It is a trifle unsettling to check out the Geonet pages, notice the large cluster of continuing aftershocks around “25kms east of Seddon”, and then to realise that looking out my window I can more or less see that spot. It surprises me quite how much damage and disruption Wellington has already had despite being several hundred kilometres from Culverden and the site of Sunday night’s major quake.

US politics and a good book make worthwhile distractions.

I’ve just been reading The Broken Decade: Prosperity, Depression and Recovery in New Zealand 1928-39, by the local historian Malcolm McKinnon. It is, as far as I’m aware, the first substantial scholarly history of the depression years in New Zealand.

The Great Depression was a tough time for many people in many countries, New Zealand not excluded.

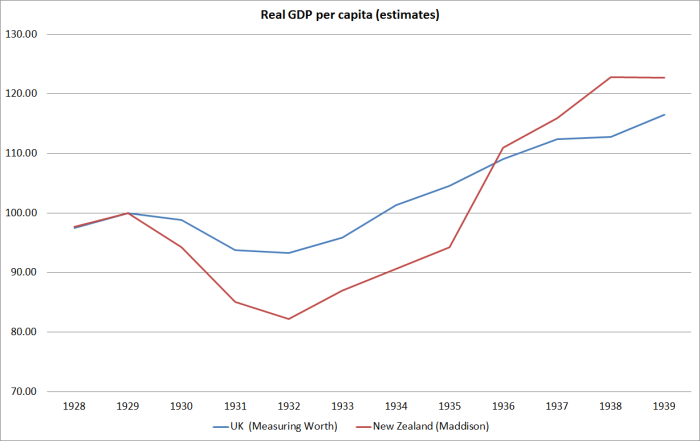

Whereas for the UK, the fall in real per capita GDP wasn’t much larger than the experience in the 2008/09 recession (and the 1930s recovery was faster), in New Zealand real GDP per capita is estimated to have fallen by almost 20 per cent.

No wonder there was a net migration outflow during the Depression – small, by the standards of some we’ve seen since, but then the travel costs back to the UK were much greater than today’s three hour flight to Sydney, Brisbane or Melbourne.

No wonder there was a net migration outflow during the Depression – small, by the standards of some we’ve seen since, but then the travel costs back to the UK were much greater than today’s three hour flight to Sydney, Brisbane or Melbourne.

What made it so tough for New Zealand? We went into the Depression with staggeringly high levels of debt – high government debt (perhaps around 170 per cent of GDP just before the Depression), and a highly negative net international investment position. Most of the external debt was owed by the government (central and local), and most government debt was external. And within New Zealand there was a huge level of farm debt – mostly not owed to banks (which didn’t do that sort of long-term finance) but to government agencies, non-banks, relatives, and to other individual private sector entities. Many farmers bought their farm, and the seller (whether family or other) left mortgage funding in the farm to be paid off over the subsequent decades.

When export prices, and consumer prices, fell very sharply, the debt overhangs became much more pronounced. In respect of the farm debt, wealth was reallocated among New Zealanders (lenders better off, borrowers worse off, at least if debt servicing was maintained). In respect of the public debt, the servicing burden became much more difficult, and a larger proportion of New Zealand’s nominal GDP has to be devoted to servicing that debt. Nominal GDP is estimated to have fallen by a third between 1929 and 1932 – and export receipts fell 40 per cent. The additional servicing burden was particularly severe on the foreign debt which still had to be serviced in sterling, as New Zealand’s own newly-emerging currency gradually depreciated against sterling.

The extent of the fall in activity in some cyclically-sensitive sectors was pretty stark: building permits issued for new houses and flats fell by almost 80 per cent.

But, no doubt as ever, it wasn’t all contraction and decline. Electrical appliances were becoming ever more widely adopted, and with it electricity generation continued to expand right through the Depression years.

Perhaps even more striking was dairy sector production and exports. Sheep numbers in 1935 were almost unchanged from the level in 1929, but the number of dairy cows in milk was 42 per cent higher than in 1929. And here is total dairy production.

I’m not sure I understand quite what was going on in that sector: presumably some combination of new technology, the desperation that came from the high levels of debt hanging over these farmers, and low direct marginal production costs (family labour) made it worthwhile to markedly increase cow numbers and overall milk production despite the low international prices for dairy products.

And substantial as the overall drop in real per capita income was, the fall was spread very unevenly across the population (as is no doubt the case in every recession). Unemployment was high – estimates vary, but even among adult males the unemployment rate probably peaked near 15 per cent (I’d give you 1991 comparisons if only the Statistics New Zealand website were not down in the earthquake aftermath). And there was a lot of resistance to wage cuts during the Depression, but for many of those who kept their jobs – and especially those in salaried jobs, not affected by cuts in overtime hours – real purchasing power actually increased during the Depression. My own grandfathers were in their mid-late 20s when the Depression began – both were in work throughout, and both bought new houses in the early 1930s. As McKinnon highlights, as much through his large selection of photos as from the text, “life went on”: society ladies graced race meetings, the All Blacks still played, and so on.

McKinnon’s book advertises itself as focused on the politics of the period, rather than the economics, and although there is a lot of economic-related material in the book, New Zealand is still lacking its first book-length economic history of the era (although of course it is treated to some extent in the few economic histories of New Zealand). Putting New Zealand’s experience systematically in cross-country comparative perspective (eg New Zealand, Australia, Canada, Ireland – and perhaps Uruguay and Argentina – and, say, the United States and the United Kingdom) would be fascinating.

It is a richly documented book, but with some gaps. For a book avowedly focused on the political side, it was surprising that the author had made use of New Zealand official archives, but not those of the UK – key export market, key source of finance in a stressed period, and of course key international relationship more generally. And even locally, although the book covers the whole period 1928 to 1939, there is very little attention to developments on the right of politics after 1935, including the formation of the National Party.

In terms of policy responses to the Great Depression, my own sense is that the politicians did about the best they could. With hindsight it was clear that a substantial currency deprecation would have been a helpful remedy – perhaps the single most potent response New Zealand could have deployed in the face of a severe global downturn. But in 1929 there still wasn’t a strong sense of New Zealand even having its own currency, let alone it being something that our government could control the value of. As time went on, the option of a more structured devaluation became a centrepiece of the policy debate – advocated by many economists – but even then the dividing lines weren’t clear cut. Export industries generally welcomed the idea, but workers and unions – focused on the expected rise in the cost of imports – didn’t. And for a government with a massive foreign debt, the additional servicing burden from a currency depreciation was a certainty, while the expected increase in tax revenue over time was no more than a hypothesis. When the government finally acted in early 1933 to formally depreciate the exchange rate, it prompted the then Minister of Finance, William Downie Stewart, one of ablest figures then in politics, to resign in protest. For several years afterwards, the devaluation remained a point of political contention (and even scholarly contention – at the time the US academic Kindleberger, later famous, argued that our devaluation had largely just pushed down the international price of dairy products).

Of course, the standard Keynesian line is that countries should have used fiscal policy more aggressively to attempt to maintain demand through the Depression years. Sadly, New Zealand was already debt constrained, and external debt markets were fragile at best. Additional public spending (even if totally domestically financed) might have boosted demand, but it would also have put more pressure on the balance of payments (in a non floating exchange rate world). A few years ago, in Paul Goldsmith’s book on the history of the New Zealand tax system, I stumbled on what should surely be the last word on the possibility of New Zealand borrowing and spending more back then, from Keynes himself.

Visiting London in late 1932 (after the worst of the disruption to the UK external capital markets was over), Minister of Finance Downie Stewart met Keynes. Stewart recorded in his diary:

“I asked him if he would borrow if he was in New Zealand in order to get through the crisis. He said, “Yes, certainly if I were you I would borrow if I could, but if you asked me as a lender I doubt whether I would lend to you.”

By that time, the fall in the price level had taken the level of government debt to well over 200 per cent of GDP.

The servicing burden of high levels of public debt was a major issue in many countries during the Depression. In some cases, it led to direct defaults: Germany, for example, simply ceased paying reparations (and New Zealand, as a small recipient, was a loser from that). The UK, and various other European countries, ended up defaulting on their war debts to the United States (the UK also suspended some of our war debts to them). In other cases – not just involving government to government debt – the approaches were more subtle, but they involved effective defaults nonetheless. In the United States, for example, government bonds had typically been payable in gold. The Roosevelt administration had those clauses revoked, and at much the same time went off gold, effectively depriving holders of a large proportion of their contracted returns.

In New Zealand (and Australia) there was a different approach again. In respect of domestic government bonds, holders were simply forced to accept a lower interest rate on existing debt than they had contracted for – as part of the legislation, if they didn’t accept the exchange, they would face a punitive tax to achieve the same effect. I wrote about that interesting episode in a Reserve Bank Bulletin article a few years ago.

What was interesting, in both countries, was the reluctance to do anything about the foreign debt (much the largest component of both countries’ public debts). The unexpected fall in the price level, and in nominal incomes, had massively increased the burden of the debt. But both countries still needed access to those funding markets, to rollover maturities at very least. Neither country defaulted on central government external debt, focusing instead on the goal (about which they could do nothing much directly) of raising the world price level, so as to lower the effective servicing burden. That finally happened, although in New Zealand’s case market unease about New Zealand’s external debt remained a serious concern – much more so than anything in the last 30 years – right down to the outbreak of the war. Had it not been for the war, external default might well have happened in 1939/40.

This has been a fairly discursive post. There are a lot of other aspect of the Depression in New Zealand I could write about – especially the handling of distressed farm debt – but I’ll save those for another day. For anyone interested in New Zealand’s experience of the Depression, I’d recommend McKinnon’s book. It is a sobering remind of an event that still shapes perceptions, and where – among the now very old – memories are still often seared by the experience. Never again, people hoped for decades. And then there was 21st century Greece.