

The Bank likes to run the charts showing how bond yields surged upwards in late March, and then fell after it intervened with the LSAP.

The global rush to cash and liquidation panic was well-recognised. Quite probably, central bank interventions helped to stabilise things. But that is a different proposition from a claim – which is the one the Bank and its supporters are making – that the current level of yields, six weeks on, is being very materially influenced by central bank purchases. One could mount a counterargument that where yields are now isn’t much different than where they might have been anyway given (a) the OCR being stuck at 0.25 per cent for now, and (b) the economic situation having got a whole lot worse than it was, say, on 16 March, and (c) medium-term inflation expectations having fallen quite a bit further.

One might say the same looking at this chart of the swaps yield curve on various dates.

The grey line was the peak in rates amid that flight to cash that most severely affected te bond market. But again, compare the 16 March line (the day the Bank cut the OCR) with the latest observation last Thursday. It has the feel of the sort of fall – concentrated over the front five years – you might have expected if you’d been told that in the interim the economic situation had got so much worse and inflation expectations had fallen materially.

But, again, the counter-argument will come: what about all those fiscal deficit and the big volume of debt issuance coming down the track? To a first approximation, my response is “what of it?”.

First, recall what else is going on. Investment demand has slumped and is likely to remain lower than it was for several years. And private savings preferences also appear to have risen. So if we are thinking about what might be expected to happen to interest rates – even if the Reserve Bank were buying nothing – we have to think not just about what the government is doing but about the private sector. Money is, after all, fungible. Absorption, frankly, seems unlikely to have been an issue, in a very lightly-indebted sovereign – even if the Reserve Bank had not done any LSAP.

Gross public debt as a share of GDP is now projected to rise by 30 percentage points between last year and 2023/24. But it isn’t as if big increases in public debt have never been seen before. In fact, the last time was only a decade or so ago, when gross public debt as a share of GDP rose by 20 percentage points between 2008 and 2012. There was no asset purchase programme then and – as illustrated above – once markets became convinced that the OCR would have to stay down for a while, it wasn’t enough to stop implied forward rates falling a long way.

And how much would we expect changes in government debt to affect interest rates, absent central bank intervention? Views will differ on that, but the Governor did write about exactly that issue in his relative youth, publishing empirical estimates drawing on work he’d previously been part of at the OECD. Perhaps the Governor has changed his view since 2002, but then he estimated that 30 percentage points on net debt might have been worth perhaps 15 basis points on bond yields, all else equal (which it decidedly isn’t right now, with very high levels of excess capacity).

Another point worth bearing in mind is that even the Reserve Bank will, I think, concede, that very long-term interest rates just don’t make that much difference to many people in New Zealand, other than just lowering the government’s own financing costs. The marginal activity in the residential mortgage market, for example, is typically around one and two year fixed rates. And yet the data on the Bank’s LSAP shows that more than two-thirds of all the Bank’s government bond purchases have been for maturities of 2027 and later. So even if those purchases are having a material impact on those very long-term rates, so what? To what end? As it is, we know that shorter-term fixed rates have hardly fallen at all in real terms – what one might have expected with a small, badly lagging, OCR response, not with all the power the Bank asserts its balance sheet purchases can have.

Perhaps also the Bank is right that there has been some helpful exchange rate effect, and we do not know the counterfactual. But we do know how much the TWI has often fallen in past serious recessions, and it is much more than anything we’ve seen to date this time. The LSAP might be a little better than nothing, but it is no substitute for the OCR the Bank is now so reluctant to use.

Are there other possible channels where there might have been an impact? A commenter last week noted that perhaps equity markets were higher as a result? Perhaps, although the effect must surely be small, but equity markets have always been seen as much less important a part of the transmission process here than in, notably, the US. The Bank and its supporters have also been talking up portfolio balance effects – in other words, the people selling bonds to the Bank have to do something with the money that is freed up. Again, perhaps there is some small effect, but it is difficult to see where such material tangible effects might be. For example, I’ve seen this chart a couple of times in ANZ publications

It is a useful chart (altho perhaps with a line missing?), with data on corporate bond yields that those of without a Bloomberg terminal can’t otherwise easily track. The Reserve Bank doesn’t buy the corporate bonds, but purchasing government bonds may displace some holders into corporate debt. But, again, count me fairly sceptical that the ongoing LSAP programme is explaining much about the current level of these yields, given (a) weakening OCR expectations, and (b) the weakening economic environment. It is hard to be sure, but it is hard to believe that any effect is very large.

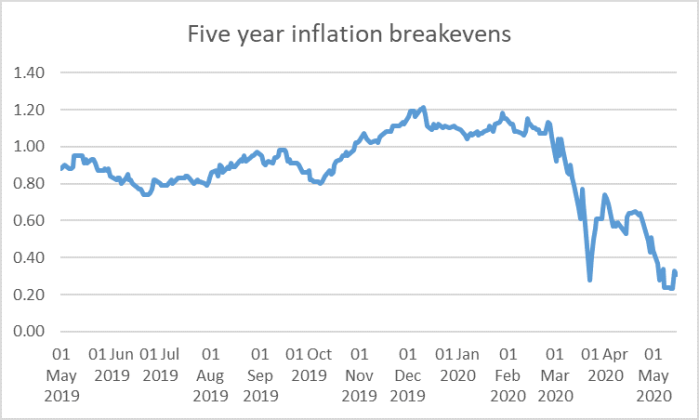

We don’t have real-time inflation data, but we do have near real-time proxies for inflation expectations – and especially changes in them – from the inflation-indexed government debt market. When implied inflation expectations for the next five years on average have fallen by about 80 basis points (measured imprecisely, so call it anything from 70 to 90 points) in just a couple of months

it is not a sign of a central bank that is doing its job well, of a central bank whose instrument is doing what needs to be done, even allowing for all the fiscal support as well. If we had a Minister of Finance who really cared about macroeconomic stabilisation he’d insist on change.

A deeply negative OCR, generating retail rates near-zero (consistent with what the governments is lending to SMEs at) is more like the sort of monetary policy stance we need, one that might make a real and sustantive difference to inflation, inflation expectations, output and (un)employment. What we have at present is theatre – arguably doing little harm and perhaps a modicum of good, but successfully (it appears) from the Bank’s perspective distracting from where the real gains might be had.

Good work………..Perhaps the choice of QE as opposed to deeply negative rates is linked to the fact the RBNZ will effectively financing the govt deficits over the next two to three years at 0% interest (interest payments received on RBNZ holdings will be paid straight back to the govt as part of the annual dividend).

And the bonds themselves can simply be cancelled when they reach maturity: one govt agency (Treasury) refusing to pay another (RBNZ)

Radically cutting the OCR to say, -2.5% and therefore being the world leader by a mile, might spook the horses….

So why pass up an apparent “free lunch” with a QE program ?

LikeLike

I’m glad you used the “apparent”. When all boiled down, the govt is borrowing from the banks at 0.25 percent ( the rate the RB pays them) while exposing itself to a high degree of interest rate risk.

The really odd thing is that the Bank could readily do both: negative OCR and LSAP.

LikeLike

There is no such thing as a free lunch. Someone pays for it. Interest rates have been falling but do not forget that every balanced investment fund including Kiwisaver will have 40% or more invested in bank savings. Borrowers gain but it is not the time to borrow as there is no revenue. Borrowing without a revenue stream is negligent trading which makes directors personally liable. No accountant in their right minds would encourage their Board of Directors to borrow at this time.

LikeLike

if the RBNZ is flooding banks with deposits/reserves to pay for its QE, why are the banks still paying 2.5% to raise term deposits from the public ? Surely the banks have more cash than they know what to do with ?

LikeLike

Cash isn’t the issue. Banks are subject to regulatory requirements that compel them to have a large proportion of their total funding in either retail deposits or fairly long-term wholesale funding. The cost of offshore long-term funding is still holding up quite a bit, so it is sensible for the banks to bid quite aggressively for retail deposits. One might be able to mount an argument for relaxing that regulatory restriction for the time being, but for now it is what it is.

LikeLike

Interesting to read commentary that the NZ government will need to ‘pay the debt back’ one day. But, the public debt stock will likely stay at new high levels in the hope the debt/GDP ratio will eventually fall? So, RBNZ holdings of government bonds – via the LSAP plan – eases ‘rollover risk’ during the period of rising debt/GDP ratio?

LikeLike

Maybe, altho debt maturities in the next five years are not particularly large and as NZ will still have one of the lower debt ratios of the OECD countries I’m sceptical that rollover risk would prove to be an issue. Of course, if private sector demand comes roaring back that will put upward pressure on interest rates across the board….but that would generally be a good thing, a sign of success.

LikeLike

Hi Michael,

I appreciate your expert commentary on this, and it makes sense to me as a layperson that negative interest rates are going to be far more effective than QE. However what do you make of the case that sufficient QE, together with credible commitments by a central bank, must be capable of getting inflation to target? There is a whole world of assets the RBNZ could commit to potentially buying as part of a “whatever it takes” approach. Inflation will get to 2% before the RBNZ owns the whole world.

LikeLike

Remember that the LSAP at present is really just an enormous asset swap: RB buys mostly quite long-dated govt bonds (at a time when, if anything, the govt should be lengthening debt duration) and in exchange issue a large volume of call deposits (settlement cash at the RB). That sort of exchange will never be transformative, even if it can make some useful difference at the margin.

Inflation could be got to target without further OCR cuts with a large enough fiscal policy commitment, focused not just on income support but on direct state purchases of goods and services, combined with a commitment from the RB not to offset those effects. Doing so might be inefficient, inequitable, skew the economy more inwards, and close of lots of future fiscal options (the strands to my argument favouring mon pol) but it would almost certainly work.

As per Friday;s post, I don’t think there is enough macro policy support, but relative to the scale of the issue QE is mostly theatre.

Could the Bank buy up all sorts of other assets and make a difference? Perhaps a little, but then you are really in fiscal policy territory, but where buying existing assets does less stimulation than purchasing newly produced stuff.

LikeLike