There was an interesting post from Peter Nunns on Transportblog the other day, attempting a bit of a back-of-the-envelope decomposition of how various factors, including land use restrictions, might have contributed to the rise in real Auckland house prices over the 15 years since the end of 2001.

Nunns starts his decomposition with the suggestion that:

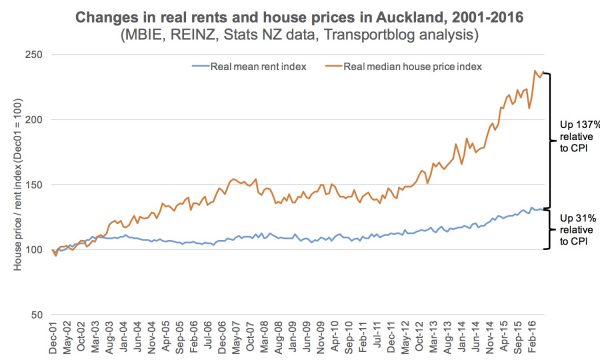

One simple way to disentangle these factors is to look at the relationship between consumer prices, rents, and house prices:

- When rents rise faster than general consumer prices, it indicates that housing supply is not keeping up with demand

- When house prices rise faster than rents, it indicates that financial factors – eg mortgage interest rates and tax preferences for owning residential properties – are driving up prices.

and with this chart

Disentangling the contribution of various factors isn’t easy. A lot depends on what else one can reasonably hold constant. Nunns seems to assume that holding real rents constant is a reasonable benchmark, and that we can then think about the change in net excess demand for accommodation by looking at deviations from that benchmark. Thus, roughly, he suggests that a 31 per cent increase in house prices can be accounted for by supply shortfalls.

Over this period, I’m not at all convinced that is right. Why?

Largely because of the big changes in long-term interest rates, which – all else equal – should have affected supply conditions in the rental market. Specifically, when interest rates fall a long way it is a lot cheaper than previously to provide rental accommodation (the available returns on alternative assets having fallen so much).

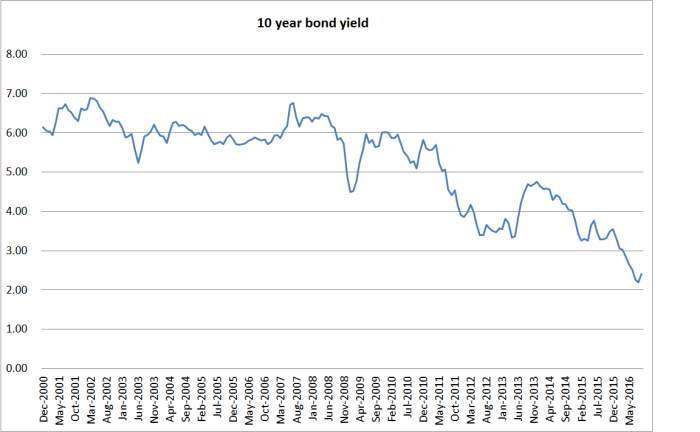

And what has happened to interest rates over this period? Well, here is a chart of the 10 year bond rate since the end of 2000.

There is always a bit of noise in the series, but long-term nominal government bond yields are now about 350-400 basis points lower than they were in 2001. A little bit of that is falling inflation expectations (around 50 basis points according to the Reserve Bank survey). But fortunately in 2001 we also had a 14 year government inflation-indexed bond outstanding, and we do so now as well. In late 2001, that indexed bond yielded about 4.6 per cent, and the current yield is around 1.6 per cent. Real long-term bond yields look to fallen by at least 300 basis points (and around two-thirds of that fall has taken place in just the last five years or so).

Short-term real interest rate haven’t fallen that much. Short-term rates are more volatile, so here I use a two year moving average.

| 1st mortgage rate | 6mth term deposit rate | |

| Dec 2001 | 7.99 | 5.86 |

| Sept 2016 | 6.14 | 3.59 |

Even on these measures, real interest rates have fallen by perhaps 1.5 percentage points.

In a well-functioning housing supply market, those sorts of falls in real interest rates might reasonably have been expected to be reflected in lower real rents.

Quite how much a fall one might have expected in such a market will depend on a variety of assumptions one makes. But if landlords had been looking for an 8 per cent annual real return on rental properties back in 2001, then even a 2 percentage point fall in real interest rates, might readily have been consistent with a 25 per cent fall in real rents – in a well-functioning housing market. If real risk-free rates have fallen by more like 300 basis points – as the indexed bond market suggests – that would be consistent with more like a 40 per cent fall in the rental cost of long-term assets.

These are all illustrative hypotheticals. They assume that new assets can readily be generated. But in a well-functioning housing markets, new houses can be readily generated. New unimproved land can’t be (there is a given stock, only what it is used for can be changed). But in well-functioning housing markets, the unimproved land component of a typical new house+land package will be quite low. Think of dairy land prices at perhaps $50000 a hectare and you start to get the drift. All else equal, in well-functioning housing supply markets, when interest rates fall unimproved land values should be expected to increase, but the value of land improvements and houses shouldn’t be much affected at all.

But even that story is a cautious one (biased to the upside). After all, interest rates typically fall for a reason – big trend falls don’t occur in isolation. One such factor is low expected future returns (eg lower expected rates of productivity growth). And interest rates are not a trivial factor in the cost of land improvements, associated infrastructure, and house building itself. Again, all else equal, lower interest rates should lower the real cost of bringing new houses onto the market – reinforcing the expected fall in real rentals.

Of course, this is so detached from the reality of Auckland (or New Zealand more generally) housing markets that it is difficult to even envisage such a scenario. We have land use restrictions – which tend to produce high land prices and high rents – and when those restrictions run head on into severe population pressures (especially unanticipated ones), it is hardly surprising that house and land and rental prices rise. But when that clash (between land use rules and rising population) occurs at time when real interest rates have been falling a lot, looking at trends in rents can badly confuse the issue.

I’m not wedded to a story in which all the increase in real house prices in recent years is down to supply restrictions interacting with rapid population growth. In his piece Nunns notes a couple of other possibilities

some other ‘financial’ explanations could include:

- New Zealand’s tax treatment of residential property, and in particular investment properties – unlike many of the countries we ‘trade’ capital with, we don’t have any form of capital gains tax on property. All else equal, this means that we should expect structural inflows of cash into our housing market, driving up prices

- The impact of ‘cashed-up’ buyers coming in without the need to borrow money to invest in properties – including, but not limited to, foreign buyers.

But….our tax treatment of investment properties has become less favourable not more favourable over the last few years (reduced and then abolished depreciation provisions, the introduction of the PIE regime, lower maximum marginal tax rates. If these arguments have force at all – and they typically don’t when supply is responsive – they should have worked in the direction of (modestly) lowering house prices over the last decade or so.

And while I suspect there is something to the “cashed-up foreign buyer” story, again any such demand only raises house prices when supply is unresponsive. If supply is responsive – which it would be without all the land use restrictions – such demand would be just another export industry.

Of course, the common story is that lower interest rates have raised house prices. And perhaps they have to some extent, but (a) recall that interest rates are lower for a reason, and real incomes now (ie the expected basis for servicing debt) are much lower than would probably have been expected a decade ago, and (b) lower real interest rates do not raise the equilibrium price of even a long-lived asset if that asset can be readily reproduced. In well-functioning housing markets, houses can be, and unimproved land is a small part of the total cost. If lower interest rates raise house prices, it is only to the extent that land use and building restrictions make it hard to bring new supply to market. (As it happens, of course, in much of New Zealand real house prices are no higher than they were a decade ago when interest rates were near their peaks.)

To a first approximation, trend rises in real house prices are almost entirely due to supply constraints. There can be all sorts of demand influences – some government-driven, some not – and it can be useful to identify them, but in well-functioning housing supply markets they don’t generate rising real house prices.

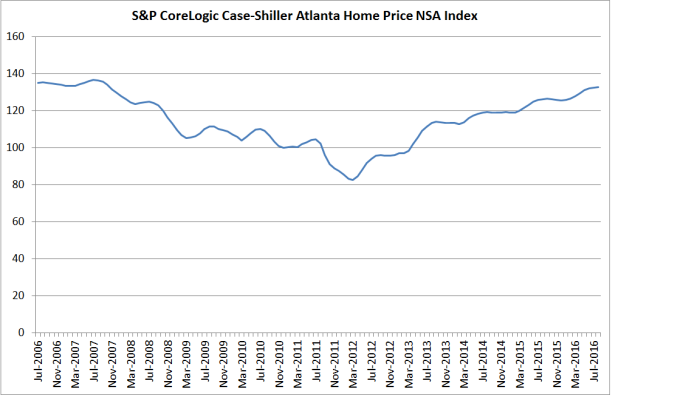

As just one illustration, here is a chart of nominal house prices for Atlanta over the last decade. Atlanta has had rapid population growth, has experienced significant falls in real interest rates (like the rest of the US), is in a country with mortgage interest deductibility for owner occupiers, and is not obviously a worse safe-haven for Chinese money fleeing the weak property rights of China, and yet nominal house prices are no higher than they were in 2006.

Thanks Michael. It is great that the in depth economic analysis matches the superficial (common sense?) take on affordable housing. Being if we reform conditions in a way to make it is easier to build new houses then house prices and housing costs (rents) will become cheaper.

You might be interested about the diverse range of support mine and yours recent writing about housing is getting. Check this out https://medium.com/@brendon_harre/housing-affordability-the-question-is-why-not-how-or-what-cefffd2f9924#.lcmuaeikf

LikeLike

You are right that a discussion about house prices really is a discussion about the price of money (interest rates) due to the leverage that marginal buyers need to purchase a house in the first place.

There are plenty of cashed up buyers – cf the H10 series from the RB recently on the value of the housing stock vs the level of mortgage debt – the LVR is comfortably below 30%… so not all of them are from offshore (China) at all.

A couple of other points that impact on supply:

– Council costs and timeframes… we have seen a number of instances in Auckland where developers have been turned away because Watercare won’t connect them to its system, and the infamous delays in getting consents through the Council processes…

– The amount of cash need to connect to Watercare is now $13k per dwelling and the Reserve Contributions in some parts of the city are well over $30k… you can’t get affordable housing because the council charges so much that its impossible!

Also there has been a big decline in the liquidity in the secondary market… the number of listings shown on realestatae.co.nz is down almost 7,400 compared to October last year, or 24%… that’s quite a drop over 12 months and speaks to a tight market wherever you look…

LikeLike

Actually the BIG problem is the cost of land. $30K of fees per dwelling is nowhere near as significant a problem as a land price ranging from $1,000,000 per hectare at the fringe, to many millions per hectare closer to the centre of a city. Out of this raw land at this price, there needs to be space sacrificed for roads, footpaths, public space, etc. The raw land cost contribution to a $300,000 section of 1/10 of an acre, is easily over $250,000.

As Michael says, even good dairying land is $50,000 per hectare, and there is plenty of this within practical driving distance of the urban area in most cities. This is the crucial element in all truly affordable, stable-price cities: that $50,000 per hectare (or less) land is the opportunity for market-disrupting developers to put <$100,000 1/4 acre sections on the market. It is undeniable that this works in practice in dozens of US cities still – and it used to work here before growth boundaries. In fact Council "planners" tended to be engineers whose whole focus was on "enabling" market disruption, not on enabling gouging rackets in land within an arbitrary boundary.

LikeLike

Good sound analysis, Michael. Fortunately we have a “working experiment” in a country, the USA, where they do have significant differences between land supply regulations from region to region, which enables outcomes under identical demand-side national-level policies to be analysed.

There have been some honest attempts to mathematically model housing market inflation “by city” in the USA and the only way a credible formula can be devised with explanatory power, is to put all the demand-side stuff inside a pair of brackets, and have a kind of binary on/off multiplier outside the brackets based on land supply settings. Mills and Jansen are the authors of one such paper; Heeboll and Anundsen are another.

In countries that do not have the regional variety of regulatory settings on land supply, and economists attempt to put everything into the one formula as factors, including land supply inelasticity, it will be impossible to reach an objective conclusion that will properly inform policy makers.

LikeLike

Joseph Minicozzi, US Urban planner writes,

“Many US cities and towns around the country is hurting financially.

Most of us – city planners, elected officials, business owners, voters, and the like – understand that the city brings in more tax revenue when people shop and eat out more. However, we often overlook the scale of the property tax payoff for encouraging dense mixed-use development.

Many policy decisions seem to create incentives for businesses and property developers to expand just about anywhere, without regard for the types of buildings they are erecting. I argue that the best return on investment for the public coffers comes when smart and sustainable development occurs downtown.

We’ve found that this principle applies: downtown pays. It’s simple math.

Put simply, DENSITY gets far more bang for its buck.

We simply cannot afford how the current system creates incentives for suburban sprawl – which is unsustainable both environmentally”

http://www.planetizen.com/node/53922

LikeLike

Note that the reference to “property tax” is the Rates in our NZ terminology.

LikeLike

Bah. Cargo-cultism. Because there are examples of economically-thriving high density locations, the whole world should be high density and then the whole world would be just as thriving as those examples. Yeah, right.

There is a world of difference between density that EVOLVED along with economic activity that is inseparable from density anyway; and density that has been forced on everyone by regulatory prescription. It is common knowledge among urban economists in the UK, that their productivity gap is due to having an unusually restrictive planning system since 1947, well before other western nations starting adopting such approaches.

Click to access Sub%20001%20Phil%20Hayward%20-%20Submission.pdf

That is not to say that dense and productive locales might not be prevented from evolving, because of restrictions against density. It is absolutely right to minimise and remove such restrictions “just in case”. But it is cargo-cultist, self-destructive lunacy to put a boundary round everything and FORCE density on everyone and everything, to a great extent by way of such inflated land prices that people and businesses cannot afford the space they would choose otherwise. There are unintended consequences from this approach, that make it yet another classic historical lesson about the “fatal conceits” of minds atracted by prescriptive planning.

LikeLike

Alex Anas in “Discovering the Efficiency of Urban Sprawl” (2011):

“…Planners, like urban economists devoted to the monocentric model, have long viewed sprawl as something that should be reduced. Such a bias leads to potentially drastic planning and policy remedies of which the restrictive urban growth boundary is the prime and most costly example. A higher level of sprawl and polycentric land use may indeed be optimal. To the extent that TOD and the New Urbanism are perceived as anti-sprawl tools, they may be wrongly promoted. But these tools of modern planning have an important role to play in serving niche markets. Planners may do better to view them as mechanisms that will promote efficient polycentric land uses…”

And here is an excellent example: Peter Calthorpe himself was involved. It may be “sprawl” but it demonstrates how much is possible with low-cost greenfields land as the start point.

Click to access C037024.pdf

Ironically trying to do New Urbanism in the context of growth boundaries, prescriptive planning, and extractive behaviour by site owners, is riddled with unintended consequences and worse net big-picture outcomes.

LikeLike

Michael, I know you like to keep your blog elevated above the kind of point I am about to make, but….

I have encountered more than one economist who seems to revel in the “authority” that their qualification grants them, to erect fancy theoretical edifices that shift the blame for “market failures” away from regulatory interferences. Some of these economists are Statists, some are bleeding-heart social do-gooders, and some are fundamentalist Greens, often incorporating a touch of the Watermelon about them, and/or a touch of misanthropy. These people seem to me to fill a role similar to that of the “intellectual” clerics who worked on “disproving” radicals like Galileo in their day. It was simply unthinkable to those clerics that Galileo could be right, because it would mean their whole belief system would be discredited and a slippery slope effect started.

Notice how the “debate” with some people never seems to progress beyond “regulatory rationing of land supply does not cause the price inflation” (or not enough to worry about). They can’t bear the thought of the debate even moving on from “yes it does”, to the point where we need to decide “is it worth it anyway”? They don’t want to discuss far more effective fiscal alternatives such as immediate pricing of roads and infrastructure use and resource consumption – it is “land rationing or nothing”. You can understand this if the underlying mind-set regards land per se as sacred, and utilisation of resources for “consumerism” per se, as evil. Or if the underlying mind-set despises people having freedom to choose between a potentially infinite range of options, even if their choices are properly “priced”.

The inherent suspicion of or knee-jerk rejection of “pricing” really indicates that an “economist” is in completely the wrong profession, just as medieval priests in the profession of “astronomy” were in the wrong game.

LikeLike

I’ll stick up for the Catholic church on most things, but yes I think you make a reasonable point. in fairness, we all probably have our blindspots – so much more dangerous precisely because they are hard to spot.

LikeLiked by 1 person

Spread over 129 km, Auckland is not land rationed. It is height rationed. Instead of lots of blah blah blah. Just tell us exactly where you can build the 400,000 houses we will need in the excess land you see available that has not already been identified under the Unitary Plan stalled due to 107 legal objections by the community?

LikeLike

Your endless recycling of this dishonest argument is getting tiresome.

Between your “129 km” end points there is thousands of square kilometers of land that is NOT allowed to be built on. If it WAS allowed to be built on, we would not have an affordability problem. The spread-out towns north and south of Auckland are many kilometers beyond the Auckland urban area “fringe” and almost as far outside the Auckland growth boundary; and therefore it is utterly invalid to use the distance between such towns as some kind of indicator of Auckland’s existing “growth” or even potential “infill growth”. The amount of land inside the growth boundary is a miserable fraction of the comparable “available land ratio” in median-multiple-3 cities. This is the crucial factor.

Ironically if it were not for the growth boundary, many of the people commuting to Auckland from as far away as Thames and Paparoa, would instead live in a home they could afford, most likely somewhere not far beyond where the existing Auckland “fringe” is. The present policy, intended to “keep the city compact”, has the perverse effect that commuting distances are increased on average. Even inside the Auckland built-up area fringe, there is an increasing incidence of forced inefficient commutes because the population is being increasingly “sorted by location” according to “what they can pay”, which swamps normal, logical and efficient location decisions. This is the best explanation why a city like London can be 5 to 10 times denser than comparable US cities and yet have an average commute time 50% longer. In fact in global data, all the “monster commute” cities are the densest ones; and they all have a severe land affordability problem which is the instrumentality for locational inefficiency among the residents and businesses.

Abolishing “height rationing” will NOT create affordability; all the EVIDENCE is that the value of sites are so elastic to allowed density when there is a growth boundary, that the tighter you are allowed to cram people in on the available land, the HIGHER the “economic rent” you are able to “extract” from each person or household. This is why there are so many median-multiple-3 cities with a density of 1500 people per square km, and Hong Kong with 26,000 people per square km has a median multiple of 16+

The argument for increased height and increased density might as well be nothing more than a ploy by the existing Auckland site owning “rentier” class. By the way I am all in favour of market-led intensification in the right places in undistorted urban land markets. Houston is the fastest-intensifying city in the USA and probably the entire first world today, and it achieves this BECAUSE it does NOT have a growth boundary, NOT “in spite of” not having one. The following blog is a goldmine of remedial education on this – and see my comments in the comments threads of both these essays:

https://www.buildzoom.com/blog/cities-expansion-slowing

https://www.buildzoom.com/blog/can-cities-compensate-for-curbing-sprawl-by-growing-denser

LikeLike

Ignorance of facts does not make your copy and paste literature applicable to Auckland. Let’s see some real suggestions from you where you intend these new houses within the 129km stretch that is currently called Auckland would have to be built. So far all you have spewed is endless copy and paste literature.

LikeLike

Houston has 6.2 people million spread 118km from the Woodlands to Texas city compared to Aucklands 129km from Leigh to Pukekohe. The difference is that Houston is a circular city but Auckland is a elongated city. Circular cities have shorter travelling distance with a larger coverage. Auckland is a long city creating longer travelling distances over a much land coverage areas. Auckland has hills and valleys, streams and rivers so when you build roads you also need to.build bridges and you also need tunnels. The longer the distance the more bridges and the more tunnels are required. It is the infrastructure costs that is prohibitive in Auckland. Therefore sprawl is not the answer for Auckland. It is already sprawled over 129km already longer than Houston. In between you have 57 sacred volcanos, the Waitakere ranges, Maori land reserves, the queens chain due to the thousands of rivers and streams. The rest are privately owned lifestyle blocks. You cannot force private owners to risk their homes just to build affordable houses. They do not want to shift and they not want to sell.

LikeLike

The other day I was offered a property 1600sqm for $1.7 million tied up with a Housing NZ purchase guarantee for $850k per house for the 5 house subdivision. The profit margin was $120k per house. I turned the project down as I considered the development risk was too high with that margin offered.

LikeLike

I can use my own eyes. And Google Earth. Readers can make up their own minds who is spewing nonsense here and refusing to engage with evidence (and who has questionable motives). There is literally thousands of square kms of land on which new subdivisions like Mangere could continue to be built.

The isthmus itself is the only place where the city shape is squeezed by geography, to the north and even more so to the south, there is room to grow in all directions. The “twin city” and the “system of cities” is a perfectly valid model. Auckland’s current dysfunction would be alleviated by more satellite cities expanding with cheap land, to the north and the south. There is enough land around Pukekohe alone, for the entire current city of >1 million people, to have been located there had history been different. Local balances of residences and employment is a norm anyway; planners need to stop trying to force concentration in central Auckland.

If there really is “no land” suitable to build new subdivisions on, why is the growth boundary policy being so vigorously defended, often with sham, dishonest and fraudulent arguments? All we need to do is rezone for even more dense development, the growth boundary is redundant because according to you, there is nowhere for suburban growth to go anyway. I think the planners don’t make such a stupid argument themselves – they know full well that land prices could be collapsed if it was made legal to merely convert lifestyle blocks to multiple houses. The space taken up by lifestyle blocks is already bigger than the area inside the growth boundary. Very simply matter to change the zoning. If you can change the zoning inside the growth boundary to have apartment towers built, you can change the zoning outside the growth boundary too.

There would not be so many lifestyle blocks if people had more options between these massive-footprint ones outside the growth boundary, and obscenely expensively priced postage-stamp sections inside the growth boundary. Many people living on 5 acres might have been perfectly happy with a 1/4 acre, but the only option is 1/10 of an acre for >$1,000,000, or lifestyle blocks for about the same price! The lifestyle blocks are priced at the correct, FAIR land price. The price of land for subdivided lifestyle blocks would remain low if the regulatory floodgates were opened. The Auckland planners know this and fear it.

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11138332

LikeLike

Phil, are you not aware that Mangere has sacred caves which Fletcher’s had to abandon 500 house subdivision after spending millions on planning and earthworks? Did you not notice those sacred caves on Google earth? Did you not notice the 57 sacred volcanoes with the thousands of tiny streams and rivers as it streaks across the valleys that have 8 metres exclusion zones along every single stream and river called the Queens chain?

LikeLike

It is rather silly and childish to suggest planners fear anything or that my motives are questionable. Planners plan in accordance to the wishes and well being of the community that pays their wages. Rate payers ultimately decide what needs to be built and where. The Unitary Plan has been stalled by 107 legal objections. Most by the business community and can easily be dealt with but it is the objections from the Grey Lynn suburbs that is stalling the entire Unitary plan as well as the heritage groups eg Wellsford, the fight to keep any housing from encroaching on the natural beauty of its volcano and its surrounding valleys.

I am currently building on Mt Roskill or now called Puketepapa and so far it has taken 3 years for a 3 site subdivision. Cost overrun by 100%. Excavation required approval by Land minister and the Governor General. Earthworks monitoring required by Iwi. Archeological assessments was a requirement. This is a site with existing houses.

LikeLike

Hi Michael

Thanks for the discussion; you definitely raise some good points.

My point in writing that post was to illustrate that there are some components of the rise in house prices that can be related to supply shortfalls in a fairly straightforward way (rising rents being an indication of a contemporaneous supply-demand shortfall), and some that can be correlated to movements in interest rates (although the timing of that story doesn’t line up as neatly as one would hope; treat with caution!).

However, a large share of the rise in house prices can’t be explained so readily, which is why we must draw upon inferences from models and previous empirical studies. This also explains why there’s a lively debate about *why* prices are rising – different people have different models. Personally, I’m sympathetic to arguments about constraints to housing supply being a major long-run driver of price trends. But it’s probably not the only thing going on.

On your point that rents should fall in response to lower interest rates provided that supply isn’t constrained: Are you able to point to any cases where this has occurred to any significant degree? Looking at some data for Atlanta, which you cite, it looks like real rents fell modestly post-GFC, but given the fact that the share of income spent on rent was rising at the same time this might reflect falling incomes (and hence lower demand) rather than falling interest rates.

http://www.deptofnumbers.com/rent/georgia/atlanta/

TL;DR: Multiple working hypotheses.

LikeLike

Interesting question re falling real rents Peter. I don’t know of examples off the top of my head but then I don’t know much about specific city rental market. It would be interesting to have a look at a range of those growing US cities where price to income ratios have been low and fairly stable.

As ever, and as you note, recessions can muddy the water.

LikeLike

Peter: can you see that the evidence shows that there are two fundamentally different types of urban property market based on two different types of “economic rent in land”?

One has the freedom of conversion of non-urban land available in superabundant quantities, to urban use, without any regulatory choke. Land values and rents in these cities are “differentially” derived: the land rent curve follows a classic theoretical model shaped curve, up from the very cheap surrounding land, in smoothly gradual increments reflecting the transport cost savings, and gradually towards the centre, local clustering and amenity-value effects. The house price median multiple in these cities is always around 3 and the trend over time has been for sections and houses to increase in size for the same real price.

The other does not have the freedom of conversion of non-urban land available in superabundant quantities, to urban use. Land values and rents are “extractively” derived just like the prices of most goods and natural resources and land were back when Karl Marx was writing. That is, people are forced to pay the maximum they can stand, in a bidding war against each other, for what they need to exist. There is no such thing as consumer surplus under these conditions. The average household once spent 50% of their income on meagre quantities of food, and the prices of rural land reflected this extractive power. have you read Brendon Harre on housing and the Corn Laws? Please also read my own “The Power and Necessity of Consumer Surplus” (2013).

Trade, transport technology and other technology such as refrigeration, eliminated extractive economic rent in most products and resources. Automobility ultimately eliminated it in urban land. This was common knowledge among not just economists, but interested specialists like architects (Unwin, Wright, Geddes etc), social reformers like Charles Booth, and the car maker Henry Ford. Housing for decades displayed the classic progression of consumer surplus, getting larger and higher quality and better-appointed for the same real price.

Suddenly urban planners curtail the process by which automobility anchors the urban land rent curve in surrounding superabundant low-cost land supply; real house prices skyrocket; urban land prices skyrocket even more dramatically (when house prices have trebled, land values have inflated 20 to 30 fold); people begin crowding and making sacrifices to attempt to remain housed, based on their income and “ability to pay”. No amount of upzoning, redevelopment and crowding mitigate the chronic “extraction” from incomes, of “housing costs”. This is a mirror-image of the opposite trends under automobility in the middle of the 20th century.

Of course the predominant form of housing tenure in pre-automobility markets was and still is in developing countries, renting rather than owning – plus illegal slum housing. Democratized home ownership in the legal market itself is just as much a legacy of automobility as reduced urban land rent is.

Proving this is a slam-dunk. The data is all out there. Some “economists” don’t want to know.

Other big factors like credit and population growth and tax laws, are red herrings. They do not create an extractive-rent urban land market and they do not sabotage a differential-rent effect. Absence of credit in an extractive market, as is the case in many third world countries, will merely result in more renting, on extractive terms; illegal accommodation; and the few successful new “owner” entrants to the formal housing market doing so with cash laboriously accumulated across generations. Bertaud notes that the motor scooter’s ubiquitousness in some developing cities has led to more spacious and better-appointed “motor scooter dependent suburban” illegal slums.

There is no recorded level of population growth that has been sufficiently high to swamp the price-stabilising effect of “freedom to convert land between uses” – certain US cities in the 1950’s, for example, or certain southern US cities in the last 2 decades. If anything, scale economies in housing supply increases in these examples.

A recent report revealed that some developing-nation cities have joined the “median multiple 3 club”, disgracing the regressors in the “first” world. No lack of population growth in these examples either.

http://unassumingeconomist.com/2016/09/global-housing-affordability-what-do-we-know/

As Michael implies, favourable tax treatment for landlords, historically was justified by its benefits to renters, as the supply of rental accommodation was stronger than otherwise. The option of systemically affordable ownership was an inherent part of the same “norms of the time”.

An interruption to the rent-anchoring effect of superabundant potential volumes of land supply, is what changes the way everything else acts and interacts. It is like adding a catalyst to an otherwise inert mix of elements, or like withdrawing the moderating elements in a nuclear reactor core to allow a chain reaction to begin. The world will not comply with theoretical efforts to explain systemic changes in urban land market behaviour some other way, just as the heavenly bodies did not comply with the mantras of the medieval theocrat “astronomers” rebuking Galileo (already having burned Copernicus at the stake for the same “heresy”).

LikeLike

Rents are rising in Auckland but not in the measures offered by median rents stats. The second dwelling concept offered by the Unitary Plan allows 2 separate dwellings at the cost of a firewall, toilet facilities and a separate kichen which equates to 2 rental streams from one dwelling on almost all residential properties in Auckland.

LikeLike

Eg say a 4 bedroom house rents for $700 a week. Convert that to 2 dwellings offered by the Unitary Italy plan, you have 2 two bedroom dwellings renting for $450 a week but the total rent increases to $900 a week but median rent stats fall even though the actual rent rises.

LikeLike

FYI – this is from Peter Nunns. For some reason your site required me to post under an old pseudonymous wordpress account.

LikeLike

ANZ’s net interest income rose $149 million, or 5%, to $3.029 billion

ANZ, Gross lending rose 5% and customer deposits grew 8%.

Nonetheless CEO David Hisco said a challenge for the New Zealand economy at the moment is the slower overall rate of deposit growth than lending growth, noting the banking sector makes up the difference through offshore funding, which is “relatively” more expensive.

“Many New Zealanders see housing, particularly in the current low interest rate environment and in cities like Auckland where there is high demand for accommodation, as the most profitable way to get a return on their money,” Hisco said.

“That’s why ANZ New Zealand supports the Reserve Bank’s tightened restrictions on investor residential lending.”

Clearly the problem with ANZ’s profit drop has got nothing to do with deposits because savings deposits continue to outstrip lending growth but for some strange reason it is being touted by the CEO David Hisco that it is NZ reliance of overseas funding causing the fall in profits when clearly it is not. No wonder the government and the public is confused. The CEO of our largest bank is apparently rather clueless as well or deliberately misleading.

LikeLike

With the Atlanta example – is it possible that within the context of the USA, Atlanta is a bit like Palmerston North? Or New Plymouth.. And if so, what do nominal house prices for those places look like since 2006?

LikeLike

well no, because Atlanta has had pretty rapid population growth (unlike most of those NZ places where real house prices are still below NZ peaks – in some cases even nominals). Current population for the Atlanta MSA about 5.7m, and still increasing at around 1.5% pa

LikeLike