When I read yesterday’s OCR review release from the Reserve Bank, my first thought was actually about process. This was the first interim – ie between full Monetary Policy Statements – OCR review since the new Monetary Policy Committee took over responsibility.

The actual statement from the committee was about 175 words long. It was accompanied by the summary record of the meeting (“the minutes”) that was about 530 words long. That looks anomalous. When there is a full MPS (with projections), the minutes are – in normal times – not much more than a modest supplement. But when there are no numbers and the press release itself is so short, the minutes are always likely to be the main event. Given the way the Minister of Finance has chosen to set up the new system – “minutes” released simultaneous with the policy decision (not done in plenty of other countries), and minutes not generally conveying individual views – I wonder what the point is of having both statements on the occasion of interim OCR reviews. There is nothing in the press release that couldn’t quite easily have been included in the minutes (almost all of it is there anyway) and having two documents just opens up risks of conflicting wording or differences of emphasis (in this case, the minutes are clearer on the likelihood of another cut than the statement is), for no obvious benefit. It isn’t a big issue, but if I were in their shoes I’d be taking another look in the light of experience. As it is, when one document has three times as many words as the other, the focus of attention is likely to fall on the longer fuller document.

Having said that, (with a sample of only two cases admittedly) experience is already confirming that the summary record of the meeting is really just a long-form version of the policy statement (whether the OCR review one, or the first page of the MPS). I get that, for largely inexplicable (and unexplained) reasons, the Minister of Finance was keen on encouraging consensus decisions – not an approach we take, for example, in the appellate courts, when individual judges are responsible for their own views and free to express them – but the minutes we’ve so far really add nothing. Take the possibility of an OCR cut yesterday. This what they said, all of it.

The Committee discussed the merits of lowering the OCR at this meeting. However, the Committee reached a consensus to hold the OCR at 1.5 percent. They noted a lower OCR may be needed over time.

Wouldn’t a useful summary record have given some indication of the arguments members (perhaps only some) found persuasive in favour of a cut and the considerations that led them (by consensus) to conclude that it wasn’t an appropriate decision right now. There is no sense of richness to the discussion, no insight into the thought processes or arguments or models being used, just nothing. And this is early days, when presumably the Committee wants to put the best foot forward, to suggest real change, real gains in transparency. It was predictable that the new-look committee would probably become little more than a slightly different front window for the Bank’s longstanding preference to tell us only what they think we need to know, only when they want to tell us. It could have been different, even under the severe limitations of this legislation, but it would have been an uphill battle even with the right people – and there is now documentary evidence that several of the likely best people were simply excluded from consideration from the start. MPC members are free to speak publicly, but thus far none has. It is a shame, but it is what I pointed out in my submission on the legislation last year, that the monetary policy reforms always appeared more cosmetic than real.

As for the actual OCR decision, I think it was the wrong decision (although I wouldn’t make too much of the point). Data have weakened here and abroad, inflation is – and has persistently been – below target, the exchange rate is holding up, and there is little real prospect of a sustained reacceleration of growth or of inflation pressures. Oh, and market measures of medium-term inflation expectations are around 1 per cent, not 2 per cent. In that climate, being a little pro-active and cutting the OCR now looks to have been the better choice. It isn’t clear what the risks to moving would have been. It is only six weeks until the next MPS, but (a) the MPC won’t have a lot more domestic information between now and then (eg the labour market data come out only 27 hours before the next release, and won’t be properly incorporated – or in the projections at all) and (b) the way the global situation is going one can’t rule out the possibility that another cut could have been warranted by then. Then again, markets strongly anticipate central banks.

Perhaps the saddest bit of the press release was this plaintive, orphaned, line

Inflation is expected to rise to the 2 percent mid-point of our target range,

The Bank has been saying this for years. December 2009 was the last time annual core inflation (on the Bank’s sectoral factor model was as high as 2 per cent). There is no support offered for their view, either in the press statement or in the minutes, and no evidence even of any discussion to risks around the story. I guess anything is possible, but it simply doesn’t seem the most likely story any longer. The Bank’s former chief economist used to argue that they had to say this (that inflation was heading back to 2 per cent) because if they didn’t, it meant they should have been changing the OCR. Well, quite. But in these circumstances, the line should just have been quietly dropped – or some more analysis/argumentation provided to support their beliefs.

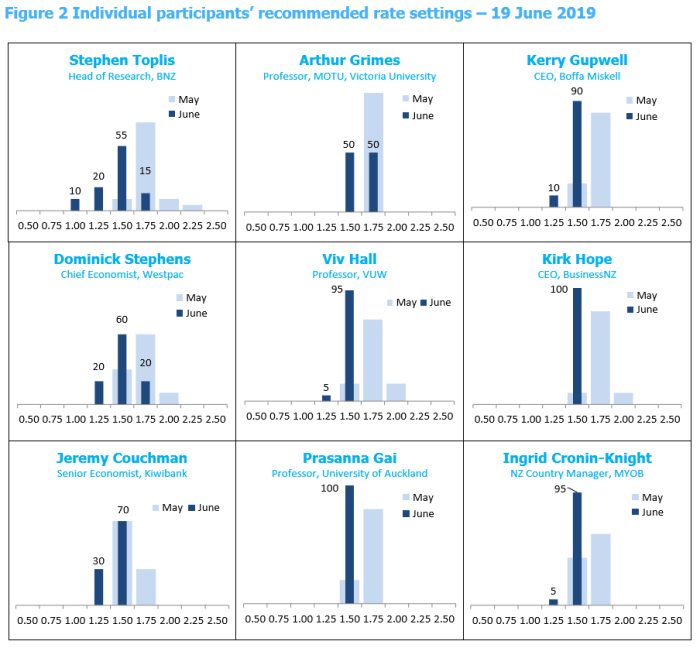

Earlier in the week, the NZIER released their Shadow Board exercise, in which a group of economists and business people offer their advice, and their range of views, on where the OCR should be set (conditioned on the target the Bank is given). I know various readers are dismissive of the exercise – and it does appear to be limping on towards eventual termination, rather than helping shape the debate – but I’ve always had a geeky interest in exercises like this, even while noting that the Shadow Board tends to adjust into line with the Reserve Bank, rather than providing much collective leadership or independence of perspective. This was in evidence in the NZIER press release this week

NZIER’s Monetary Policy Shadow Board has adjusted their recommendation in the wake of the Reserve Bank’s OCR cut in May.

It is strange that experts would adjust their view of what the OCR should be just because the Reserve Bank – with no monopoly on knowledge and huge margins for error – changed its view. But here were the individual views of the panellists.

I’ve always been puzzled too by how anyone could be 100 per cent confident of their view of where the OCR should be. When I was on the Reserve Bank’s OCR Advisory Group (a forerunner to the MPC), we introduced a survey of this sort, where each member’s advice to the Governor had to include a probability distribution (summing to 100 per cent) on what the OCR should be (eg 50% 1.5 per cent, 25% 1.25 per cent, 25% 1 per cent). Being a bit stubborn, and reminded of the breadth of the historic confidence intervals in OCR forecasts, I always tried to discipline myself to spread my probabilities over perhaps six alternative OCR settings, with not too high a probability on the OCR I actually recommended. Apart from anything else, it was a helpful prompt to think about what would invalidate my central view. Most of these respondents don’t seem to do anything similar. For what it is worth, my current distribution might look something like this

| 0.5 or less | 5 |

| 0.75 | 10 |

| 1 | 20 |

| 1.25 | 35 |

| 1.5 | 17.5 |

| 1.75 | 7.5 |

| 2 or more | 5 |

The most interesting view in the chart (setting aside how tightly bunched his views were) is that of former Reserve Bank chief economist Arthur Grimes, who indicated a 50 per cent probability that the OCR now should still be 1.75 per cent. In his comments he notes

Conditions imply no need to change the OCR right now, but that has to be balanced against the unnecessary (and unwise) cut to the OCR at the last decision. Hence it is a 50:50 call as to whether the cut should be restored or whether to leave the OCR as is.

It is an interesting stance, more “hawkish” (for example) than the (typically) most hawkish of the local banks (BNZ), and it is a shame no media seem to have asked Arthur to elaborate on his view. He must hold it strongly – the words are much more forceful than just the numbers would have been – and it would be interesting to read his fuller reasoning. After all, although my central view appears to be substantially different to his, the margins of error/uncertainty in this game are quite large enough that he could prove to be correct (my own probabilities – above – overlap with his). Perhaps it is just that Arthur is downplaying the target midpoint, even though it is highlighted in the target given to the committee, and in that case it is just a personal policy preference. But if it is a genuine difference of model, of making sense of current or prospective economic or inflation developments, it would be interesting to see his reasoning.

But for me, the downside risks, and the asymmetric nature of the consequences of being wrong – surprising high inflation means getting into the top half of the target range for the only time in more than a decade, while the approaching limits of conventional monetary policy mean that any further slippage in inflation expectations could really aggravate the next significant downturn, arguing for erring – if it all – on the side of a lower OCR.

“shadow boards” are a complete farce. None of these people really has any skin in the game. If I got my calls wrong, as one or two of these people have, consistently, for years, I’d lose my business and have to go back to being a bank economist (God Forbid!).

The market is the true test of expectations and the TIPS market and longer dates IRS (5y5y forward) are screaming at the RBNZ.

LikeLiked by 1 person

I had been tempted to mention you by name in the post Peter, but forebore (“I know various readers are dismissive of the exercise”)!

As someone with no real skin in the game, I will still stick up for the occasional value can be offered……..

all while not disagreeing at all with your bottom line.

LikeLike

There’s something very ‘Eurovision song competition’ about a shadow board. We don’t believe in market pricing because we know best…. quasi-totalitarian.

I was pondering this and your latest article on Gabs (personally I think the role in Ireland is made for him – no impact on anything) – and it’s really clear what the source of a lot of our problems actually is, it’s character. Our leaders seem to have a distinct lack of character; humility, honesty, openness to advice and willingness to accept responsibility, admit mistakes and learn from them. Personally, I’m quite happy to learn from others – better to hear painful words than to be banged on the head by life (or the market) – and admitting you’ve made a mistake isn’t humiliating, it’s liberating. Mistakes are part of life. For some reason, our leaders just can’t say “ok, I made a mistake”…

LikeLike

I know what you mean about the Irish job, but (a) I suspect there actually some power and thus risk around regulation of the domestic financial sector, and (b) altho no one at the ECB is likely to take him seriously,a troubled experiment like the euro has more standing/credibility when it has serious people – like Orphanides or Lane – as Governors of even small central banks in the system. Perhaps the summary: he might not matter much, but they should still have chosen (much) better. I haven’t seen a good account yet of why the strong female contender didn’t get the job (hardly like to be sexism from such a woke-lefty government).

LikeLike

Jacinda Ardern on the Nation, declared that she made a mistake on Kiwibuild. She usually refer to her pre election manipulation and lies usually as aspirational. This is the first time she has called her lies a mistake.

LikeLike

On the issue of transparency, Scott Sumner’s blog has a link to recent mercator article by Robert Hetzel ( https://www.mercatus.org/system/files/hetzel-rules-vs-discretion-mercatus-working-paper-v1.pdf ) on making monetary policy strategy more transparent. I hope the RB MPC reads this stuff….

LikeLike

What interests me is the reaction of banks following any reduction in the OCR.

The last move in Australia saw the Banks pass on some of the reduction but there was a surprising amount of criticism that they did not pass the whole amount on to customers.

There appears to be a reluctance in NZ to pass on any reduction so where is the benefit if banks don’t act when given a signal?

LikeLike

Don’t forget the exchange rate channel. Typically matters a lot.

LikeLike

Problem is Michael, that with the ToT strong, asset market volatility subsiding and rates coming down elsewhere it’s hard to engineer a weaker TWI. And if the US$ weakens, then kiwi may only have one way to go.

LikeLike

Indeed, but OCR adjustments are against some “all else equal” benchmark (ie cut the OCR and the TWI is likely to be a bit lower than otherwise).

Of course if the world really turns nasty, risk appetite is likely to turn strongly against the NZD, and commodity prices aren’t likely to hang up for long.

LikeLike

Our meat and milk exports to China seem to be escalating boosting China to our top export destination. Part of the reason seems to be this bubble tea drink and coffee culture that uses milk as a key main ingredient. Even in Auckland, Gong Cha bubble tea drink shops are popping up everywhere and customers drink it as a daily ritual 2 to 3 times a day.The serving cups are huge, looks like 800ml cup sizes.

LikeLike

Don’t forget that Household savings almost equal to Household debt. Our Australian banks make a higher margin being able to leverage against these savings. Therefore they need to keep savings interest rates high enough to attract savings that they can lend out.

LikeLike