It was a poor package. On so many counts. And my sense of that has only strengthened overnight. Perhaps at best one might label it as a curate’s egg – and rather more in the original meaning than the colloquial one.

It had the feel of a package that started as one thing, perhaps relatively small, two or three weeks ago when the government was still focused on the coronavirus as a China issue – things that had happened, but which would now gradually if slowly sort themselves out – and on the small range of sectors materially directly affected by the China experience. They were backward looking, and they refused to face up to what was clearly coming – and it was as clear as day at least a week ago. So then rushed changes were made to the package on the fly, including efforts to bulk it up to look enormous – presumably solely for political reasons – regardless of whether the components were relevant at all to the times or to the specific needs in responding to the situation that is upon us. And at the same time, whether because they were caught by the momentum of their own process, or because they are still reluctant to front the severity of what awaits us, most of the really pressing issues were barely even addressed.

The government then has the gall to talk of a new round of measures in the Budget – two months away – allegedly to be focused on the recovery phase. There is (a) absolutely no way they can wait until the Budget to do a lot more, and (b) the recovery phase is much more likely to be something to think about in next year’s Budget. Remember the comments from Prof Michael Baker reported in the Herald a day or so ago: anyone who thinks this will be over by Christmas hasn’t thought hard enough. Or, as he went on to rephrase, perhaps Christmas 2021.

I want to focus mostly on the economics, but the politicisation by the government was also unfortunate. Crisis times, all in this together etc. But there were the silly boasts that somehow this package was bigger than was done in 2008/09 – which is true but irrelevant since (a) this is quite different sort of shock, (b) there was huge fiscal stimulus already put in place in the 2008 Budget, oblivious to what was just about to break, and (c) there was room for 575 basis points of interest rate cuts (and the exchange rate fell sharply). There was, in fact, no discretionary fiscal stimulus in New Zealand during the recession itself: it wasn’t needed. Then there were the attempts to wrap themselves in the cloak of Michael Joseph Savage – Labour’s icon – in “responding to the Great Depression”. At least some of them are presumably historically literate enough to know that Savage didn’t take office until the worst of the Depression in New Zealand was long past and recovery was well underway. Or the silly attempts to boast that their package was bigger than some others when (a) as we shall see, for coronavirus purposes a lot of their numbers were simply irrelevant, and (b) the scale of interventions globally is rising by the day (those other packages were last week’s news). It isn’t exactly confidence-inspriring re the seriousness of the Prime Minister’s leadership in a crisis when she goes on TV to claim this would be the biggest package she announced, and then it becomes very evident that the numbers were simply cobbled together in a way that produces just barely that result – headline-grabbing rather than substantive policy.

What would have been much more welcome was evidence that the Minister and Prime Minister clearly understood what was going on, what the key issues were, what the relevant horizons were, and so on. But there was little or none of that.

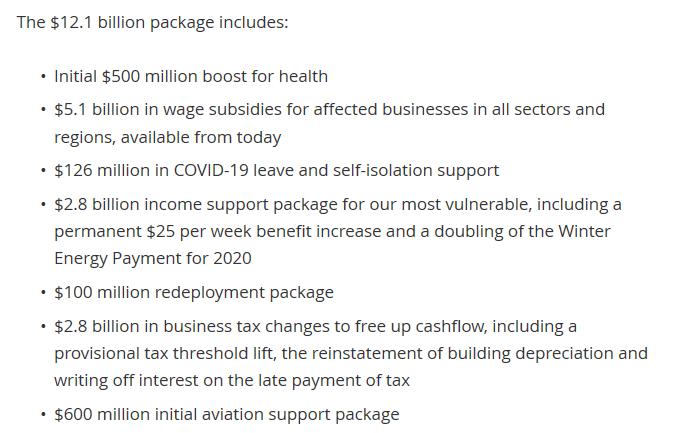

To get specific, this is the table summarising the package

We’ll get the easy bits out of the way first. No one is going to argue with more resources going to health, although (a) some have asked why it wasn’t more (is that really all the sector can really use if we face 18 months of suppression strategies?), and (b) why this hadn’t been done at least six weeks ago.

And there probably isn’t much to quibble about (at least for now) re the sick leave and self-isolation support.

I didn’t see any details of the “redeployment package” although in his speech Robertson did make some comments, including mention of a package for Gisborne to be announced in the next few days. I guess the amounts are small, but mostly it seems to be a waste of time – most likely before long hardly anyone (well apart from the health system and a few online retailers) will be taking on any new staff, and that could be the case for many months. Face to face training doesn’t seem likely either. It looks like just a legacy of where the package began weeks ago.

There is nothing to say about the “initial aviation support package” because they’ve said nothing about it, except that it apparently doesn’t include an Air New Zealand bailout. Other than that, it isn’t entirely clear why this line item exists in the package, but I guess it bulked out the headline number.

And then we started getting to the big bucks. Unfortunately, many of the big bucks are scheduled to be spent in several years time, and have nothing whatever to do with the coronavirus, whether stabilisation or recovery. Because the thing that doesn’t get much attention in public consciousness is that the $12.1 billion number is total additional spending over four fiscal years. That is an approach that makes sense in normal times (recognises the ongoing implications of new commitments) but it bears no relationship to the support provided for the coronavirus situation this year.

Thus, the business tax reforms they announced seem generally sensible. I’ve argued against the previous government’s abolition of depreciation on buildings ever since the National Party adopted the policy in 2010. It was daft and without any good economic foundation, so I’m really glad to see it being scrapped. Probably this was planned for this year’s Budget anyway (I hope so). But it has nothing whatever to do with coronavirus, with stabilisation, or even with recovery. And the bulk of the spend will be in future years. It is simply in here to (a) bulk up the numbers, and (b) as some sort of political counterpoint to the next item, welfare benefits.

Raising welfare benefits permanently also has nothing to do with coronavirus. Again most of the spending (at least $1.8 billion of it) won’t even be in the March 2021 fiscal year, and of the remaining billion probably only $700 million will be paid out in the next six months (largely the “winter energy payment”). Raising welfare benefits permanently has long been a cause of the Green Party and probably much of the Labour Party. There is talk that this too was going to feature in the (election-year) Budget. If so, it is just in this package to (again) bulk out the headline number.

But the increase in welfare benefits now is much more pernicious than that. Life on a benefit isn’t easy (and before anyone scoffs about what do I know, that isn’t just rhetoric: I have a close family member living on a long term benefit). But what beneficiaries at least had going for them this year was certainty of income: the government was not going to default or closedown, unlike many private sector employers (with the best will in the world on their part). They and public servants were safe. And yet the government chooses to lock-in a permanent boost to its spending commitments (a) to those with the least degree of income uncertainty now, and (b) when the country is in the process of becoming a lot poorer and scarce resources need to be used wisely. Raising benefits might or might not have been a reasonable luxury in settled times. It is simply irresponsible and evidence of fundamental unseriousness to do so now. (And before anyone tells me about the high marginal propensity to consume that beneficiaries have, let me remind you that now is not the time for stimulus or encouraging people to spend more: instead we are entering a phase of deliberately choosing to shrink the economy to give us the best hope of fighting of the effects of the virus). Oh, and the unemployment rate is going to rise a lot, and one of the big challenges after this is all over is going to be reconnecting people with the labour market, at a time when wage inflation will have been depressed anyway. In that context, higher benefit replacement rates (relative to wages) is really the last thing that makes sense in getting the economy back on track.

All of which leaves us with the centrepiece of the strategy, the wage subsidy scheme. It is probably reasonable enough as far as it goes, but “as far it goes” is no more than a very short-term holding action, not remotely enough to really address much at all (it runs til June, the crisis will not, banks (for example) and other creditors will know that. So, before long, will most households).

But again there is a strong suspicion of political vapourware in the numbers. The scheme is estimated to pay out $5.1 billion in the next three months. That is a lot of money.

It is paid out at a rate of $7029.60 per full-time employee. That means they expect to pay out for about 725000 fulltime equivalent employees (there is a lower rate for part-time employees). That sounds like a lot.

In the latest HLFS, there were 2.6 million employees in total (including the self-employed). Of them 2.1 million were fulltime. Applying the same ratio the package does (part-time staff are paid for at 60 per cent of the fulltime rate) to the 519000 part-time staff produces a full-time equivalent number of employees of 2.44 million. In other words, the headline budget figure is premised on paying out in respect of 30 per cent of all employees in the coming quarter. And this is even though the payment is capped at $150000 per employer, equivalent to compensating for only up to 21 staff. And you can only get the payment is your monthly revenue is down 30 per cent year on year

Now, sure, there are lots (and lots) of businesses with fewer than 21 staff. But lots of employees (by number) work for big organisations, both in the public and private sectors. All those universities who were moaning about foreign students a few weeks ago could only each get $150000 (if total revenue had even fallen 30 per cent) even though they employ thousands of people each.

I am not saying that the $5.1 billion total is impossible. But it seems unlikely. And in particular it seems inconsistent with (a) the political messaging about the severity of the economic shakeout (even yesterday the Minister still wouldn’t accept that a recession was a done deal), and (b) the preliminary Treasury forecast the Minister was happy to wave around suggesting that at worst we’d have only about a 3 per cent fall in GDP.

I reckon I have been consistently one of the most pessimistic commentators about the economic effects. It isn’t that hard to envisage GDP falling 5 per cent in the June quarter alone (reality could be a lot worse than that if suppression really comes to New Zealand), but that isn’t the sort of message the government is giving New Zealanders. Either they aren’t being honest with us, or they’ve just bulked up the headline numbers (it isn’t as if any underlying assumptions about any of the forecasts have been released).

So for all the talk of a 4 per cent of GDP package etc, it would probably be more realistic at this stage to think in terms of immediate additional outlays (next few months) of no more than half that (and not even all that will be helpful). Those are still big numbers: 2 per cent of annual GDP is 5 per cent of four months’ GDP. The Minister released a chart suggesting the package will boost annual GDP itself by 2 per cent over the next year, but that too seems optimistic (but hard to tell how much without Treasury releasing their assumptions/workings).

But for whatever immediate good some elements of the package might do, it still largely fails to address the real and pressing issues. In particular, in typical recession debt service costs for borrowers (new and existing, at least for floating rate borrowers) drop sharply, and returns to depositors drop sharply. That reallocation is a natural and normal part of the rebalancing and stabilisation process. Despite the spin from central bankers (abroad as well as here), 75 points just does not cut it: 500 points has been more like it in recessions (over a period when none has been as bad as what we are facing now). Between a central bank that refuses – adamantly promises – not to cut further, and a failure to ever deal with the lower bound issues, nothing is on the way. That has to change. The government could and should simply insist on it changing now. (Related to this, what fall in the exchange rate we’ve seen – also a natural part of shock absorption – is tiny compared to the usual recessions.)

And even more pressingly, in this unique sort of shock, the package does nothing about stabilising income expectations for firms or households in a way that would support banks being willing to (a) maintain existing credit exposures, and (b) be willing to significantly extend credit to cover the gaping net revenue holes that will be opening up for many firms (and households). That needs urgent action. With the best will in the world, and much harassment from the Governor and the Minister, banks are businesses too and have shareholders to answer to (primarily) and their own future existence to protect. They can read things like this week’s Imperial College paper arguing that suppression strategies may need to be kept in place for most of the next 18 months. If so, with no income guarantees – and not even any certainty about what subsequent emergence looks like – as a bank you would often be in breach of your duties to extend more debt in many cases. And many people – firms and households – would be reluctant to borrow more. Better to manage and minimise exposures early, to whatever extent one feasibly can.

Of course, governments could lend direct. But that simply isn’t realistic on any sort of scale. Much better to think hard about the sort of idea I advanced in a post on Monday where the government passes emergency legislation guaranteeing – in legally enforceable form (perhaps it could even just be done under the guarantee powers of the Public Finance Act, but better to get parliamentary sanction) – that no firm or household/individual would have net income in 2020/2021 (and perhaps even the following year) less than 80 per cent of that for the last year (for firms, the guarantee would be scaled to the extent they retained staff). Doing so would give a floor – and thus remove much of the variance in expectations – for households, firms, and for actual/potential lenders. It should help underpin a willingness to extend credit. It should also serve as an underpinning if we find ourselves adopting shorter-term expedients – as say France has done – of temporarily suspending utlilities bills or mortgage payments: utility companies could themselves get bridging finance if banks knew household would still have most of their income, and banks themselves wouldn’t face the need to record impaired assets etc.

I want to come back, in a further post, this afternoon to my overall proposed package, including answering some of the questions/objections. I still believe it is the best and fairest approach to take, complementing some of the other shorter-term cash income support measures (which would be nested within the guarantee). But whatever the precise form of what they do, the government simply must act very quickly to ensure that credit is available. (And on that score the Reserve Bank temporary suspension of the scheduled increase in capital requirements is of second order significance, not remotely the main game.

Finally, I can only repeat a point I’ve made in various posts and numerous tweets over the last week: this is not the time for encouraging new private spending. There will come a time for that, and it is likely that fiscal policy will have a significant role to play then. But this is a time when we are deliberately scaling back the economy – quite possibly savagely for months at a time – and discouraging spending in many areas. We need to ensure have the income to live on, but for now much the most important economic priority is some set of guarantees – supported by the strong Crown balance sheet – that means households are able to borrow, existing businesses are able and willing to borrow, and banks are genuinely willing to maintain and increase lending…..in the face of the most hostile and uncertain economic conditions of the lifetimes of almost all of us.

The government now needs to get serious and get down to real economic policy work. It would be also good if they started authoritatively fronting with New Zealanders about just how tough things are going to get. A lot of New Zealanders, who don’t obsessively follow the news or events abroad, really still have little no idea.