In almost any well-functioning country, The Treasury should be one of the very best government agencies: a repository of wisdom, experience, rigour, and the skepticism that comes from seeing all too many “bright ideas” put forward over the years. If the Secretary to the Treasury is going to give public speeches – and there are reasonable arguments that someone in that role shouldn’t (one doesn’t come across public speeches from the chief executives of MBIE or MFAT, two other major departments) – we might reasonably expect something judicious and rigorous, and which provides at least some fresh and interesting insights on the issues he is addressing. It should be a public reflection of the very best of the sort of insight and advice The Treasury is offering their primary “customer”, the Minister of Finance.

As an example, speeches by Ken Henry, the former head of the Australian Federal Treasury, almost always met that standard – I looked forward to reading them, and expected to see some or other issue or argument a little differently as a result. It isn’t about whether or not one agrees with the points the speaker is making – often one learns most from thinking hard about cases made by able advocates of an alternative view – but about the quality of what is on offer.

The speeches of our current Secretary to the Treasury simply don’t reach that standard. On Thursday I wrote about Gabs Makhlouf’s recent speech about disruptive technological change. Only a true believer can have felt better for reading it – deriving, perhaps, a sense of validation in having such a senior official, a pillar of the establishment, say it.

Perhaps more disconcerting was Makhlouf’s speech earlier this week titled (apparently with reference to the title of Oscar Wilde’s famous play, The Importance of Being Earnest: A Trivial Comedy for Serious People) The Importance of Being Auckland: Strengths, Challenges, and the Impact on New Zealand, delivered to something called the “Committee for Auckland Advisory Group Summit”.

It is a disappointingly poor speech – I wish I could say I was surprised, but I wasn’t really. It was a piece that combined lightweight analysis, (very) selective choices of evidence, and a use of rhetoric that might have been becoming from a Cabinet minister pursuing voters, but should have been beneath a senior public servant. It was all too similar to previous speeches: not just one bad example amid an otherwise solid record.

There were three main parts of the speech. I don’t have anything to say on the material on infrastructure, much of which is simply a list of points from another report.

Makhlouf begins with a celebration, in a section headed “Auckland’s Strengths”. The text reaffirms Makhlouf’s position as a true believer: a rapidly growing population is apparently something to celebrate, and the cultural/ethnic diversity of the city is “exciting”. Here is what he has to say

Why do I find this exciting? It’s because high levels of diversity provide dividends including through increases in innovation and productivity.

Auckland’s diversity is particularly critical for our international connections. There’s much more to international connections than trade. It’s the other international flows – flows of capital and people, and the accompanying flow of ideas – which are the key to reinventing trade, and which will lay the foundation for a more prosperous New Zealand in the long-run.

The high number of overseas-born Aucklanders can bring new skills, new ideas and a diversity of perspectives and experiences that help to make our businesses more innovative and productive. And perhaps most importantly, they often retain strong personal and cultural connections to other parts of the world, which opens up, and helps us to pursue, new business opportunities.

Auckland is truly New Zealand’s gateway to the world. It’s not just that there is a big number of companies here doing business internationally. It’s the port and airport linking the country to global markets; and tertiary institutions, researchers and innovators linking us to global knowledge.

Which might all sound fine, until one starts to look for the evidence. And there simply isn’t any. Perhaps 25 years ago it was a plausible hypothesis for how things might work out if only we adopted the sort of policies that have been pursued. But after 25 years surely the Secretary to the Treasury can’t get away with simply repeating the rhetoric, offering no evidence, confronting no contrary indicators, all simply with the caveat that in “the long run” things will be fine and prosperous. How many more generations does Makhouf think we should wait to see his preferred policies producing this “more prosperous New Zealand in the long run”?

If the Secretary to the Treasury was going to address the economic issues around Auckland, one might have hoped there would be at least passing reference to:

- New Zealand’s continuing relative economic decline, despite the rapid growth in our largest city,

- Auckland’s 15 year long relative decline (in GDP per capita), relative to the rest of New Zealand,

- The contrast between that experience, and the typical experience abroad in which big city GDP per capita has been rising relative to that in the rest of the respective countries,

- The failure of exports to increase as a share of GDP for 25 years,

- The fact that few or any major export industries I’m aware of our centred in Auckland (the exception is probably the subsidized export education sector) – and by “centred” I don’t mean where the corporate head office is, but where the centre of relevant economic activity is.

He might also have linked to the recent presentation by Jacques Poot (in a Treasury guest lecture), in which Poot was keen not to sound very optimistic about just how large those economic benefits of diversity really are, or to the work of Bart Frijns – an (immigrant) professor in Auckland (see last sentence of the extract above) – whose recent work suggests that on some measures, in some contexts, there may be net costs, not benefits at all.

Of course, one can’t say everything in a single speech, but when a credible case could be made that the Auckland-centred model is in serious trouble, it is bordering on the seriously unprofessional to not even allude to any of these sorts of points, even if only to explain why the Secretary interprets then differently than, say, I might.

So keen was Makhlouf not to undermine his good news creative fiction about the Auckland economy that the one difficulty he does allude to is buried under a different heading “Social Outcomes”.

Let me start with social outcomes. Auckland scores well on quality of life indicators but other measures suggest not everyone is able to enjoy what Auckland has to offer. Social outcomes vary significantly across Auckland, highlighting the potential importance of sub-regional thinking and analysis to lift social outcomes across the board in Auckland.

Issues with the labour market contribute to patchy social outcomes across the city. While Auckland has higher productivity than other urban centres in New Zealand, it also has an underutilised labour force. For example, the five year average unemployment rate in South Auckland is 11.7 percent compared with 6.3 percent for the rest of Auckland and 6 percent for New Zealand overall. That’s the sort of discrepancy that has a real impact on the quality of life of families and communities.

To the first paragraph one can only say “And?” In what city – or decent-sized town – ever did “social outcomes” not “vary significantly”?

Similarly, differences in the unemployment rate across groups within cities will occur everywhere – if we had the data, I’m sure the unemployment rate would be higher (and probably the participation rate lower) in Porirua than in Karori/Kelburn. It might be good if were not so, but it isn’t obviously an Auckland-specific issue. After all, across the country as a whole, the average unemployment rate over the last five years for Europeans has been 4.3 per cent, while that for Maori has been 14.7 per cent, and that for Pacific populations has been 13.4 per cent. Given that the population of South Auckland is disproportionately Maori/Pacific, the issues in South Auckland seem most likely to be mainly national than (intra-Auckland) suburban.

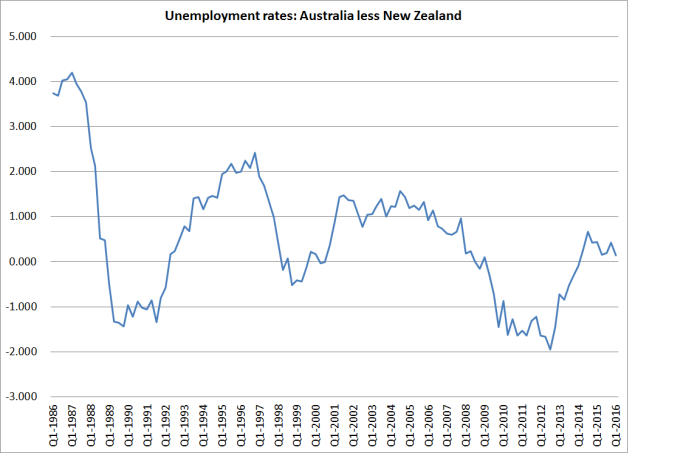

But there is an Auckland underperformance that might almost escape you if you didn’t read that second paragraph quite slowly and carefully. The unemployment rate in Auckland is higher than that in the rest of New Zealand. For a long time, that wasn’t so.

The chart shows the gap between the unemployment rate for New Zealand as a whole. Over the history of the HLFS until around 2007, Auckland’s unemployment rate averaged a bit below that of the rest of the country. There was some clear cyclicality to the gap – Auckland’s economy/labour market seems to have been more badly hit in recessions (I’ve highlighted the 1991 and 1997/98 recessions) and does relatively better in good times. In a well-functioning economy, that better performance is what I’d expect. After all, the Auckland labour market is so much deeper, and more diversified, than that in other centres, that it should be easier for workers and firms to find each other, matching the skills offered and required, than in a smaller area, typically prone to more idiosyncratic shocks.

But even by the end of the last boom, Auckland’s advantage seemed to be fading. And in every single quarter since the start of 2007 – nine years now – Auckland’s unemployment rate has been above that in the country as a whole. The gap is slowly closing again – but the operative word is “slowly”. It is a quite stunning example of the (frankly rather surprising) extent of Auckland’s economic underperformance. It certainly has “social” implications for the people adversely affected, but make no mistake, it is a striking economic issue. And with barely a mention by the government’s chief economic adviser in a speech on the importance of Auckland’s economy.

I was going to write quite a bit about the second half of Makhlouf’s speech, on house prices and housing supply. I have lots of scrawls in the margins of those sections, about both substance and style. Like Graeme Wheeler, Makhlouf appears to have it in for “speculators”. And I’m sure, for example, that Makhlouf’s comments that central and local government have “been working well together” in “addressing the housing challenge” must be a great comfort to those priced out of the market by the combination of central and local governments rules and policies. They are probably more interested in outcomes – which are shockingly bad – than in knowing that the bureaucrats are working well together.

But perhaps the line that caught my eye most was one that Treasury consciously chose to highlight on its Twitter feed: “Auckland NIMBYism hurting New Zealand”. Perhaps “NIMBY” is a convenient shorthand in the popular press, and among sloganeers. One might have hoped that the Secretary to the Treasury might have avoided clearly pejorative labelling of people, whose interests stands in the way of his preferences. There is no analysis – even by way of allusion – to the fact that in most new residential developments, private covenants (voluntary contracts) provide exactly the sorts of binding protections (and more) that residents of Orakei or Epsom might be looking to councils for in the current Auckland debate. Reasonable people might differ on where the lines should be drawn, and quite which existing features of communities should be able to be protected. But to simply decry the interests of property owners seems closer to demagoguery than to detached analysis and insightful policy advice. It also occurred to me to wonder quite what the longstanding residents and property owners in existing suburbs might make of someone fairly fresh off the plane from the UK telling them how their suburbs should be changed. I’m quite sure that Makhlouf has the best interests of New Zealanders at heart, but when you are a newly-arrived outsider, sometimes you need to be conscious of quite how you sound, and quite what your stake is in the country you are advising on, relative (say) to those who have lived their whole lives in Auckland.

In closing his speech, Makhlouf offered this odd paragraph:

The famous photographer Sir Cecil Beaton once appealed to people to “be anything that will assert integrity of purpose and imaginative vision against the play-it-safers, the creatures of the commonplace, the slaves of the ordinary.” From what I can see, many Aucklanders are heeding that call in their own way. And having the right infrastructure, supported by economic incentives that send clear, efficient and effective signals, will enable Aucklanders to continue to exercise their dynamism and diversity and to do the best that they can do.

When I looked up Beaton, his seemed a somewhat reckless life, ending in financial stress. Perhaps it is the style the dreaded “speculators” emulate – but then we already know Makhlouf disapproves of them. Surely most people, in most places, in most times, crave the security of a home, an income, a family, the commonplace things that mostly conduce to sustained happiness (and prosperity for that matter). Risk is, of course, part of life, and many of the great financial successes involved some mix of great risk and great luck. But we seem to be in an upside-down world in which a Secretary to the Treasury (self-described cautious guardian of the government’s finances) scorns the natural concerns of the vast mass of people. One might add, that – with the full support of the Treasury – we’ve been eschewing the commonplace, and the “play-it-safers” in our Think Big policy for Auckland over the last 25 years. And there is little good – for the vast mass of Aucklanders (and New Zealanders) – to show for it.

Makhlouf quotes various English figures in his speech. I’ve always been quite keen on Kipling. In his famous poem “If” comes the lines

If you can make one heap of all your winningsAnd risk it on one turn of pitch-and-toss,And lose, and start again at your beginningsAnd never breathe a word about your loss;…you’ll be a Man, my son!

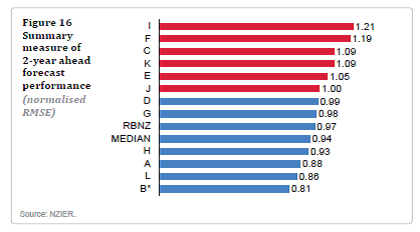

The median forecaster is between forecasters J and D. Again, the Reserve Bank looks no better (or worse) than the group of forecasters clustered near the median forecaster.

The median forecaster is between forecasters J and D. Again, the Reserve Bank looks no better (or worse) than the group of forecasters clustered near the median forecaster.