Belatedly working my way through The Treasury’s Budget economic forecast tables, I checked whether they had become any more optimistic about the success of the government’s economic strategy. Successive governments have talked about a more outward orientation, and it seems likely that any successful and sustained lift in New Zealand’s overall economic performance would have as one marker of success an increasing share of GDP accounted for by trade with the rest of the world (big markets out there, big opportunities to buy and sell).

But the numbers in The Treasury’s latest forecasts translate into the same downbeat charts I’ve been generating now for some years.

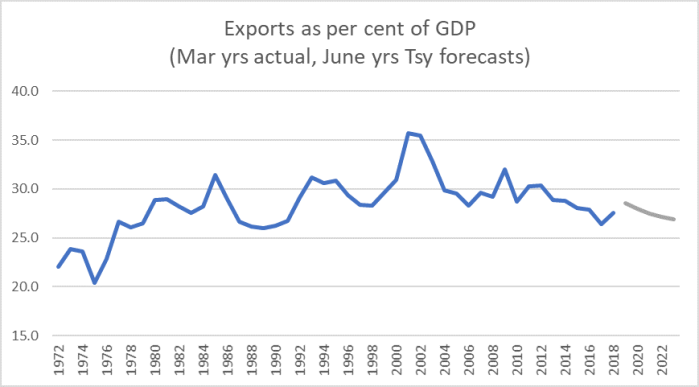

Here is exports as a per cent of GDP.

By the end of the forecast period, when the government is likely to be finishing its second term, Treasury (on current government policies) thinks exports as a share of GDP will then be about where they were in 1977.

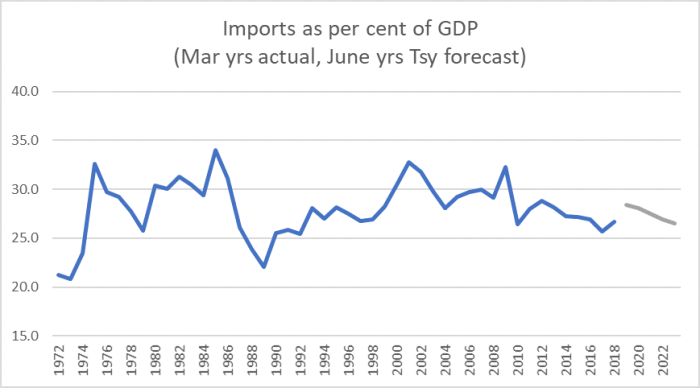

And imports?

There is nothing remotely transformational. Just more mediocre underperformance.

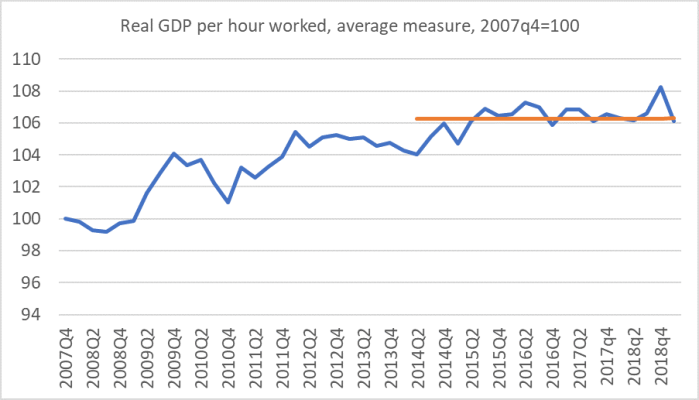

What about productivity? Well, here The Treasury is rather upbeat.

This is the actual record of labour productivity growth, including an estimate for the March quarter 2019 using Treasury’s published GDP forecast.

That’s next to no actual productivity growth for five years, and none at all for four years.

But, as ever, Treasury thinks things are just about to come right. “As ever”? Here’s a table I included in a post at the end of last year, suggesting that Treasury simply had the wrong model for thinking about productivity.

| HYEFU forecasts for labour productivity growth published in Dec | |||||

| Forecasts for June yrs | 2014 | 2015 | 2016 | 2017 | 2018 |

| 2016 | 2.2 | ||||

| 2017 | 1.6 | 1.6 | |||

| 2018 | 1.1 | 2.1 | 2 | ||

| 2019 | 1.2 | 0.8 | 1.5 | 2 | |

| 2020 | 0.7 | 1.3 | 1.7 | 1.1 | |

| 2021 | 1.4 | 1.5 | 1.2 | ||

| 2022 | 1.3 | 1.2 | |||

| 2023 | 1.2 | ||||

The forecasts in the latest BEFU for the three out years (to 2023) are exactly the same as those published in December’s HYEFU.

Treasury has consistently expected a significant recovery in productivity growth, and it has equally consistently failed to arrive. Is there any reason to think they are more likely to be right now? It isn’t as if anything much in the policy framework has changed for the better.

(Of course, if the productivity growth fails to materialise, so – most likely – will the headline GDP growth, and the revenue estimates will be threatened.)

The other thing I find consistently odd about The Treasury’s macro numbers is their view all our inflation problems (undershooting the target that is) are now behind us: from this quarter, the forecast inflation rates are consistent with annual inflation at 2.0 or 2.1 per cent all the way to the end of the forecast period. As a result, on their numbers, there are no OCR cuts (their numbers will have been finalised before the recent actual cut) and before too long OCR increases start being implemented: three years hence they expect to have seen 75 basis points of increases.

And, of course, this is the same sort of story they’ve been telling us for years. Wrongly.

In many respects, medium-term macroeconomic forecasting is a mug’s game. Few, if any, can do it consistently well. So the numbers aren’t interesting in their own right – they tell us nothing much about what actually will happen – but they do tell us something about the forecaster’s models, and when the forecaster is also the government’s lead economic adviser that in itself can matter.

On these numbers, we have a Treasury that sees no sign of an increasing outward orientation to the economy, seems to think an unemployment rate of about 4.5 per cent is as good as it gets in normal times (ie roughly the NAIRU), and continues to pick projections of productivity growth seemingly out of thin air, even against a backdrop of years of little or no productivity growth for recent years, no change of economic policy approach, no nothing,

For all the (quite appropriate) fuss about the outgoing Secretary to the Treasury, it is now only three weeks until his scheduled departure date and no replacement has yet been announced. That in itself should be quite concerning, suggesting SSC is struggling to come up with someone with the right mix of competence and go-alongness. There is a whole range of institutional performance issues a new Secretary should address, but the characteristics that might qualify someone to be appointed by the current SSC regime may well be exactly the wrong sort of characteristics to expect any material change for the better from after 27 June.