I’ve written a couple of times about the review former State Services Commissioner Iain Rennie has been conducting, at the request of the Minister of Finance, into two aspects of the governance of the Reserve Bank:

- whether something like the existing internal committee in which the Governor makes his OCR decisions should be formalised in legislation, and

- whether the Reserve Bank should remain the “owner” of the various pieces of legislation (RB Act, as well as the insurance and non-bank legislation) it operates under.

An earlier OIA request from a journalist saw The Treasury refuse to release the terms of reference for the report, but they did release the terms of engagement. I wrote about that here. We learned from that release that the report had been delivered to Treasury in mid-April. We also learned that

In completing the work, the author will engage with an agreed set of domestic and international experts.

and

The key deliverable is a report, which will be peer reviewed by a panel of international experts.

I was interested to know who these experts were, and lodged an OIA request with Treasury. No doubt, they could readily have responded in a day or so, but after four weeks they did finally respond yesterday.

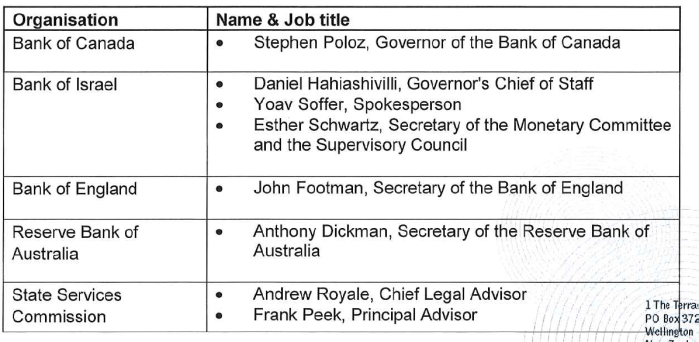

Anyway, this was the list of “agreed domestic and international experts”.

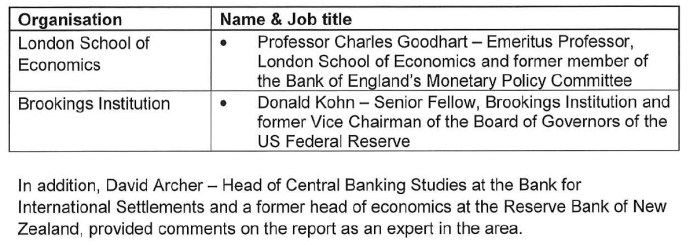

and this was the list of reviewers

It is a curious list in many ways. Setting aside the SSC people, of whom I know nothing but who are presumably knowledgeable on issues of governance of New Zealand public sector institutions, not a single one of the central bank experts (first list) has any experience of, or exposure to New Zealand (let alone actually being a New Zealander).

And Rennie, with Treasury’s agreement, appears to have consulted only current serving central bankers. No doubt several will have had useful perspectives to offer on their own central banks’ experiences. But the world of central bankers is a fairly clubby (or collegial) one, and you would have to think it unlikely that Rennie would have heard anything from these people that would cast doubt on how the arrangements their New Zealand peers operated under were working. And among those current central bankers only one (Poloz, the Canadian Governor) has any stature in his own right; the others appear to be “corporate bureaucrats”, able no doubt to pass on information about how things work in their own central banks, but not self-evidently qualifying as “international experts” on central bank governance etc.

One might have supposed that any number of other people (even from abroad) could have provided valuable perspectives and insights. For example, retired Governors and former members of decisionmaking committees, who are freer to speak their mind. Lars Svensson, the leading academic and former monetary policy board member, wrote a review of our Reserve Bank in 2001 for our then-government. Having had extensive experience as an insider since then, and retaining an interest in New Zealand, he would have seemed like a natural person for Rennie to have consulted. In fact, there is not one academic on the list. Not, for example, Alan Blinder, former vice-chair of the Fed and author of academic work on decisionmaking by committee. There are no private economists on the list. Not, for example, Willem Buiter now chief economist of Citibank and a former academic and member of the Bank of England’s Monetary Policy Committee. And no one from abroad with, say, a Treasury perspective, or the perspective of a Minister. Bernie Fraser, for example, had been both Governor of the Reserve Bank of Australia, and Secretary to the (Australian) Treasury.

And not a single person from New Zealand made the expert list? Not Arthur Grimes, who was heavily involved in the design of the current system and later chair of the Reserve Bank Board. Not Don Brash, who was Governor under the current system for 12 years. Not thoughtful former Board members such as (for example) Hugh Fletcher. Not people who had been involved from a Treasury perspective (especially in the years since Rennie himself left Treasury). And, of course, no one who has written on the issues domestically.

You might, incidentally, be wondering why people from the Bank of Canada and the Bank of Israel top the list of experts. That is likely to be because Canada is the only other advanced country central bank with the Governor as (formally) single decisionmaker (Canada has quite old central banking legislation, and the Bank of Canada has much narrower responsibilities than our Reserve Bank). And until relatively recently, Israel also had the Governor as a single decisionmaker, before the legislation was overhauled and a mixed committee (internals and externals) took over the monetary policy decisionmaking role. The Israeli experience should be interesting, but again you have to wonder why Rennie didn’t consult Stan Fischer, former Governor of the Bank of Israel, and now vice-chair of the Federal Reserve.

What of the international peer reviewers? There were three, and each will have been likely to have added something in commenting on Rennie’s draft. But, again, there is a distinctly “let’s keep this inside the club” feel to it all. Goodhart, for example, is a respected academic economist, and former staff member and Monetary Policy Committee member at the Bank of England. But he is now rather elderly, and has had a very strong relationship with the Reserve Bank of New Zealand over the years – including as guest speaker at the (rather extravagant) 50th anniversary celebrations of the Bank, and then someone used as an expert witness by the Bank at the parliamentary select committee when the current Reserve Bank Act – governance and all – was being legislated (rather controversially) in 1989.

Donald Kohn is pretty highly-respected in international central banking circles. So much so that Treasury omit to note in their description that, having retired from a career at the Federal Reserve, he is now a member of the Bank of England Financial Policy Committee, so still entirely within the central banking club. He has visited the Reserve Bank and, from memory, wrote up his experiences pretty positively.

The final reviewer is David Archer, former Assistant Governor and Head of Economics at the Reserve Bank (and sometimes mentioned on lists of potential future Governors). He now holds a senior position at the Bank for International Settlements, a body owned by central banks (including ours) which describes itself thus

The mission of the BIS is to serve central banks in their pursuit of monetary and financial stability, to foster international cooperation in those areas and to act as a bank for central banks.

I worked with David closely over a long period, and he was usually pretty willing to speak his mind. He certainly knew the Reserve Bank well – at least in the days before financial regulation became so important, and before the Reserve Bank moved more back into the mainstream of central government as a major regulatory institution – but you have to wonder quite how free he will have felt to offer views the Reserve Bank might be uncomfortable with – the Governor visits the BIS pretty frequently – especially as those views will themselves presumably be discoverable in time.

So the offshore people consulted, or used as reviewers, seem as though they will have been a rather partial perspective on the issues at hand. No doubt, all provided some useful information and perspectives, but you can’t help thinking there could have been a lot more there if Rennie had sought it. Then again, as State Services Commissioner his reputation was hardly that of someone keen on open government. What is perhaps more troubling is that The Treasury was okay with all this.

Despite this published list, you have to wonder who else Rennie in fact consulted. Why I do suppose there was anyone else? Because, somewhat by chance, I also yesterday got a response from the Reserve Bank to an Official Information Act request for minutes of the Reserve Bank Board.

In the minutes of the Board meeting held on 30 March this appears

There follows almost three pages recording the details of the Board’s discussion with Rennie (and his supporting Treasury staff). every single word withheld (on somewhat questionable grounds). Nothing else ever gets three pages of text in the Board minutes – in fact, the process for appointing a new Governor is still not being minuted at all, even in this latest set of releases.

I don’t have any particular problem with Rennie consulting with the Bank’s Board. They are likely to have some useful experiential perspectives to offer, but if the discussion covered almost three pages of minutes and – according to Treasury – no one else in New Zealand with any familiarity with central banking issues was consulted, it does all have the feel of an insiders’ job. Perhaps that is what Steven Joyce wanted. It isn’t what the situation requires. Meanwhile, one can only hope that the report itself, along with the terms of reference, will be released before too long.

New Zealand isn’t the only country looking at these issues. The Norwegian government just this week released an independent report they had commissioned looking at the future governance and mandate of their own central bank. The summary report is very easy to read, and includes specific draft amendments to the law to give effect to the report’s recommendations. Among those recommendations is a streamlined system of governance, with proposals for a monetary policy committee (40 per cent of whose members would be externals appointed by the government), and for a separate Board to which the Governor would be responsible in his role as chief executive of the Bank. We can only hope that the completed Rennie report will be as clear and crisp.

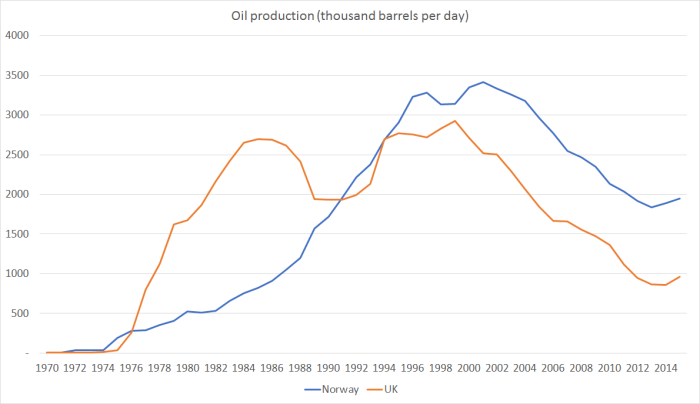

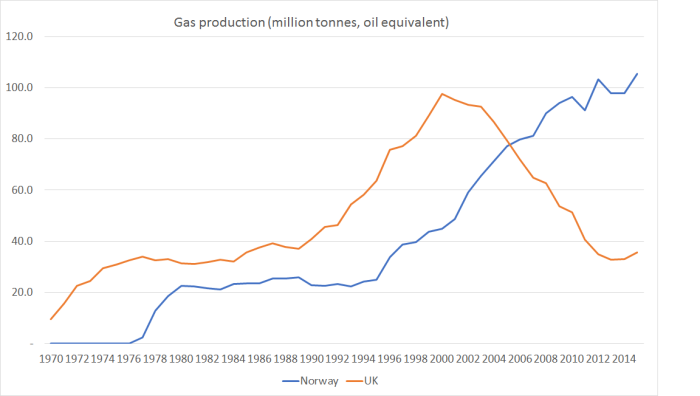

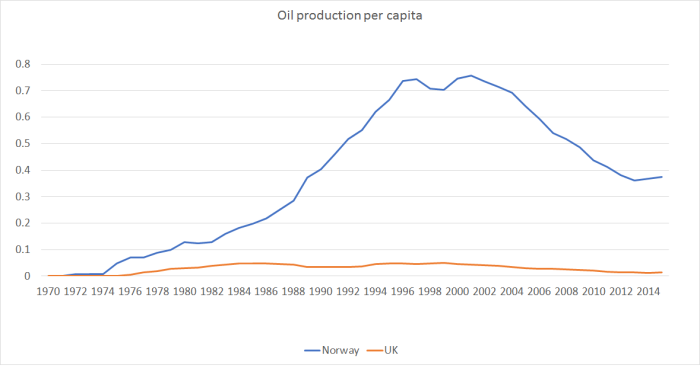

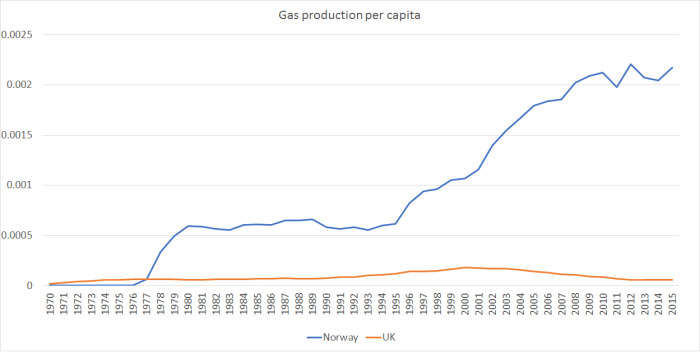

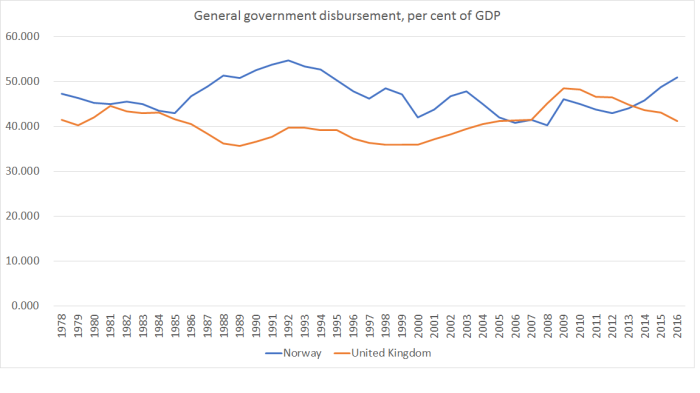

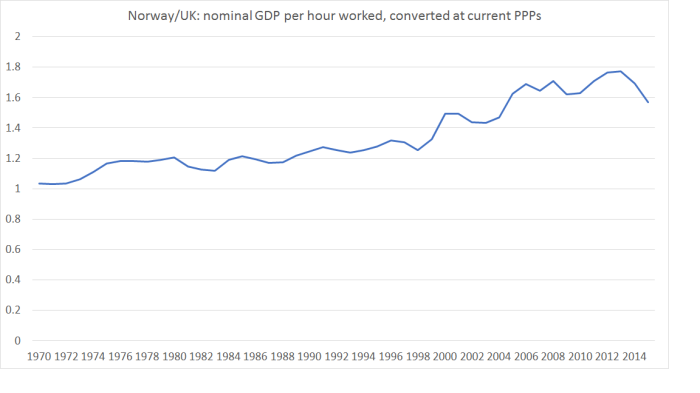

These days, by contrast, GDP per hour worked in Norway is around 60 per cent higher than that in the UK (which is in turn quite a bit higher than New Zealand’s). Norway has among the very highest material living standards of OECD countries, and the UK is still in the middle of the pack.

These days, by contrast, GDP per hour worked in Norway is around 60 per cent higher than that in the UK (which is in turn quite a bit higher than New Zealand’s). Norway has among the very highest material living standards of OECD countries, and the UK is still in the middle of the pack.