The CPI data were released a couple of days ago. There was, inevitably, a lot of commentary around higher petrol prices, although most commentators noted that the Reserve Bank was likely to “look through” what we are seeing, and not adjust monetary policy just because of higher petrol prices. That would, indeed, be consistent with the Bank’s mandate – and practice – over almost thirty years of inflation targeting.

One can have all sorts of debates about what sorts of effects should be “looked through”. We used to have lengthy discussions attempting to distinguish between petrol price effects themselves, indirect effects (eg higher airfares or courier costs directly resulting from higher fuel prices) and second-round effects – the real worry, if changes in oil/petrol prices came to affect the entire inflation process, including medium-term expectations of inflation. Those risks were real, and realised, back in the 1970s oil shocks, and that set the scene for much of the subsequent discussion and precautionary debate.

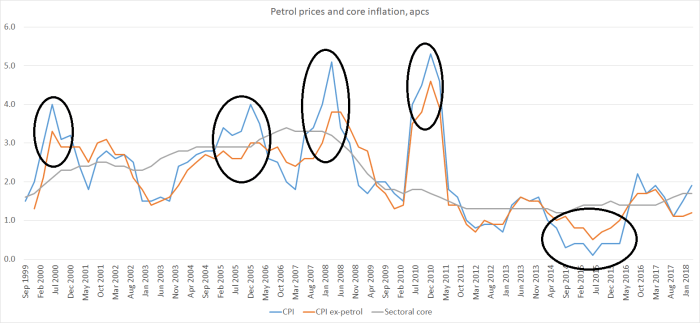

SNZ only has a CPI ex-petrol series back to 1999. In this chart, I’ve shown the headline CPI inflation rate, the CPI inflation rate ex-petrol, and the Reserve Bank’s preferred core inflation measure, the sectoral factor model.

I’ve highlighted four episodes in which petrol price inflation was much higher than overall CPI inflation, and one (quite recent) when it was much lower.

In the first of those episodes – around 2000 – the surge in petrol prices coincided with quite a lift in core inflation. Bear in mind that the economy was recovering from the brief 1998 recession, and the exchange rate had fallen sharply.

In the second episode – 2004 and 05 – the surge in petrol price inflation coincided with no change in core inflation.

In the next episodes – 2008 and 2010 – the surge in petrol price inflation coincided with a fall in core inflation. In the 2008, the Reserve Bank explicitly recognised some of this at the time, and talked of scope to cut the OCR soon, despite the high headline inflation.

And in the recent episode when petrol price inflation was very low, there was no fall in core inflation – if you look hard enough, it may actually have increased very slightly.

There is talk that, if oil prices persist, headline inflation could get as high as 2.5 per cent before too long. The experience of the last couple of decades suggests that will tell us nothing useful about underlying/core inflation trends, or about the appropriate stance of monetary policy. And the preferred core inflation measure remains below the target midpoint, as it has been for almost a decade now.

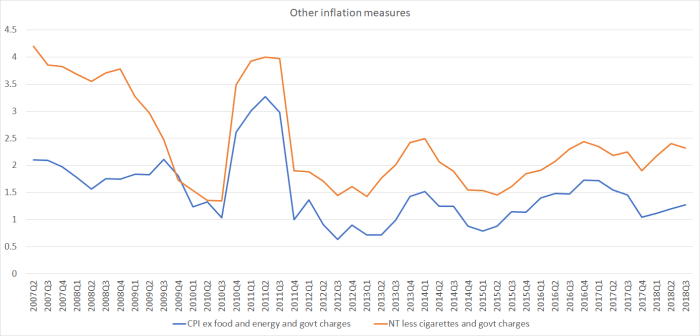

Here are a couple of other series worth looking at.

The blue line is a fairly traditional sort of exclusions-based core inflation measure: excluding volatile items (food and fuel) and (administered) government charges (altho not tobacco taxes), and the orange line is non-tradables inflation excluding government charges and cigarette and tobacco taxes (which, you will recall, have been raised relentlessly each year, in a political non-market process). There is no sign in either of these series of underlying inflation moving higher in the last year or two. Core non-tradables inflation of under 2.5 per cent is not consistent, typically, with core (overall) inflation being at 2 per cent.

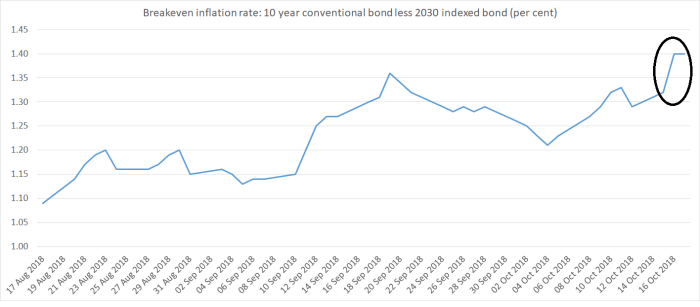

Having said all that the financial markets appear to have taken a slightly different view of this week’s inflation data. Here is a chart of the breakeven inflation rate from the government bond market – the difference, in this case, between the 10 year conventional bond rate and the 2030 indexed bond (real) rate. I’ve highlighted the change since the inflation data were released.

At 1.4 per cent, the gap is still miles off the 2 per cent target midpoint (or than the comparable numbers in the US), but the latest change does look as if it is worth paying at least a bit of heed to. Perhaps it will dissipate over the next few weeks, but if not it wouldn’t be a cause for concern, but some mild consolation that – after all these years – there was some sign of market implied inflation expectations edging a little closer to target.

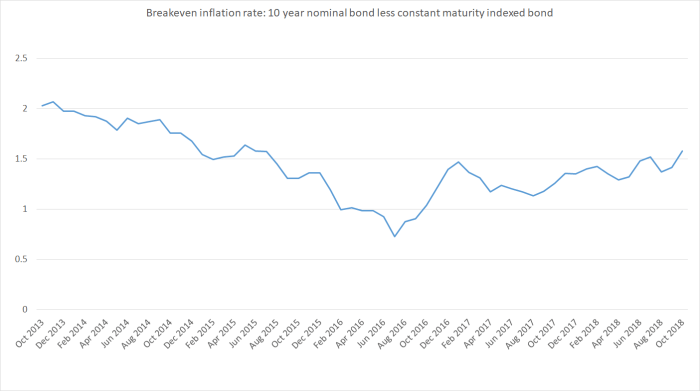

What about a longer run of data? We only have a scattering of inflation indexed bonds, in this case one maturing in September 2025 and one maturing in September 2030. The 2030 bond was first introduced five years ago this month. Creating a rough constant maturity 12 year indexed bond series – the 2025 bond had 12 years to run in 2013, and the 2030 one has 12 years to run now – and subtracting the result from the Reserve Bank’s 10 year conventional bond series produces this (rough and ready) chart.

A clear rebound from the lows of 2016, but implied breakeven inflation rates still much lower than they were five years ago.

There still seems to be quite a long way to go for the Reserve Bank to really convince investors that, over the decade ahead, they will do a better job of keeping inflation averaging near target than they have done this year to date.

Continuing to talk down the risks of the next serious recession, and the limitations of policy here and abroad to act decisively to counter such a recession and the likely deflationary risks, is cavalier and irresponsible. It might (seem to) help confidence in the short-run, but if those risks crystallise – and central banks should focus on tail risks in crisis preparedness – the Bank will bear a lot of the responsibility if the economy performs poorly, and inflation ends up so low as to vindicate (and more) the evident lack of confidence among people putting real money on a view about the average future inflation rate.

The higher petrol prices go up, the higher percentage of people would switch to electric. That is likely the reason why this 70 year old NZ petrol retailer, Waitomo is starting to try and compete to bring down petrol prices. They would be fully aware if petrol prices continue upwards, there would not be a future for petrol as people switch to electric. If you want to try and extend the life blood of your 70 year old business for the long haul, you need to get out there and try and force petrol prices down to discourage the switch to electric.

LikeLike

GGS: is this the strangest comment you have ever posted? Petrol ranks close to water and air as something we cannot live without. NZ has a fleet of a million fossil fuel vehicles – will they be abandoned because of a petrol price rise? If fruit and veg go up in price I buy and eat less, if petrol goes up I keep buying it and when my money begins to run out I still buy petrol but eat less food or cheaper food. Fully electric vehicles may well be on their way but at present are completely insignificant.

Linking petrol price to general inflation makes sense but sharp price changes are often related to international events such as an Arab Israeli war and such events are likely to change NZ consumer attitudes – maybe more home tourism and personal debt reduction.

LikeLike

Personally I do think that most of us operate from a sensible logic standpoint. I like driving a large Lexus SUV and I am totally aware of my petrol costs. I am looking seriously at upgrading my old gas guzzling which is now 11 years old. I have avoided buying a new petrol SUV until electric SUV’s become available at a lower price by the major brands. Lexus has only the hybrid available which means only the Tesla X is available at $160,000.

A 2012 Lexus RX450 hybrid is available for only $35,000 which would immediately reduce my petrol consumption by as much as 70% which makes it more viable. But second hand Nissan Leaf’s are available at $12,000. Of course there could be the risk of a replacement electric battery that have perhaps 8 to 10 years lifespan. This is a additional $17,000 risk or perhaps risk a $4000 refurbished electric battery.

So it is a question of price points before it forces a change over from petrol to electric. My boss had already transitioned his fleet cars to hybrids for some years now from his petrol guzzling Chryslers which means that if full electric cars become available he would make that changeover.

LikeLike

Hybrids have the advantage that you do not need charging stations. This means there is no reliance on the electricity grid.

LikeLike

Which means that solar power infrastructure needs to occur first before a. critical mass switch to electric vehicles can occur.

LikeLike

I know you love inflation for reasons I don’t really understand, nor do you personally care about its consequences on people, but it wasn’t petrol prices in isolation that went up.

Rates up 5.1%

Transport up 5% (Private Transport services up 13%)

Cigarettes up 11%

Home ownership costs up 4.1%

Vegetables up 11%

And so on. This reduces the disposable income of people using these things, and I think most people will notice.

Inflation expectations are sensitive to petrol prices, and along with potential forthcoming effects from imported inflation from the lower exchange rate I’d say it was almost a given headline inflation will rise and so will core inflation. My view is that further second round effects seem inevitable and it would make a lot of sense for the Bank to be signalling higher rates are now more likely sooner than they have recently been saying. Recent data shows the economy is not in any kind of trouble that would warrant OCR cuts, which would quite possibly inflame inflation.

LikeLike

Quite a caricatured (and misleading) description there in the first paragraph………

The Bank hasn’t managed to get core inflation to the target midpoint once in the six years since that reference point was explicitly highlighted. As I’ve said here previously, I would happily lower the target to something focused on (true) zero – which would mean fewer tax distortions as well – provided the govt does (as it really should) something about the lower nominal bound on interest rates.

Re the latest quarter, not that there was no change in sectoral core inflation.

Re expectations, yes there will be some spillover into year ahead expectations measures, but it has never been clear that those measures reflect behavioural changes.

In this post, I didn’t address what the OCR should be now, just that (without a lot more detailed contextual analysis) the petrol prices changes shouldn’t alter that stance.

LikeLike

Michael is driven by a more purist monetary policy which means either direction is ok as long the RBNZ sticks to a 2% inflation target and some discretion between 1% and 3% inflation. The assumption usually is that higher interest rates would curb consumer demand and therefore lower inflation and vice versa.

My view is that given that NZ household Savings deposits more or less equates to household lending which means that interest rates either up or down does not curb overall consumer demand. But there is actually substantially more commercial debt than commercial savings which means that the early stages of a interest rate rising actually leads directly to higher inflation as businesses increase prices to cover the additional costs.

The RB actually is actually the negligent party that drives up inflation in the early stages of a interest rate rising program. The economy gets wrecked and businesses shut down. It is when job losses start then consumer demand is curbed by both savers and borrowers. That is why the RBNZ tends to move interest rates up fast usually in 4 or 5 interest rate rising within 12 months intentionally damaging the economy and forcing job losses to curb consumer spending.

LikeLike