Perhaps not surprisingly there has been a lot of coverage of yesterday’s CPI outcome – an inflation rate of only 0.1 per cent for the year; materially lower than either the Reserve Bank (in its December MPS) and all other published forecasters had expected.

Quite what the numbers mean isn’t so clear-cut, and I’ll come back to that, but it is very low inflation.

Of course, this is an era of low inflation. According to the OECD database, nine OECD countries had even lower inflation (or deflation) than we did last year – eight of those countries have policy interest rates at zero (or even a bit below).

The media made much of our inflation rate being the lowest since 1999, but they probably missed the story. After all, 1999 isn’t that long ago (and the target was lower then). And in those days, the CPI included retail interest rates, and interest rates dropped by around 400 basis points in 1998. All the experts thought that in a deregulated economy including interest rates in the CPI was daft – apart from anything else, it meant that when the Reserve Bank tightened monetary policy, inflation temporarily went up. So daft in fact that the Policy Targets Agreement in place at the time, signed by Winston Peters and Don Brash, set the target in terms of CPIX (ie the CPI excluding credit services). In fact, the way the official CPI was calculated was changed shortly afterwards to essentially the approach used today.

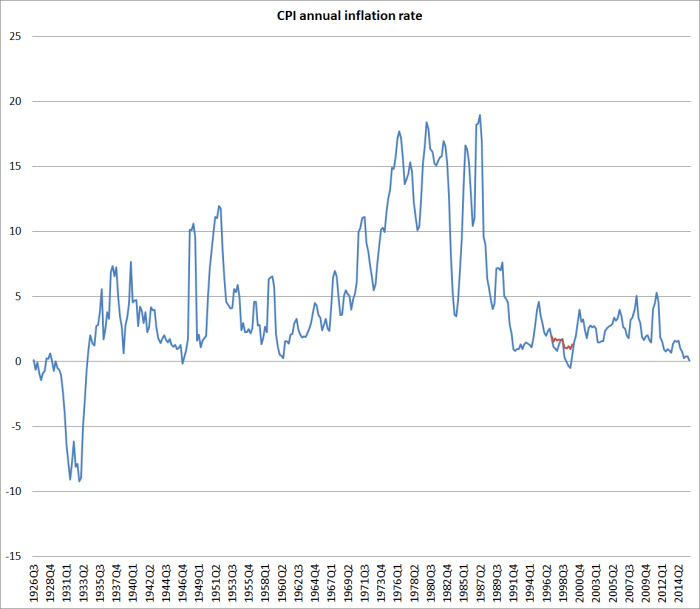

We don’t have a consistently compiled historical CPI in New Zealand (the way all sorts of things have been measured, but especially around housing, has changed materially over time, but then so – for example – has the extent of price controls, regulation etc). But here is a chart using the official historical CPI all the way back to the 1920s, with an overlay (in red) of the CPIX inflation rate over 1997 to 1999. At the trough, annual CPIX inflation was around 0.9 per cent – not that much below the midpoint (1.5 per cent) of the then target range.

Taking a longer horizon, annual CPI inflation got as low as 0.3 per cent in 1960 (I recall tracking this number down in the early days of inflation targeting and holding it out as something to aspire to, the last time New Zealand had managed ‘price stability’). And since the Reserve Bank opened in 1934, the only time annual inflation has really been lower than it was in 2015 was in 1946, when the annual inflation rate briefly dipped to -0.2 per cent. The lowest inflation rate for almost 70 years might have been more of a story. “Lowest inflation since the Great Depression” would no doubt be a headline the Reserve Bank will be keen to avoid, but that too must be a non-trivial risk now.

Quite what to make of the inflation numbers is another matter. Although the Reserve Bank has been playing up headline inflation in its recent statements, headline inflation shouldn’t be (and rarely is) the focus of monetary policy. What matters more is the medium-term trend in inflation: as the PTA puts it

“the policy target shall be to keep future CPI inflation outcomes between 1 per cent and 3 per cent on average over the medium term, with a focus on keeping future average inflation near the 2 per cent target midpoint”

But it has been four years now since headline inflation was 2 per cent. The Reserve Bank keeps telling us it is heading back there relatively soon, and has continued to be wrong. Even before this latest surprise, they had been forecasting it would be another two years until inflation got back to 2 per cent.

If the weak inflation was all about petrol prices perhaps we could be relaxed – whatever mix of supply and demand factors is lowering oil prices, taken in isolation it is a windfall real income gain to New Zealand consumers. But CPI inflation excluding vehicle fuels was 0.5 per cent last year, down from 1.1 per cent in 2014. Indeed, tradables inflation excluding vehicle fuels was -1.2 per cent in 2015, also a bit lower than the 0.9 per cent in 2014.

Over the last few years, a common explanation for New Zealand’s low inflation rate had been the rising exchange rate, which tends to lower tradables prices. But the exchange rate peaked in July 2014, and in the December quarter 2015 (having already rebounded a little) it was 7 per cent lower than it had been in the December quarter of 2014. Of course, some Reserve Bank research not long ago suggests that when the exchange rate has fallen previously the inflation rate itself has tended to fall – presumably because the exchange rate falls don’t occur in a vacuum and are often associated with a weakening terms of trade and a weakening economy.

Government taxes and charges throw around the headline CPI – for the last few years, large tobacco tax increases held headline inflation up, and more recently the cut in vehicle registration fees lowered the headline rate. But in the last year, non-tradables inflation excluding government charges and tobacco and alcohol taxes was 1.8 per cent, exactly the same as overall non-tradables inflation. Non-tradables prices tend to rise faster than tradables prices (think of labour intensive services) so with an inflation target on 2 per cent, one might normally be looking for a non-tradables inflation rate of perhaps 2.5 to 3 per cent.

What of the “core” measures of inflation? Probably for good reason, the “ex food and energy” measures don’t get much focus in New Zealand. But SNZ do report such a measure, and it recorded 0.9 per cent inflation last year, right at the bottom of the target range although barely changed from the 1.0 per cent in 2014.

The Reserve Bank reports four core inflation measures on its website. None of them is close to 2 per cent, but the message from them in terms of recent trends isn’t that clear. Two measures (the weighted median and the factor model) suggest little change in the core inflation rate over the last year. One of them – the trimmed mean – suggests a material slowing in core inflation (indeed, in quarterly terms the trimmed mean – which excludes the largest price changes in both directions – had its weakest quarter in 15 years of data). But the fourth measure – the sectoral core factor model – actually suggests that core inflation has picked up quite noticeably over the last few quarters. It is a pretty smooth series, and so an increase in inflation from 1.3 per cent to 1.6 per cent, especially when headline inflation is so weak, is worth paying attention to.

The sectoral core measure has been the Reserve Bank’s preferred measure of core inflation, and mine. Frankly, I’m not sure what to make of it, although I take some comfort from the fact that the increase seems concentrated in tradables prices (the sectoral factor model separately identifies common factors among tradables and non-tradables prices and only then combines the two factors). The tradables factor seems quite sensitive to exchange rate movements – as one might expect – but is not obviously something monetary policy should be responding to. It is always important to think hard about data that go against one’s story, so I remain a bit uneasy about what the sectoral core measure is telling us (even recognizing that it has end-point problems, that mean recent estimates are sometimes subject to quite material revisions).

For the last nine months I’ve been arguing here (and had earlier been arguing the case internally) that monetary policy needs to be looser if future inflation is once again to fluctuate around 2 per cent – the target the Governor and the Minister have agreed. Somewhat belatedly, and grudgingly the Reserve Bank has cut the OCR, and it will take some time for the full lagged effects of those cuts to be seen. Current core inflation – whatever it is – partly reflects the lagged effects of previous overly-tight policy.

In terms of future monetary policy, yesterday’s CPI results in isolation aren’t (or shouldn’t be) decisive. They rarely are. But equally there isn’t much reason in those data for anyone to be confident that inflation will relatively soon be fluctuating around 2 per cent. That confidence matters – as I noted earlier in the week, both financial markets and firms and households have been gradually lowering their expectations of future inflation . If that becomes entrenched, it is harder to get inflation back up – but the risks of trying more aggressively to do so are also diminished (people today simply aren’t looking for inflation under every stone, worried that some nasty inflation dynamic is just about to destroy everything they’ve worked for).

And context matters too. As I explained in December, I thought the Reserve Bank’s case that the economy and inflation would rebound over the next couple of years – and hence no more OCR cuts were needed – was unconvincing. The intervening six weeks have done nothing to allay those concerns. Over recent years there were some huge forces pushing up domestic demand – strong terms of trade, the upswing in the Christchurch repair process, and the huge increase in net migration. None of those factors seemed likely to be repeated. Dairy prices seem to be lingering low, global economic uncertainty is rising, global growth projections are being revised downwards (even by that lagging indicator, the IMF) and just today US Treasury bond yields dropped back below 2 per cent. Unease seems to be turning to fear, in a global climate where deflationary risks seem more real than those of any very substantial positive inflation.

In sum, the case for further OCR cuts in New Zealand now is pretty clear, and the risks (of materially or for long overshooting the inflation target) seem low. Would doing so boost the property market? Relative to some counterfactual, no doubt. That is a feature not a bug. Monetary policy works in part by increasing the value of long-lived assets, and encouraging people to produce more of them. But what it would also do is lower the exchange rate, providing a buffer to more-embattled tradables sector producers (think dairy farmers) and increasing the expected returns to new investment in other areas of the tradables sector.

Who knows what the Governor and his advisers will make of the recent data flow. In a more transparent central bank we could look forward to seeing the minutes of next week’s meetings, the alternative perspectives and arguments. As it is, the Governor will tell us what he wants us to know in his OCR release next week, and perhaps in his speech the following week.

Looking back, seems to me the introduction of inflation targeting coincided with a wider policy trend toward product, labour, and financial market liberalisation (obviously, without discarding all aspects of political influence). Given this, the CPI index is really nothing other than the aggregated outcome of firm level pricing decisions which are presumably made within relatively flexible/competitive end markets. Further, over time, goods/services tend to become commodity in nature (e.g. mobile phones; pay TV) with price becoming a more important element of customer acquisition / retention. If the forgoing is roughly right, why wouldn’t prices tend to fall in the ‘long run’ or over a horizon greater than that identified by most inflation targeting central banks? And this is even before thinking about the emergence of China/global supply chains, demographics, the use of technology to improve information dissemination etc during the past few decades.

Perhaps the inflation targeting framework requires tweaking or an overhaul? At least to my mind, the crisis and subsequent developments suggest central bankers are currently better placed to contribute to real economic outcomes via a focus mainly on financial rather than price stability. No doubt this is heresy to those who maintain faith in a central bank’s ability to control the general domestic price level but then again, it took a while for the gold standard to be banished to the pages of history…

LikeLike