The Reserve Bank of New Zealand’s Board published its Annual Report last week. It didn’t attract any coverage, but then it was hard to find – buried inside the Bank’s own large glossy (expensive?) report, and with no accompanying press release (not even a mention in the Governor’s own press release). And it didn’t say much anyway.

The Board isn’t part of the decision-making structure of the Reserve Bank. Unlike a typical corporate or Crown entity, all the powers Parliament has given to the Bank rest with the Governor personally. The Board are agents for the public and the Minister in holding the Governor to account, and so need to be – and to be seen to be – at arms-length from management. I’ve criticized the Board previously for not publishing its report separately, and not even insisting that it is separately visible on the Bank’s website. The Board must have noticed that criticism because in this year’s report they claim that they are “specifically tasked…with publishing its annual assessment within the Bank’s Annual Report”. Unfortunately, even on this small detail they are wrong. The Reserve Bank Act allows the Board’s Annual Report to be published with the Bank’s report if the Board agrees, but it certainly does not require the Board to agree or mandate the way the Board report is buried inside the Bank’s report. It is a small detail, but perhaps one again suggestive of a Board that too often sees itself as part of the Bank, working hand-in-glove with management, rather than as a fairly independent entity, charged with challenge and review of the Governor’s stewardship. As I’ve noted previously, the practice until now of having a former staff member chair the Board seems to have been a part of that identification with management.

It is a hard job for the Board to do well. Typically Board members aren’t experts in the areas the Bank is responsible for. And they don’t spend much time on the issues either – they aren’t paid that much, and the current and former chairs have both had demanding fulltime chief executive positions of their own. The Board has no resources: there is no independent budget, no staff. And not only is the Governor himself still a member of the Board, but the Board secretary is a member of the Bank’s senior management group. The Board can ask for (but not compel) papers to be provided, but the Governor has total control over what they get back, even though it is the Governor’s performance they are charged with monitoring and evaluating.

So it is a deeply flawed model. In no other area of public life I can think of has a review body been set up that is so close to, and so dependent on, the entity/person it is charged with reviewing. Like so much of the rest of the Reserve Bank governance model, the role and structure of the Board is overdue for reform – the more so as the Reserve Bank has chosen to exercise more and more discretionary powers.

Cynics might think that problems were deliberately built into the legislation, and that there was never any intention of the Board playing a serious role in holding the Governor to account. The cynics are wrong. As I’ve explained previously, the original conception of the Reserve Bank’s role was a fairly mechanical one, and even the first Governor thought of accountability as pretty mechanical – if (core) inflation was outside the target range he would lose his job. So there were genuine good intentions when the Act was written in 1989, and when it was amended in 2003, to require the Board to publish an Annual Report. But good intentions haven’t produced good results. Poor structures make serious review and accountability more difficult than it should be, but the individuals successive Ministers have appointed to the Board haven’t done much about doing the best with the flawed structure they operate within. That is something those individuals – all no doubt capable and competent people in their own fields – need to take responsibility for.

This year’s Board Annual Report spans eight pages of text. That might sound moderately promising, except that almost all of the text is descriptive material: lengthy lists of meetings held, topics discussed, and so on. If you went to the Report looking to get a sense of the Board’s views – as might befit a body established by Parliament, paid with public money – it would be pretty thin pickings. As far as I could see, the only judgements were as follows:

- “the Board’s overall assessment is that the Bank continues to perform its functions to a high standard….and contributes to New Zealand’s stability and prosperity”, which is interesting, but comes out of the blue with no supporting analysis or evidence.

- “on the basis of the information and advice available to the Governor at the time of his decisions, the Board assessed that the four MPSs and the intervening OCR reviews met the requirements laid out in section 15 of the Reserve Bank Act”. These are quite formal technical judgements, made at the time of each OCR decision, not ex post reviews of the conduct of policy, (and, in terms of attention to detail, section 15 of the Act deals only with MPSs, not with other monetary policy adjustments or OCR reviews).

- “the Board agreed that the November 2015 and May 2016 Financial Stability Reports met the requirements contained in section 165A(2)(a) and (b) of the Reserve Bank Act.

- “the Board reviewed the Bank’s health and safety policies in the context of the new legislation and advised that these should be reviewed annually and be externally audited”, and

- “the Board….endorsed the decision taken by the Governor to cease pre-announcement media lock-ups”. I presume we shouldn’t interpret this as meaning that they disagreed with canning the pre-release analyst lock-ups.

Which is all very well, but in none of these occasions does the Board offer any basis for their judgements. There is no sign in the text that they had thought about any alternative models, engaged with any alternative perspectives, or anything of the sort. To the extent there is any analytical discussion at all in the Board’s Report (and it is brief), it could have been lifted straight from the Governor’s own report. If the Board genuinely believes that the Governor has been doing a good job, even with the benefit of hindsight, that is certainly an option open to them, but surely they owe us – the stakeholders – rather more evidence of having engaged with the issues and alternative perspectives than is on display again in this report? If there is one thing everyone recognizes about things like monetary policy, it is that reasonable people can interpret the same material differently, even given a pre-specified target like the PTA. But there is no sign of that at all in this report. And is the Governor really so perfect that the Board could find nothing in the entire year about which it was willing to express concern? I suppose it is possible, but I’m sure even the Governor would recognize that he is – like all of us – a flawed human being, rather than some plaster saint.

There are other areas for concern. I highlighted last year my concern at how the Board seemed to see its role as “having the Governor’s back”.

Too often, the Reserve Bank’s Board seems to see a significant part of its role as being to help the Governor spread his story and to explain the choices the Governor is making.

And this year the Board uses exactly the same words it used last year to describe the functions they host for locals “elites” on the evenings of Board meetings

This outreach is a longstanding practice of the Board to ensure visibility of its role among the wider community, and to facilitate directors’ understanding of local economic developments, and the wider public’s understanding of the Bank’s policies.

As I noted then

Worthy activities for management, but that isn’t the role Parliament envisaged for the Board – whose purpose is to hold management to account, not help management explain their choices to (select elements of) the public.

The public needs awkward questions, not sympathy. The Board isn’t there to be a part of the Governor’s PR programme, but as part of citizens’ protection in respect of perhaps the most powerful unelected individual in New Zealand. But there is just no sign that the current Board members get the distinction, or are interested – or perhaps capable – of playing such a role.

There is also the constant risk of the Board getting too involved with management to be able to credibly hold the Governor to account. I was interested in this extract from the Report

With the Governors present, the Board met three of the chairs and a deputy chair of the four major banks for discussions on two key issues: the governance of New Zealand subsidiaries of the large Australian banks; and regulatory issues that are currently front-of-mind for New Zealand bank boards. The banks discussed risks in the dairy and housing sectors and the impact of LVR limits on balance sheet risks. The banks also discussed the review of the Bank’s outsourcing policy and risks associated with possible cyber threats.

Sounds like an interesting series of meetings, but what role of the Board was being pursued here? The Reserve Bank Board has no role in such areas of policy, and if its concern was about being able to hold the Governor to account, if the commercial bank boards were ever going to speak freely, they weren’t likely to do so with the Governor in the room. Individually, such meetings probably do little harm, but they just reinforce a sense of a Board which serves the Governor’s interests more than it serves the interests of the people of New Zealand, or (more specifically) the sort of role Parliament set out for them.

The one key power the Reserve Bank Board has is to recommend the appointment of the Governor. The Board – not one of them elected, very few of them widely known, none with any accountability themselves – control the appointment, since the Minister cannot appoint as Governor someone the Board has not recommended. It is now less than a year until the current Governor’s term expires, and yet there is nothing in the Annual Report from the Board on how it thinks about the exercise of that appointment powers; no sense of what makes a good Governor in such a powerful public role, and no discussion at all of (for example) the Bank’s succession planning. Successful organizations typically promote from within, but 1982 was the last time a Reserve Bank Governor was appointed from within – contrast that with the Reserve Bank of Australia. But you would have no sense from this report that the Board was even paying attention to such issues, or grappling with why the Bank appears to have had such a poor record of developing potential Governors.

As I said, with such limited resources and such dependence on Bank management, the Board members face quite a challenge to do the sort of job Parliament asks of them, and which citizens should expect. There are plenty of much better resourced review agencies around the New Zealand public sector, and when a government finally gets round to reforming the Reserve Bank Act they should look hard at such models, but there is a lot more the current Board could do, and be seen to be doing. Under the chairmanship of Arthur Grimes and Rod Carr, there was a strong predisposition to support the Governor and the institution’s decisions. That needs to change. The Board works for citizens – and the Minister of Finance – not for the Governor.

The Board has recently chosen a new Chair, an outsider for the first time rather than a former insider. The challenge for Neil Quigley will be to try to lift the performance of the Board, and reorient it in the direction Parliament clearly intended (including when it required publication of a Board Annual Report). It won’t be easy, and some of the Board members might not be keen – keeping cosy with the Governor is much easier – but if they believe the current governance model is the appropriate one, and one that can work well, they owe to us, and to themselves, to show it can work much better, and offer much more scrutiny and challenge, than on the evidence before us it has been doing in recent years. Apart from anything else, support and endorsement is usually that much more persuasive if there is demonstrable evidence that those who end up offering the support have posed hard questions, brought alternative perspective to bear, and come away convinced. Unreflective echoing of the perspectives of the decisionmaker convinces few people anywhere. If anything, it just leaves questions about the quality of institutional governance in the New Zealand public sector.

As individuals Reserve Bank Board members typically look better than that. But they need to demonstrate that they have what it takes in this demanding role.

(Three months ago, I outlined what I thought the Board should have covered in this year’s report. To no one’s surprise, there is little or no overlap with the actual report.)

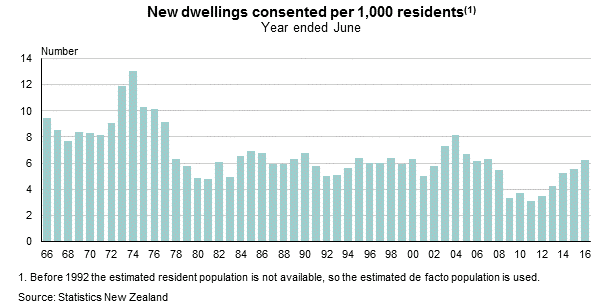

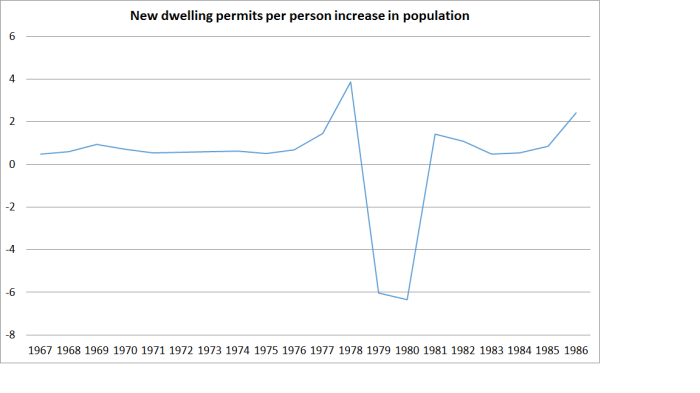

What happened? Well, in the late 1970s the large scale outflow of New Zealanders got underway, and the number of non-citizen immigrants had also been scaled right back. In the years to June 1979 and June 1980, the population is actually estimated to have fallen slightly, and yet 18000 and 15000 new dwelling consents were granted in each of those two years. For the three June years from 1978 to 1980 there was no population growth at all, and yet there were more than 50000 new dwellings consented. No wonder that over the late 1970s and through to around early 1981, New Zealand experienced the largest fall in real house prices (around 40 per cent) in modern history.

What happened? Well, in the late 1970s the large scale outflow of New Zealanders got underway, and the number of non-citizen immigrants had also been scaled right back. In the years to June 1979 and June 1980, the population is actually estimated to have fallen slightly, and yet 18000 and 15000 new dwelling consents were granted in each of those two years. For the three June years from 1978 to 1980 there was no population growth at all, and yet there were more than 50000 new dwellings consented. No wonder that over the late 1970s and through to around early 1981, New Zealand experienced the largest fall in real house prices (around 40 per cent) in modern history.