Being a bit early for an appointment yesterday, I ducked into a secondhand bookshop and emerged with a history of Countrywide Bank (by Tony Farrington, published in 1997), to add to my pile of histories of New Zealand financial institutions and major corporates. For younger readers, perhaps unfamiliar with the name, Countrywide grew up from the building society movement, became a bank in the late 1980s after deregulation, and was taken over by the National Bank (itself later taken over by ANZ) in the late 1990s.

As I idly flicked through the book, I came across the account of one of those little episodes in financial history that (as far as I know) are not that well documented: the run on the building society, in April 1985. Literal physical retail bank runs – people queuing in bank branches and out onto the street – just aren’t that common. When there was a run on Northern Rock in the UK at the start of what become the widespread financial crisis of 2008/09, the story was told that it was the first retail run in the UK for 140 years. I am not sure if that is strictly true, but (fortunately) such runs are rare. Deposit insurance supposedly contributes to that, but so do well-managed banks.

In April 1985, it was still the very early days of the comprehensive new wave of financial liberalisation that had begun when the Labour Party had taken office the previous July. And it was only six weeks since the exchange rate had been floated, and five weeks or so since the extreme pressure on liquidity had seen overnight interest rates trade up towards 1000 per cent. One-month bank bill rates peaked at about 70 per cent, and three-month rates peaked at around 35 per cent before the Reserve Bank intervened to stabilise the situation. The overall level of interest rates had risen enormously (even post liquidity stabilisation) and anyone left sitting on (say) long-term government bonds faced very substantial mark-to-market losses. There was a great deal of uncertainty about who might flourish, and who not, in the new environment. And the newly-floated exchange rate was not exactly stable.

According to the Countrywide history’s account, in early April there had been rumours circulating for several days about the viability of Countrywide, which crystallised on Wednesday 10 April when an Auckland radio station ran a comment from one of their journalists that “there is no truth in the rumour that Countrywide is in financial difficulty”, which seems to have made the rumour much more widely known than it had been.

Countrywide protested to the radio station (perhaps reasonably so, but inevitably it was futile – what was done was done), and they prepared a media release supposed to highlight their strength, but it took several days to get this in daily newspapers. Reading the release now, with 34 years hindsight, I’m not sure that as a nervous depositor I’d have been reassured by it – indeed when financial institutions boast about how rapidly they had been growing (in a climate of big changes in relative prices, and a great deal of uncertainty) it is probably reason for increased unease.

By this time, deposit withdrawals were already increasing significantly, and management was at pains to ensure that no branch was in danger of running out of cash even briefly. And by this time, management had tracked down how the rumours seem to have started – in the failure of a totally unrelated trucking company Countrywide Transport Systems Limited. By then, the knowledge wasn’t much use to them. They’d planned a press release explaining where the rumour had come from, but before it could run they had to deal with a development completely from left field: a Social Credit (monetary reformers) MP had issued a press statement referring to “widespread rumours about the impending collapse of a major building society” (by this time there were only two majors).

Countrywide called in the Reserve Bank and the then Governor, Spencer Russell, managed to get hold of the MP concerned – at Wellington airport – within 45 minutes of the statement being issued. Morrison retracted the statement, but it was too late. As the history records “hundreds of depositors demanded their money”.

The run seems to have been focused in Wellington (and Hamilton), with queues outside several branches – 50 metres down the street outside the main Lambton Quay branch. By the end of the day, customers had pulled out $10 million of deposits (Countrywide’s total assets then were about $445 million). The next day, Thursday, they lost another $9 milliom in deposits (not just “mums and dads”, with withdrawals by solicitors being particularly evident.

The powers that be engaged in a significant (and successful) effort to staunch the run, with statements from the Associate Minister of Finance, the Governor of the Reserve Bank and the chief executive of the National Bank all reassured the public that Countrywide was sound. By the Friday, it was estimated only $1 million of panic withdrawals occurred.

(These numbers don’t fully add up but) the history records that total deposit losses over the period of the run were around $30 million – a far from insignificant share of total deposits. Countrywide estimated that the run had involved a direct P&L hit of around $1m, arising from the need to liquidate assets (government stock) in a rush, and additional staff, advertising, and communications costs.

And then the money flooded back – it is recorded at times there were long queues to deposit the funds that had been withdrawn just a few days previously. And the history mentions – without comment – that people were often depositing the same cheque they had taken from Countrywide only a few days previously. I don’t really remember the run – I was a junior Reserve Bank economist doing monetary policy stuff, and yet there is no mention of the run in my diary at all – but that factoid was grist to the mill in debates about financial stability for years to come. If you were so concerned about the health of your bank (building society) as to run on the bank, spend an hour in a queue, forfeit your place in the queue for mortgage eligibility (this was a thing still in 1985), why would you (a) take a cheque from the very bank you were concerned about (the danger of mugged on Lambton Quay had to be small, for example), and (b) why would you then not bank it straight away and pay for expedited clearing? I still don’t claim to fully understand the answer to either question.

Eligibility for mortgage lending was still an issue in early-mid 1985. Banks and building societies had been liability-constrained, and thus the practice grew up of having to have a suitable “savings record” with a specific lender to get a (first) mortgage (at least if you didn’t work for a bank, an insurance company, or the Reserve Bank). The lender was doing you a favour not (as now to a great extent) the other way around. Pulling your money out of the financial institution you might want to borrow from really was a big issue. Of course, better to lose your place in the mortgage queue than to lose your deposit (had it come to that), but it was a hurdle many depositors faced then that they would not face now.

As it happened, times were a changing, and the history records that Countrywide eventually “relented” (their words) and restored to their place in the mortgage queue those who had pulled their money out in the run. Before very long, those depositors would have found other lenders competing to lend to them.

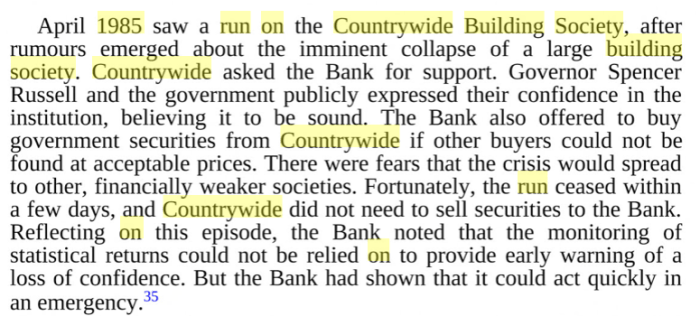

There are quite a number of unanswered questions in the Countrywide history (unsurprisingly – geeky monetary economists weren’t the target market for the book), and I had a look at various other books on my shelves to see if I could find any other angles. There was nothing in Roger Douglas’s book or in the biography of (then Deputy Governor) Roderick Deane, but there was a brief mention in the history of the Reserve Bank published in 2006. Here is the relevant text.

But, of course, that passage only raises further questions, including ones about how the Governor (or the Associate Minister) could be confident in their assertions about the soundness of Countrywide. Whatever the substantive health of the institutions, were their statements well-founded in verified and verifiable data, or were the statements to some extent a confidence-trick: well-motivated, but actually based on little or no more information than the public had? (There are readers of this blog who would pose similar questions about the style of bank supervision adopted by the Reserve Bank to this day.) The Bank’s files may offer some answers (or maybe not). And was the statement of support from the National Bank chief executive supported by offers on unsecured liquidity assistance (that would be a clear signal of confidence that might have encouraged the Reserve Bank).

Perhaps the authorities made a relatively safe call – after all, resurgent inflation meant that the value of Countrywide’s loan collateral was rising. On the other hand, like all regulated entities in those days, Countrywide had had to hold significant amounts of government securities, and government security interest rates had risen sharply. Many institutions – notably the trustee savings banks – had taken big mark to market losses, and there was a strong sense that the viability of some of them would have been in jeopardy, especially if there had been timely and clear mark-to-market reporting. Add in the high and very variable wholesale funding costs (probably only a small proportion of Countrywide’s funding) and one is left wondering how robust an analysis lay behind the official statements of support. There was another building society run – on competitor United – a few years later, and the Reserve Bank history records that that time United took the view that official statements of support (Governor and Prime Minister) were tardy. What sort of rethinking went on internally after the Countrywide episode?

I’m not playing any sort of gotcha here. If anything, it is more a plaintive appeal for some economic and financial historian to undertake a systematic treatment of the New Zealand banking and financial sector through the liberalisation period. There were all manner of small crises and near-crises during this period (PSIS, the devaluation “crisis”, Countrywide, United, RSL, the DFC, NZI Bank, the BNZ (twice) and probably others that don’t spring immediately to mind. There are serious scholarly treatments of the experience in the Nordic countries with liberalisation at about the same time, but surprisingly little about New Zealand.

Not, I suppose, that historians will be able to help answer the question of why panicking depositors took their money in a cheque and then, it appears, in many cases didn’t even rush to get the cheque cleared, or to bank it at all.

I’m sure there are readers who were involved to some extent in these matters, whether at the Reserve Bank or elsewhere. I’d welcome any perspectives or insights in comments.

UPDATE: See the comment below from Andrew Coleman about the United run.