A couple of weeks ago I wrote a post on where the Labour Party seemed to be going on monetary policy, informed by Alex Tarrant’s interest.co.nz article on his conversations with Grant Robertson. It all seemed to amount to not very much – wording changes to make explicit an interest in the labour market (employment/unemployment), but without much reason to think it would make much difference to anything of substance. My suggestion was that there was a distinct whiff of virtue-signalling about it. And the sort of change Robertson seemed interested in on the governance front – legislating the position of in-house technocrats – seemed unlikely to be much of a step forward at all.

Last week, interest.co.nz had a piece on the same issues by former Herald economics editor Brian Fallow, also benefiting from an interview with Robertson. Fallow pushes a bit harder. His summary is that

The changes Labour proposes to make to the monetary policy framework sit somewhere between cosmetic and perilous, but closer to the former.

Cosmetic for the sorts of reasons I’ve outlined. On the one hand, the Bank has always taken the labour market into account as one indicator of excess capacity. And on the other hand, plenty of pieces of overseas central banking legislation refer to employment/unemployment somewhere, but there is little evidence that the central banks in those countries have run monetary policy much differently, on average over time, than the Reserve Bank of New Zealand has.

Robertson’s response is pretty underwhelming.

Asked how much difference the regime he advocates would have made, had it been in place in the past, he said, “In the very immediate past, not that much, truthfully. But there have been other times in our history, and there have been other examples around the world, when lower interest rates could have helped to reduce unemployment.”

If he was serious about this making a difference, he’d surely be able to quote chapter and verse. When, where and how does he think it would have made a difference?

He is, however, clearly tantalised by the current situation

Even now, “Are we satisfied as a country that with 3.5% growth 5.2% unemployment is okay?”

Given that the Treasury thinks our NAIRU is nearer 4 per cent, I don’t think we should be content. But Robertson has spent so long over the last few years defending Graeme Wheeler that he can’t quite bring himself, even now, to suggest that monetary policy could have been conducted better in the last five years, whether on the current mandate or something a little different.

If the proposed change isn’t cosmetic, Fallow worries that it could be perilous. Why? Because when he pushes Robertson he gets a more explicit – and more concerning – answer than the one Alex Tarrant got.

He has told interest.co.nz’s Alex Tarrant that he was not going to tell the Reserve Bank whether one objective is more important than the other.

Talking to me, however, he said that ultimately the bank would remain independent. “But if unemployment starts to get out of control I would expect in that environment it says ‘At this time we are preferencing that and we are going to lower rates by a greater percentage than we might have’.”

In the event of a stagflation scenario he would expect it to focus more on the falling output and employment side of the dilemma and to ease.

“I think the setting of a clear direction here is what is important.”

In short Robertson seems to be saying that if Parliament were to change the statute, the message to the bank would be when in doubt err on the side of stimulus.

If unemployment is prioritised by the Reserve Bank in such circumstances, it is a recipe for inflation getting away. In the medium-term, monetary policy can really only affect nominal variables (inflation, price level, nominal GDP or whatever), it simply can’t affect real variables. Using monetary policy to pursue such goals directly is a risky prescription. I wouldn’t want to overstate the issue – New Zealand isn’t heading for hyperinflation – but part of reason we and other countries ended up with persistently high inflation in the 1970s is that too much weight was placed on unemployment in setting monetary policy. Getting inflation back down again was costly – including in terms of increased unemployment. On a smaller scale, as Fallow highlights, the desire to “give growth a chance” was part of what was behind the monetary policy misjudgements of 2003 to 2006, when monetary policy wasn’t tight enough.

Robertson’s words suggest he still hasn’t thought the issues through very deeply or carefully. For now, I’m sticking with the “cosmetic” or virtue-signalling interpretation of what Labour is on about. And I’m still uncomfortable at the lack of command of the issues and experience in someone who aspires to be Minister of Finance later this year.

But yesterday, a mainstream economist came out in support of more or less the direction Robertson is proposing. In his youth Peter Redward spent a few years at the Reserve Bank, and then spent time in various roles, including at Barclays and Deutsche Bank, before returning to New Zealand and establishing his own economic and financial markets advisory firm. He focuses on emerging Asian foreign exchange markets, but keeps a keen eye on monetary policy developments in New Zealand.

In his short piece at Newsroom, Peter Redward says It’s time for a Reserve Bank change. He notes of the last few years that

Whether Governor Wheeler consciously aimed for a hawkish interpretation of the Act, or not, we may never know. But hawkish he’s been, leading to tighter monetary conditions than were necessary, boosting the New Zealand dollar and confining thousands of New Zealanders to needless unemployment.

And argues that

…maybe it’s time to adopt a dual mandate in the Act. One possibility is the dual mandate of the U.S. Federal Reserve. The Federal Reserve has a two percent inflation target but it also targets ‘maximum employment’. Economists have differing interpretations of ‘maximum employment’ so it acts as a constraint, and that’s the point.

While no one knows exactly where ‘maximum employment’ in New Zealand is, I believe most economists would agree that it’s likely to be consistent with an unemployment rate somewhere around 4.5 percent (give or take 0.25 percent). If the Reserve Bank had a dual mandate, its elevated level would have acted to constrain the bank’s aborted tightening of policy in 2009 and 2014.

I’m very sympathetic to his critique of Graeme Wheeler’s stewardship of monetary policy, and highlighted in numerous of my own commentaries, after it became apparent that the 2014 OCR increases had been an unnecessary mistake, the Governor’s apparent indifference to an unemployment rate that remained well above any estimates of a NAIRU.

But I remain a bit more sceptical than Peter appears to be about how much difference a re-specified mandate might have made. As I’ve argued before, past Reserve Bank research suggests that faced with the sorts of shocks New Zealand experienced, policymakers at the Fed, the RBA and the Bank of Canada would have responded much the same way as the Reserve Bank of New Zealand did. That work was done for periods prior to 2008/09 – for most of the time since then the Fed was at or very near the lower bound on interest rates, so the game was a bit different – but it isn’t clear that the specification of the target has been the problem in New Zealand in the last few years. After all, simply on inflation grounds alone the Reserve Bank hasn’t done well.

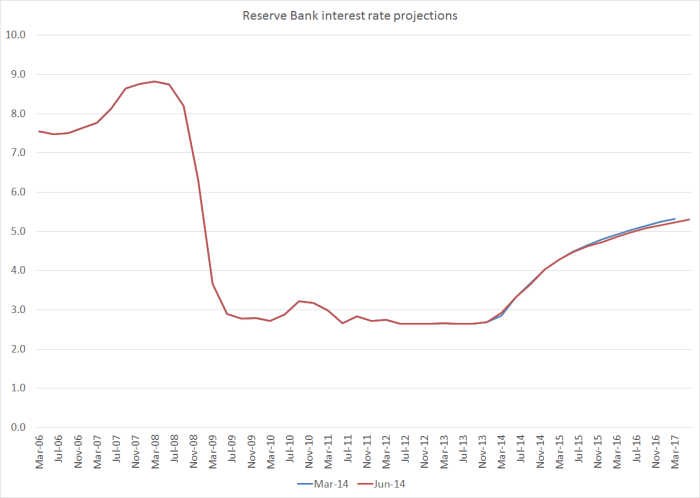

Here is a chart of the Reserve Bank’s unemployment rate projections from the March 2014 MPS, the occasion when they started raising the OCR.

The second observation is the last actual data they had – the unemployment rate for the December 2013 quarter. So when they started the tightening cycle they thought the unemployment would be falling quite considerably that year, before levelling out around what they thought of as something near what they must have thought of as the practical NAIRU (this was before last year’s revisions to the HLFS which lowered unemployment rates, and NAIRU estimates, for the last few years). The problem then wasn’t that they didn’t care about unemployment, it is that they got their forecasts – particular as regards inflation – badly wrong. It isn’t clear why a different target specification would have altered the policy judgement at the time.

Perhaps it would have done so once it became apparent that the OCR increases hadn’t really been necessary, but a stubborn refusal by the Governor to concede mistakes, even with hindsight, plus a mindset firmly focused on how “extraordinarily stimulatory” monetary policy allegedly was – when no one had any real idea what a neutral interest rate might be in the current environment, and when inflation stubbornly didn’t rise much if at all – seem more likely explanations. The Bank kept forecasting that inflation would rise and unemployment would fall – the jointly desired outcomes.

(And if one looks at the Bank’s forecasts in mid 2010, when they made the previous unnecessary start on tightening, one gets much the same picture – forecasts of falling unemployment and rising inflation, that simply didn’t happen.)

So why should we supposed that a different specification of the target would have made much difference to how policy was set? We had an institution that was misreading things, in a political climate where no one seemed much bothered by the unemployment rate holding up, and where for a long time financial markets endorsed the approach taken by the Reserve Bank (often more enthusiastic for future tightenings than even the Governor and his advisers were). Getting something closer to the right model of the world (for the times), and quickly learning from one’s mis-steps, seem likely to matter more than the words of the Act in this area.

As I’ve said repeatedly here, I’m not firmly opposed to amending the relevant clauses of the Reserve Bank Act to mention the desirability of things like a low unemployment rate. But even the Federal Reserve Act makes clear that good monetary policy focused on a nominal target creates a climate consistent with high employment. High employment isn’t a goal for the Federal Reserve is supposed to pursue directly, even if – all else equal – a high unemployment rate relative to an (uncertain) NAIRU is a useful indicator that something might be wrong with monetary policy settings. It isn’t clear there is anything much to gain from such amendments – or that they are where the real issues regarding the Reserve Bank are – but sometimes perhaps virtue needs to be signalled? My own concrete suggestion in this area would be to require the Reserve Bank to publish, every six months, its own estimates of the NAIRU and to explain the reasons for the deviations of actual unemployment from the NAIRU, how quickly that gap could be expected to close, and the contribution of monetary policy to the evolution of the gap.

Brian Fallow’s article suggested that Labour still hasn’t settled on how to reform the governance of the Reserve Bank.

Robertson is non-committal at this stage on the composition of a monetary policy committee to take interest rate decisions, including to what extent it should include members from outside the bank.

Peter Redward has a more specific proposal for him.

What’s needed is a formal Monetary Board complete with published minutes and, released after a grace period, transcripts of the meeting and the voting record of members. In a recent speech, U.S. Federal Reserve Vice Chair, Stanley Fischer, argued that this arrangement is superior to the sole responsibility model in achieving outcomes and accountability. Changes to the role and responsibility of the Governor will necessitate changes to the structure of the Reserve Bank Board. Best practice would suggest that a Monetary Board should be created to set monetary policy with the Reserve Bank Board selecting candidates for the committee while maintaining oversight of the bank. To ensure that external board members are not simply captured by the bank it may be necessary to provide a secretariat similar to the Fonterra Shareholder’s Council, operated at arms-length from bank management.

It isn’t my favoured model, but it would be a considerable step in the right direction, and far superior – in terms of heightened accountability and good governance of a powerful government agency – to Graeme Wheeler’s preference to legislate his own internal committee. The biggest problem I see with the Redward proposal, is that it has too much of a democratic deficit. Monetary policy decisionmakers shouldn’t be appointed by other unelected people – the Reserve Bank Board – but by people (the Minister of Finance and his Cabinet colleagues) whom we the voters can toss out. That is how it is pretty much everywhere else.

Peter’s proposal focuses on monetary policy. But, of course, the Reserve Bank has much wider policy responsibilities, including a lot of discretionary power – not constrained by anything like the PTA – in the area of financial regulation. I presume he would also favour committee decisionmaking for those functions. I’ve proposed two committees – a Monetary Policy Committee and a Prudential Policy Committee, each appointed by the Minister of Finance, with a majority of non-executive members, and with each member subject to parliamentary confirmation hearings (although not parliamentary veto). It is a very similar model to that put in place in the United Kingdom in the last few years. It puts much less reliance on one person – who will sometimes be exceptional, and occasionally really bad, but on average will be about average – and would be more in step with the way in which other countries govern these sorts of functions, and with the way we govern other New Zealand public sector agencies. I hope the Labour Party is giving serious thought to these sorts of options, and while the headline interest is often in monetary policy, the governance of the financial regulatory powers is at least as important to get right.

And then of course, getting a good Governor will always matter a lot. The Governor, as chief executive, will set the tone within the organisation, and determine what behaviours are rewarded and which are frowned on or penalised. If the Reserve Bank failed over the last few years, it wasn’t just because Graeme Wheeler was the sole monetary policy decisionmaker – his advisers mostly seemed to agree with him – but because of the sort of organisation he fostered, where “getting with the agenda” seemed more important and more valued than dissent or challenge, in area where few people know anything much with a very high degree of confidence. Character and judgement are probably, at the margin, more important than high level technical expertise.

And while people are thinking about reforms to the Reserve Bank Act don’t lose sight of how little accountability and control there is over the Reserve Bank’s use of public money, or about the provisions it has carved out for itself from the Official Information Act which allow it to keep secret submissions on major policy proposals even – perhaps even especially – when they come from parties who would be affected by those proposals.

Revising the Reserve Bank Act was the first legislative priority for the first Labour government that took office in 1935. I’m not suggesting the same priority if there is a new Labour-led government later in the year, but there is a real and substantial agenda of reforms to address, which will take time to get right, and which take on some added urgency in view of the vacancy in the office of the Governor that needs to be filled by next March. That appointment – a key step in the reform and revitalisation of the Reserve Bank – should be led by whoever is Minister of Finance, not by the faceless (and unaccountable) men and women of the Reserve Bank’s Board, the people who have presided complacently over the mis-steps of the last few years.