The Prime Minister was also on TV3’s The Nation last weekend. Most of the interview was about immigration.

Late last year, I wrote about some earlier, probably rather off-the-cuff, remarks that Key had made about immigration, in which he described the recent high net migration inflows as a “time of great celebration”.

The TV3 interview was a rather more substantial occasion (The Nation isn’t exactly a mass market programme), and it was about the issues, not just an opportunity to attack his political opponents. The Prime Minister will no doubt have been briefed for it by his own DPMC officials, and perhaps also by MBIE, the government department responsible for immigration (administration and policy). And yet I was surprised just how insubstantial his answers were, and a little alarmed at the central planner’s mentality that they evinced. On Radio New Zealand yesterday, Matthew Hooton described the current government as the most interventionist since the 1970s. That mentality was fully on display in John Key’s interview. I had to watch the interview again to be sure that I had correctly heard a Prime Minister from an avowedly centre-right party declare that there was an optimum number of (immigrant) truck drivers.

I was pleased to see that the interviewer kept the focus on the flows of non-New Zealand citizens. New Zealand can’t, and shouldn’t try to, control the comings and goings of New Zealand citizens. We can’t even, and shouldn’t try to, control the outflows of non-New Zealand citizens – the people who come and, after a time, find that New Zealand isn’t quite right for them, or just find an even better opportunity somewhere else. But every inflow of a non New Zealand citizen requires the approval of the New Zealand government – that is what immigration policy is about. (As a matter of policy, we allow any Australian citizens to move here without advance approval but (a) that is still a New Zealand policy choice, and (b) the numbers involved are pretty modest (over the last 40 years the annual net inflow of Australians has fluctuated between 0 and 3500)).

The Prime Minister, of course, was keen to emphasise the fall in the net outflow of New Zealanders. In the data released yesterday, there was still a net outflow of 3890 New Zealanders to Australia over the last year. That is, by the standards of recent decades, a small net outflow, but the people who know New Zealand best – New Zealanders – are still choosing to leave rather than to return (and to a country where real per capita income has been falling for the last couple of years, and hasn’t grown in seven years). That should be telling the Prime Minister something.

The interviewer kept trying to push the Prime Minister to name an “optimal number” for the inflow of non New Zealanders. He consistently refused to do so, asserting that there was no limit to number of arrivals he would be happy with “so long as they add value to New Zealand”. Oddly, neither he nor the interviewer mentioned that actual government policy is rather different. After all, there is a target level for the number of residence approvals granted (45000 to 5000o per annum), that target is approved by Cabinet, and the target has not changed for quite a long time. Despite all the fluctuations in the number of foreign students, or short-term workers, the residence approvals programme is the main way in which immigration policy boosts the population over time. Broadly speaking, I think it is a sensible way to run immigration policy – we shouldn’t be playing around with the target each year in the light of immediate pressure, but setting some medium-term targets and reviewing them from time to time. But there was simply no discussion as to whether 45000 to 50000 is the best target, or how we might know. Why not, for example, 30000 per annum more? Or fewer?

In fairness to the Prime Minister, there was also nothing explicit along the lines often found in MBIE documents, lauding New Zealand’s immigration policy as a “critical economic enabler” or a “key lever” in economic strategy. But he didn’t seem far from that either, but with equally little evidence. He asserts that immigration is a source of growth, without ever being quite clear what he had in mind.

Everyone recognizes that increases in immigration boost demand, and tend to boost total GDP. Bur our real interest should be in per capita or per hour worked measures, whether of GDP or of national income – and, to be even more specific, in what, if any, gains there are to those who were already here. From an economic policy perspective, immigration makes sense if it makes those of us who were already here better off. But despite running one of the largest immigration programmes in the advanced world, neither the Prime Minister, nor his advisers in MBIE and Treasury, have been able to produce any evidence that New Zealanders as a whole have been made better off. In his interview, the Prime Minister didn’t even try to make the case, to (for example) outline the channels by which he believes New Zealanders are being made better off. (And, in fairness, the interviewer didn’t push him to do so.)

Instead, the Prime Minister seemed reduced to assertions that the high rate of immigration is a “sign of success” or even “a badge of honour”, asserting that people don’t want to come to countries that aren’t doing well.

It is surprising that anyone takes that line of argument seriously. At the grim extreme, Turkey, Lebanon and Jordan – none of them terribly well-performing – have been very attractive places to non-natives in the last few years. They are simply (much) less bad than Syria. But more generally, immigrants tend to move from poorer countries to richer countries, and for all its disappointing performance over 60 years or more, New Zealand still offers higher incomes than most of the countries of the world. That people want to come here simply reflects what we already know, that New Zealand is better off than most places. It sheds no light at all on whether New Zealanders are benefiting from the large scale immigration programme run by successive governments. And that should be the question we constantly ask.

It is not as if this is some unimportant question: if New Zealand’s productivity growth or per capita income growth was outstripping that of all its peers there might still be an interesting question as to what contribution immigration was making to that outperformance. But only a handful of people would care much – there would be plenty of prosperity to go round. But we’ve kept on underperforming for decades, despite the allegedly productivity-enhancing immigration programme.

And yet the Prime Minister is adamant that “we need these people”.

I’m not entirely sure why. There are plenty of people around to offer cynical explanations of anything and everything John Key does. Perhaps there is merit to that – as for most politicians – when it comes to tactical choices. But the large-scale immigration programme seems to be one of those things which he genuinely believes in.

No doubt it helps that his official advisers (Treasury and MBIE) keep telling him we benefit from the immigration programme, even if they don’t offer – or even really try to offer – any evidence of those benefits. That inclination is probably reinforced by the fact that the global elites among whom he moves treat the benefits of immigration as almost axiomatic.

And I don’t suppose he has ever seriously engaged with the fact that, despite its poor productivity record, New Zealand has had some of the highest real interest rates in the advanced world for at least the last 25 years, or the possible connection from that (and the associated high real exchange rate) to the weakness of business investment in New Zealand, and the failure to make any progress towards his own government’s (well-motivated but questionable) goal of markedly increasing the export share of GDP.

But I suspect that a significant part of why Key supports such a large immigration programme is because he buys into the skill shortages story. It was the only story that he used in the TV3 interview. Employers tell MBIE, and those taking surveys, that they can’t find staff locally, and that if they can’t find staff it will impede their ability to grow their business. MBIE certainly believes the story – as I wrote about a while ago, it suffuses their annual report on migration trends.

What I find remarkable in this document, as in other MBIE immigration work I’ve seen, is the absence of any sense of market processes, and how the market might sort these things out. For example, if there are excellent opportunities here which New Zealanders are simply ignoring in their rush to get to Australia, surely we’d expect real wages to increase here? If that happened, some of the opportunities might disappear. Some New Zealanders might change their minds about going to Australia. Some people might regard more training as worthwhile, to better equip themselves for those higher-paying opportunities. Some will switch jobs from less rewarding ones, to the ones where the returns are now higher. Some people might work harder or stay in the workforce longer. But not one of these market mechanisms is even discussed. And this from a key economic agency, implementing the policy of a vaguely centre-right government? Does it not occur to them that “shortages” don’t happen in most markets, and when they do they are usually just a sign that the price has not adjusted. Why does MBIE think that labour is different?

Although MBIE and the government seem to see immigration largely as a labour market phenomenon (“a critical economic enabler”), the price of labour “wages” appears only once in the entire document (purely descriptively). “Price” does not appear at all. In fact, “productivity” and “competition” each appear only once, in neither case in the context of an analytical sentence. “Labour market” does appear repeatedly, but almost always only descriptively. There is simply no sense, anywhere in the document, of a competitive market process at work. If one were being unkind, one might think MBIE saw the role of government as being to ensure that the right pegs were in the right holes.

And that seemed to be how the Prime Minister saw it, as he talked of the need to juggle which occupations were on, and off, the approved list, and never once talking about market adjustments, changes in wages etc. In fact, it was where the comment about the optimal number of immigrant truck drivers came in – apparently truck drivers have recently been removed from the list.

From an individual employer level it all makes some sense. Importing a foreign worker really can relieve an individual firm’s shortages. But it simply doesn’t do so economywide, and isn’t necessary anyway. Markets and price/wage adjustments take care of reconciling supply and demand, in and across markets. One might have hoped that the Prime Minister of a centre-right government might, just once, have made that point.

When I make the point about market adjustment, I often get some sceptical comments – higher wages, I’m told, would price producers out of the market. But if we decided to have a much lower level of immigration a lot of things would change. Some industries would shrink markedly. We’d have a fairly flat population, so we’d probably have a much smaller construction sector, freeing up a lot of labour. We’d have lower interest rates, and a lower real exchange rate. Resources would, over time, shift from the non-tradables sector to the tradables sector, as more offshore opportunities became viable for smart New Zealand firms. In some sub-sectors which have been favoured by immigration policy – dairy workers for examples – wages might be expected to rise somewhat, to attract more New Zealanders into the industry. But remember that the real exchange rate would be lower. We simply don’t need government officials deciding which particular skills to import this year.

These arguments aren’t remotely new even in a New Zealand context. In a chapter in the Oxford History of New Zealand in 1981, Victoria University economic historian Professor Gary Hawke wrote

“Ironically, the success with which full employment was pursued until the late 1960s led to frequent claims that labour was in short supply so that more immigrants were desirable. The output of an individual industrialist might indeed have been constrained by the unavailability of labour so that more migrants would have been beneficial to the firm, especially if the costs of migration could be shifted to taxpayers generally through government subsidies. But migrants also demanded goods and services, especially if they arrived in family groups or formed households soon after arrival and so required housing and social services such as schools and health services. The economy as a whole then remained just as “short of labour” after their arrival.”

But 35 years on Radio New Zealand was still leading its news bulletins last night with a story along the lines of “despite record net migration flows, employers claim skill shortages are as severe as ever”. We simply shouldn’t be surprised. Immigration simply does not ease skill shortages in the economy as a whole or, typically, ease pressure on resources. Across a range of colonies of settlement, Prof James Belich illustrated that point quite effectively in his 2009 book Replenishing the Earth.

If there are real gains to New Zealanders from large scale immigration – and the onus really should be on the Prime Minister and other advocates to demonstrate those gains – they simply don’t come that way.

Finally, Auckland. The Prime Minister was astonishingly upbeat in his story about Auckland, and dismissive of the implications for house prices. Now, we can all accept that high immigration does not cause housing market problems, and serious affordability issues, when housing and land supply are only lightly regulated. But that isn’t the New Zealand situation. The government has been unwilling or unable to legislate to facilitate the sort of physical growth of Auckland that would have kept urban land (and house) prices in check. Given that, it is quite reasonable to ascribe much of the rise in Auckland house prices to the immigration policy that the government can, but won’t, change.

But the Prime Minister simply falls back on “global city” arguments. He asserts that Auckland has “reinvented itself”, and now competes on a global stage with cities like Sydney, Dubai, London and so on. According to the Prime Minister, young Aucklanders simply cannot expect house prices to come down again – this is, we are told, the price of being a “global city”.

This is really nonsense on two counts. The first, of course, is that there are plenty of successful fast-growing cities in the United States where real house prices have not risen materially at all, and where price to income ratios remain about as low as they were in New Zealand for decades. As just two examples, Houston and Atlanta are both materially larger, fast-growing, by most counts more successful, and home to much more international business than Auckland is. Yes, real house prices in Sydney and London and Auckland might not ever come down, but if so in each of them that is a direct result of government choices – constraining the supply of urban land in the face of population pressure (in the New Zealand case, the population pressure itself mostly resulting from immigration policy choices).

But perhaps more concerning is that there is just no evidence of this Auckland economic success. Auckland’s population has grown much faster than that of the rest of the country, and Auckland is much bigger than any other place in New Zealand. According to the champions of the immigration programme, and of the application of agglomerationist ideas more generally, this should have seen Auckland’s economic performance pulling away from that of the rest of the country. If anything, the data suggest that the opposite is happening. I ran this chart, from the regional GDP data, a couple of weeks ago.

If Auckland has “reinvented itself” anywhere other than in the heads of the Auckland Council and government officials, it doesn’t look to have been for the better.

The regional GDP data aren’t an ideal measure by any means – and they can be a bit cyclical, as in the short-term Auckland benefits from the initial boost to spending from high immigration flows, and suffers when immigration slows – but once again there is just no sign of the gains (incremental or transformational) that the advocates of the immigration programme, as a key economic lever, would have been looking for. International trade isn’t growing (share of GDP), productivity growth remains disappointing, our biggest and fast growing city is slipping relatively. All we are left with is some large distributional effects: firms in the non-tradables sector do okay, but those in the tradables sector suffer (and others never even get started); those who own land in Auckland do well, while those who ever want to buy into that market suffer. And so on.

There are plenty of year to year fluctuations in overall net migration numbers. They shouldn’t really be the focus, and even if they were there are distinct limits to what governments can do about them. But we deserve a much more compelling case for how the large scale medium-term immigration programme is benefiting New Zealanders as a whole than the Prime Minister (or his officials and ministers) has given us.

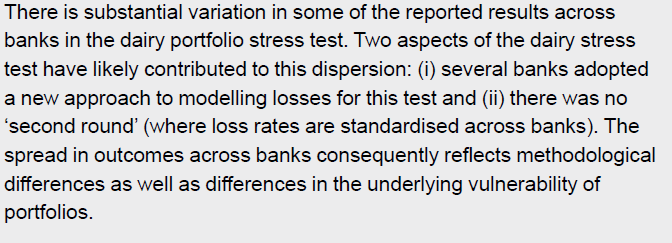

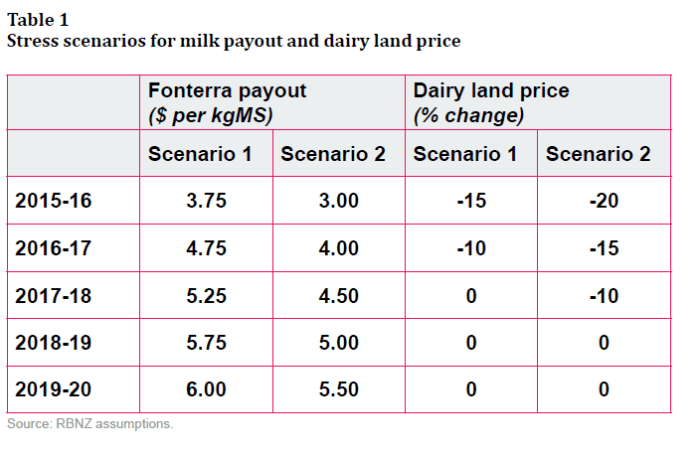

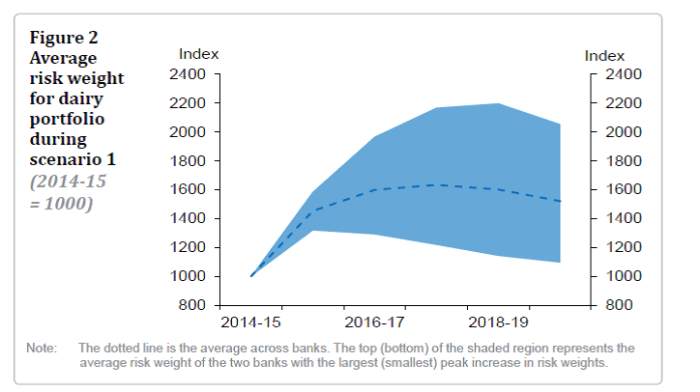

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release.

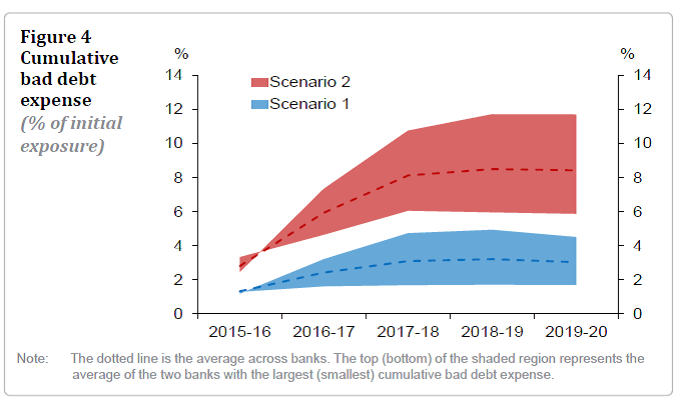

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release. In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As

In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As

I

I