That was the question a radio interviewer asked me this morning, about the talk of new Reserve Bank direct controls on banks’ housing lending. He wanted a succinct answer. Mine was simple: No. The question was about talk of loan to income ratio restrictions, but the answer would be the same even if the question had been about the Financial Stability Report as a whole.

Take the talk of loan to income restrictions on banks’ housing lending first. There was no mention of this in the FSR itself, and even in the press release there was just a brief, but telling, reference:

The Reserve Bank is closely monitoring developments to assess whether further financial policy measures would be appropriate.

And yet clearly it is a major issue. In fact, it dominated the press conference later in the morning. Journalists asked question after question, and slowly drew information out from the Governor and Deputy Governor. But there seemed to be no clear communications plan, and no developed messaging. And none of the material was in the statutory accountability document they had just published. It wasn’t impressive.

As Treasury pointed out last year, in many ways if the country is going to be dragged down the path of direct restrictions on banks’ loan portfolios, it would have been better to have looked first at loan to income restrictions (“speed limits”) rather than loan to value restrictions. Servicing capacity is typically more important than the current value of collateral. The Reserve Bank could have adopted loan to income restrictions back in 2013. But the Governor was in a hurry. There was, in his telling, a desperately urgent issue and the Bank simply couldn’t wait: it had to do something, and LVR restrictions were what could be done very quickly. The policy process in the lead-up to those restrictions was shockingly bad – one (unelected) man had a bee in his bonnet, and there was little or no debate or discussion allowed (trying to pose some questions was when I got offside with the Governor).

Back almost three years ago when those restrictions were put in place, all the talk was of the temporary nature of the restrictions. When people discussed it internally, I think most people had a sense that “temporary” might mean a couple of years. The true believers thought that the top would have been knocked off the housing market by then, with the LVR restrictions having limited the new debt taken on in the last upward surge, and then things could get back to normal – leaving bankers to decide the composition of their own portfolios.

But then we had a new wave of LVR restrictions last year. In 2013, the Bank had not only seen the restrictions as temporary, but it was staunchly opposed to having different policies for different regions. By last year we had new LVR restrictions – this time some mortgage borrowers were judged better than others, even for exactly the same underlying risk characteristics, and banks were allowed to lend in some places but not others. And now the drums are beating for yet more restrictions – perhaps even tougher, perhaps more differentiated, LVR restrictions, or perhaps loan to income restrictions. There seems to be no end in sight.

Asked about this yesterday, the Bank seemed a bit bashful. The Deputy Governor noted that the Bank had never seen these things are permanent but………housing and financial cycles can be very long, so “temporary” might still be rather a long time. I suppose exchange controls – and all the other restrictions that Walter Nash and his successors imposed on us in decades past – weren’t permanent either. It “only” took 36 46 years to get rid of exchange controls.

Frankly, the Bank seems torn between two poles, and just hasn’t done the hard thinking or analysis – or been exposed to the hard questioning by MPs and the media – to reconcile the two stances.

On the one hand, as they note in the opening sentence of the press release “New Zealand’s financial system is resilient”. (That was also the story three years ago, when LVR limits were first imposed, but then the excuse was “but it might not stay that way if we let things carry on”). As I noted (at length) last year, the stress tests the Bank had done in conjunction with APRA also suggested that the banking system could cope with very severe adverse shocks (including surges in unemployment on a scale beyond anything ever seen in floating exchange rate countries). The latest FSR reported the results of new stress tests (reported in Box C of the document), done late last year. The Bank did not publish a great deal of detail this time, but if anything the shocks look to have been a little more severe than those used in the earlier stress tests (no doubt befitting the further rise in house prices). Once again, banks seemed to come through largely unscathed. Total loan losses amounted (over several years) to around 4 per cent of initial assets – similar to the 2014 result. Of this, 0.6 percentage points related to Auckland property lending. As the Bank noted, loan loss rates on the housing mortgage books were only around 40 per cent of those observed for most other sectors. There is simply no evidence that banks – individually or collectively – have been doing housing lending in a way that would jeopardise their own financial soundness or that of the financial system. That is consistent with the international results – which the Bank has previously cited – in which vanilla housing lending has rarely played an important role in systemic financial problems (especially in floating exchange rate economies).

And yet, and yet…..they reach for ever more direct restrictions on banks. Now don’t get me wrong. The New Zealand housing market (and especially that in Auckland, which is exposed to more pressures) is a disgrace. There is no excuse for price to income ratios of 5, let alone those of around 10. And central and local government policymakers are almost entirely responsible for those outcomes. The Bank seems to half recognize this. They talk of the interacting pressures of high rates of immigration at the same time that the urban land supply market isn’t working well. But they don’t follow this point to its logical conclusion. If the prices are largely the outcome of structural policy choices, there is no particular reason to think they are the fault of banks, or borrowers, let alone the despised class of “property investors”. The Reserve Bank’s job is to use its regulatory powers to promote a sound and efficient financial system. But the stress tests – and their own regulator judgements, expressed in the press release – suggest that the system is sound, robust and resilient. And yet with every new set of restrictions they further undermine the efficiency of the financial system.

There are severe housing market policy problems, but there is no evidence that they are problems the Reserve Bank is responsible for, or needs to take action to try to remedy or ameliorate. As I noted the other day the Reserve Bank has two main jobs. The first is the soundness and efficiency of the financial system, and the second is keeping inflation near target. At present, they are failing at the latter, are continually compromising the efficiency of the financial system, and all while skewing are policy (both regulatory policy and monetary policy) towards action supposedly designed to make safe a financial system that they tell us is already robust.

I couldn’t check this electronically this morning, but my impression was that there was almost no discussion at all in the FSR on the efficiency of the financial system, and the impact of Reserve Bank regulatory measures on the efficiency of the system. That looks to be out of step with the statutory requirements for these documents. I also thought it was interesting that there was little or no discussion of banks’ lending standards and practices. I know the Bank is dominated by people with a macroeconomics background, but surely we expect to learm something in a document of this sort about the judgements the Bank, and its supervisors, are making about credit standards?

I wanted to pick up just three more dimensions of the material the Bank covered in the FSR.

The Bank went to some lengths to argue that the LVR restrictions might have had only a “transitory” impact on house prices (the Deputy Governor’s words) but had led to a structural improvement in the quality of loans on bank balance sheets. In support of this claim they produced a chart showing a reduction in the share of mortgages with LVRs in excess of 80 per cent. In fact, there are all sorts of problems with this claim. First, they don’t show us what has happened to the proportion of loans with LVRs just below 80 per cent (or just below 70 per cent for Auckland investors). The difference in the riskiness of a loan with an 80.1 per cent LVR and one with a 79.9 per cent LVR is trivial, and yet regulatory restrictions typically impose these sorts of cliffs, with lots of loans gathered just on the approved side of the limit (and in ways which don’t appear when there are no regulatory restrictions). The data mean different things in a regulated environment.

But that isn’t the end of the issue. First, if people couldn’t borrow 85 per cent of the value of a house from a bank themselves, some will deterred from buying for the time being. They might save a bit more and then go and buy. But others will turn to other sources of credit. The Bank correctly notes that there has not been a big increase in housing lending by non-bank lenders (not covered by the LVR restrictions, since the Bank has no legal power to impose such restrictions on them). In itself, that lack of (this form of) disintermediation is interesting – and perhaps worthy of further analysis (especially as it points to quite high efficiency costs from the restrictions).

But non-bank lenders aren’t the only alternative sources of credit, In many cases, parents or family members will have been tapped. In some cases, those family members will be in a very good financial position and might be happy to lend from their credit balances. But in other cases, a lower mortgage for the child might be offset by a higher (if still less than 80 per cent) mortgage for the parent. In a crisis it is not individual loans that threaten the soundness of banks, but the exposures across whole portfolios. It is quite possible that much of the apparent reduction in risky housing lending is offset by a general weakening in the overall credit quality of the portfolio. If not, it would still be useful for the Reserve Bank to have engaged with the issue and explained why it concluded that these issues were not material.

Relatedly, the Reserve Bank has simply never engaged with the behavioural responses of banks to direct restrictions on portfolio composition (which we had simply never had in New Zealand prior to 2013). These are profit-maximizing businesses. If Reserve Bank restrictions limit high LVR housing lending, it reduces profit opportunities (and use of capital) in that part of the business. But what have banks done to maintain their profits and ensure that capital is fully deployed? Surely a common take on regulatory restrictions is that they might dampen the risks we can see, while encouraging additional risk taking in less obvious areas. I don’t know how banks responded to the LVR restrictions, but I’m pretty sure the response to the LVR restrictions wasn’t “you know, Graeme, you are right: we shouldn’t be seeking so much profit, and instead we’ll send the capital we would have been using in that business line back to Australia”. I think we are owed better analysis of these issues from the Reserve Bank (and its large pool of analysts) before we accept that LVR restrictions have actually improved the soundness of the financial system.

In a sense, what each new set of regulatory interventions seems to do is the provide cheaper entry levels to the market for those purchasers who aren’t directly affected by the regulatory restrictions. Each time a new set of interventions is announced there is a bit of a pause, and those pauses look like buying opportunities for those who can (at the expense – pure and simple – of those who can’t – those upon whom the Reserve Bank looks unfavourably). The favoured might be the middle-aged trading up, cashed-up New Zealanders returning from abroad, those whose value to the banks means they are favoured recipients of credit from within the speed limits, those with wealthy parents etc (and even the non-resident foreign buyers, a significant part of net new demand in the Auckland market). In general, the interventions advantage the haves at the expense of the have-nots. Such redistributive policies might be what we elect politicians to do, but they shouldn’t be what unelected central bankers are about.

One keeps hearing disapproving comments – including from the Reserve Bank – about people purchasing residential properties to run rental services businesses. I know there is a strong community bias in favour of owner-occupation, and that the rate of owner-occupation has been falling. But here the Reserve Bank – and others who engage in this tarring of people in the rental services business – is simply engaged in scapegoating. All societies need scapegoats – to bear symbolic responsibility for what has gone wrong – but if they are going to be part of a good policy regime there needs to be rather more robust differentiation between symptoms and causes. If central and local government policies on immigration, land use, and building, combine to make house prices unaffordably high to young couples starting out, it is hardly surprising that those people end up renting (for longer) instead. And someone has to own the houses. The Reserve Bank was again citing yesterday statistics suggesting that around 40 per cent of housing sales are to “investors”, but why would this be a surprise (or even a concern, giving the “rigged” housing market?). The home ownership rate itself is dropping towards 60 per cent, most rentals are provided by the private sector, and the median investment property is probably turned over a bit more frequently that the median owner-occupied house.

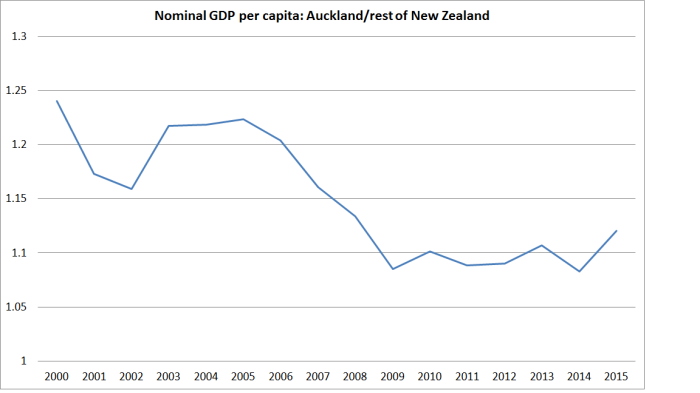

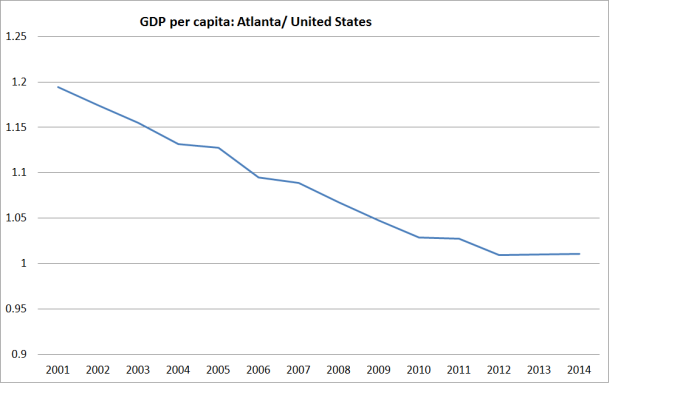

Finally, the Reserve Bank notes – in a concerned fashion – that household debt to income ratios are now (just) around the pre-recession peak. In itself, this is a fair enough observation, but as so often in these documents it is the context or interpretation that is missing. As I’ve noted before , there was no sign that the level of household debt as it was in 2007/08 lead to serious or systemic financial problems. And that was so even though all the research evidence suggests that it is large increases in debt to income/GDP ratios in short periods of time that has often foreshadowed financial crises. The fact that debt to income ratios now are not materially higher than they were eight years ago – coming off 15 years in which that ratio had increased enormously – should be a source of comfort rather than concern. We simply don’t have a good sense of what an “equilibrium” debt to income ratio is, and (in any case) such an equilibrium is likely to be highly endogenous to the extent to which the housing market is distorted by structural factors. In Atlanta – where median house prices are around US$180000 and house price to income ratios ar around 3 – household debt to income is likely to be much much lower than it is in Auckland.

And the causation runs largely from housing distortions and house prices to debt, and not the other way round. It is disappointing that the Reserve Bank never explicitly recognizes that if house prices are driven higher by the interaction of immigration and supply restrictions – and that is exactly what the Governor says – younger generations will need to have more gross debt relative to income to buy the housing stock from older generations, than would be the case in a less distorted (much cheaper) market.

There was some interesting material in trhe FSR, but in the end it fell well short of what we should expect – or even of what the law requires. Wielding so much discretionary regulatory authority single-handed – in a way that simply shouldn’t be happening in our parliamentary democracy – the unelected Governor surely owes the public much more in-depth analysis of the issues and risks before we lurch into yet another ill-considered hasty patch on the symptoms of a serious problem, responsibility for which rests in the Beehive and – to a lesser extent – in council chambers up and down the country? The quality of the supporting analysis for last two LVR interventions was threadbare (or worse). As they continue to undertake the analysis on further restrictions – and talk to the Minister and Treasury, as part of getting loan to income limits on the (non-binding) list of tools in the MOU – lets hope that the quality of the argumentation and research evidence rises to much better levels than we have seen to date.

As a final point, there was some mention in the FSR of the results of the Reserve Bank’s regulatory stocktake released late last year. In that stocktake there was encouraging talk from the Bank of adopting longer consultative times for regulatory proposals and of possibly finally moving to routinely publishing the submissions they receive (as many other agencies, and select committees do, but which the Reserve Bank has consistently refused to do.). There was nothing on either of these points in the discussion in the FSR yesterday. I hope they are not backing away again.

UPDATE: This afternoon the Reserve Bank has put out a consultative document on the possibility of publishing submissions. It appears to be strongly skewed towards maintaining the status quo.

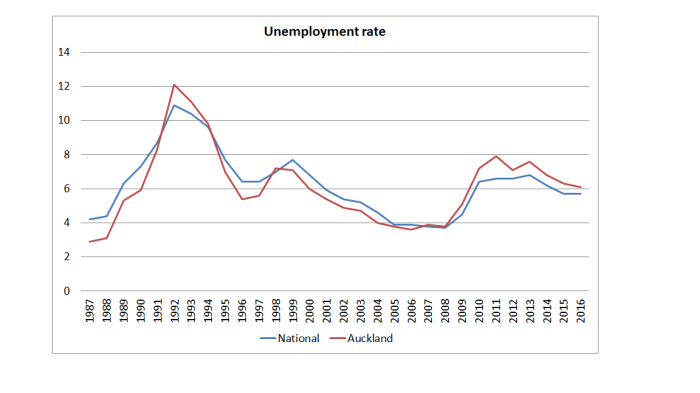

And it isn’t just that Christchurch has had a very low unemployment rate through the repair and rebuild period. Graphing the Auckland unemployment rate against that of the median region produces much the same picture.

And it isn’t just that Christchurch has had a very low unemployment rate through the repair and rebuild period. Graphing the Auckland unemployment rate against that of the median region produces much the same picture. And the massive increase in student visa numbers (mostly to second tier non-university entities), many of whom later acquire residence, is on top of that.

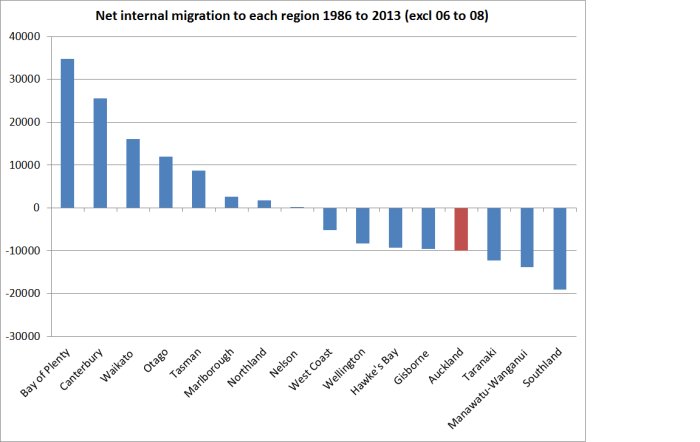

And the massive increase in student visa numbers (mostly to second tier non-university entities), many of whom later acquire residence, is on top of that. Net, a small number of New Zealanders left Auckland for other parts of the country. Relative to Auckland’s population, the estimated outflow is tiny, but there is just no sign of New Zealanders flocking to the “success” of Auckland (and note that this period includes the outflow of people from Christchurch in couple of years after the earthquakes). Perhaps things have been different in the last three years, for which we don’t yet have data.

Net, a small number of New Zealanders left Auckland for other parts of the country. Relative to Auckland’s population, the estimated outflow is tiny, but there is just no sign of New Zealanders flocking to the “success” of Auckland (and note that this period includes the outflow of people from Christchurch in couple of years after the earthquakes). Perhaps things have been different in the last three years, for which we don’t yet have data.