Belatedly working my way through The Treasury’s Budget economic forecast tables, I checked whether they had become any more optimistic about the success of the government’s economic strategy. Successive governments have talked about a more outward orientation, and it seems likely that any successful and sustained lift in New Zealand’s overall economic performance would have as one marker of success an increasing share of GDP accounted for by trade with the rest of the world (big markets out there, big opportunities to buy and sell).

But the numbers in The Treasury’s latest forecasts translate into the same downbeat charts I’ve been generating now for some years.

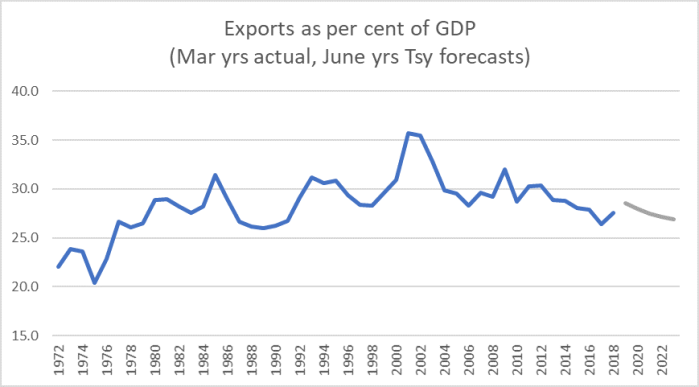

Here is exports as a per cent of GDP.

By the end of the forecast period, when the government is likely to be finishing its second term, Treasury (on current government policies) thinks exports as a share of GDP will then be about where they were in 1977.

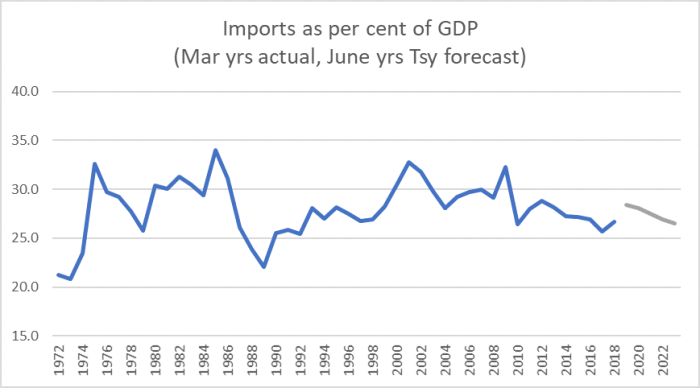

And imports?

There is nothing remotely transformational. Just more mediocre underperformance.

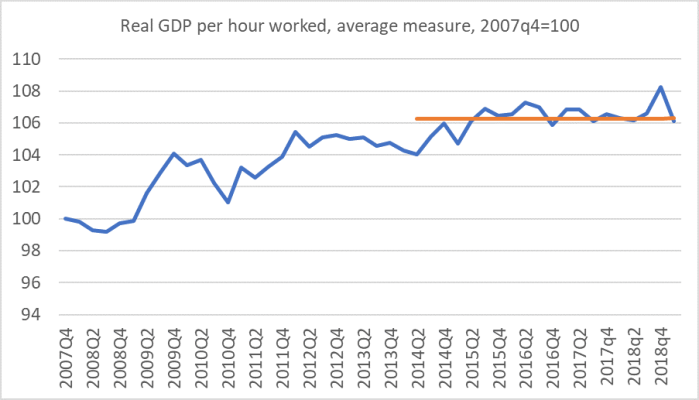

What about productivity? Well, here The Treasury is rather upbeat.

This is the actual record of labour productivity growth, including an estimate for the March quarter 2019 using Treasury’s published GDP forecast.

That’s next to no actual productivity growth for five years, and none at all for four years.

But, as ever, Treasury thinks things are just about to come right. “As ever”? Here’s a table I included in a post at the end of last year, suggesting that Treasury simply had the wrong model for thinking about productivity.

| HYEFU forecasts for labour productivity growth published in Dec | |||||

| Forecasts for June yrs | 2014 | 2015 | 2016 | 2017 | 2018 |

| 2016 | 2.2 | ||||

| 2017 | 1.6 | 1.6 | |||

| 2018 | 1.1 | 2.1 | 2 | ||

| 2019 | 1.2 | 0.8 | 1.5 | 2 | |

| 2020 | 0.7 | 1.3 | 1.7 | 1.1 | |

| 2021 | 1.4 | 1.5 | 1.2 | ||

| 2022 | 1.3 | 1.2 | |||

| 2023 | 1.2 | ||||

The forecasts in the latest BEFU for the three out years (to 2023) are exactly the same as those published in December’s HYEFU.

Treasury has consistently expected a significant recovery in productivity growth, and it has equally consistently failed to arrive. Is there any reason to think they are more likely to be right now? It isn’t as if anything much in the policy framework has changed for the better.

(Of course, if the productivity growth fails to materialise, so – most likely – will the headline GDP growth, and the revenue estimates will be threatened.)

The other thing I find consistently odd about The Treasury’s macro numbers is their view all our inflation problems (undershooting the target that is) are now behind us: from this quarter, the forecast inflation rates are consistent with annual inflation at 2.0 or 2.1 per cent all the way to the end of the forecast period. As a result, on their numbers, there are no OCR cuts (their numbers will have been finalised before the recent actual cut) and before too long OCR increases start being implemented: three years hence they expect to have seen 75 basis points of increases.

And, of course, this is the same sort of story they’ve been telling us for years. Wrongly.

In many respects, medium-term macroeconomic forecasting is a mug’s game. Few, if any, can do it consistently well. So the numbers aren’t interesting in their own right – they tell us nothing much about what actually will happen – but they do tell us something about the forecaster’s models, and when the forecaster is also the government’s lead economic adviser that in itself can matter.

On these numbers, we have a Treasury that sees no sign of an increasing outward orientation to the economy, seems to think an unemployment rate of about 4.5 per cent is as good as it gets in normal times (ie roughly the NAIRU), and continues to pick projections of productivity growth seemingly out of thin air, even against a backdrop of years of little or no productivity growth for recent years, no change of economic policy approach, no nothing,

For all the (quite appropriate) fuss about the outgoing Secretary to the Treasury, it is now only three weeks until his scheduled departure date and no replacement has yet been announced. That in itself should be quite concerning, suggesting SSC is struggling to come up with someone with the right mix of competence and go-alongness. There is a whole range of institutional performance issues a new Secretary should address, but the characteristics that might qualify someone to be appointed by the current SSC regime may well be exactly the wrong sort of characteristics to expect any material change for the better from after 27 June.

I’m increasingly convinced that NZ is fundamentally a thinly populated, geographically isolated nation made up mostly of poor people and small businesses, but with an overlay of globalist knowledge workers living mainly in Wellington (the public servants) and Auckland (the commercial leaders).

The knowledge workers do well for themselves, but they have given up on solving the problems that lead to most NZers (and NZ) just getting by. There’s always Australia as an option for the knowledge workers.

Arguing for the deep reforms needed to lift productivity risks the knowledge workers – especially our political class – being considered kooks and subsequent loss of comfortable salaries.

NZ remains a comfortable, clean and safe place to live if you have an adequate income. So there is no burning platform for deep economic reform.

LikeLike

The knowledge workers also do not understand economics or business, for the most part, judging from conversations I’ve had this week.

LikeLike

The table “HYEFU forecasts for labour productivity growth published in Dec” – does this mean per capita productivity or is it just an estimate for the growth in the number of workers (both immigrants and the elderly working past retirement age)? If the former it proves the treasury are consistent pollyannas and if the latter rather pessimistic.

Does your graph of exports as a fraction of GDP include tourism? Surely tourism has been expanding for years so if it is included it proves our export businesses are doing really badly. If it is not included as an export then is it large enough to distort the GDP total and make exports appear to be in decline when they are actually OK.

LikeLike

1. The productivity variable Treasury uses is GDP per hour worked.

2. Yes, it is total exports including tourism and other services.

LikeLike

Your two answers support your argument. They depress me. The Treasury ought to be depressed to.

LikeLike

Bob, not too sure why you would be depressed over a garbage statistic? An IT guy should have worked out already that tourism export as a percentage of GDP is a nonsense statistic.

LikeLike

GGS: it doesn’t matter if it is a ‘garbage’ statistic so long as it is consistent. If you look at the first graph and remove whatever the ‘tourism element’ might be it shows exports as a fraction of NZ GDP declining. You have prevously expressed support for NZ tench businesses – well their exports are declining. I prefer more basic agricultural based businesses and they are not doing well either. If NZ exports decline then as you mention in another post it means our NZ$ becomes less popular and the result will be we all become poorer which is a sad prospect for my children.

LikeLike

Bob, actually correction to my statement. It is not actually garbage statistic but garbage interpretation of that statistic. Ideally you would want Export GDP to Total GDP to fall rather than rise as a good thing. The reason being that if that $1 export dollar is spent again and again in the local NZ economy then that is a positive rather than a negative.

LikeLike

Our Top exports by product to country destination. Notice that it is dominated by China. We export $14 billion to China out of a total export of $83 billion.

Milk powder, butter, and cheese China $4.5 billion

Logs, wood, and wood articles China $3.1 billion

Meat and edible offal China $2.3 billion

Other personal travel Australia $2.1 billion

Other personal travel European Union $2.0 billion

Meat and edible offal United States of America $1.7 billion

Meat and edible offal European Union $1.6 billion

Other personal travel China $1.5 billion

Education travel services China $1.3 billion

LikeLike

Correction: Our exports to China is $18 billion out of a total exports of $83 billion in total.

LikeLike

No, tourism exports as a percentage of total GDP is a garbage statistic because an export dollar spent in the domestic economy flows through the domestic economy in many multiples.

LikeLike

Rodney Dickens is currently commenting on the “value” of Tourism

LikeLike

The value of tourism is like any of our exports. It creates a international demand value for our NZD currency. Without this international demand for our NZD we will not have the value to buy the imported goods we crave.

LikeLike

The link will take you to the latest Raving –

Click to access TourismVsDairyJun19.pdf

A fun thing about doing research for a Raving is that it can lead to unexpected conclusions. The starting point for this Raving was comparing the performance of tourism, generally considered a growth industry, with the dairy industry that is driven by technology as much as anything and therefore should also perform like a growth industry.

What I found was that neither has performed like a real growth industry over the last two decades with this probably more the case for tourism. Probably because a lack of data for the dairy industry means a comparison can’t be made over two decades.

This follows up on the Raving that looked at some features of the boom in international visitors that is showing signs of faltering (use this link to access it – http://www.sra.nz/pdf/TourismRevisitedMay19.pdf). The next Raving will most likely identify some of the real growth industries.

Worth the read.

Basically neither tourism nor milk have gone anywhere for us.

.

LikeLike

Meanwhile;

The Government’s tax-take for the 10 months to April 30 was $2.3 billion more than what it predicted just a week ago in this year’s Budget.

In Budget 2019, Treasury predicted the tax revenue for 2019 would be $68.8 billion, but actual figures out on Thursday show $71.1 billion.

Treasury defended its forecasting saying the significant variance could be explained by a change to Inland Revenue systems.

https://www.newshub.co.nz/home/politics/2019/06/government-s-tax-take-billions-of-dollars-above-forecast.html?fbclid=IwAR1Ce1hXVMBq0mm0AVmDOlaZe_nxLuPn1bAIR3N5ngVOJ6wa2ew8ZD9jKTU

LikeLike

I would have picked our long long warm and dry weather over summer that would have meant higher spending activity with longer days of warm dry paradise partying weather.

LikeLike

I suppose the problem is both is that they are focused on low value ‘exports’… I’ve always considered tourism to be a low wage industry and with dairy the focus of Fonterra is maximising the farm gate milk price at all costs – this is NOT a good way to build long term value…

LikeLike

Tourism is a low wage industry and expansion could actually reduce average incomes when we import immigrants to fill those extra low wage tourism jobs!

LikeLiked by 1 person

Tourism is a low wage industry but it doesn’t have to be. It should be possible to nudge it from quantity to quality, away from low wages, long inconvenient hours, overloading of NZ infrastructure, high CO2 emissions.

LikeLike

The Goldcoast tourism in Australia relies on highly engineered billion dollar theme park tourism.

LikeLike