Ages ago I signed up to get the weekly market outlook publication from the Moody’s rating agency. I very rarely look at, but my eye was drawn to the title of this week’s edition, “Not Even the Great Depression Could Push the Baa Default Rate Above 2%”. I’m a sucker for almost anything about the Great Depression, especially when combined with very long-run charts.

The report highlighted that there is an increasing number of credit rating downgrades for (US) high-yield (“speculative”, “risky”) corporate issuers, and that at present high-yield spreads haven’t widened to reflect that in the way one might typically expect. But they also took the opportunity to note that there is nothing similar going on for safer corporate credits: if anything there are more upgrades than downgrades at present for Baa rated industrial companies.

A Baa rating is the Moody’s equivalent of S&P’s BBB. Both are the lowest of the “investment grade” ratings (all the ratings from A- to AAA are the higher investment grade ratings). A Baa rating isn’t for a borrower that would be regarded as rock-solid, but is still a pretty good-quality credit. A reasonable and prudent investor probably wouldn’t look askance at having some of such a credit as part of their portfolio.

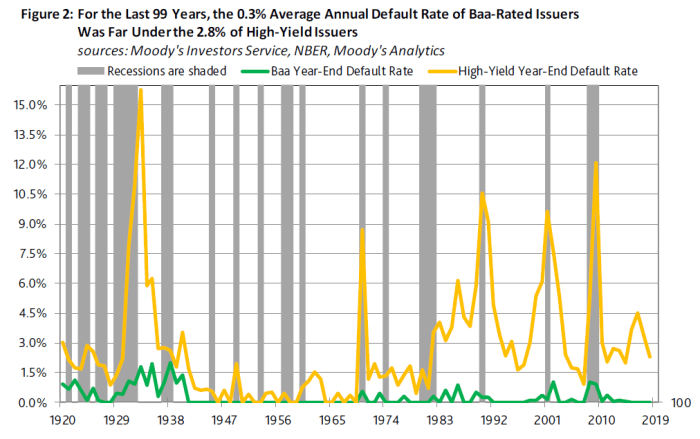

And this was the chart that that Great Depression headline related to.

The two recessions of the 1930s were savage (the second savage but fairly short) – about as bad, on many metrics, as the Greek experience in the last decade. And yet, even then, not (quite) 1 in 50 Baa-rated issuers (recall that these weren’t the most rock-solid issuers) failed (defaulted). And over 99 years of data the average annual default rate for Baa-rated issuers was 0.3 per cent (and over the second half of that period – including the severe 2008/09 recession – the average default rate was lower than in the first half of the period, when active counter-cyclical macro management was still a contentious novelty.)

Loosely speaking, a 0.3 per cent annual default probability could be seen as roughly equivalent to a probability that a particular Baa-rate issuer will default once in every 333 years.

Readers will recall that the Governor of the Reserve Bank plucked, pretty much from thin air (at least going by the documents they’ve released), a benchmark of requiring banks to have sufficient equity capital to cope with a 1 in 200 year event.

But how safe do the rating agencies regard our big banks at present, on the current capital ratios? For that, you can’t just look at the headline rating, which incorporates the prospect of government bailouts, and/or interventions such as recapitalisation by a parent (both factors that affect the ratings for our big banks), but want to look at an assessment simply of the balance sheet of the rated entity itself (“standalone ratings”).

I couldn’t see a nice summary of the Moody’s standalone ratings for the big banks in New Zealand, but I did find this summary of the S&P ratings, in an article on the Reserve Bank capital proposals.

S&P says the stand-alone credit profile of one or more of ANZ NZ, ASB, BNZ and Westpac NZ could be increased to ‘a-‘ from ‘bbb+’ if the Reserve Bank proposals are implemented. And if their Aussie parents choose to inject capital to meet the Reserve Bank proposals, this could lift their stand-alone credit profiles to ‘a’ from ‘a-‘.

A stand-alone credit profile is S&P’s opinion of a debt issuer’s creditworthiness, in the absence of extraordinary intervention from its parent or affiliate or related government, and is one component of a credit rating.

The current standalone ratings are already at the upper end of the Baa/BBB rating. I also couldn’t find a similar long-term default rates chart for S&P (like the Moody’s one above) but an S&P table of defaults since 1980 suggests a very similar default rate over that period for S&P BBB issuers (like the big New Zealand banks) than for Moody’s Baa issuers.

It is easy for people to have a go at rating agencies – the Governor of the Reserve Bank has done so – but actually what the chart at the start of the post highlights is that for conventional issues of securities, Moody’s seems to have done just fine (were they now rating issuers consistently too generously you would see an upsurge of defaults, but there has been no sign of that in recent decades).

This isn’t a new point: Ian Harrison has made much the same point, in a more developed way, in his critique of the Reserve Bank’s proposals. But sometimes a picture helps.

According to the rating agencies – and recall that the Reserve Bank echoes the assessment in the tone of its comments in each FSR – New Zealand banks already have a mix of asset books and funding structures (debt/equity mix) consistent with an extremely low probability of failure, even absent parent support. Perhaps not inconsistent with that, no major retail New Zealand bank (or Australia or Canadian bank) has failed in a very very long time.

The case for much higher minimum capital requirements just hasn’t been made.

Albeit recalling the credit ratings assigned to several banks/financial institutions ahead of a recent financial crisis that very few expected.

LikeLike

“According to the rating agencies” – cant trust them as far as they can be thrown. They were complicit in the mis-rating of the mortgage securitization in the US that led to Leahmans collapse.

LikeLike

There is more than credit risk, conduct risk for example. It’s not that the Royal Commission was inconsequential. Operational risk is an increasing worry among risk managers: money laundering, cyber risk, etc. These risks have become bigger: UBS, Danske, Swedbank, Rabobank, ING, Credit Suisse. All these banks suffered significant losses from a risk category that the Reserve Bank and pundits ignores.

LikeLike