Late yesterday afternoon someone sent me the link to this

Almost two months into the Reserve Bank’s financial year it authorises a 41.7 per cent increase in spending for the current financial year and a 26.3 per cent increase the following year, both relative to the amounts approved in the current five-year Funding Agreement signed in June 2020.

The variation had, apparently, been slipped onto the Reserve Bank’s website the previous day (22nd).

I’m signed up to the Bank’s email notifications. These were the ones from the last week

There was no press release from the Bank, and none from the Minister of Finance either. For huge increases in the spending of an institution whose performance has been under a great deal of scrutiny in the last year or two, the institution actually charged with keeping domestic demand in check to keep inflation at/near target.

The Funding Agreement model, which governs how much of its income the Bank can spend, itself is very unusual. I wrote about it, and the background to it, in a post a few years ago, before Orr took office, when the Reserve Bank Act review was being kicked off. The Funding Agreement model was better than what had gone before – not hard, since previously there were no formal constraints at all on Reserve Bank spending – but not very good at all. The model was set up when the Bank was (overwhelmingly) conceived of as a monetary policy agency, with a few other peripheral functions. The five-year horizon, with nominal allocations fixed in advance, was seen as having the (modest) advantage of providing a bit of financial incentive for the Bank to meet its inflation target: if it didn’t its real spending constraint would be tighter than otherwise. These days, the bulk of the Bank’s staff are devoted to policy and regulatory functions. Most such government agencies are funded by annual appropriations, approved (and scrutinised) by Parliament through the annual Budget process. In that earlier post, I’d come round to thinking that model should be applied to the Reserve Bank too.

The variation slipped onto the website a couple of days ago exemplifies what is wrong with the current system (perhaps especially under the current players – Orr/Quigley and Robertson – but they are only egregious abusers of a poor system).

This is public spending on public functions. We have a Budget for that. There is no obvious reason why, if there really was a compelling case for more money for the Reserve Bank, it could not have been announced at the same time as the Budget. After all, governments have to prioritise, and voters have to make judgements about what they do and don’t choose to spend money on. Taxpayers are the poorer whether or not the spending is through some agency subject to parliamentary appropriation or the Reserve Bank. As it is, the Bank’s financial year began on 1 July, so why the delay in agreeing/announcing this big increase in approved spending?

But then note the specific timing. The Minister of Finance signed the variation on 31 July. Orr and Quigley only signed it, and then had it slipped onto the website, on 22 August. It doesn’t take more than five minutes to get a document across the road to the Reserve Bank, and even if they wanted Quigley’s signature on it (it just needs any two Board members), and they wanted a physical rather than electronic signature, a return courier to Hamilton could no doubt have been done in 24 hours. Most probably, they didn’t want the variation to be known any earlier because……last week was the Monetary Policy Statement, when the Bank was having to acknowledge it hadn’t yet made much progress in getting core inflation down and that interest rates might be higher for longer, when the Bank would face a press conference and an FEC hearing, and when they’d do the quarterly round of making some internal MPC members available for interviews. It came on the back of those stories a couple of weeks ago [UPDATE: the week MoF signed the variation] about the Minister and the Public Service Commissioner having meetings with government department chief executives urging upon them fiscal restraint. The last of those Bank media interviews appeared a couple of days ago. It was bureaucratic gamesmanship, presumably abetted/approved by the Minister, to minimise budgetary scrutiny and accountability on what is a huge increase in allowed spending.

By law, they had to publish the Funding Agreement variation on the Bank website as soon as possible after it was signed. They did that, even if you had to be eagle-eyed or lucky to spot it. The Minister must present a copy to Parliament within 12 sitting days. Had the agreement been signed on 31 July (when Robertson signed it, but not the others) that would have been this month. As it is, perhaps he’ll do it in the next few days, but it could be November/December, after the election.

Under the old Reserve Bank Act, Funding Agreements were subject to parliamentary ratification. In a way, it was a bit of a charade, as there were no consequences if it was voted down (it isn’t mandatory for there even to be a Funding Agreement) but it did establish a principle, and did allow a parliamentary debate and a spotlight on proposed Bank spending). In one of the very worst parts of the Reserve Bank Act reforms – that genuinely took things backwards, rather than just made botched or inadequate improvements – the government removed the provision from the Act requiring parliamentary ratification, and thus the platform for parliamentary debate (about a level of spending which in absolute terms is no longer small).

We also, at this point, have no real idea what the Minister has approved this spending increase, in straitened times, for, or why he approved it. There is, of course, no ministerial press statement, and there is no hint of a huge spending increase in the Minister’s latest letter of expectation (although this must have been underway for months, and I had a clearly well-informed email months ago encouraging me to ask questions and lodge OIAs then, which I didn’t get round to doing).

All we have at present is this

which is clearly designed to emphasise the new functions, but there is just no way they can be costing any significant part of the extra $48m. And in any case, we simply can’t take as trustworthy anything Orr and Quigley say any longer, abetted by Robertson, without explicit verification.

(One problem with the Funding Agreement model is that it includes capex so we don’t even know yet the split between ongoing operational spending and capex items).

There should, eventually, be some transparency. One positive aspects of the recent legislative reforms was a requirement that the Bank must publish a budget (previously I had pointed out the Bank’s funding was an untransparent as that of the SIS)

By law, the variation to the Funding Agreement slipped onto the website on Tuesday had to accompanied by an updated budget. But, so far, there is no sign of one. There are budget numbers in the 2023/24 Statement of Performance Expectations released a while ago, but they bear no relationship to the numbers in this variation (and there is no substantive mention of the Funding Agreement, or any variations to it, in that document). I’ve searched their website and can find nothing else.

We have no details, Parliament has no say, and the Minister and Governor and Board chair arranged to ensure the really big increase in funding was (a) kept just as low profile as possible, and (b) wasn’t disclosed at all until the quarterly round of scrutiny for the Bank had conveniently passed.

It is a travesty on multiple counts. The system is bad enough – spending should be occurring only with parliamentary approval, but the law doesn’t require that – and the application seems, if anything, to have been worse.

Since I assume that they will, after their fashion, eventually obey the law no doubt a “budget” will eventually appear. Even then it is unlikely to be very revealing, although might give a hint of a sense of the breakdown between bloat and actual increased statutory responsibilities. I’ve lodged Official Information Act requests with the Bank, The Treasury, and the Minister of Finance to understand better just what is going on, including how much (if any) pressure there was on the Bank to cut back on non-priority spending. One day, in a month or two, we should have some answers to that.

UPDATE (Friday)

This appeared in the comments last night

If I’m looking at the right page this detail now appears to have been removed. It was interesting that Quigley’s signature was affixed electronically, so that (of course) the long delay was not a matter of waiting for him to come to Wellington. Re the final point, there may well have been a Board meeting recently, but since the variation document itself reflected an agreement between the Bank and the Minister it would be (very) surprising indeed if the Board had not already approved the variation before MoF signed it on 31 July.

Reading the hardcopy Herald over lunch I spotted an article under the heading “Ministry boss apologises over spend-up”, referring to Mr Leauanae, the chief executive of the Ministry of Culture and Heritage (MCH) as regards the events surrounding his farewell from his previous role as head of the Ministry of Pacific Peoples (MPP) and his welcome to MCH. This was the key bit

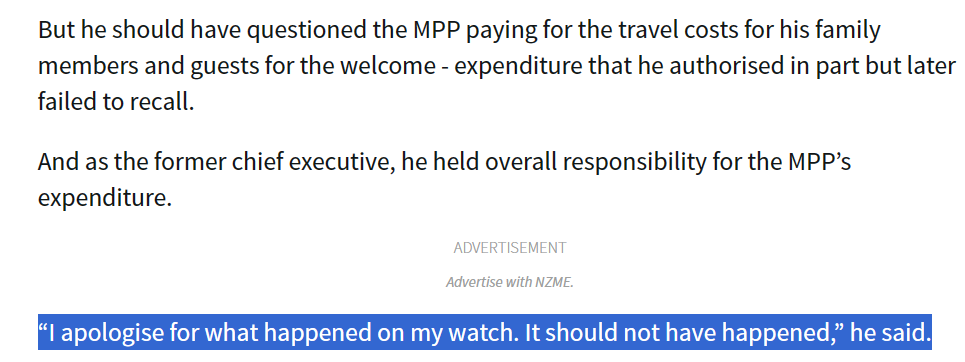

“on my watch”? He seemed to be trying to minimise what PSC had found had actually happened (written up in my post yesterday) and suggest that he himself hadn’t done much, but had after all just been the CE (so, in some sense, formally responsible but not really to blame). It was as if his wayward former underlings had done stuff that didn’t relate to him at all. What the PSC report actually described was Leauanae having accepted $7500 of taxpayer gifts himself at the farewell and then accepting $4000+ of travel for family members and friends for his welcome to MPP. (In addition of course to the rest of the extravagant $40000 spent in total on his farewell, as he moved from one small Wellington government department to another.)

As I noted on Twitter, one of the things the PSC report carefully never directly stated was quite when (a) the gifts were returned, and b) when the travel was reimbursed. It would have been easy for either the PSC report or Mr Leauanae to have given us specific dates, but they (obviously deliberately) chose not to. I have now lodged a couple of OIA requests to find out. Was it the day after the relevant events (say) or only after PSC started digging into the matter? The difference is likely to be quite important. If the former, one might take a more charitable view.

But the comments reported in the Herald prompted me to read the statement from Peter Hughes again more carefully. The lines Hughes will have been keen to see reported were

I thank Mr Leauanae for putting the matter right at the first opportunity.”

The “first opportunity” might suggest the day of the events or perhaps the day after. After all, as the full PSC reports note (carefully, without either evidence or further comment)

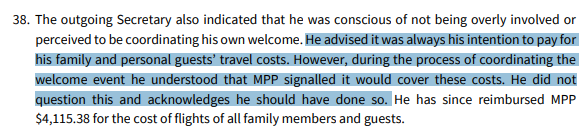

He advised it was always his intention to pay for his family and personal guests’ travel costs.

So on a casual reading you might have assumed it was all an oversight and was put right within a day or two.

But, from the Commissioner’s own statement, that can’t have been the case.

Perhaps the gifts really were returned very promptly (eg the night of the farewell function or at worst the day after), although the report/statement carefully does not give dates or times. (There is also that strange comment that he returned both the gifts and the money spent on them, which leaves questions as to whether the gifts had been able to be returned to the vendors for full refunds or not).

But that clearly wasn’t the case with the travel, because the second paragraph above says that it was the PSC review which uncovered the fact of this spending on Mr Leauanae’s family and friend’s travel, and that it was only in light of the review finding that he reimbursed MPP. And we know from the documents PSC released that they did not formally decide to look into the spending regarding the welcome to MCH until 19 June. That was eight months after the personal benefit to Mr Leauanae. That doesn’t seem even close to putting things right at the “first opportunity”, casts further doubt on Leauanae’s claim that he had always intended to pay for the travel himself, and strongly suggests someone with no strong sense of what is right and wrong when public money is being spent. Someone who still sits in a highly paid job as head of a New Zealand government department.

Peter Hughes was obviously somewhat constrained by the facts, but he consciously chose not to explicitly point out this timing, but to spin a story that would lead quick readers to think Leauanae had fixed things up straight away, not many months later only after the inquirers from his boss came calling.

Nothing in this story reflects at all well on Leauanae, and it really should be staggering that he goes on as a government department CE with, as far as the report suggests, no adverse consequences (he just repaid things when he finally got caught). Of course, it isn’t just the personal benefit, but the modelling and leadership (or lack of it) that will have led his former MPP underlings to think the lavish expenditure was ever acceptable, and the undisciplined processes etc reported last night in the Newshub story after they got hundreds of pages of documents from MPP. What gets you dismissed, or strongly encouraged to resign, when you hold a New Zealand government department CE role? Clearly not this record.

I’m also a bit surprised no one seems to have asked relevant ministers whether they have any confidence in Leauanae. In one of the weird bits of our legislation, they can’t sack him themselves, no matter (apparently) what he did, but the position of a CE would surely be untenable if the Prime Minister and the Minister of Culture and Heritage (as it happens the Deputy PM) indicated that they had no confidence in Leauanae. The PM has been reported as saying that the expenditure was unacceptable, but what of it? What is he going to do about it? He is, after all, the Prime Minister, and it is hard to believe that the Opposition parties will be leaping to the defence of Mr Leauanae.

Of course, it is always possible Hipkins and Sepuloni do still have confidence in Leauanae, even after what is already revealed about him (personal entitlement, weak and undisciplined financial management and people leadership etc). If so, that would be sadly telling. But you might have thought media outlets would at least ask whether they still have confidence in him, and if so why.

Yesterday the news broke of the extravagant spending at the Ministry for Pacific Peoples (MPP), and to a lesser extent at the Ministry of Culture and Heritage, centred on the transfer from one division to another of the core public service of MPP’s then chief executive Laulu Mac Leauanae. In the spirit of the unified public service (all that stuff that Peter Hughes and Chris Hipkins touted), shifting from running one smallish unimportant department to running another one seems about on par with someone moving from one modest division of an indebted private company to another.

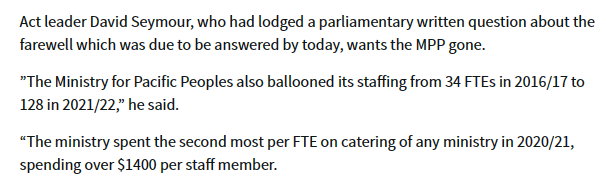

As the Herald reports MPP has already been a bit of an example of the extravagance with the public purse over recent year. A quadrupling in staff numbers for an agency with no clear or legitimate purposes….

In this example, staggering amounts ($40000) were spent on a farewell (for a person who’d worked for the Ministry for only five years), including extravagant personal gifts to the outgoing chief executive. Probably there was a case for a morning tea in the office (a cake and a few sausage rolls etc) or a drink after work for staff and a handful of outsiders. But it is hard to see a case for having spent more than a couple of thousand dollars in total. And impossible to see any case for (anything more than token) taxpayer-funded personal gifts…..the more so when the outgoing CE was just transferring to another wing of the same organisation.

And thousands of dollars spent by MCH on a welcome? What happened to simply turning up – at your new division of the same (government) enterprise – and starting work, with perhaps a staff morning tea or all-staff meeting at some early getting-to-know-you point? MCH has under 200 staff. Supermarket sausage rolls come quite cheaply. Four Governors started at the Reserve Bank in my decades there, and I don’t recall anything more extravagant for any of them (and in the earlier years the Reserve Bank was not a notably austere organisation).

You can read the Public Service Commission’s report and statement here. But what isn’t said there is at least as interesting as what is.

Starting with, how did PSC come to be so asleep on watch?

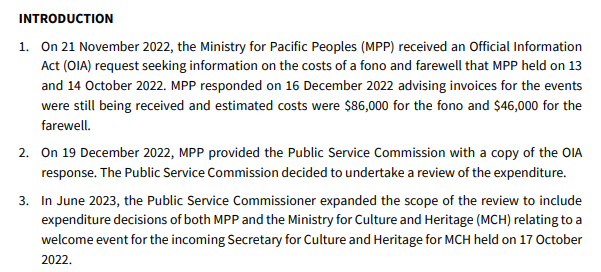

The farewell (and welcome) occurred in October. But this is the introduction to the PSC report

So either PSC didn’t even know about the event(s) – which frankly seems unlikely, unless they are even more slack than it seems – or no one there stopped to wonder just how much public money was being spent….until someone in the public asked. It is also pretty remarkable that MPP – by then under an acting CE – never thought of mentioning the OIA request to PSC until after the response had already gone to the respondent. As regards the costs of a farewell for one of the Public Service Commissioner’s CEs. And even when in mid January PSC decided to look into the farewell spending, it wasn’t for another five months that they thought to look at what had gone on as regards the welcome.

And that Herald extract above leaves one wondering just how much of all this we might have heard of the waste if it had not been for the written parliamentary question. Perhaps that is unfair, but the Commission’s approach was on display in a letter sent by the Deputy Public Service Commissioner on 17 January to the acting CE of MPP.

In that letter she states

my expectation is that the entire review process will be completed by mid to late February 2023. The final report will be published on the Commission’s website, but it will not identify any individuals by name and your agency will have the opportunity to comment on the draft report before it is finalised.

Not sure how she envisaged a report on a farewell for a CE naming no names but…. And it is August now.

Perhaps more concerning was this later in the letter

Which feels a lot like an attempt by PSC to stymie uses of key instruments of scrutiny and democracy (OIAs and PQs). It isn’t clear what OIA grounds they might have tried to withhold using……but with the OIA that rarely seems to stop agencies…..and PQs are questions from MPs to ministers, not matters that should be within the ambit of the PSC. The same text is in a letter dated 19 June from Peter Hughes to the MCH chief executive.

The PSC report has no reflections at all on PSC’s role or approach (or on any briefings they might have provided to their minister – at the time all this kicked off that was Chris Hipkins). In addition to the matters already touched on there was nothing at all about their own approach to agency oversight or to key appointments, that meant a culture developed in one or two of their agencies where spending of this sort happened. But of course to have done so might have been embarrassing for them, including because they had just promoted the CE, lauding him as a “sophisticated organisational leader” and not missing the opportunity to mention that expensive senior management course he’d recently done at Oxford. And yet his MPP senior management team not only thought it was okay to spend up big on his farewell (transfer) but (as the report documents) did so with no decent systems or budgets. The values and priorities of top leaders are well known by those beneath them. Nothing about this report suggests this CE preached or lived any sort of public sector frugality. But, never mind, he got the promotion……and holds the bigger job to this day.

Quite a lot else is glided over too. This is from the Peter Hughes statement

But neither here nor in the report are there any relevant dates. Mr Leauanae should simply never have accepted government departments paying for travel for his family members (tickets don’t just turn up), so reimbursing the cost when found out just doesn’t cut it.

Hard to see that sort of lackadaisical attitude being acceptable in anyone, at any level of the organisation. but……he was CE, displaying no sign of appropriate leadership at all. At best careless, at worst entitled (and note that the PSC report cites no evidence for his claim that “he always intended” to cover those expenses himself). And when did these refunds happen? A few days after the event, or only after PSC started digging? If it were the former it is highly likely PSC would have said so. Hughes refers to “the first opportunity” but the report itself does not.

And what of the gifts?

Many of the same questions arise? Surely on the day of the farewell, any public service leader should have expressed immediate extreme discomfort and returned all the gifts the same day? But there is no sign of any of that, and no indication that anything was returned before PSC started digging.

One could go on to note the sort of expenditure Hughes and the PSC seem to have no problem with. Recall that the welcome was to a transferring CE in a New Zealand public service department. As I said, a few sausage rolls and a welcome speech might seem reasonable. But not to PSC, which deemed all of this “moderate and conservative”

Sausage rolls and cup of coffee just don’t present the same challenges (or sheer waste). There was also this weird claim that somehow lavish expenditure was appropriate because

“In addition, the incoming Secretary was a Matai or chief, community leader as well as a public service leader.”

What he is or does in his private life is really neither here nor there (or shouldn’t be). You could be a hereditary peer, a billionaire, a generous philanthropist or whatever, and the fact remains that public money is being spent on a transfer of a public servant from one small agency to another.

In the end, the report seems to be largely a whitewash, at best slapping Mr Leauanae over the hands not even with a wet bus ticket but with a feather. He was found out, paid the money back after the event, and goes on to hold a CE position, in which if he ever utters words along the lines that public money should be used sparingly, rules adhered to in spirit as well as letter, staff probably scoff and go “one rule for you, and Peter Hughes’s favourites, another for the rest of us”.

But why should we be surprised? The twin cultures of entitlement and corruption, all accompanied by public sector bloat, are creeping ever onward. It is rare that any culprit ever pays a price – another Hughes CE took hospitality from an agency lobbying him to exercise discretion in their favour, and he went on to get a knighthood – and by their indifference we have to conclude that the government itself is unbothered.

As for the Opposition parties, they do part of their job in bringing some of this stuff to light and making a fuss now. But is there any sign of a robust open commitment to specific and much higher standards when their turn in government eventually comes? A CE who did what Mr Leauanae did (and allowed to happen) simply should not be still holding a government department CE job. That he is says that the standard now is not even “don’t get caught”. What standard is that for either other public servants? What sort of accountability to citizens and taxpayers?

In the years after the financial crises of 2008/09 one often read plaintive cries of “and who went to prison?”, and angry claims that the system was rigged. I can’t say that I was ever much moved by such lines. We simply don’t – or shouldn’t – generally imprison people for being bad at the business they are in, whether it is banking or baking, even if the businesses themselves were big, and the people concerned had employers who’d previously paid them lots (and lots) of money.

There has been a plethora of books about aspects of that crisis period. Glancing along my bookshelves just now I counted 100 or more, most of which I’ve read. Some were very analytical, some were lively descriptions of some aspect or other of that period, some country-specific, some more general, some were more about policy and policy institutions, some more about bankers and financial markets, but not one of them disconcerted me (and that is putting it very mildly) in the way that Rigged, a new book by BBC economics correspondent Andrew Verity did. (Amazon Australia shows the publication date as 1 August 2023, but I ordered it and it arrived a few days ago). It is a simply astonishing story, which shows a whole set of authorities (notably the British ones) in a very very bad light.

The context is the so-called “LIBOR crisis”. For readers who followed that story over the last decade, much of what follows won’t be new, especially if you’ve been in the UK. But I hadn’t really, because it seemed to be mostly a moral/political panic, in the “why aren’t evil bankers in prison?” vein. And, to be honest, from what little I had read of the story, I knew that I’d observed stuff in the little New Zealand markets in my years in the Reserve Bank’s Financial Markets Department that, if you were concerned about this sort of thing, was arguably more egregious.

LIBOR is (or was) the “London Interbank Offer Rate” (there was also LIBID – “bid” – although I don’t think it gets a mention in the book). It was a major set of benchmark short term interest rates, in various currencies, off which many other contracts are priced. LIBOR rates were set each morning – under the auspices of the British Bankers’ Association (BBA) – when cash dealers in each of 16 banks would indicate (for each currency and term)

“At what rate could you borrow [unsecured] funds, were you to do so [in the London market] by asking for and then accepting inter-bank offers in a reasonable market size just prior to 11 am?”

The submissions would be ranked, with the top and bottom four excluded and the remaining eight averaged. Individual banks’ experiences could be expected to differ a bit (although not by much in normal times), and for any individual dealer answering the question there might be a (tightly-bunched) range of possibilities. It was an estimate, informed usually by data in fairly liquid markets, with the exclusion and averaging rules dealing with outliers and, thus, typically expected to result in a reasonable central estimate. Very short-term rates would typically be very close to the relevant central bank’s policy rate. Within each bank, there was often a bit of jockeying: other dealers might have positions that would benefit a little from that day’s LIBOR rate being just a bit higher or a bit lower, but since the cash dealer had to lodge a response at which his (they were almost all male at the time) bank could borrow, any leeway was apparently very slight, perhaps one basis point, occasionally two.

And so it had gone on for a couple of decades. Regulators knew how the system worked, the adminstrators (BBA) knew how the system worked, as did participants in the markets.

But then the financial crisis began to build in the second half of 2007 (the crisis period is often dated from 9 August that year, the Northern Rock crisis became public in early September 2007). Short-term interbank funding markets were no longer as liquid as they had been and material gaps started to open up between where banks would lend to each other unsecured and the central bank policy rates (either for fully collateralised lending or risk-free deposits at the central bank itself). And there were swirling differences in market and media perceptions of which banks might be a bit less sound than others.

You might have hoped that each bank’s dealer would simply continue to submit each day his best estimate of what his bank could borrow at unsecured and let things fall where they may. But that didn’t happen. Instead it became something of a “dirty secret” (except not very secret at all since people in banks and markets knew it, as did the key regulatory bodies, and there were even stories in the major financial newspapers) that the published LIBOR rates no longer represented a best estimate of what individual banks (or the sector as a whole) could borrow from each other at. Verity focuses in on Barclays, where the cash dealer seems to have tried quite vigorously to follow the rules, which resulted in Barclays posting rates above those of the rest of the panel of banks, which (submissions being visible to others) in turn prompted concerns “if they are having to pay that much they must be in more trouble”, and even a sell-off in the share price. And so the pressure came on the dealer from above to bring his submissions more into line with those of the other banks. He, rather grudgingly (documenting his concerns and uttering them to anyone who would listen), went along. Regulators and central banks on both sides of the Atlantic were aware of what was going on, and if anything seem to have been more sympathetic to Barclays than (say) concerned that posted rates (used as benchmark pricing across the system) no longer reflected real borrowing costs.

As the financial crisis intensified so did the problems (some quite practical, in that at times the markets had frozen so badly that really no bank could borrow unsecured from others, so in truth there probably should have been no LIBOR rate at all). The gaps between unsecured interbank rates (both “true” rates and published LIBOR rates) and policy rates was high and widening, at times when central banks – in the UK, but in most other countries – were cutting policy rates deeply to try to lean against the collapse in demand and economic activity. Market rates often weren’t coming down much (in some cases they were rising) and politicians and their advisers were often getting increasingly uneasy.

And so the pressure – and this is extremely well-documented in the book – came on banks to put in lower LIBOR submissions. Doing so wouldn’t change actual borrowing rates – either interbank or the retail rates that the wholesale rates influenced – but I guess it was going to get better headlines, and it might make it “look” like things (policy responses) were “working”. In the UK case (the focus of the book), this involved not just very senior figures at the Bank of England, but them channelling pressure from The Treasury and Downing St itself (people named include very senior and otherwise respected figures, including a current Deputy Governor of the Bank of England, and someone who was until last year the permanent head of The Treasury in the UK). Very senior bankers were left in no doubt that the authorities wanted the LIBOR rates marked down, and they complied, ordering their underlings (the cash dealers and their immediate bosses) to bring LIBOR submissions more into line. The differences here were not a matter of a basis point or two, but often 50 basis points or more. Relative to the LIBOR rules, anyone with a contract in which they received the LIBOR rate was, in effect, being bilked out of a lot of money (vice versa if you were paying LIBOR). One could, of course, argue, that central banks were actively trying to lower short-term rates generally by a lot, but…….acceptable instruments don’t generally include pressuring bankers to write down numbers that simply don’t reflect reality. If central banks really wanted market rates even lower, they had tools available to make that happen directly.

The more pragmatic and less idealistic of you may here be drumming your fingers and going “needs must”, and in a crisis what needs to be done gets done. I wouldn’t agree with you – institutions are supposed to be built for resilience under stress, not for fair weather events only – but if that was the end of the story, it would have been quickly lost to history.

But it wasn’t the end of the story.

As the crisis faded, in some circles the narrative that someone “needed to pay” took hold. At least in the UK, as I read the book, there wasn’t much interest in pursuing anything around LIBOR, until the Americans got involved. You might reasonably wonder what the activities of British officials in Britain and British employees of British banks in Britain, as regards a benchmark rate owned and administered by a British entity (the BBA) had to do with the US, and its Department of Justice and CFTC. They seem like good questions, but such is the world as it is, and the trans-national overreach of the US on matter financial. As Verity tells it, Obama’s nominee for head of the CFTC had had close ties to Wall St and wasn’t going to get confirmed by the Democrat-controlled Senate unless he was going to take a credible stance as an avenging angel of wrath.

My interest is less in the US side of things than in the UK, where (thanks to leaks in particular) the book is astonishingly well-documented. Anyway, the US started pursuing banks abroad (Barclays in particular in this book), in what seems like a bizarre process in which they relied on the banks themselves to search their own documents, and then negotiated (large) administrative fines, which saved the banks and their CEOs and chairs, all while throwing under the bus a few fairly junior employees who’d initially been more or less compelled to talk to the US authorities, thinking of themselves as expert witnesses etc, only to find themselves personally in the gun,

These employees became alert to the prospect of spending much of the rest of their lives in a US prison, (having regard to the very low acquittal rate in US courts) for things they were quite sure they had never done, except as normal, accepted commercial practice, well known to central banks and regulatory agencies on both sides of the Atlantic, typically either authorised or instructed by senior managers within their own banks. And so several became convinced their only option was to get themselves charged in the UK, preferably engaging in a plea deal that might involve, to all intents and purposes, lying to conform with the preferred narrative of the UK authorities, to get to stay in the UK and not destroy themselves and their families financially. Others preferred to defend themselves in the UK, several were charged in the US (before US courts finally overturned the very basis on which they had been charged).

And, to be quite clear here, none of all this regulatory and legal action involved anything that had gone on during the financial crisis (when not only had authorities, notably the Bank of England, been aware of how the system worked, they had actually been part of engineering LIBOR submissions a long way from actual market rates). Instead, the bounds of interest were very carefully drawn to cover only the period prior to the crisis beginning to unfold. The focus was on how these dealers had lodged their LIBOR submissions in normal times, as many many like them had done for a couple of decades. The focus was on other people in each bank suggesting to the dealer that their positions might benefit from a slightly higher or slightly lower LIBOR (the basis point or two mentioned above, in reaching a necessarily imprecise estimate).

And what was the offence? Well, there was none in statutory law. None.

Instead, the authorities wheeled out an old common law offence “conspiracy to defraud”, which – at least as Verity tells it – was so little regarded by the UK commercial barristers prior to the crisis that there had been a push to remove it. Under these provisions/precedents, there was no need to show that anyone had lost, or to quantify any losses. And yet the political rhetoric was all about egregious rip-offs, suffering customers, and rigged markets. Judges ruled – without allowing appeal – that it was enough that someone in a bank had suggested to the bank’s cash dealer that his/her positions might benefit from a slightly lower/higher LIBOR and the dealer to say something like he’d see what he could do. There was – according to English justice- a conspiracy to defraud – all recorded in emails and trading room recorded phone calls. The same judges then refused to allow testimony from expert witnesses as to how markets actually worked (in one case regarding EURIBOR submissions, the UK judge refused to allow testimony from the people who had written the code of conduct around the operation of EURIBOR).

Here, some scale and perspective is worth noting. As I noted above, LIBOR worked with a panel of 16 banks, with the four highest and four lowest for any particular currency/term on the day excluded. If perhaps a dealer in one bank had shaded his bank’s estimates 1 basis point in one direction (remember that plausible range was typically not much more than a couple of basis points), then even assuming there was not some other bank with exactly the opposite interest, the chance of affecting LIBOR at all was low, and the magnitude of any plausible effect tiny. There are hard numbers at places in the book.

By contrast, the activities during the financial crisis period, done in full awareness and often with the encouragement of the authorities and of specific named very senior bankers, never saw judicial scrutiny.

And so eight bankers – cash dealers – went to prison in the UK, serving non-trivial custodial sentences, for offences that no one thought were offences until the “avenging angel” mood took hold in the wake of the crisis. And when I say “no one” here I mean not just the dealers, but their bosses, their bosses’ bosses (the chief executives of the banks were the board of the BBA which administered LIBOR), and the central banks and regulatory authorities on both sides of the Atlantic, but particularly (and at very senior levels) the Bank of England. Not one Bank of England official rang the police (or SFO) at any point to express concern at the normal commercial way they knew the market worked, and those senior people are on record during the crisis encouraging/abetting/ (perhaps) instructing, bankers to deviate from the LIBOR rules, including passing on the political pressure from Downing St (which was no part of any central banker’s mandate).

And yet, as Verity records, in 2015 at the height of the hysteria – and amid the criminal trials – the then Governor of the Bank of England delivered a major speech in which he would “publicly demand that the government should change its sentencing guidelines to raise the maximum jail term for “rogue traders” from seven to ten years”. This was (is) the same central bank that (Verity records) “George Osborne had urged the central bank to come clean about its role in Libor, [but] the Bank of England had decided against that. Freedom of Information requests would be consistently rejected in the succeeding years”.

Your reaction might be to wonder why anyone would be particularly sympathetic to well paid (not very senior) bank traders. Because it was an egregious abuse of justice: sound process and integrity matter whether it is a scruffy teenager or a nicely-dressed multi-millionaire trader facing the system. Any of us could one day be in gunsights of the state. I mean, if one were going to (in effect) create retrospective offences and start prosecuting bankers for them mightn’t one prosecute those in charge (all the way up) who were actively aware of how things worked, authorised and rewarded people, and at times directly instructed behaviour that was egregiously distortive (in terms of LIBOR rules/practices (rather than, as in at least one case a ‘whistleblower’), and consider expert testimony from people with responsibility for overseeing the relevant markets etc.

The conduct of three lots of people in this whole affair warrant scrutiny:

the politicians. How did Cabinet ministers stand by and allow these prosecutions and imprisonments when (if nothing else) they knew the people who managed and instructed those charged walked free, with no criminal or civil consequences whatever? And how did former PMs and Cabinet ministers (Gordon Brown, Alistair Darling – Chancellor during the crisis) never speak up and out, not just about their own roles but the disproportion of sending low level people to prison while their bosses walked free? It is the sort of act of omission that leads people to simply despise politicians,

the senior bankers. Many despise them already, but really……..you keep your job and your bank or walk way with tens of millions in retirement packages etc, while seeing former staff – who acted on your instruction and authorisation – sent to prison, people against whom charges were laid only because you did your own searches of your own bank records, saved yourself, and tossed some staff to the criminal authorities. Just despicable. Who ordered Peter Johnson (cash dealer at Barclays) to mark down his submissions, despite Johnson’s explicit written dissent? Why, the very top tier of Barclays’ management.

the central bankers (and the like). I expect better from central bank and Treasury officials. Not necessarily excellence or at times even basic competence, but integrity and decency. I’ve met and dealt with some of the individuals named (I recall now sitting in the Bank of England’s chief economists’ seminar in May 2008, in the early days of the crisis, listening to Sir John Gieve, deputy governor responsible for financial stability – altho, curiously, not named in the book) so perhaps it shocks me more. Perhaps one can defend the approaches senior BoE or HMT (or even Downing St) officials took during the crisis, but they actively aided (and seem to have pressured banks to facilitate) the distortion of LIBOR. I’m not suggesting any of them should have been prosecuted, but how (a) does the Bank of England justify not revealing in full its own part and knowledge during the period, all while Mark Carney as Governor was baying for the blood of traders, and b) how come that, even in retirement, not one of these people spoke out and suggested that it was simply wrong to be sending these people to prison. None of them appears to have been willing to speak to Verity, none has spoken in public, and we are left guess whether just possibly one or two might have said quietly “I say old chap, are we really sure about this?” (if so, to no apparent effect). It reflects very poorly on all involved, some of the most senior (and otherwise) respected figures in British economic and financial policy. One could see it – perhaps unfairly but it isn’t obvious what other interpretation makes sense – as circling the wagons in their own defence, and that of their peers who ran the banks. Never mind the juniors, we can destroy their lives and marriages and send them to prison. (These the same people whose own policy misjudgments – viz recent inflation (Andrew Bailey gets a couple of minor mentions in the book) – result in few/no consequences beyond gilded retirements and knighthoods or peerages.)

From the sound of the book, the English prosecutorial and judicial systems have quite a bit to answer for as well, but….I’ll leave that to the lawyers.

The whole thing smacks of a witchhunt: someone must pay, these individuals their bosses have helpfullly pointed us to are someones, so they will do (and it wouldn’t do to pursue the bosses or else, perhaps, confidence in the system might be eroded – which if true should have at very least raised questions as to whether the whole grossly-slanted chain of prosecutions, where eg juries were never allowed to know what regulators had known in advance, was being pursued for any reason other than the a politically-driven effort at distraction).

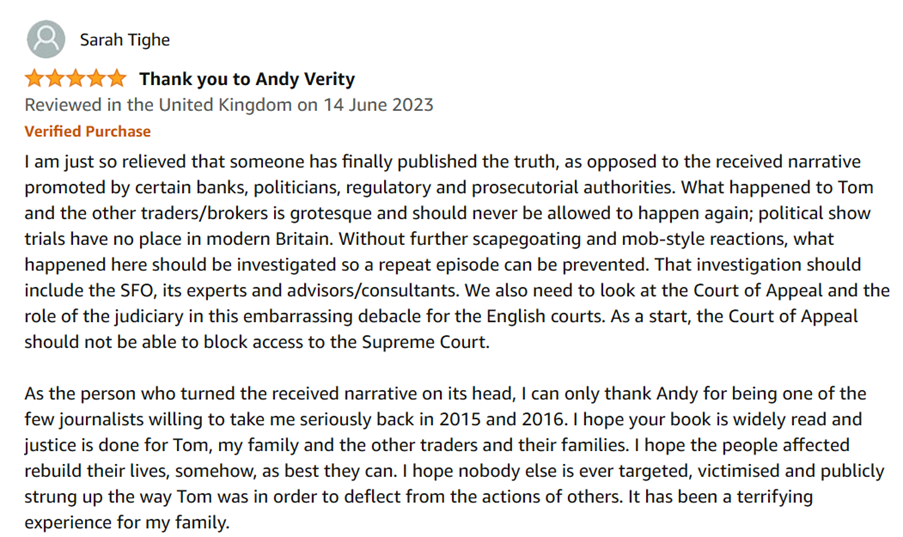

It is hard to tell if I’ve done a 325 page book justice. All I can do is to encourage people to read it. Yes, it is about technical stuff, but Verity does an impressive job of explanation and translation, and his story is supported with copious direct quotations, most of which would never have come to public light if a big dump of documents and recording had not been leaked to him. I’m going to leave you with the Amazon review comments of Sarah Tighe, herself a lawyer, ex-wife of one of those sent to prison (there is a recent extended interview with him here)

I went looking for reviews of the book, and couldn’t yet find any yet. But interest in the issue seems to be rising again in the UK (here is a recent parliamentary speech from a senior backbencher).

One fears that even if the individuals eventually have their convictions overturned (and how do you compensate someone for a life destroyed?) that officialdom in particular will never have to answer the hard questions it seems it (collectively and as accountable individuals) should.

PS Someone who isn’t named in the book, but the division he ran is, is the Reserve Bank’s Deputy Governor whose CV includes this

Now that was probably a fourth [UPDATE: or perhaps 5th1] tier position in the Bank of England, and he took this specific position up just after the worst, so he wouldn’t have been in any sort of direct decision-making role. But one is left wondering how he feels about those sent to prison while he’d been a fairly senior part of a system and institution that was encouraging banks actively to manipulate LIBOR submissions/rates. It should matter in someone who is (a) on the MPC, b) is head of financial stability here, and c) must be one of the favourites to himself be the next Governor of the Reserve Bank. There is that old line “the standard you walk by is the standard you accept”. No one should accept – or walk by – the standards of officialdom on display in this book.

See references to Hawkesby in footnotes to the organisation chart on page 60 of this later BoE report

It was the Monday a few days before Christmas 1992 when a colleague wandered into my office and asked if, by any chance, I was interested in a couple of years in Zambia. My colleague had just returned from a few years at the IMF in Washington and had been rung the previous day by a former colleague of his desperately looking for someone who was interested in being resident economic adviser to the Zambian central bank, all at short notice, as the incumbent was due to leave shortly, and the reform programme (and IMF programme) was in trouble, with inflation through the roof. If I recall correctly, they’d had someone lined up, who had a baby, but news of a cholera outbreak had come through a few days previously. The job was going vacant again.

My knowledge of central Africa was sufficiently sketchy that, in those pre-internet days, I had to wander down to Bennetts bookshop on Lambton Quay and buy a Lonely Planet guide to Africa to (a) securely locate Zambia on a map and (b) find anything at all about it. I rang the guy who was just about to finish up (an RBA secondee I knew), and if some of his stories were sobering – consumer good scarcity so real that he told me that afternoon they’d released the staff because some or other essential had finally appeared in shops – the job itself sounded challenging and potentially rewarding, with a new Governor with no background in central banking or macro but with a serious commitment to overhauling and lifting the performance of the institution. Within 24 hours I had a (very remunerative) offer on the table.

The Reserve Bank subscribed to the hard copy Financial Timesand a couple of days later an issue with a Zambia supplement landed on my desk

What wasn’t to appeal? Idealism even in the FT headline. Zambia was, if I recall correctly, only the second African country to have restored multi-party elections and to have changed governments.

I was young and single and had more or less done what the Bank had asked me to do when they’d prevailed on me to take my then-current job a year earlier. The slaying the inflation beast phase in New Zealand looked to be more or less over. The Bank knew I was looking round, although their ideas of a next role were a bit less unorthodox than heading off to somewhere like Zambia. A little reluctantly, they agreed to the secondment.

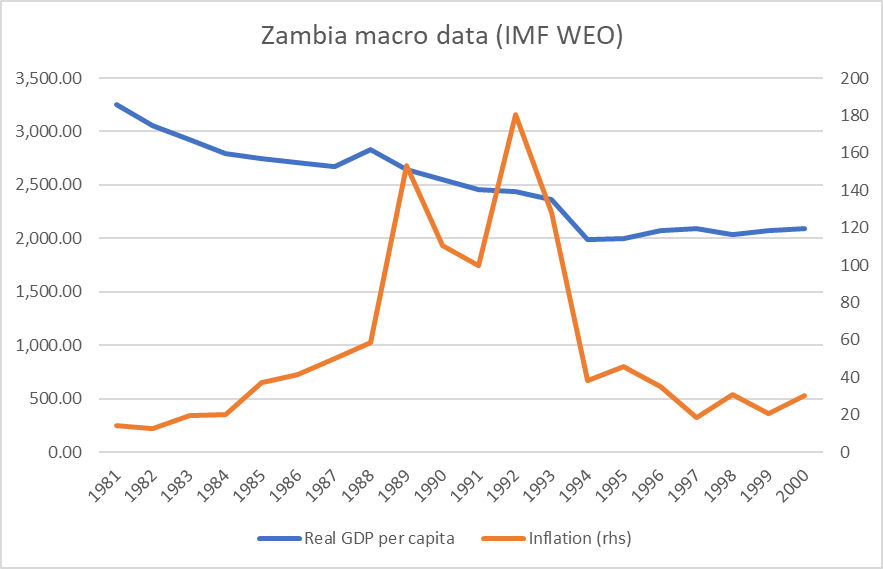

Inflation in Zambia was 181 per cent in the year to December 1992 and, if anything, rising (monthly inflation rates were about 10-12 per cent), and with all the donor goodwill in the world (and there was a lot of it towards the Chiluba government, just 12 months into the new era) things had to change. Making sense of what was going on wasn’t helped by the (literal) inability of the central bank to produce a balance sheet (there had been a serious computer system failure months earlier.

It was a wild, exciting and often frustrating, time to be there. As a place to live – and despite the mostly great climate – there was a little to commend it, but professionally that first chaotic year pushed one to the limit. In some respects, it was the best job I ever had, with that sense of being able to make a real difference, and see the people around me growing and developing capability.

As the blame for any really serious bouts of inflation rests with politicians, so ultimately does the credit for beating it (not only wasn’t our central bank formally independent, but when the governing party has 80 per cent of the seats in Parliament changing legislation wouldn’t have been much of an obstacle anyway). And if the roots of really serious inflation are always fiscal, so are the solutions. Zambia’s was the “cash budget”: the Minister agreed that money would not be spent that was not first in the government’s accounts at the central bank (whether from taxes, donor grants, or domestic borrowing), and each morning we and Ministry of Finance officials would pore over the numbers to get a sense of what payments could go through.

When it was made to work – and it was harder than it sounds, with threats and political tensions almost by the day – we presided over a liquidity squeeze on a scale rarely seen. Flicking through old diaries yesterday I found reference to Treasury bill auction yields at times averaging 600 per cent or more. The exchange rate, which had relentlessly trended down for many years, stopped falling and even began appreciating in nominal terms – it was to be a savage appreciation in real terms. I don’t have monthly data to hand (yes, even then Zambia – unlike modern New Zealand – had a monthly CPI) but if I recall correctly we even had a couple of negative inflation months. It wasn’t a new dawn of price stability – annual inflation settled in a range around 30-40 per cent – but the looming threat of hyperinflation has been beaten.

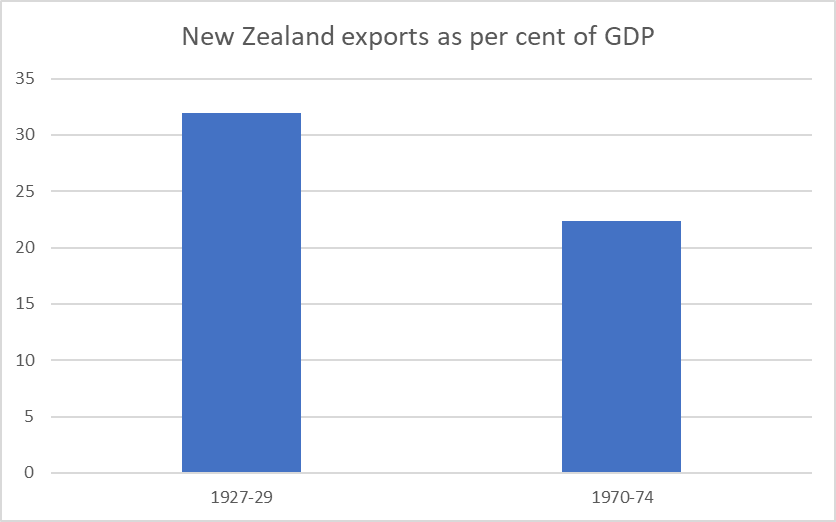

It was hardly a new dawn of prosperity. As in most places, difficult structural reforms have short-term real economic costs, and driving out entrenched inflation is rarely costless either. We didn’t have timely national accounts data then, so this chart caught my eye when I put it together a few weeks ago: notice the almost 20 per cent fall in real GDP per capita in a single year from 1993 to 1994. We knew it was tough – aside from anything else, exporting firms were not slow telling us – but the numbers are still sobering. Cold turkey treatments aren’t easy. In the space of a few months, we went from having the IMF doubting the seriousness of the authorities (and in fact outright lies were at times told by the authorities to the IMF to keep the programme on course) to having them concerned we had “got religion” and were overdoing things.

The Governor, Dominic Mulaisho, was probably the most inspiring person I ever worked for. As I said earlier, he’d had no background in central banking or macro, had only been appointed in 1992, and had had a history as a senior official in various leading government agencies in the post-independence period. He was also a published novelist, educated in Catholic mission schools before university in (then) Southern Rhodesia, and was, I think, always disappointed that my own command of Shakespeare and English poetry didn’t match his. He could be endlessly frustrating – I found diary reference to a 7 hour Monetary Policy Committee meeting one Saturday, an MPC that then was just about data presentations and lifting the quality of economic analysis and debate – but had an absolute commitment to better days for his country, and for the institution, and a stubborn integrity that finally cost him his job a couple of weeks before my term ended in 1995 (we were trying to close down a Zambian multi-national banking group that was evidently insolvent, but which had powerful friends). As just one indication of what he was up against, the night before I left the country he invited me round to his house and over drinks told me the story of travelling abroad with the then Minister of Finance who took him aside and (so my diary records) said “Governor, my aim is to get rich and to get rich quick. Your job is to help me do that, not to obstruct me. Why don’t you help me?” (both men are now dead).

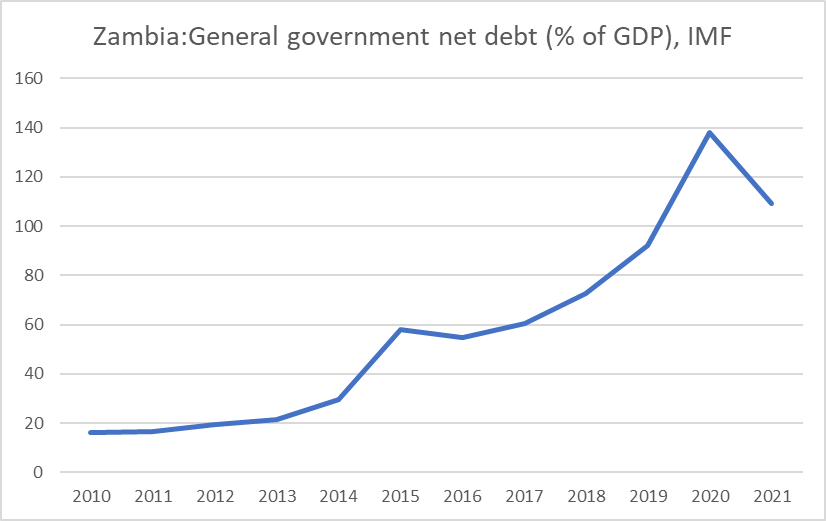

The prompt for this post is that I have spent the last couple of weeks back in Zambia. Times have changed. Several of the young grads I worked with then now hold some of the most senior positions in the central bank (and the chief economist from those days is now the Minister of Finance). Zambia isn’t without its continuing macroeconomic challenges. Debt-fuelled splurges over the last decade ended in a default on the foreign debt in 2020.

And if there seems to be lots of donor and international agency goodwill towards the new government (and many of the great and good have visited Lusaka this year, including Janet Yellen, Kamala Harris, and the IMF Managing Director), hopes of a substantial debt writedown are currently stalled.

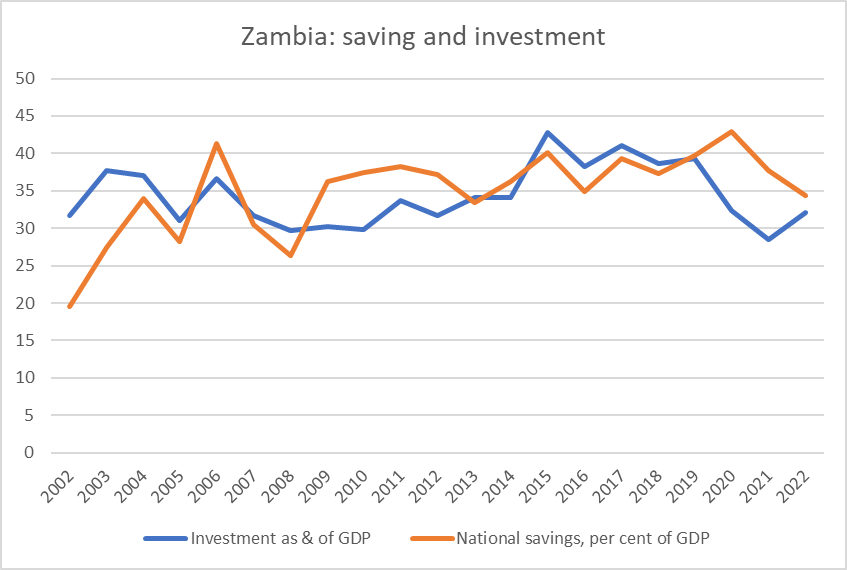

You can see the investment the debt helped finance in the data

Investment rates of 40 per cent of GDP are high by anyone’s standards.

But it was also visible as I walked and was driven around Lusaka over the last couple of weeks. You can see the new public infrastructure and the new private investment (shiny new office complexes, and the proliferation of small malls in the middle income parts of the city), even if the old main street, Cairo Road where the central bank is, was much the same as ever. It is visibly a different, and less raw, place than it had been 30 years ago. And you find something of that in the numbers too: in a country with a very rapid population growth rate, real GDP per capita is estimated to have risen 60 per cent since 2000.

The group I was working with asked a lot of questions about the contrasts and my experiences 30 years previously. As I reflected on it, one that struck me was the nature of the region. In 1993 when I first went, Zambia itself was a little more than year on from a democratic transition. Lusaka had hosted the ANC in exile and if they’d mostly returned home, the transition to democracy in South Africa was still a hopeful prospect rather than an accomplished fact (Chris Hani was assassinated just a few weeks later). The Angolan civil war still raged, the Mozambique conflict had ended only a year earlier, Namibia had become independent as recently as 1990, in Malawi the brutal Hastings Banda still ruled, and the genocide in Rwanda was only a year away. The DRC was, well, the DRC. (By contrast, Harare was a haven of functionality, before the chaos descended in Zimbabwe). These days, if democratic transitions aren’t common outside Zambia, peace and relative stability reigns, and there is a sense of relative normality about much of the region. Various countries have managed some material real income growth. And the best hotel in Lusaka – that I lived in for a year, and stayed in again last month – is now owned by, of all entities, the Angolan sovereign wealth fund.

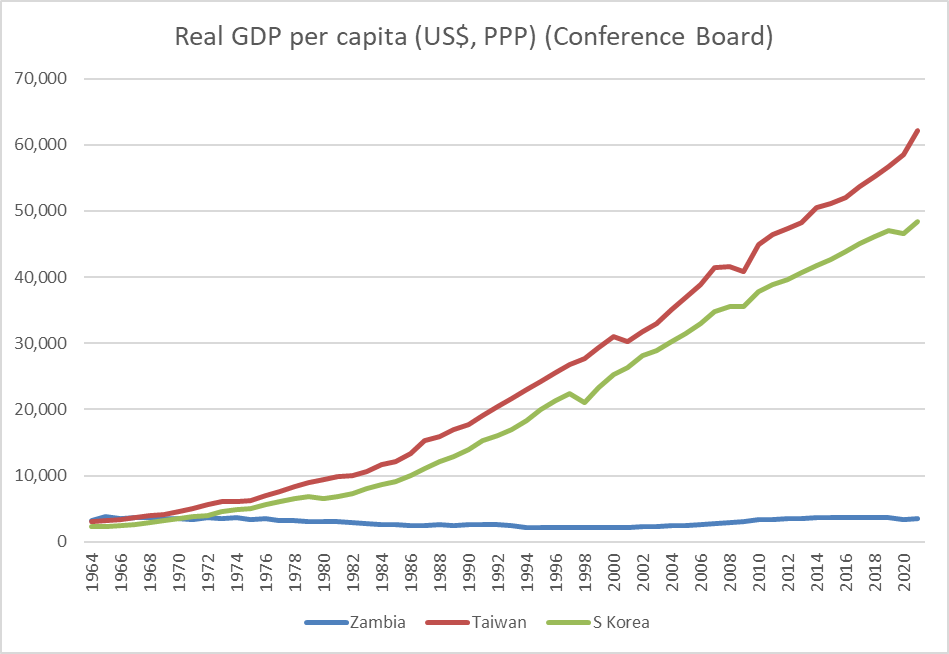

But then there is the longer-term context. Back in the 1990s we used to tell the story (including to the numerous international visitors who passed through) that at independence in 1964 Zambia had been a bit richer (per capita income) than Taiwan and South Korea (one of the richest countries in Africa, at a time when South Korea and Taiwan were already in the early stages of their growth trajectory). I put this chart on Twitter a few weeks ago

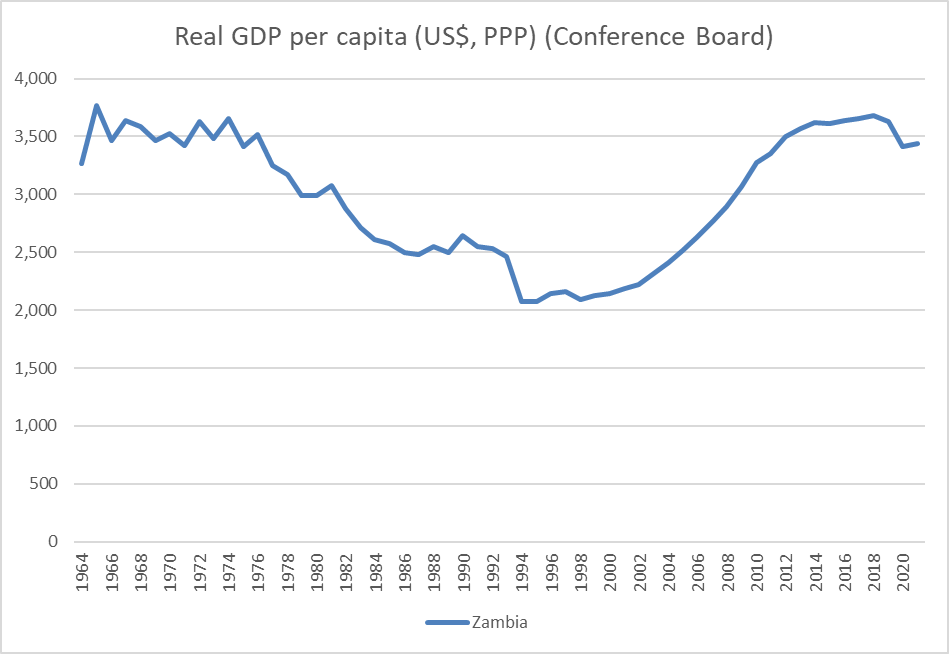

And here is the Zambian version alone

Almost 60 years on, real GDP per capita is barely higher now than it was at Independence.

It is a great country, with friendly people, abounding in physical resources (land area alone is equal to France and Germany combined) and still a major copper producer. If you have never been to the Victoria Falls you really should one day. And there are many countries in Africa worse off than Zambia (and much richer South Africa has also seen next to no real per capita GDP growth since the mid 70s). There is a lot I like about the place, but……the challenges before them to achieve and sustain big improvements in material living standards for their people are huge.

(Among the things to like, I picked up Covid while I was in Zambia. Unlike New Zealand, a colleague could wander down the street to the nearby chemist and buy me a cold and flu remedy that really worked – no bans on pharmacy sales of pseudoephidrene products there.)

Back in 2020 and 2021, in and around the straight economics and economic policy posts, there were quite a few on aspects of the Covid experience in New Zealand, particularly in a cross-country comparative light.

More recently, you see from time to time suggestions that New Zealand’s experience may have been so good that in fact excess mortality here since Covid began might actually have been negative (in which case, fewer people would have died than might have been expected had Covid never come along.

A couple of alternative perspectives on that caught my eye in the last couple of months, both from academics, one from a physicist and one from an economist.

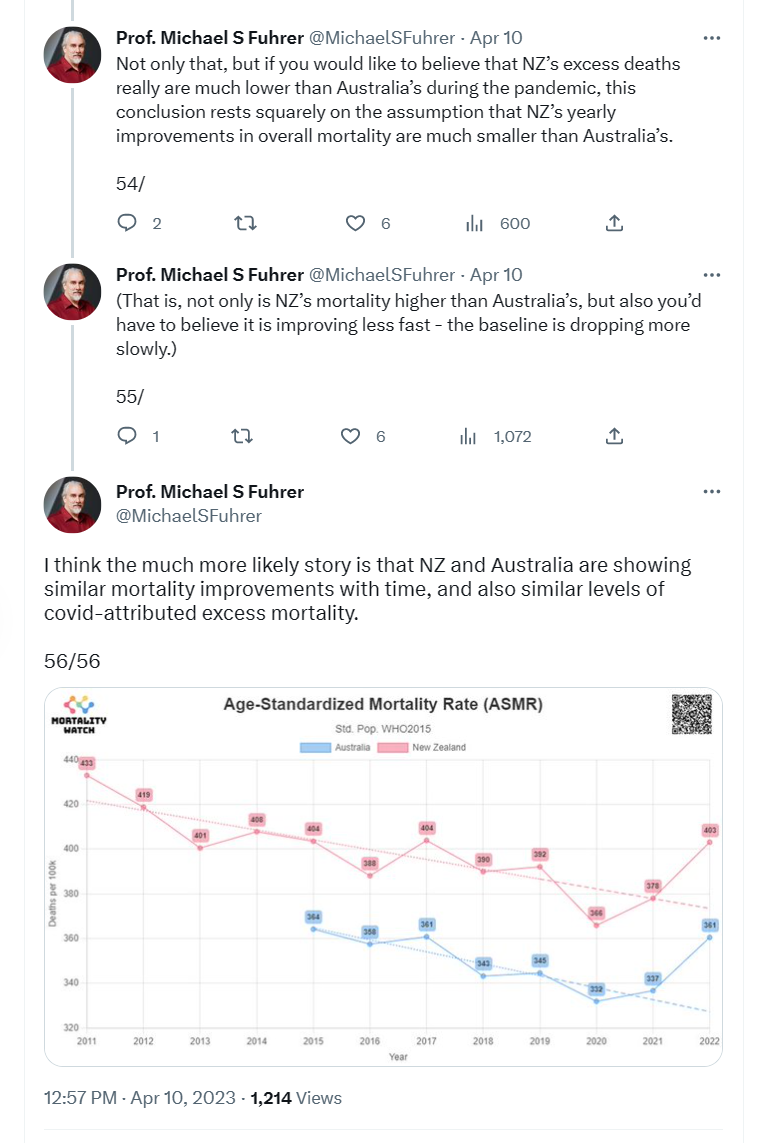

The first was a very very long Twitter thread from Professor Michael Fuhrer at Monash in Melbourne. His thread starts with this tweet

and after reviewing the evidence, and granting that

he concludes that

All of which sounded plausible, at least having read the entire thread.

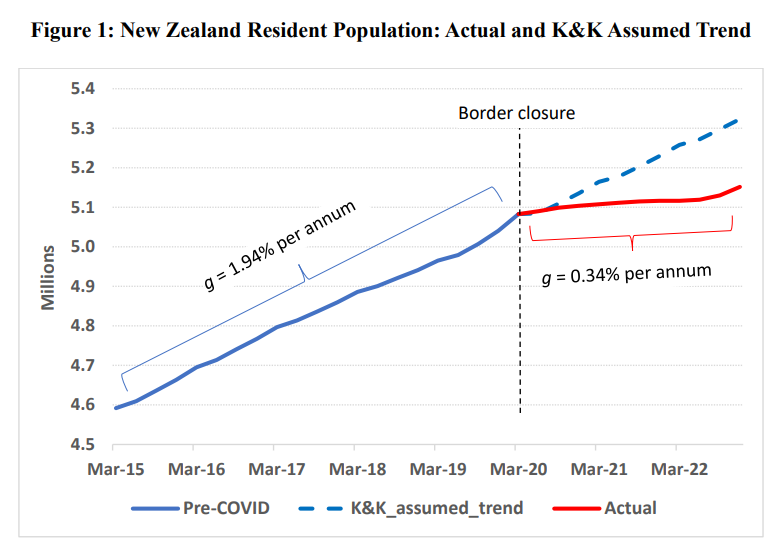

For New Zealand, one of the biggest things that changed over the first 2.5 years of the Covid era was a dramatic slowing in the population growth rate, not because of Covid or other deaths but because net migration went from a hugely positive annual rate to a moderately negative rate. Pre-Covid – and probably again now – migration is the biggest single influence on the year to year change in New Zealand’s population. He includes this chart

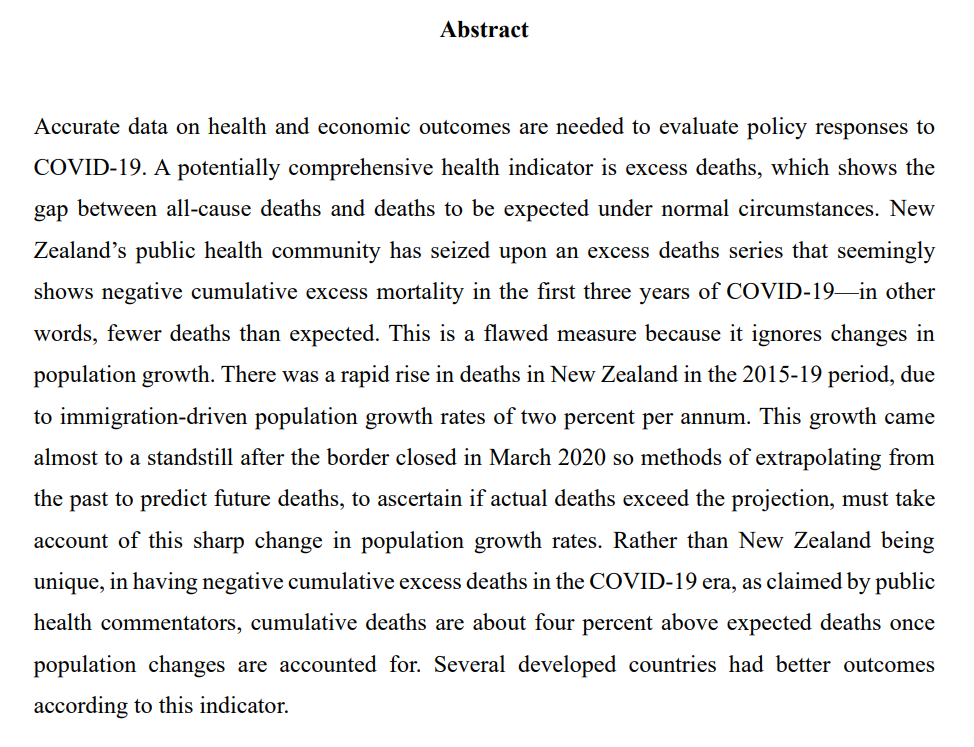

Here is Gibson’s abstract

It is a short paper, and easy enough to read, so I’m not going to elaborate further, and will simply cut and paste the final page.

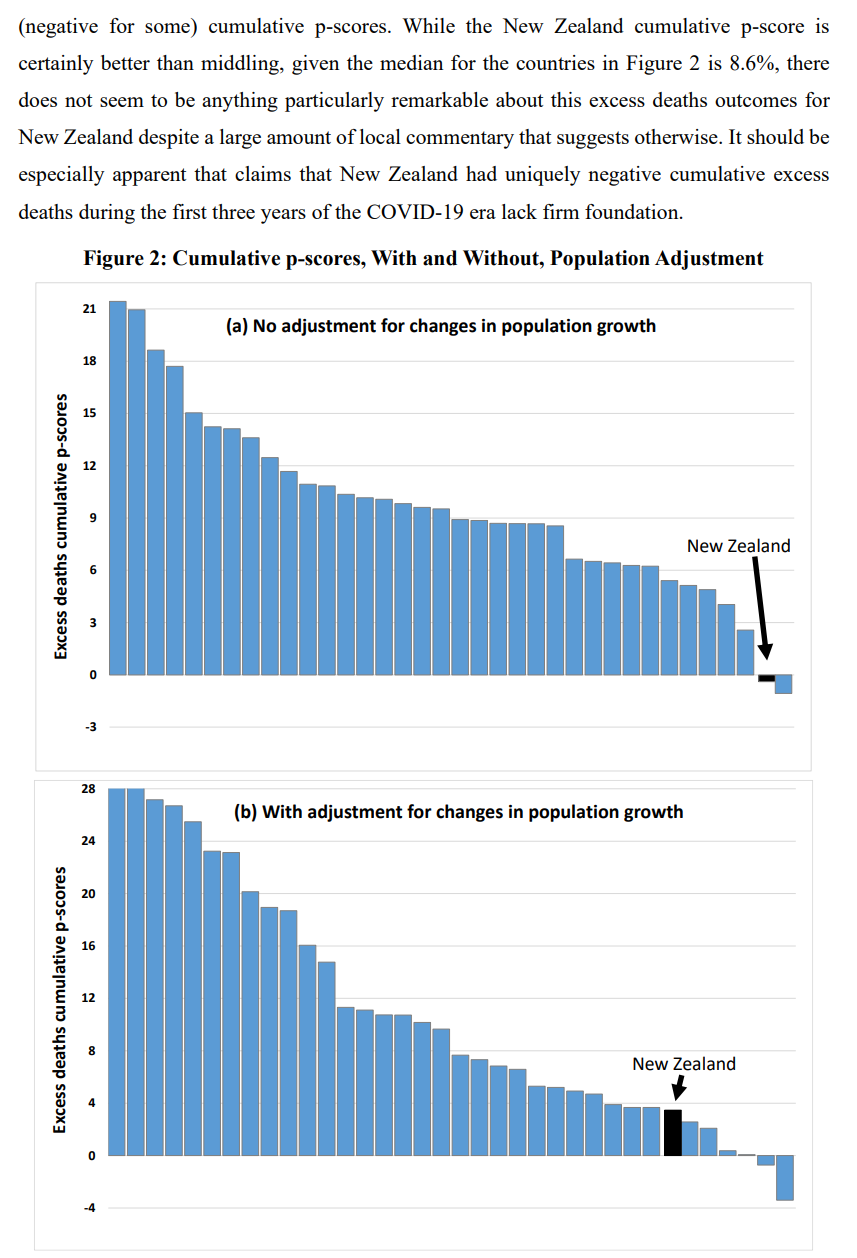

It is a shame he hasn’t labelled all the other countries, but his text tells us that the countries to the right of New Zealand on that bottom chart are Luxembourg, Canada, the Netherlands, Iceland, Israel, and Australia. Note too that several countries just to the left of New Zealand have estimated excess mortality barely different from that estimated for New Zealand.

Across the entire grouping of countries New Zealand still rates fairly well (there are many other things we might reasonably hope to be in the best quartile for but are not; this one we are), but as he notes for the three years to the end of 2022 even in New Zealand there does appear to have been positive excess mortality in the Covid era.

I have no particular point to make, but found both Fuhrer’s thread and Gibson’s note interesting notes, providing some useful context to thinking about the New Zealand experience. Since one still sees claims (including reportedly from David Seymour just a couple of days ago) that there have been no excess deaths in New Zealand over the Covid period, is it too much to hope that some media outlet or other might give some coverage to what appears to be careful work by, in particular, Gibson, a highly-regarded New Zealand academic?

There is an op-ed on the Herald website this morning on “The role of corporate profits in inflation”. It is written by Max Harris, a lawyer and political activist. He was campaign manager for Efeso Collins in the Auckland mayoral race last year, which should give you a sense of how far to the left he sits on the political spectrum.

Harris is a smart guy, and it is evident from the article and his tweets that he has read a number of papers that have emerged recently from overseas academics and some central bankers suggesting that corporate profits might have some distinctive role in explaining the recent surge in inflation. I say “distinctive” because in the same way that nominal GDP can be decomposed into price and volumes, it can also be decomposed into returns to labour and returns to capital. In a demand-driven surge in inflation it would entirely normal to see all four of those items growing at above-average rates. And since both wage rates and employment tend to be stickier (slower to adjust) than profits – which are the residual, what is left over after other business expenses have been met – it shouldn’t be unexpected to see profits rising and falling earlier and more markedly than, say, wages. That wouldn’t tell you that profits were “to blame” for the inflation in any meaningful sense.

I’m not going to devote this post to unpicking the entire literature on profits and this cycle. Instead, I just wanted to present a few New Zealand charts.

One of the few things I agree with Harris (in this article) on is that New Zealand economic data is not really fit for purpose. There are significant gaps, in coverage, frequency, and timeliness, which really should be remedied. There aren’t (m)any votes in good economic data but it is the sort of thing good governments should be spending on nonetheless.

All that granted, it was striking that there was only one New Zealand specific number in Harris’s article

Now, to be fair, op-eds don’t provide for a limitless word count. But it isn’t hard to do much better than that one number.

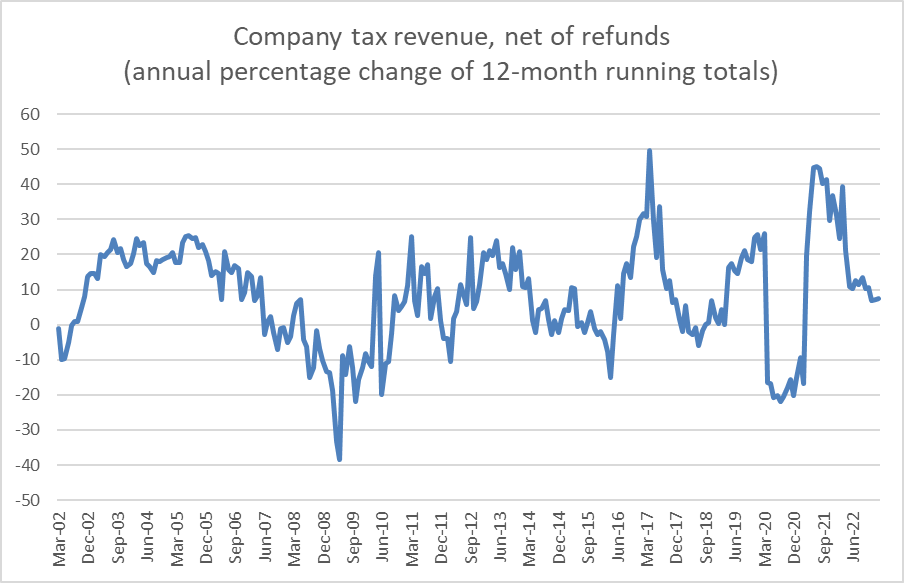

I found a description here as to what Ed Miller had done (note that his calculation was done nine months ago) and replicated his number. Using the Treasury monthly tax database, sure enough you find that company tax revenue (whether including or excluding refunds) for the year to March 2022 was 39 per cent higher than it had been in the year to March 2021.

But here is some context

For the 12 months to February 2023 net company tax revenue was up 7.5 per cent on the 12 months to February 2022. The most recent nominal GDP data is only up to December 2022, but nominal GDP in the 12 months to December 2022 was 8.5 per cent higher than in the 12 months to December 2021.

But perhaps the key point is that company tax revenue is very volatile (in the 12 months to April 2017 the annual growth had briefly reached 50 per cent), with deep troughs and high peaks. That isn’t just because profits can be volatile, but also because of loss carry-forward provisions (when your firm makes a loss one year IRD won’t send you a cheque, but you can credit those losses against future profits (if/when your firm returns to profit). When those losses are exhausted, revenues can jump up very quickly even if profits themselves are less variable.

In this specific case, of course, the year to March 2022 (which Harris cites) followed the year to March 2021, a year in which net company tax receipts had been down 17 per cent.

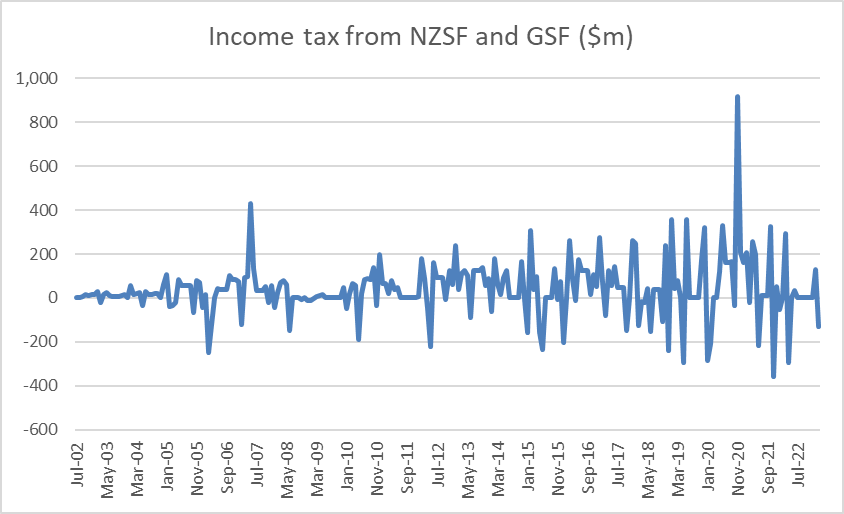

We could dig a little deeper on the same Treasury spreadsheet. Treasury breaks out income receipts from NZSF and GSF, which are really just branches of the central government itself.

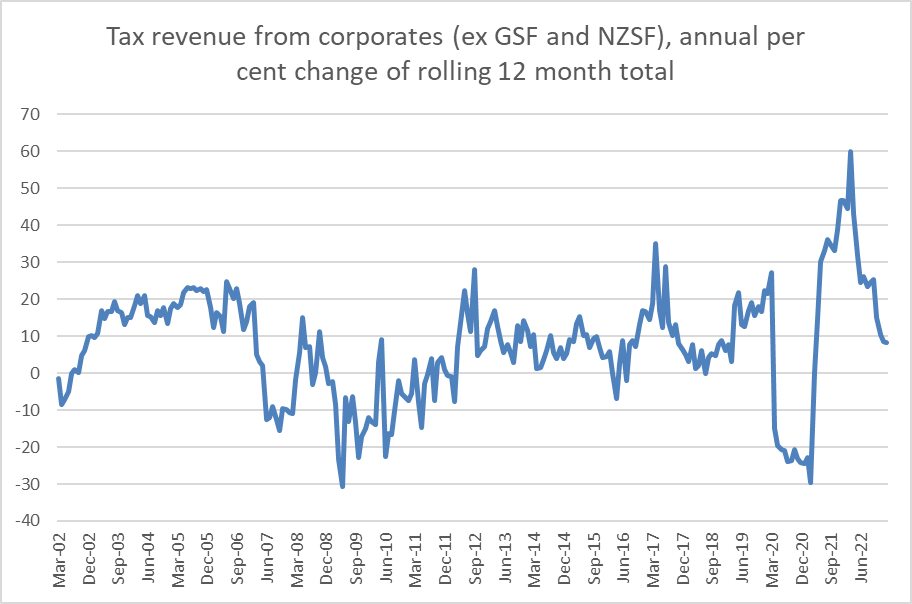

NZSF (the big dollars here) was only set up 20 years ago, so the initial figures were mostly small. These days it is large and has quite volatile returns (and, it appears, tax liabilities). Here is what the corporate tax line looks like with NZSF and GSF income tax removed (which is one of the adjustments Treasury does to get to core Crown measures of tax)

The recent peaks and troughs are even larger. (Note that when, as they did in the 12 months to March 2021, tax revenue from this source falls 30 per cent it then needs to rise by about 42 per cent just to get back to the starting level ($m).

Strangely, we rarely hear much from people like the Green Party when company tax revenue is falling sharply.

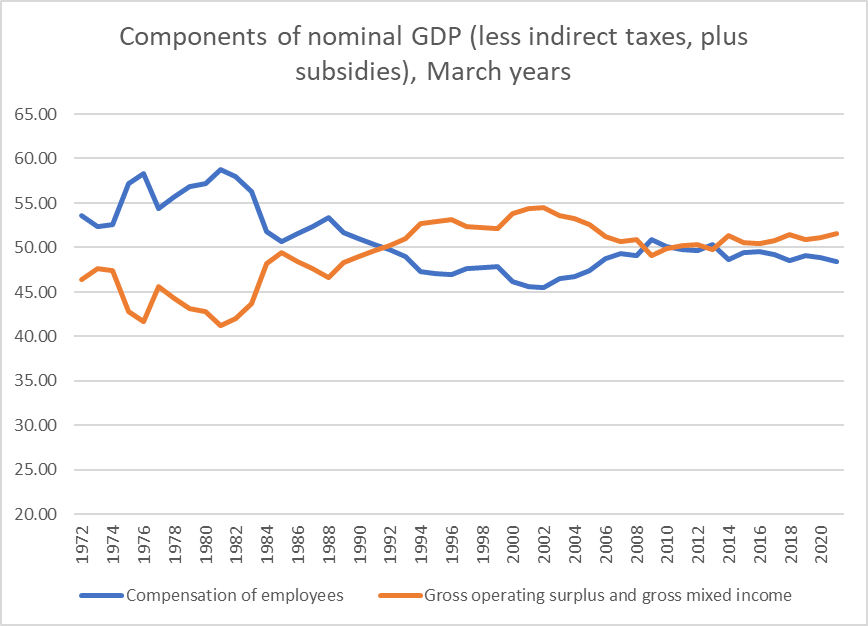

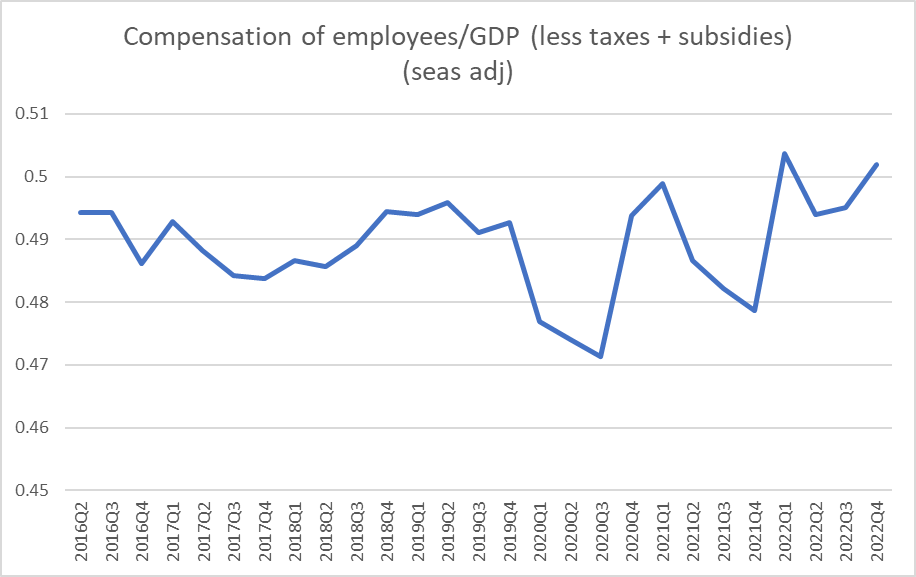

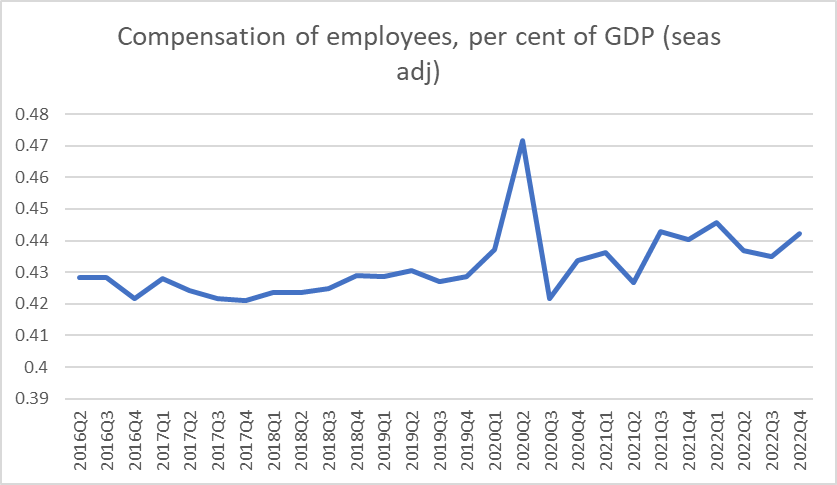

One of the gaps in New Zealand’s macroeconomic data is a full quarterly income measure of GDP. However, SNZ has made steps in that direction in recent years, and we now have a quarterly nominal income measure of GDP and a compensation of employees component of quarterly nominal GDP.

As context, here is the annual data showing both compensation of employees and operating surplus/mixed income up to the year to March 2021

The labour share of GDP (at least the bit going to employees) has fallen a bit in the last decade, but then it has risen a bit more in the previous decade (profits and mixed income share vice versa).

The quarterly data only start in 2016 but are right up to date (December 2022 quarter)

The Covid wage subsidies muddy the picture (sharp shortlived dips in both 2020 and 2021) but over 2022 as a whole the compensation of employees share of (adjusted) nominal GDP was higher than it had been pre-Covid. The picture may be clearer simply as a share of nominal GDP

That isn’t particularly surprising. It isn’t that wage rate growth has run ahead of general inflation or nominal GDP growth, but that the number of people employed, the number of jobs, has increased very rapidly, and the labour market has been running very tight (really on whatever measure you choose to look at). As a reminder if the wage share of nominal GDP has risen a bit amid the inflation surge, that means the other components of GDP (profits and mixed income) have…..shrunk a bit as a share of nominal GDP.

None of this to suggest that pro-competition reforms would not be welcome in New Zealand. They would (although in many cases we could expect the Green Party to oppose them), but the presence or absence of such restrictions is unlikely to materially explain developments in inflation of the scale we – and many other countries, many with more liberal competitive markets – have experienced in the last couple of years. Prima facie, responsibility still looks to rest – as it usually does when such things happen – with monetary policy, either having actively poured fuel on the fire, or (more usually) not having recognised and responded to emerging demand-led inflation anywhere early or aggressively enough.

Readers might also find useful a new column on The Conversation by a professor of economics at Waikato. He puts more weight on that brief Treasury analysis than I did (see previous post), but ends up in a very similar place.

Occam’s razor isn’t always the most useful approach, but when one has had highly expansionary monetary and fiscal policy and have had unprecedentedly low unemployment rates (and general difficulties finding staff), the onus would appear to be on those who want to explain anything very much of New Zealand’s core inflation (in particular) by factors other than the conventional macroeconomic ones. Harris’s column doesn’t credibly make such a case, or point to other New Zealand specific work that does. But, yes, in demand-led booms (especially the early stages) profits will tend to be strong. That doesn’t shift the responsibility off central banks, any more than would be the case when there is a surge of wage inflation, again reflecting unsustainable excess demand for labour.

UPDATE:

To be clear, I am not (repeat, not) suggesting that all of the rise in company tax revenues in the year to March 2022, as cited by Miller, was simply a reversal of the fall in the previous year. About half of it was (company tax revenue was down 17% in the previous 12 month period). My wider point that is an unexpected surge in demand – and it was totally unexpected by macro forecasters – will show up first in profit growth.

As a grossly oversimplified illustration: the local fish and chip shop might have half a dozen staff rostered on on a Friday night. If a lot more people turn up than usual for a Friday night, (not only will wait times be longer but) profits for the day will rise a lot. Wage costs won’t have changed – rosters and wage rates were set in advance – rent won’t change, lighting costs won’t change, but there will be an increase in the cost of goods sold (materials – fish, chips, perhaps oil). If demand remains stronger for longer, you might expect more people to be rostered on, perhaps their wage rates to rise, and so on. Revealed preference suggests workers generally prefer to shift short-term risks – upside and downside – onto firms, and profits will fluctuate accordingly.

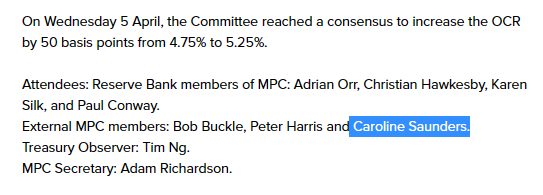

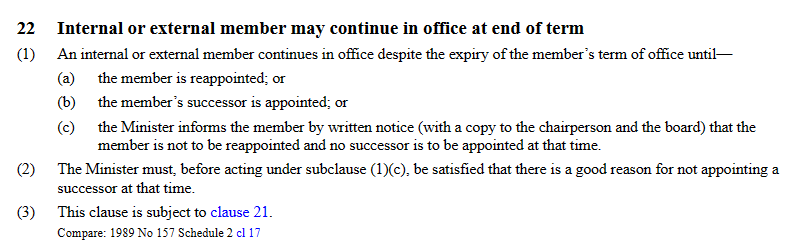

There was a mistake in Monday’s post about the Reserve Bank’s MPC external member Caroline Saunders’ term (and I am grateful to Brad Olsen of Infometrics, on Twitter, for pointing me back in the right direction).

Saunders’ 4 year term, from 1 April 2019, expired last Friday. She is eligible to be appointed for one more term (the law sensibly limits external members to no more than two four-year terms) but she has not, it appears, been reappointed (by contrast, the other two externals were reappointed when their first terms expired this time last year).

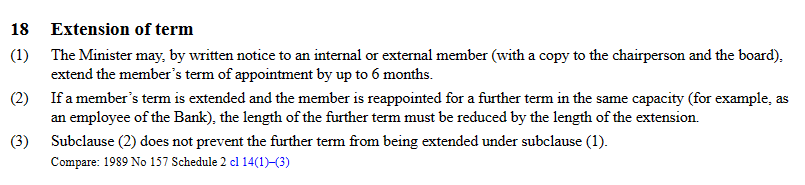

As I noted in Monday’s post, the Minister of Finance has the ability to extend the term of an MPC member (each of the clauses referred to here are from Schedule 3 of the Reserve Bank Act)

Any such extension to a first term sensibly counts against the total time a member can be appointed to a second term for (so extensions can’t be used to lengthen the total time a first term MPC member is appointed for).

Any such extension has to be notified in the Gazetteand given the significance of the MPC you might expect either or both the Reserve Bank and the Minister to put out a press release informing people, including markets, of any such extension.

The extension provisions make a lot of sense in principle, especially when elections roll round quite frequently and the convention is that new permanent appointments should not be made close to, or to commence even after the time of the election. (Interestingly, given that MPC members can only be people nominated by the Bank’s Board, there seems to be no requirement for the Minister to consult the Board – perhaps reasonable since only a maximum of a six month extension seems to be envisaged.)

There is no sign that Saunders’ term has been officially extended either (I checked again just now and there is still no mention of an extension on the Bank’s page detailing all the MPC members and their terms).

And so I assumed that Saunders would not be able to participate in yesterday’s OCR decision. And that is where I was wrong. She could, and she did. On did

And on could

In other words, having put in the law an explicit provision for formal notified (ie transparent) temporary extensions, deliberately designed not to add to the total term if the member is latter formally reappointed, they also slipped in a clause a bit further down the Schedule that lets the Minister of Finance leave in place any MPC member indefinitely (in the case of internal members only as long as they remain Reserve Bank employees – clause 21), with no formal actions, no consultation with the Board, no transparency, and at best greatly diminished accountability. It seriously undermines the idea of fixed terms or term limits (both of which were sensible innovations adopted by this very same Minister of Finance). It is also corrodes the role of the Board – not something I’m opposed to either in principle or (with current membership) in practice, but it was this Minister who decided to retain the central role of the Board in determining membership of the MPC.

There is simply no need for this provision once a formal temporary extension provision was in place, and its use undermines just a bit more any confidence in the MPC regime.

A fair bit of the way the New Zealand MPC model was designed (strengths and weaknesses) was taken from the Bank of England model. That isn’t too surprising and the Bank of England model is, I think, generally regarded as one of the better models around (the main weakness in it, replicated here, is the in-built majority for Bank of England staff, although the appointment processes in the UK mean that is less troublesome and risky than here). But the Reserve Bank version – law and practice – is a pale shadow of the British model, from designers who liked the form of the Bank of England and the substance of the RBA.

Recall that the Governor, Board chair and Minister here have got together to blackball as potential externals anyone with current or potential future research and analytical excellence in macroeconomics and monetary policy.

Recall too the practice under which the externals neither record their views in the minutes nor – except on the rarest, hardly seen at all, occasion – give speeches or interviews.

By contrast the Bank of England has had many able, informed, energetic, active, and open expert external MPC members, whom we hear from.

In the UK, external MPC members front up at the relevant (Treasury) select committee and are expected to answer questions on their views. As importantly, although the select committee has no veto rights, MPC members are expected to appear before the Treasury select committee for a pre-commencement hearing before their term starts. In at least one case such a hearing resulted in an appointee not taking up their position.

In New Zealand, nothing is heard at all from these not-very-expert – in one case appointed mostly because of her sex – external members at any point ever. We know nothing of their views, nothing of their contribution, little or nothing of their capability for and in the role. And whereas the UK goes through a pretty open selection process, with the Chancellor advised by The Treasury making the final calls, in New Zealand there is little sign Treasury has any substantive involvement (OIA evidence suggested none when reappointments were done last year) and the formal power largely rests with the Reserve Bank Board – a bunch of lightweight non-experts apparently appointed mostly to meet diversity criteria.

But at least, or so it appeared, when their term was up they’d be gone – or formally reappointed with appropriate paper trail. After eight years at worst, we could be sure they were gone (unless, say, promoted to Governor). That is how the UK legislation works.

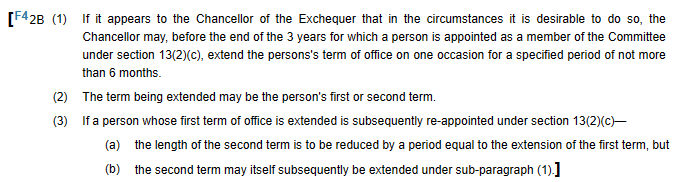

From the relevant schedule of the Bank of England Act 1998

In the UK, members are limited to two three year terms. I don’t have too much problem with New Zealand’s two four-year terms approach – at least if we were going to have actual expert external MPC members – given the smaller pool of potential people here (although three year terms here would minimise election year reappointment issues).

Note also that in the UK legislation – clearly the model for New Zealand – the Chancellor is explicitly restricted to extending a term for a particular individual only once. That seems a prudent restriction – otherwise the Chancellor could extend a person indefinitely (six months at a time, all the while holding a whip hand over the individual to vote the way the Chancellor might prefer). But that restriction has not been carried over to the New Zealand law (see above), and one is left wondering if read strictly the New Zealand law may actually allow repeated six month extensions, I’m no lawyer, but might a court interpreting the New Zealand law look to the UK model and suggest that ministers and Parliament made a conscious choice not to impose such a prudent restraint?

And there is no suggestion anywhere else in the Schedule that any member can just remain in office indefinitely so long as the Chancellor does nothing. As you would expect, because in a well-run system there is no need – officials and ministers get on with making permanent appointments and if for some rare reason, eg election timing, it isn’t appropriate or possible to make an appointment immediately there is a tightly-limited and transparent provision for one time-limited extension.

It isn’t clear what was going on here when the law was drafted. Was it an oversight to have both formal and transparent time-limited extension provisions and a default non-transparent indefinite right to remain provisions. Perhaps, but if it was a deliberate choice, what possible good reason did the Minister and his advisers have?

It also isn’t clear quite what is going on now. There is no obvious reason why a proper appointment – or reappointment of Saunders – could not have been made (they managed it last year). There is no obvious reason why, if some spanner got in the bureaucratic works, Saunders could not have been formally extended for six months (it is entirely in the Minister’s power). And there is no evident reason for letting her simply remain indefinitely, with no notice or transparency (and it seems particularly odd in the current context, drifting ever closer to a tight election where the Minister may lose his ability to appoint a permanent MPC member). There must be an answer – for a position involving on paper a major macro policy decisionmaker at a time when monetary policy is rightly under a lot of scrutiny – but none of the public are favoured with the facts.

(I idly speculated that perhaps there had been some run-in with the Minister’s appointees on the Board. Perhaps they want someone, or some type (race/sex/whatever) of person, and the Minister doesn’t? But even if there was something to that there is still nothing to stop the Minster having given Saunders a formal extension for up to six months.)

Neither the law nor the practice are very satisfactory at all. This MPC member has exercised considerable power (at least on paper) through several years of serious monetary policy mistakes, and not only has there been no public or parliamentary accountability at all, but now we find that the Minister can, by doing nothing, just leave her in place indefinitely, with no transparency, no accountability, and no end date at all. The same option exists for Peter Harris’s second term which expires on 30 September. There should be some clarity from the Minister as to whether – in view of the proximity then of the election – he proposes to extend Harris (the appropriate option in the circumstances) or simply do nothing and let him stay in office.