ANZ’s New Zealand operation has had a bad run lately, what with the problems around the version of a model they were using for calculating operational risk capital, and then yesterday’s announcement of the loss of their CEO. Perhaps it is a failure of imagination on my part, but I can’t claim that either episode greatly bothered me, whether as a customer or more generally. Yes, both incidents suggest a degree of untidiness that isn’t ideal, but it is a big organisation and they were pretty small issues. Perhaps it suggests the local board doesn’t amount to much, but why would that surprise anyone? Local incorporation is mostly about having (a) some assets that we can be reasonably sure will be available to meet local liabilities in the (very low probability) event of a major bank failure, and (b) having someone to prosecute if governance failures proved to have risen to a prosecutable standard (a reason for the otherwise questionable requirement for some of the directors to be locally resident). Beyond that, it makes sense for the whole of the ANZ group to be able to be run, as far as possible, as a single entity.

But rather lost amid the headlines yesterday was a very useful new piece from the ANZ’s economics team, “Prospects for unconventional monetary policy in New Zealand”. It is a very substantial piece of analysis, which gets into quite a lot of detail on how New Zealand might handle a situation in which the conventional limits of monetary policy had been exhausted (ie when the OCR has been cut to some modestly negative level). I would encourage anyone with even a passing interest in the topic to read it.

Pretty much ever since this blog began in 2015 I have been lamenting the apparent failure of the Reserve Bank to take this issue very seriously. It never popped up in Statements of Intent or gubernatorial speeches (in the days when we had a Governor who made them), even though many other countries had run into those limits in the last recession, and in most cases the pace of economic recovery had been disconcertingly slow. Back in 2013 or 2014, perhaps the Bank had some small excuse – the then management was so convinced the OCR was heading back up (and by a lot) that effective lower bounds just didn’t seem like an issue New Zealand needed to worry about. But that was five years ago, and the OCR now is 1.5 per cent not the (say) 5 per cent the Bank might have hoped for.

In the last 18 months, there has been some movement by the Bank, Last year, they published a Bulletin article surveying the experiences of other countries with unconventional monetary policy, and then offering some initial thoughts on options for New Zealand. I wrote about that article here, welcoming the fact that it had been done, and the survey of other countries’ experiences, but regretting an apparent degree of complacency by the Bank about the New Zealand situation and the likely effectiveness of such policy tools. That complacent tone characterised various comments the Governor has made at MPS press conferences: lots of handwaving, little hard analysis, and no engagement at all with just how slow the recovery was in most countries that were reduced in unconventional measures. As I noted, central bank complacency risked coming at a cost – a cost not to the comfortable central bankers themselves, but to those left unnecessarily unemployed for long periods of time.

The new ANZ piece is valuable for a number of reasons. First, it will be more widely disseminated than the Reserve Bank article. Second, it isn’t from the Reserve Bank (we need a wider range of discussion and debate around these isses and risks), and third, it goes into more operational detail (around important features of existing RB liquidity facilities etc) in several places than anything previously in the public domain.

I don’t agree with everything in the ANZ piece, and in particular I was surprised by the number of references to how distortionary or risky unconventional policies have been in other countries. The rather bigger issue is that they mostly have not achieved much, at least once we got beyond the immediate crisis period (and this is a distinction the ANZ authors make). As I’ve noted here repeatedly, there is little or no evidence that – whatever the initial announcement effects – long-term bond rates have fallen further relative to policy rates in countries that used unconventional policies than in countries that did not.

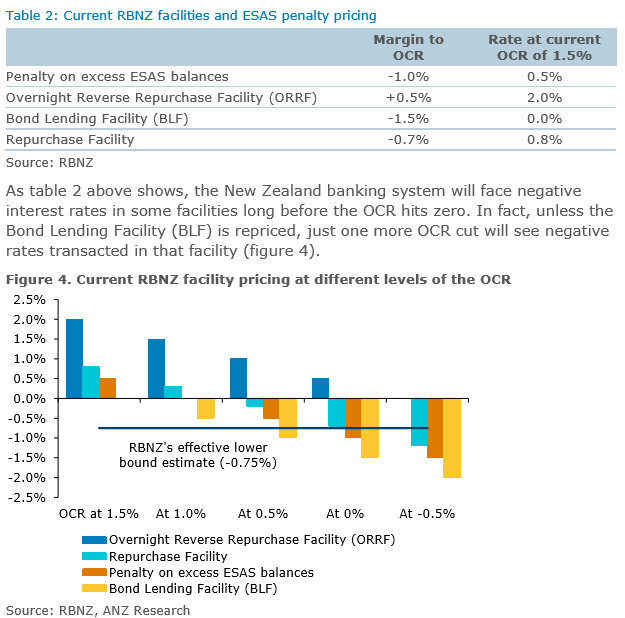

There was a useful reminder that some official RB interest rates will go negative well before the OCR itself gets to a negative number. This is from their document

The Bond Lending Facility is a facility whereby market participants can borrow bonds from the Reserve Bank (to support smooth market functioning) and, as the authors note, is little used.

The ANZ authors put more emphasis on the penalty on excess balances in settlement accounts. I wrote about the Bank’s strange tiering policy in a recent post, but the gist is that the Bank determines for each bank what value of deposits at the Reserve Bank earn the OCR, and anything in excess of that earns 100 points less than the OCR. Banks manage their settlement cash balances to minimise the extent to which anyone bears that lower return But if the OCR were at -0.25 per cent, the rate on excess settlement account balances would be -1.25 per cent on current policies. All else equal, that is a rate low enough that (a) no one else has imposed it, and (b) people might prefer to hold physical cash instead.

I’m a bit sceptical that this is a really important constraint on the ability of the Reserve Bank to use conventional monetary policy down to an OCR of around -0.75 per cent, since there is little reason to suppose the level of settlement cash balances would be rising as the OCR plumbed these new depths (if anything demand might be falling a bit), and banks would – as the Bank would want – be aggressively acting to limit the extent anyone bore the additional cost. But it is an issue that is worth debating further, and which would become salient quite quickly if the Bank went beyond OCR cuts and started using unconcventional measures to boost settlement cash balances materially. In earlier work, it was recognised that tiering policy would probably need to change if there was aggressive unsterilised asset purchases.

The authors rightly note many of the potential limitations of asset purchase options. Sure, the Reserve Bank might be able to buy up a substantial portion of the government bonds on issue – although some holders will be very reluctant sellers, having mandates that specify investment in government bonds – but even if they could, what would be the channel whereby this would revive demand and economic activity (few borrowers took on long-term fixed rate debt). And the Bank might be able to intervene heavily in the foreign exchange market – perhaps on ministerial direction, to ensure the risks fall on the Crown – but they’d likely be selling the New Zealand dollar when it was already undervalued, and if the OCR can’t go below -0.5 or -0.75 per cent, it isn’t likely that the exchange rate effect would be very large. Intervening in the interest rate swaps market has been an idea around for a decade, and I’ve never been persuaded it would accomplish much.

But the options and issues really should be more widely debated, and the Reserve Bank and The Treasury should be taking the lead in encouraging open debate and serious scrutiny of the New Zealand specific issues. As ANZ notes, perhaps interventions can be devised on the fly, but there is no excuse for finding ourselves in that position when we have had 10 years advance notice of the problem. Adrian Orr’s tree god won’t offer the answers, no matter much Orr invokes Tane Mahuta.

My frustration is that thinking doesn’t seem to have advanced much at all in the ten years. I dug through some old files this morning, and among them I found a paper I’d written at Treasury in 2009 (benefiting from discussion with Reserve Bank staff) on options if we reached the limits of conventional monetary policy. I also found a discussion note I’d written in 2011 trying to engender some debate around the legislative provisions that support the near-zero lower bound on nominal interest rates, and was reminded of the report of a Bank working group I lead in 2012 on options if we faced near-zero interest rates (sparked by the intensity of the euro crisis then). But nothing from either the Reserve Bank or The Treasury that has found its way into the public represents any advance on that thinking and work done up to a decade ago. It really is pretty inexcusable. It is almost as if our officials and minister think everything worked just fine in other countries after 2009 – it clearly didn’t – or they just don’t care.

Specifically – and this is a criticism of the ANZ note as well (not even mentioning the issue) – there has been nothing done, no debate held, no analysis published, on dealing with fact that at present people can convert limitless amounts into hard currency, and will do so at some point once interest rates on other instruments (wholesale ones in particular) are substantially negative. Here was what I wrote on that point in my post last year on the Reserve Bank’s article.

It is striking that the article does not engage at all with either of the two more radical options debated in other places and other countries:

- reconfiguring the target for monetary policy. This could take the form of a higher inflation target or, for example, the use of a price level or nominal GDP level target. Each approach has its weaknesses, but either – done in advance of the next serious downturn, not in midst when much of the opportunity is lost – could help raise, and hold up, expectations about the path of the nominal economy, including inflation.

- taking steps to material reduce the extent of the effective lower bound on nominal interest rates.

The latter remains my preference, for a number of reasons (including that the existing problem arises largely because central banks have – by law – monopolised note issue, and then not proved responsive to changing circumstances and technologies. Problems are usually best fixed at source.

If there is still a useful role for physical currency (I discussed some of these issues here), the ability to convert huge amounts of financial assets into physical currency, on demand, without pushing the price against you, is now a material obstacle to monetary policy doing its job in the next recession. There is a good case for looking seriously at a variety of reform options, such as:

- phasing out large denomination Reserve Bank notes (while perhaps again allowing private banks to offer them, on their own terms, conditions and technologies),

- capping the physical Reserve Bank note issue, scaled to growth in, say, nominal GDP (perhaps with provision for overrides in the case of financial crisis runs),

- putting a spread (between buy and sell prices) on Reserve Bank dealing in bank notes, or

- auctioning a fixed quota of bank notes, and thus allowing the price to adjust semi-automatically (when currency demand rises, as when the OCR goes materially negative) the cost of conversion rises.

These sorts of ideas are not new. They do not get rid of the entire issue – at an OCR of, say, -10 per cent, even transaction demand for bank deposits might dry up – but they would go an awfully long way to ensuring that the next recession can be dealt with more effectively than the last.

If, for example, you thought the OCR was going to be set at -3 per cent for two years, then once storage and insurance costs are taken into account (the things that allow the OCR to be cut to around -0.75 per cent now), even a lump sum conversion cost (deposits into physical cash) of 5 per cent would be enough to keep almost everyone in deposits and bonds (even at negative yields) rather than physical cash. That is a great deal leeway than the Reserve Bank has now. Having that leeway – and being willing to use it – helps ensure nominal rates don’t need to stay extremely low for too long.

In principle, many of these sorts of initiatives probably could be done in short order in the midst of the next serious downturn. But we shouldn’t have to count on unknown crisis responses, the tenor of which have not been consulted on, socialised, and tested in advance. It may even be that some legislative amendments might be required.

There is no excuse for not having these issue all sorted out well in advance, and having communicated clearly to the public (and ministers and markets) how they will be handled, secure in the knowledge that rigorous planning and risk identification has occurred.

In part, that is because of one other issue that ANZ piece doesn’t touch on (neither did the Reserve Bank article). Once a new severe recession is upon us, people will fairly quickly begin to appreciate how few effective and credible options central banks and governments have, and react – eg adjusting inflation expectations – accordingly. In 2009, the typical reaction was to expect a quick rebound, partly because that was how economies were perceived to have usually behaved, and partly because so many interventions were being thrown into the mix. Next time, people (markets) will go into a severe downturn with the memory of post-2009, an awareness of the unpropitious starting point, and an awareness of the distinct limitations of unconventional policy. All that is likely to exacerbate the downturn and further complicate effects at countercyclical stabilisation. People will suffer as a result.

We need some leadership on these issues. If the Reserve Bank won’t or can’t provide it, the Minister of Finance – who will bear responsibility before the voters – needs to lead himself, and insist that his agencies do more and better, more openly, than they have done so far.

In the meantime, well done ANZ for a substantial piece of work. Once again, I’d encourage people to read it and think about the issues and constraints it raises.