The Dominion-Post reports this morning on a speech given yesterday by the Secretary to the Treasury, Gabs Makhlouf. I might come back to the speech when I’m finally free of institutional constraints but, for now, it was his comments on migration that caught my eye. An extract:

For New Zealand, many of the benefits from high net migration levels are similar to those that come from offshore investment.

Migration helps to lift our productive capacity – it enables the economy to grow faster by increasing the size of the workforce, in much the same way that foreign capital allows us to grow faster than domestic savings alone would permit.

Right now, at a time when international demand for some commodity products is weak, strong net migration also has the benefit of bolstering demand for goods and services at home.

Like foreign investment, migrants also bring new skills, new ideas and a diversity of perspectives and experiences that help to make our businesses more innovative and productive.

And perhaps most importantly, migrants often retain strong personal and cultural connections to other parts of the world, which opens up, and helps us to pursue, new business opportunities. We are in a pretty incredible position in this regard, with so many New Zealanders – around 1 million people – living overseas, and so many people who live here having been born in another country.

Contra Makhlouf, my proposition, which I will elaborate on over coming months, is that inward migration of non-citizens is rarely, if ever, even part of the answer (whether proximate or more fundamental) to underlying economic problems. In relatively developed countries, per capita incomes of native populations have very rarely been lifted by immigration. One way to see that is to look at incomes between pairs of advanced countries over very long periods: over say the last 100 years countries which have received lots of immigrants have not typically done better than those which did not.

And when non-citizen immigration has boosted native incomes it is usually because the immigrant culture takes over and swamps what was there before (one could think of European migration to New Zealand, Australia, Canada, and the United States in this light relative to the pre-existing indigenous cultures). Cultures embed a lot of the keys to economic success. When it works well, large scale inward migration of non-citizens [I labour the description to be clear that I’m not talking about the comings and goings of New Zealanders] is a complement to economic success that was already well underway, not a contributory cause. Be it late 19th century New Zealand or the United States, Singapore or Dubai today, or 20th century Ireland (where people rationally left during the dark economic years, and large inflows occurred only after rapid sustained growth in GDP and productivity was already well-established) the longer-term economic benefits are almost all to the migrants,

Immigration allows the benefits of a country’s economic success to be shared more widely. It might be a path to success and prosperity for the migrant (if they didn’t expect that they would not migrate) but shouldn’t be seen as a path to lifting the innovation and productivity of New Zealand people and firms. In Australia, as orthodox a body as the Productivity Commission reached pretty much that conclusion almost a decade ago.

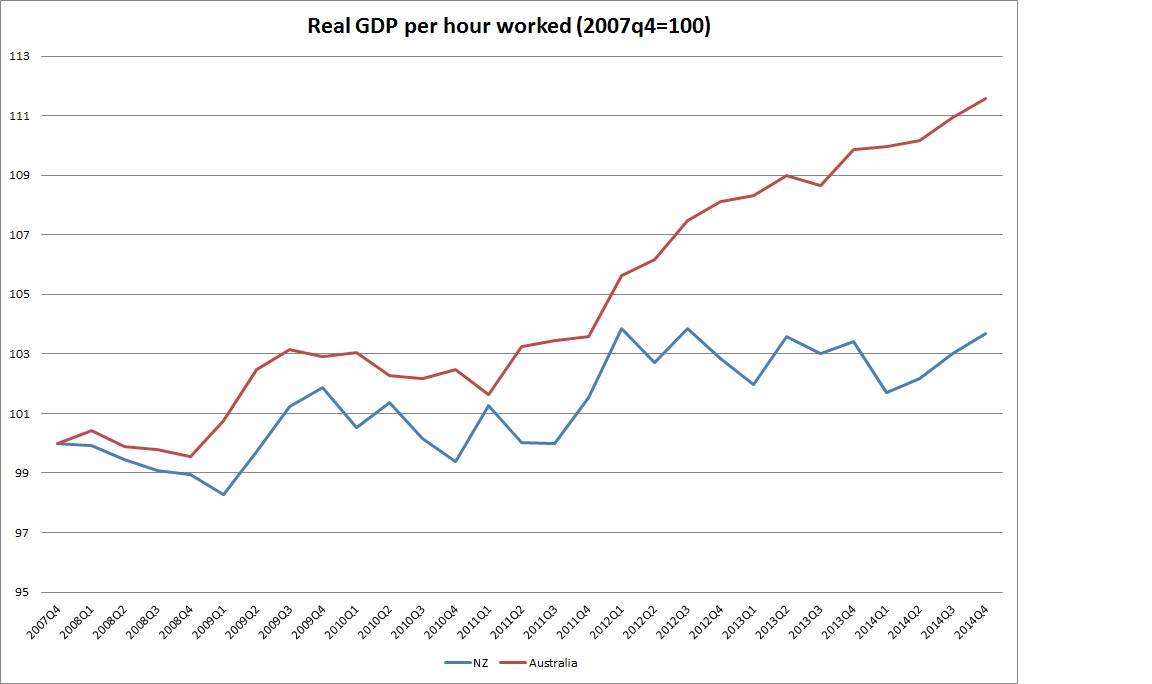

New Zealand is not an economic success story, and has not been so at least since World War Two. Finding a path that begins sustainably closing the income and productivity gaps to the rest of the advanced world, should come before governments carry on bringing in yet more people, even as our own people are choosing to leave.

{kind=link}

{kind=link}