The quarterly suite of labour market data came out yesterday, and it wasn’t a case of senior ministers at their most edifying (sadly, it is difficult to imagine things would be any different if the current government and Opposition parties swapped places, but….today’s ministers hold office today).

The one that first caught my eye was this from the Minister of Health

And in the newspaper this morning I see the Minister of Finance running the same line, suggesting that it was “of particular note” that the number of people unemployed was 8000 less than Treasury had forecast in the PREFU (the same source Brown appeared to be drawing from).

One assumes these senior ministers are smart enough not to take these lines substantively seriously. Macroeconomic forecasting two years ahead has always been something of a mug’s game. Some numbers might be needed to drop into spreadsheets – eg for budgeting purposes – but no serious observer ever expresses a great deal of confidence in any specific set of numbers forecast that far ahead. If Treasury got the current unemployment rate right to with 0.2 percentage points two years out one could say “well done them” but it might also suggest a reasonable element of luck. As it happens, on this occasion and this particular variable, the Reserve Bank was even closer, having predicted in its August 2023 MPS that the June 2025 unemployment rate would be 5.3 per cent. It was, in fact, 5.2 per cent.

I responded to Brown’s tweet yesterday afternoon thus

Treasury didn’t publish lots of detailed quarterly tables in the PREFU, but the Reserve Bank did in their August 2023 projections (completed a week or so later than Treasury’s numbers).

How are things looking?

We only have national accounts data to March. In August 2023 the Reserve Bank predicted that real production GDP would rise by 2 per cent (apc) in the year to March 2025. On current SNZ estimates, it actually fell 0.7 per cent. Private consumption was forecast to grow by 2.8 per cent and it actually rose by only 1 per cent.

What of the labour market data? The Bank had the unemployment rate forecast to be 0.1 percentage points higher than it turned out to be. But they thought the employment rate by now would be 68.2 per cent of the labour force, but it proved to be only 66.8 per cent (and they expected numbers employed would have risen by 1.1 per cent in the year to June 2025, when they actually fell by 0.9 per cent).

As for wages, the private sector Labour Cost Index measure was forecast to rise by 3.8 per cent in the year to June 2025 and actually rose by 2.3 per cent (and the difference isn’t inflation (non-tradables inflation in the year to June 2025 was actually a bit higher than the Bank had forecast a couple of years ago)).

And, finally, the OCR was forecast to be 5.12 per cent in the June quarter 2025, but ended up averaging 3.44 per cent (as it happens, Treasury’s short-term interest rate forecast was materially less wrong than the Bank’s).

None of which is really intended to have a go at the Bank (although those OCR projections always looked odd), because (a) this stuff is hard, and b) relatedly, there are big margins of uncertainty around all sets of economic forecasts, especially those two years ahead. Senior Cabinet minister deserve to be called out when they cherry pick one single datapoint and claim outcomes are better than (some forecasters thought -a couple of years previously – that they’d be) under the other lot. Calling them out won’t stop them – politicians will politik – but in doing so they (further) discredit themselves.

As for some of the recent labour market data, here are a few charts I used on Twitter yesterday.

First, hours worked

Second, (my preferred measure of) wage increases (although note that productivity growth is probably weaker now than last decade)

Third, jobs

And here is the monthly version of the filled jobs series (which is drawn directly from tax data), noting that this is the most frequent and the most timely series (NB: a monthly HLFS would be great…)

And as bank economists remind us each month, most recent estimates have been tending to be revised down as fuller information comes to hand.

And finally, the SNZ experimental weekly jobs data, this time (because the data aren’t seasonally adjusted) shown by comparison to the same weeks in previous years.

There doesn’t seem to be anything very positive in the labour market data. At best, perhaps, the drop in the number of job ads seems to have levelled out.

UPDATE: I just saw a journalist claiming the real wage increases had gone negative again. That is not so if one uses the appropriate wage measure (ie the analytical unadjusted measure of wages, which does not attempt to correct – reduce – for productivity growth), whether one then uses either the CPI or the Reserve Bank’s core inflation measure to deflate wage increases.

Various bits and pieces have emerged from the Reserve Bank in the last couple of days; two in the form of other people’s OIA requests, and one in a partial response from the Bank to one of mine lodged with Treasury.

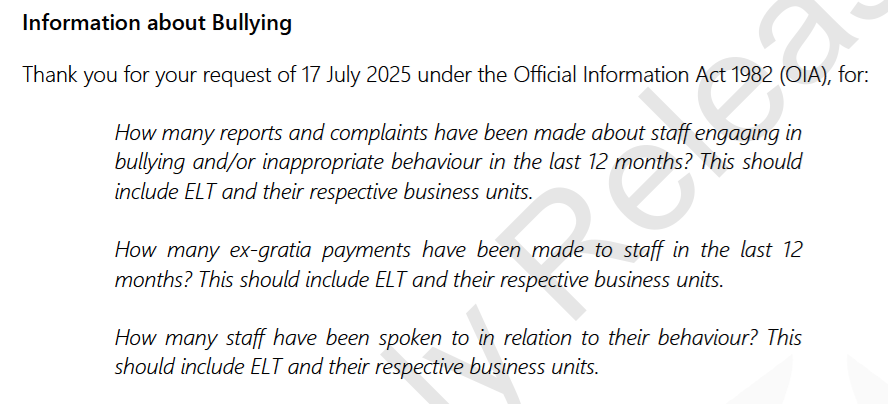

First, bullying. Someone, who must have had some knowledge of what was going on, had lodged a request for this information

Perhaps the Bank is turning over a new leaf on OIAs, as the request had only been lodged on 17 July and not only did the response go back to the requester on Monday (4 August) but they put it on their website that day (the Bank is quite selective about which responses they post, and there are often quite long lags). In fact, I just noticed there is another response – to a request lodged on 24 July – sent today and posted on the website today. If this really is a change of heart it is excellent news.

Anyway, the answers were interesting, to say the least

In the words of one former colleague, those payouts were “startling”. The 20 staff being spoken to seems a lot too, but who knows quite what standard they were using. Perhaps someone had spoken disrespectfully of the tree god, or suggested that the Bank really should have stayed within its allowed Funding Agreement spending limits? But to actually write cheques, hand over money, things must have been quite serious, even in an organisation not recently known for its budgetary discipline.

We know nothing more at this stage (amounts, specific reasons, who was responsible for the behaviour for which the ex gratia payments were made). To be entirely literal it isn’t 100 per cent clear that all the payouts were for bullying (the request covers any ex gratia payments to staff), but they probably were, given that the Bank headlines the entire response “Information about Bullying” and would have had an incentive to minimise the bullying dimension if there really were other reasons for some of the payments. Were the payments made before or after Orr left, and were any of them on account of his behaviour? I gather from Twitter that someone has lodged a further OIA so perhaps we will learn a bit more in time. But it doesn’t look good – and cases rising to level of payout must only be the tip of an iceberg, as some people are likely to be reluctant to lodge complaints, and others may simply have left the organisation.

The second OIA was about the new Auckland office (also only lodged on 24 July). You may recall that my source had indicated that the Bank had signed up to a fancy new Auckland office of a size probably inconsistent with the looming budget cuts. The Bank’s response seems to broadly back that story. The new lease agreement was signed on 4 November 2024. By that time (and as far as we can tell at present) the Bank did not know that its approved spending levels would be cut a long way back from what they had bid for when they lodged their next five year Funding Agreement bid in September. However, they were well aware that they had gone out on a limb, adopting a budget for 24/25 that was 23 per cent in excess of what they were allowed by Grant Robertson for that year under the Funding Agreement then in place, and had sought to persuade the Minister and Treasury that any (modest) cuts should be only from that unauthorised high “baseline”.

And while they may have needed a new Auckland office, this was the new space

and this was what it was to replace

In other words, they committed to more than twice the floorspace, in a more up-market building, at a time of general fiscal stringency and when they had no particular reason to suppose that they’d be allowed to keep growing. I’m not a property person but it seems that 10-15 square metres per head is about normal for typical open plan office

So it looks as though the Bank had gone lavish on the per capita floor space even if the new office was to be fully occupied at some point in future (which would have been a lot larger scale than the 164 staff and contractors they had in the Auckland office as at 30 June).

It seems a lot like a cavalier use of public money, made even worse (than their general budget excess) by the no-doubt multi-year nature of the property lease. But perhaps they’ll be able to sublet some of it?

And that spilled over into the third OIA response, that turned up this afternoon. It was part of a request I’d lodged with Treasury a couple of months ago which they’d transferred (that part of) to the Bank, and covers some late-in-the-piece material from the Bank to and from the Minister on Funding Agreement matters, after Orr had left. To be honest, I didn’t even think this material was in scope, as I’d been looking for Treasury material. As it happens, when I read what came in, parts seemed familiar, and I realised they’d already released these particular documents to someone else a month or so ago and I’d used a couple of bits of it last month (end of that post). But I hadn’t looked that closely then, and the significance of other aspects is also more apparent now.

First, last Friday I highlighted the way the temporary Governor Christian Hawkesby appeared to have actively misled FEC on where the initiative lay for the review the Bank now has underway of bank capital requirements. He played down any ministerial involvement claiming it had been just a Bank decision to do the review. That it clearly wasn’t was pretty evident from the Treasury filenote of that 24 February meeting between the Bank, Treasury and the Minister.

But to reinforce the point, here is Neil Quigley writing to the Minister on 16 March basically pleading (successfully) that she not accept Treasury’s view of how deep the cuts to operating expenses should be. This was the paper in which he pleaded that the Bank’s “culture” had evolved in light of the fiscal excess of recent years and that it would take time to change the culture and save lots of money. But he also said this

Hawkesby actively misled FEC. Once upon a time that sort of thing mattered.

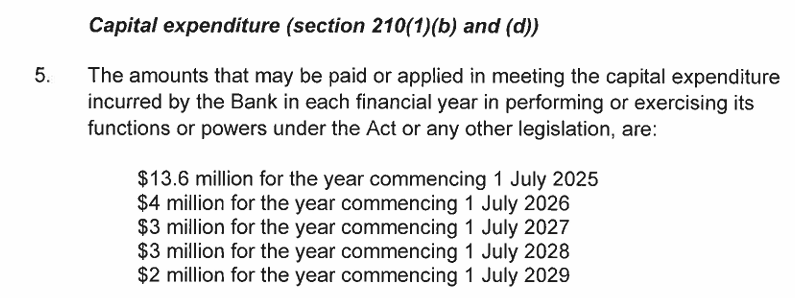

Where Quigley was largely unsuccessful at this stage was around the capital budget (not something I’d previously paid any attention to). The initial bid last September had been for $50 million over five years. At this point Treasury was proposing $26 million (which, assuming the numbers in the Minister’s Cabinet paper are comparable, was 12 per cent less than total expected capex for 2020-2025). Here was Quigley’s plea

Note that first item. If you’ve just rashly signed up to big new offices in a fancy building the fit out costs (for a lease that commenced on 1 August 2025) were likely to be large.

Quigley’s capex plea failed, and the Minister ended up agreeing to allow them only $26.3 million of capex over the full five year period. This is the annual phasing.

Which might suggest that they will be spending something close to $10 million on the fit-out of a new office that they simply shouldn’t have signed up to before they had any clear steer about the future. The 25/26 number ended up a bit higher even than the $13m Quigley had sought on 16 March – new estimates of fit out costs? – with the capex allowances for future years being slashed. (If Quigley’s plea is even roughly accurate you might wonder how sustainable all this proves – presumably the Bank will spend all its opex allowance, and perhaps they reckon they’ll come back cap in hand in a few years’ time, or degrade the existing capital and wait for the next Funding Agreement negotiations. Or Treasury might be right about what they need.)

The final observation from these papers is perhaps not of any great moment, but it is puzzling nonetheless. You’ll recall that the Bank had gone ahead and set a budget for 24/25 far in excess of what the Funding Agreement had allowed. There was never any serious suggestion that the Bank was allowed to carry forward earlier year underspends, use it all for a last year splurge, and then try to use that new level as a baseline against which any modest cuts should be set. But that is how Orr, Quigley and the rest of the board had operated (quite explicitly – it is in the Board minutes and the September 2024 Funding Agreement bid).

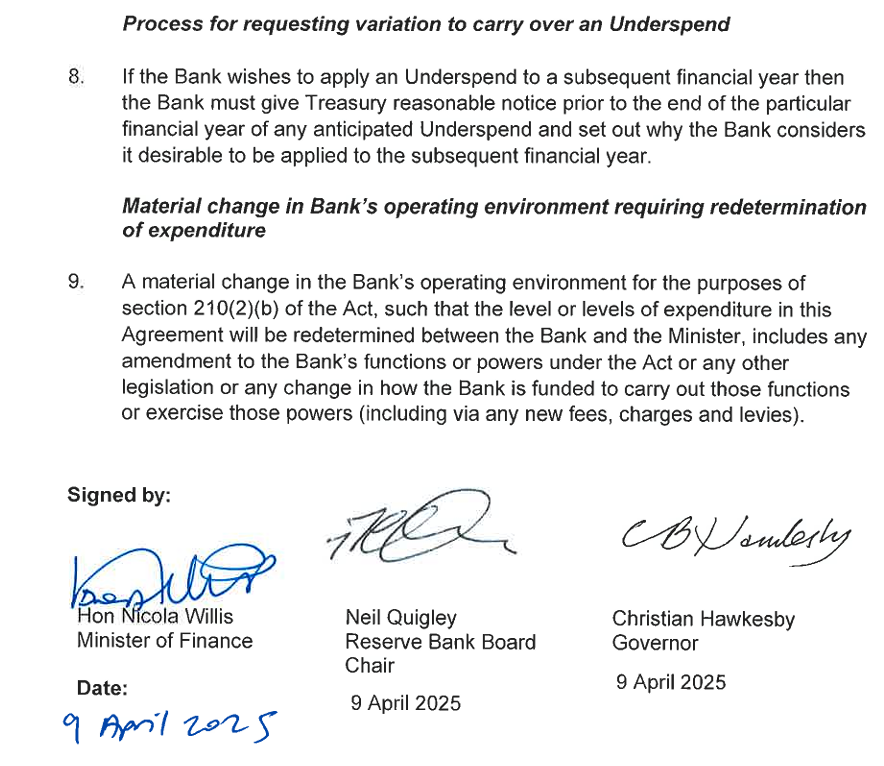

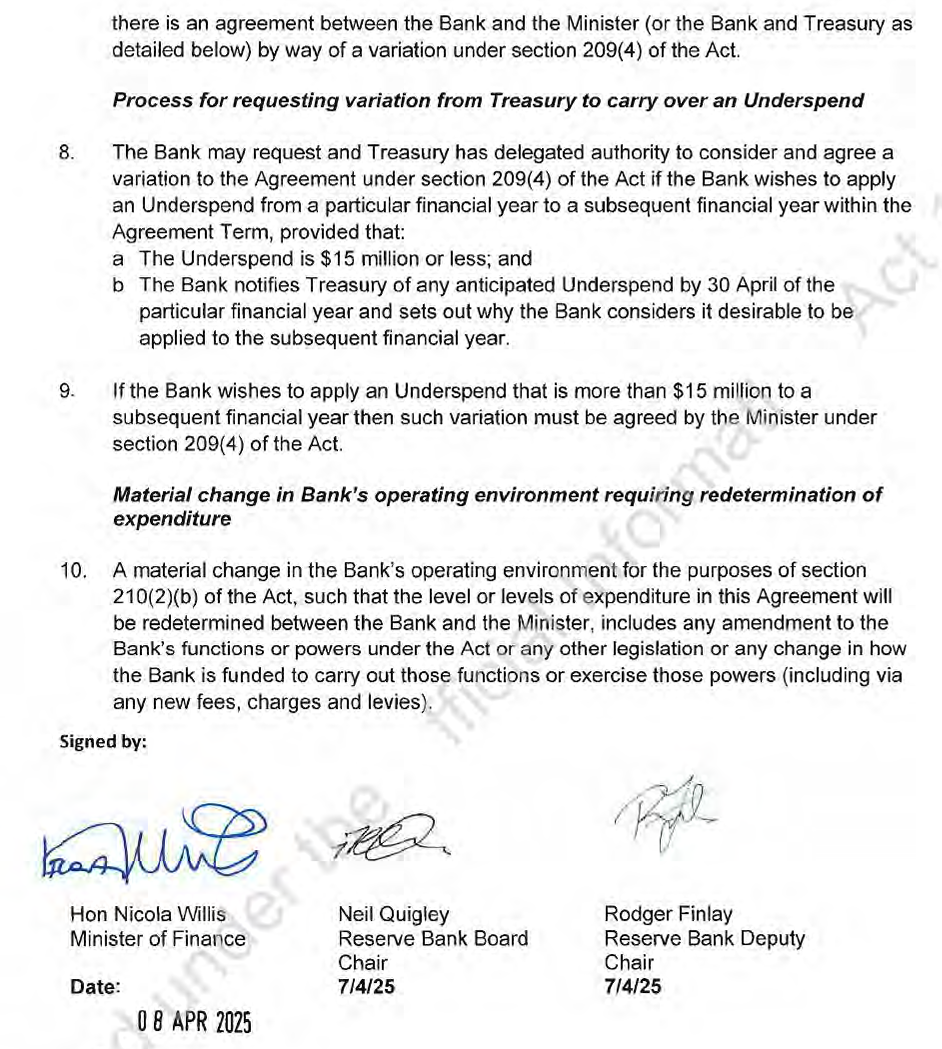

There are problems with the Funding Agreement model, which involves setting annual spending limits five years ahead. Sometimes it is hard to know when a particular cost might arise. So it probably does make sense – if this model is stuck to – to allow scope for some flexibility. It is there anyway – no one gets fired for going a bit under or over in any year (and isn’t formalised like a parliamentary appropriation), and there is always scope for a renegotiation mid-stream (as there’d been in 2023). But the Bank was keen to formalise something. I noted in a post last month that in that 16 March paper the version of the draft agreement the Bank submitted involved a model in which Treasury could agree to modest variations (up to about 10 per cent) and anything more required the Minister.

I included the signature block because what I hadn’t noticed before – hadn’t read to the end of the set of documents, which looked like they were just repetitions and admin paperwork – is that she seemed to agree to this only after she’d already signed up to something like what the Bank wanted.

In that OIA response there was this

All signed and dated and a scanned version sent back to Bank by one of the advisers in the Minister’s office, in a email of 10:14am on 8 April.

We are left wondering what happened. Quigley’s memo of 16 March did not touch on the variation issue at all. Was the Minister not made aware of it, including by Treasury, until the very last minute, or was she aware all along and very belatedly chose to take a harder line? Fortunately she did finally land on the best approach, but how? The original OIA to Treasury, lodged back in June but due shortly, may shed some light, but it just doesn’t look like a particularly smooth or adept end to the Funding Agreement process. And I wonder what Quigley, Finlay, and Hawkesby made of the latest, last, loss………..which couldn’t have happened to a more deserving bunch given their egregious bid six months earlier.

As for me, I guess I should read OIA responses – even other people’s – a bit more closely.

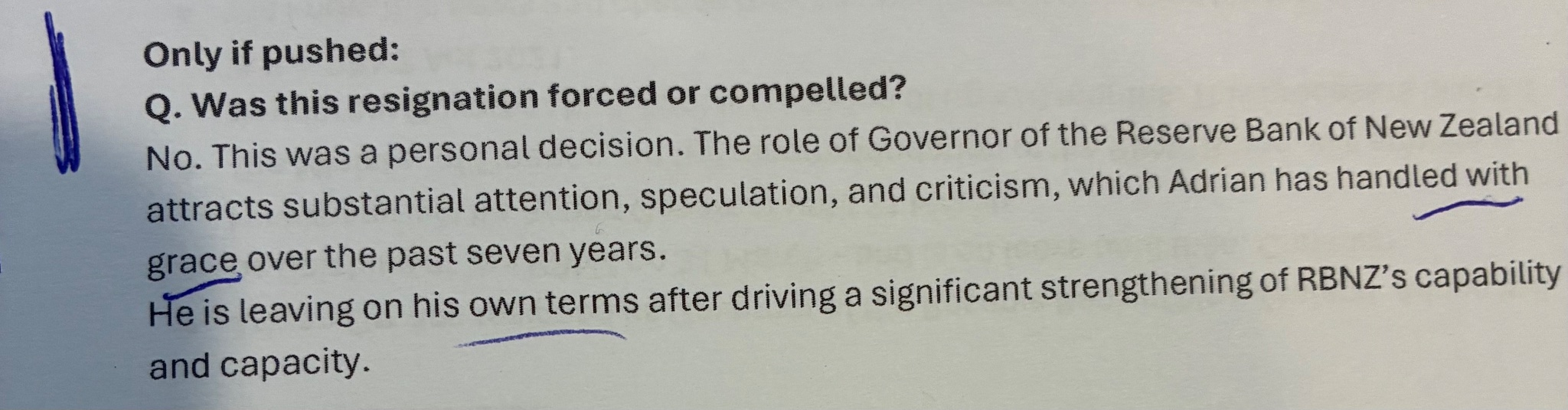

Today, 5 August, is five months since the shock resignation – or, as now seems much the most likely, engineered exit – of the then Governor of the Reserve Bank, who disappeared from office that very day, getting generously paid for several more weeks but not working until the official date his resignation became legally effective, 31 March. Since then we’ve heard not a word of explanation from him and (more importantly, since they are still public officials) have been deliberately, actively, repeatedly, and still to this day obstructed and mislead by the Reserve Bank Board, notably the chair Neil Quigley, enabled by the Minister of Finance, and implemented (in respect of OIAs) by the temporary Governor, Christian Hawkesby.

Applications for the position of Governor closed a couple of months ago, so I guess we must assume that the selection and recommendation process is now fairly well advanced. The Board established a Governor Search Committee

Being chaired by Rodger Finlay – who has no background in macroeconomics or regulatory policy, and who had a questionable start to his time with the Bank (still chairing the board of the company that owned the country’s fifth largest bank) – doesn’t inspire much confidence. And if Finlay appears like a decent general corporate governance type of person, recall that he has been deputy chair through a) the reappointment of Orr, b) the Board approving the Bank running spending levels last year far beyond what the Funding Agreement had envisaged or allowed, and c) (and so we learned yesterday) was part of the Board that allowed management to sign a new lease on Auckland offices last November, massively larger than the current office, with space for many more staff than they currently had, when i) the Bank was already spending more than their Funding Agreement had allowed, and ii) they (presumably) still had no real steer from the Minister of Finance as to what approved spending for 25/26 and beyond was going to be. [Oh, and he’s been party to the cover-up of the last five months.]

Quite a team he and Quigley must make. Not exactly a team to inspire any confidence in the wisdom of whoever they end up putting forward as a first nominee to the Minister of Finance, or a team that might assure a good potential Governor that he or she was going into a well-led governance structure. Responsibility for that is shared by those Board members and by the Minister of Finance who has continued to express confidence in Quigley (for reasons not comprehensible to anyone outside her bubble) and refused to proactively ensure vacancies were quickly filled by new able people.

We had a Governor resign once before. Don Brash announced his resignation and left office on 26 April 2002. Just under four months later, Alan Bollard was announced as the new Governor.

Defenders of the Board and Minister might point out that things are a little more complicated this time. By law, the Minister now has to consult with the other political parties in Parliament (in practice the Opposition parties, since the coalition parties will already have been involved through the Cabinet appointments process).

The law does not require the Minister to change her mind if the other parties (some or all) disagree (perhaps strongly) with a nomination, although the statutory provision would be empty if she did not pay at least some heed to concerns expressed. (There is no sign Grant Robertson did – and it was his new provision – when he went ahead and reappointed Orr, over objections from both ACT and National in late 2022, but if the provision is to have any meaning at all, you’d hope there would be some serious reflection on any objections, especially when an incumbent is not involved.)

However, if the paper work is a bit more time-consuming now than it was in 2002, bear in mind that the appointment of Bollard was accomplished in less than four months even though Michael Cullen had rejected the Board’s initial nomination.

By law (see above) the Minister and government can only appoint someone the Board recommends. But that does not mean that the Minister has to accept any particular recommendation. That isn’t the empty provision people sometimes suggest. There have only been three new Governor appointments since the legislative model came into effect (in 1990) and Michael Cullen recorded in his autobiography that he rejected the then Board’s nomination of Rod Carr (deputy and at the time acting Governor).

As was his perfect right to do. (The Board must have at least half-expected their nomination to be rejected as it was understood among senior management at the time that Helen Clark had made clear that she wasn’t going have any “Brash-clones” appointed.) I’ve long championed the much more conventional model in which the Minister gets to appoint their own preferred person as Governor directly (perhaps accompanied by scrutiny hearings by FEC before the person actually takes up the office).

But it was all done in less than four months, and it is now five months and counting since Orr left (and the Bank in 2002 was in nothing like the mess, or urgent need of new strong capable respected leadership that it is now). I hope the Minister is drumming her fingers and urging the Board to get on with it.

Quite who they might come up with remains a mystery, or whether the couple of new Board members this year might persuade their colleagues that whatever the Board has once seen in Orr he should be almost a benchmark antithesis of the sort of person who should be chosen.

I wrote a post a couple of months ago, shortly before applications closed, prompted by the advert for the job and what it suggested the Board might be after. As I have noted throughout, I don’t believe there is any obvious ideal candidate, and so inevitably compromises will have to be made (and in recruiting a person, the Board and Minister need then to have regard to the willingness and ability of the person to clean house and build a new and more capable second tier – we cannot for long be in a position where the deputy chief executive responsible for macroeconomics and monetary policy has (a) no background in the subject, and b) can’t intelligently comment on anything of substance other than from a script she has been given).

That said, straws in the wind aren’t terribly encouraging.

I’ve heard that a couple of very able applicants didn’t even get an interview (there is such an abundance of talent? Really?). And then there was media report (that I’d heard via markets people earlier) that a Bank of Canada Deputy Governor (they have many) was a strong possibility, perhaps even a frontrunner.

This would seem an ill-advised choice if it was really a direction the Board was considering taking. Gravelle seems to have no particular connections to New Zealand (other than a couple of conferences, one by Zoom), and comes from an organisation that – unlike the Reserve Bank of New Zealand – does not do banking (and non-banking) financial regulation and supervision, these days a big part of the Bank’s job. For all its undoubted analytical strengths, the Bank of Canada also has a quite different sort of monetary policy governance model (entirely internal) than New Zealand’s. And then there is the adverse selection issue: a person who was good enough to be a serious contender for Governor in his/her own country (G7 country and all that) would not be very likely to put themselves forward to be Governor of a much smaller, poorer, remote country’s central bank, a country with which they’ve had no particular ties. As a couple of people have put it to me, it is a bit reminiscent of the old imperial days – someone not quite up to being appointed Governor-General of Canada or Australia might still be handed down to New Zealand. And it is not as if parachuting in foreign appointees to top economic roles here has been a particular success story (see last two Treasury secretaries), nor in many ways was bringing back an expat after 15 years away to the Reserve Bank (even if Orr’s record makes Wheeler look less bad). Can we really have fallen so far that we can’t find a credible respected appointee at home?

Always possible I guess. Compelling choices certainly aren’t thick on the ground.

What of the temporary Governor, Christian Hawkesby? These were my comments a couple of months ago

Much of which I would repeat today. But unfortunately since early June we’ve seen not just that Hawkesby has been a part of the obstruction effort re Orr’s departure (and if he is working to Board direction the fact that he has not been willing/able to insist on a more open approach is a poor reflection on any claim he has to be thought a worthy occupant of the permanent role. And then of course there was that last sentence. We now know that not only did he repeatedly sit alongside Orr while he (Orr) mislead Parliament, but that Hawkesby himself misled them just three months ago. He proved unable to even pass that low bar I mentioned in June.

I ended that earlier post speculating on some possible sorts of names I hadn’t seen mentioned in any of the media articles (bearing in mind that the advert had talked of the importance of both financial markets knowledge and CEO experience)

Since Stobo is (a) an economist by training, b) has CEO experience, c) has financial markets expertise, and has been appointed to his current public sector role (chair of the FMA) by this government, and is a thoughtful and reflective person .you could see why he might be a strong contender if he wanted it (and was willing to give up his portfolio of directorships etc and media commentary). If one can’t have much confidence in the FMA, there’d definitely be worse people for the job.

But it is time to get on with it and get a new Governor in place. And then get on and refresh the Board, with a new chair to work with and oversee the Governor.

After The Treasury released their file note of that 24 February meeting between the Reserve Bank, Treasury, and the Minister of Finance (full copy here) a few people got in touch directly about a couple of aspects of what was written there, and what I’d made of it.

The file note indicated at one point that in the middle of the Funding Agreement discussion “The Governor left the meeting”. A couple of charitable people (not typically Orr allies) suggested that perhaps I was overinterpreting things to suggest that he’d walked out. I think they were pretty readily convinced that this was a very unlikely interpretation (in a meeting of which the Minister of Finance had already said that it had been clear to her that “emotions were running high”).

Former academic and now consultant economist Martin Lally then sent me this rather neat piece. Some of the non-economists among you might roll your eyes and suggest ‘that’s economists for you”, but I thought it was a nice example of the use of the technique to help discipline thinking.

Seems like a great opportunity to apply Bayesian analysis.

The hypothesis (H) is that Orr stormed out of this meeting. Your background data concerns his type of behaviour on other occasions. Suppose this alone leads you to the view that H has a 10% chance of being true. This is likely to be too low. The odds on H being true are then at least 1/9.

The next piece of evidence is the anonymous information about Orr’s behaviour at the meeting. I sense that you think this evidence would be much more likely to arise if H were true than if H were not true; maybe five times as likely? So, the Likelihood ratio for this evidence is 5. The odds on H being true now rise from 1/9 to 5/9.

The next piece of evidence is the meeting at Treasury a few days before the meeting in question here, on the same funding issue, after which Quigley apologised on Orr’s behalf for Orr’s behaviour. Since it was on the same contentious topic, this evidence seems much more likely to arise if H were true than if H were not true; maybe five times as likely. So, the Likelihood ratio for this evidence is 5. The odds on H being true now rise from 5/9 to 25/9.

The last piece of evidence is the minutes of the meeting in question, which reveal that Orr left during discussion about the funding issue, which Orr had very strong feelings on. If H were true, this evidence or something even more damning would be almost certain to arise because the minute taker would be most unlikely not to have recorded that Orr left. Say a prob of 0.95. If H were not true, the minutes could still have recorded him leaving at the time he did but in that case it would have to be due to quite extraordinary information he had just received that demanded his immediate departure from a discussion he would otherwise have strongly desired to be present for. It could be news of his house burning down or a serious injury to a loved one. These things happen but it would be extremely unlikely to have occurred in the 45 minute time slot in question. So, if H were not true, the prob of his departure from the meeting at this time is close to zero. Suppose events like his house burning down etc happen once every 6 months, so 1/180 chance of it happening on that day and, if on that day, 1/10 of it happening during the 45 minute duration of the meeting on that day, so 1/1,800 of it happening during the meeting, which is 0.0005. So, the Likelihood ratio for this evidence is about 0.95/0.0005 = 1900. The odds on H being true now rise from 25/9 to 47,500/9, so the prob that H is true is now 47,500/(47,500 + 9) = 0.9998, i.e., 99.98%.

So, with all this evidence, it is virtually certain that Orr stormed out of the meeting. This nicely illustrates the power of Bayesian analysis.

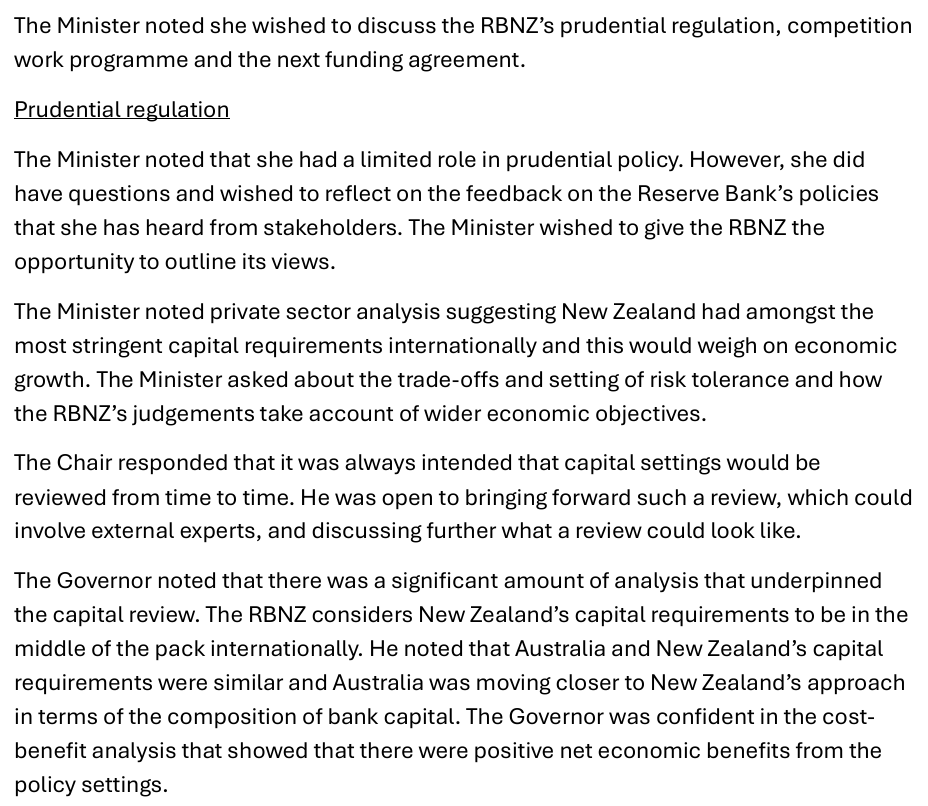

A few other people got in touch about the earlier part of the meeting, on banking regulation and competition matters. This part of the meeting was attended by Reserve Bank Deputy Governor Christian Hawkesby, whose day job at the time was financial stability, supervisory and regulatory etc issues (and he left the meeting when his item ended, thus missing the – apparent – fireworks).

The relevant bit of the file note was this

It is pretty clear from that that the Minister of Finance wanted a review. Perhaps she didn’t say it directly, but it is the clear implication of what is recorded in those first two paragraphs, and Quigley clearly recognised it as such, noting (folllowing the Minister’s remarks) that he “was open to bringing forward such a review….and discussing further what a review could look like”.

Why raise this now? Because Hawkesby is currently the temporary Governor, and supposed in some circles to be keen on getting the permanent job. Even if he doesn’t want to be permanent Governor, he is the deputy chief executive of a major government agency and a statutory appointee to the Monetary Policy Committee. Those who got in touch earlier this week reminded me that a few months ago (8 May) Hawkesby had been asked at Parliament’s Finance and Expenditure Committee about this meeting. Radio New Zealand’s report is here.

The first part of Hawkesby’s remarks seem fine

But then FEC was told this

The meeting had been only two months previously, it had been only a 45 minute meeting (of which he was only there for half an hour or so), on matters he had direct responsibility for, and the meeting itself has to have stuck in his mind given the role it seems to have played, within days, in the Governor’s departure. What’s more, surely you’d normally expect that coming out of a meeting like that there’d have been some sort of file note (especially when his boss and the board chair had appeared to be singing from different song sheets) or even an email to his direct reports in that area, and if he was really in doubt as to what went on I guess he could have asked Treasury for their file note. And yet we are supposed to believe that whether or not the Minister had requested (or only strongly implied) that a review should be undertaken was “not something that I sort of generally get into”. It reads a lot like misleading Parliament – in much the same way Orr had done repeatedly, often with Hawkesby in the room.

To be clear, I’m sure he is quite correct that “the decision to do a capital review was the Reserve Bank’s”, but in much the same way that the Governor’s decision to resign was a “personal decision” – at one level it was, but he was clearly prevailed on, pressured to go. Under the law as it stands Willis couldn’t directly compel the Bank to undertake such a review, but it will have been the less bad choice for them (she could have changed the legislation or commissioned her own review for example). And it was also a time – the end of March when the final decision to do a capital setting review was announced – where it probably will have suited Quigley and Hawkesby not to have been difficult; Quigley wanted his medical school, and Hawkesby may well have wanted to be made permanent Governor. The review would not have happened when it did without the Minister’s lead.

(And, to be clear, I don’t think that is a problem. As I’ve noted repeatedly, I think the law should be changed so that big picture prudential policy choices are made by ministers, with the Bank acting as (a) expert advisers, and b) implementing agents. I don’t think the Minister’s involvement here is inappropriate – whatever one’s view of actual capital settings – but really senior officials should not be misleading Parliament. And when they do, and when they sit silent while their bosses mislead Parliament, they really should not be serious contenders for high and very powerful office. Misleading Parliament is supposed to be a serious matter, and if MPs seem to have given up bothering over much (except when it suits), the rest of us should still insist on higher standards of integrity.

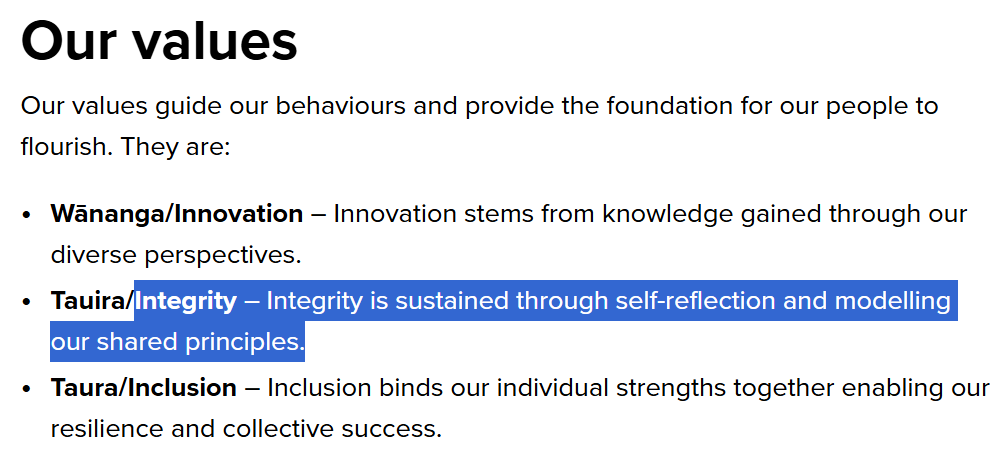

It is, in addition, supposedly one of the Reserve Bank’s own values

But perhaps those are just words. The actions at the top certainly haven’t aligning with the words for some time.

There are three things I wanted to comment on this morning, all prompted by yesterday’s release by Treasury of their internal file note of the 24 February meeting between the Bank, Treasury, and Willis.

an article in The Post this morning,

one on the Herald website last night, with further comments from Quigley, and

my own reflections on yesterday’s release.

The relevant section of the record of that 45 minute meeting is this

Post article

The Post article really isn’t worth linking to (you can no doubt find it if you want). It is noteworthy only for this extraordinary line:

“Hawkesby, and then Orr, left the 45-minute meeting shortly before it ended, but there is no evidence in the minutes that the discussion became heated.”

Which seems to ignore several things. First, the Deputy Governor is recorded as having left the meeting, but at the end of his item. He was the Bank’s senior manager responsible for financial stability and the first two items on the agenda (Prudential Regulation and Competition) were in his bailiwick, and he left when that discussion ended. He wasn’t a member of the Bank’s Board, and the Funding Agreement is between the Board and the Minister. He also wouldn’t have been one of the senior managers (CFOs and the like) providing technical/operational support on budgetary details.

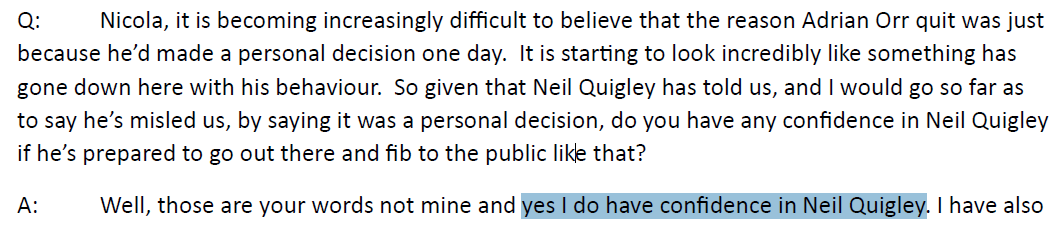

Orr, by contrast, left in the middle of the Funding Agreement item. Moreover, Nicola Willis has confirmed (it is in the Herald piece – see below) that Orr “chose to leave the meeting early” (and she is likely to be phrasing that diplomatically). And Willis told Heather du Plessis-Allan several days ago that it was clear to her that emotions were running high in that meeting.

And, finally, I guess the journalist has never been a bureaucrat. Writing down that the Governor “expressed frustration” about the Bank/Treasury relationship is likely to be a very muted and diplomatic rendering of the summary of the actual words and the tone around them. An official writing up such meetings isn’t, say, a Bob Woodward looking to capture all the drama for publication. (Note that my source last week suggested that the account was still not muted enough for Quigley, who reportedly was very upset to learn that such a record existed at all and allegedly rang Treasury to complain in no uncertain terms – an OIA may shed light on whether that was so.)

It might not be going too far to suggest that a more accurate account might involve words like “stormed out”, walking out not only on the Minister but on his own board chair, having (so the account suggests) sought to undermine his own board by making a direct play to the Minister for his personal view of what the Funding Agreement level should be (recall that Orr was both a board member, and working under board delegations of authority etc on management and budgetary issues).

Herald article

The Heraldarticle appears to have been prompted by yesterday’s Treasury release (they, like me, have had long running OIAs in with Treasury – theirs longer than mine – and this release was a partial response, while we wait for the rest of the issues to be addressed). But the article also contains quite a few comments from Quigley, apparently from an interview Tibshraeny did with him late last week after the Minister’s meeting with the Reserve Bank Board, as well as a fresh report that Willis had again expressed confidence in Quigley.

(It is to Treasury’s credit that they released both last week’s Quigley email (apologising for Orr’s conduct at a meeting with Treasury) and this file note. Either Rennie has decided that Treasury wants to be no part of the ongoing coverup and attempts to mislead by the Bank/Quigley, or (perhaps in addition) he has been encouraged in that direction by Willis, who seems to want more openness (and to be frustrated with the Board). If there are gag orders that Quigley signed the Bank up to they won’t bind Treasury.)

The article is behind a paywall so I’m not going to quote at length.

On Quigley, Willis is quoted as suggesting he is the right person for the job right now, including selecting a nominee for new Governor, and that at this “critical juncture” what matters is stability. It is pretty unbelievable, and utterly unconvincing stuff. The Bank is an embattled mess, and much of the mess is of Quigley’s own doing – spinning out the obstruction and misleading for months, overseeing the budget-busting spend up last year (that they’d not told the Minister about), and of course the appointment and reappointment of Orr in the first place. How can anyone have any confidence in a nominee out of a process led by Quigley? How could a good potential new Governor have any confidence in his chair? How can staff have any confidence in the board chair, when he is responsible for actively misleading them (as well as us) and for the big dislocations, layoffs etc the place is now going through? Rebuilding from here really demands a clean slate, led by someone commanding widespread respect and confidence.

But if the Minister’s line was perhaps predictable (you have to back someone until you fire them I suppose), Quigley’s comments were more interesting. He noted that the rest of the board had (we are told) expressed confidence in him – which perhaps isn’t unduly surprising as all but Spencer (new appointment) are as implicated as him in the events of recent months – but then must have been asked about the OIA obstructionism.

There has never ever been any sign that Quigley has any sort of commitment to openness or public scrutiny. The obstructionism, and reported quotes along the lines that he didn’t think the public had a right or need to know what went on (with one of the most powerful controversial officials in New Zealand), has to some extent been par for the course. But you did get the sense here that he feels the ground slipping away from under him. Most likely his staff gave him the sort of advice he wanted to hear on the law, but even if he got cover to hide there so far, it was a spectacularly bad call – in governance and public trust terms – to (a) be as obstructive as they’ve been (multiple OIAs have never been responded to directly, let alone completely) and b) to actively mislead the public repeatedly. No law required that. And any adviser who advised him that it was a good course of action shouldn’t be working there much longer.

In his final comments, Quigley seems to grudgingly acknowledge that his role included providing feedback to the Governor on his performance, but it is – on his telling – none of our business. He acts as if either Orr was some low level employee (say a junior accountant at Waikato University), or as if his responsibility is to the Bank and its management, rather than to the Minister and the public. And again, nothing warrants the calculated deceit of recent months, or attempts to substitute his judgement for the spirit and principles of the Official Information Act.

My thoughts prompted by yesterday’s Treasury release

A couple of additional thoughts occurred to me after reflecting further on yesterday’s release. The first (and probably not central) was this from their covering note.

The Bank had submitted its Funding Agreement bid to Treasury back in September 2024. Can it really only have been in early February that officials did even a preliminary assessment of what levels of spending they thought the Bank should be allowed? It seems odd, and yet in the papers the Bank released on 11 June in which an Orr email records him stating on 14 February “We have not heard from Treasury as to a preferred number”. It seems puzzling, but perhaps some of the outstanding OIAs will eventually shed some light.

But the bigger question is what we make of this episode of Orr’s extraordinary behaviour on Monday afternoon 24 February, in light of all else we know (or suspect). It must have been critical because, as I highlighted yesterday drawing from the Bank’s own 11 June selective release, within 24 hours various members of senior management were (a) aware an exit was a possibility, and b) putting together a working group to manage things at the Bank’s end. But, equally, it cannot have been final and determinative – except perhaps that Quigley and Willis may have concluded to themselves that Orr had to go (after undermining his board chair in front of the Minister and then walking out of the meeting, all only a couple of days after Quigley had had to apologise to Treasury for Orr’s conduct, because Orr himself wouldn’t).

I had a useful exchange yesterday afternoon with someone whose views always force me to think. This person argued that Orr’s behaviour in that meeting was tantamount to a resignation. I certainly agree that, on what we know, it was the sort of behaviour that shouldn’t be tolerated from any public sector chief executive, and there was no obvious way back from it (especially given the track record of Orr’s behavioural issues in the job, recent and past). But did Orr see it that way? Over the years he’d held the job he’d already gotten away with so much, and perhaps it is unlikely (to say the least) that it was the first time his undisciplined side had been on display in a Minister of Finance’s office. The Bank’s statement of 11 June may at one level have been accurate (if misleading)

“Distress” sounds like a reasonable description for what we now know of the 20 and 24 February meetings, and “necessary working relationships” must have been quite deeply impaired – but not just with the Board, but with the Minister and Treasury too – and Orr did finally come to a decision to go.

But there is still no sign that on 24 February he thought he was resigning, and every indication that his decision to go came only after quite a bit of pressure applied in the following few days. After all, recall my source’s story (and that person’s general account of what went on seems to have been vindicated so far where independent details have since emerged) that it wasn’t until 27 February that Quigley sent that Statement of Concerns to Orr, seeking a response (this wasn’t a quiet private chat, but something formal in writing by email), which seems to have been the final straw [UPDATE: Quigley probably also needed to get the rest of the Board squared away, who hadn’t witnessed Monday’s debacle]. And even then, if perhaps Orr wasn’t fighting too hard – it was clear he was going to lose the funding battle, and it clearly was close to his heart, and surely even he must have had some self-knowledge reflecting on his conduct over the past week – it was still a case of “senior counsel” called in by each side to negotiate, not a simple resort to standard resignation provisions in Orr’s contract, and getting him out of the office the very hour the resignation was announced.

Both Orr and Quigley will have known that it was most unlikely the Minister would sack him, and so he held leverage – I’ll go, but only if you sign up to a gag order (the limits of which, or the authority for which – did the Minister really not know? – are still not clear). He was clearly pushed, and there is no way by this point that the Board chair can have had confidence in Orr continuing (despite what he claimed on 5 March). Perhaps it was one thing to pledge that precise details of behaviour would not be disclosed, except as required by law (you can’t contract out of the OIA), but Quigley and Willis should have insisted on something like “After discussions initiated by the Board, the Governor has chosen to resign and left office today”. Except that – unless we see clear evidence to the contrary – perhaps they then preferred that we not know (and no one else on the Board seems to have objected). And so the obstructionism and repeated active deception of the public began, and continues to this day.

A few minutes ago I had this email from The Treasury

This is the document that my source last week claimed Quigley went ballistic about when he learned of its existence,

Taking Treasury’s caveats re the views expressed by anyone including Orr, can we conclude at least from the description of events that Orr walked out of the meeting in the middle of the Funding Agreement discussion, having undercut his own governing board’s views in front of the minister and his chair?

Oh, and credit to The Treasury for releasing this in full now.

UPDATE: I just wanted to put the record out there rather than write much commentary. However, I’ve had a few people get in touch suggesting that the record is capable of a more benign (for Orr) interpretation, noting that the Deputy Governor, Christian Hawkesby is also shown as having left the meeting part way through. However, I don’t think this alternative interpretation is correct. Hawkesby is shown leaving at a natural break point, where the banking regulation and supervision discussion ends. His main role at the Bank at the time was responsibility for those functions. He was not on the Board and Funding Agreement issues were mainly a matter for the Board and chief executive (supported by other DCEs on the financial management side of the Bank), so it seems quite natural that he would have left at that point.

By contrast, Orr is recorded as having highlighted differences between himself (and management more generally) and his board, and then to have sounded off at Treasury (“expressed frustration” is an official’s record, not that of a fly on the wall biographer, so likely to be understated), and then is recorded as leaving the meeting while the Funding Agreement discussion is still going on. It has also been suggested that perhaps the Minister had simply asked Quigley to stay behind. That interpretation seems unlikely given that the Treasury team (and MoF’s office advisers) were all still there (a later one-on-one might not be a surprise, but Treasury officials would not have been there to record that).

In the end, we do not know with certainty, although either Willis or Quigley (or Orr for that matter) could give us straight answers (so could Rennie, but it isn’t his role to).

As I outlined in my post on Friday, it now seems that much the most likely explanation for the sudden no-notice departure of the Governor of the Reserve Bank is that he was ousted; not formally sacked by the Minister of Finance (as she might well have had grounds to do, but it could have got messy), but – having left himself vulnerable by his record of questionable conduct – engineered out by the Bank’s Board (more specifically its chair), almost certainly with the foreknowledge and acquiescence, and possibly the direct encouragement, of the Minister of Finance herself. If so, well done them on that count. But the subsequent and ongoing active deception of the public (and of the Bank’s own staff), and the apparent defiance of the Official Information Act, is simply inexcusable, and it would seem that the Board (especially the chair), the Minister, and the temporary Governor share responsibility, to one degree or another, for that.

Looking back now, it is puzzling that this hadn’t seemed the most likely explanation pretty much ever since Orr left on 5 March, or at very least since the Bank’s big release, and statement, on 11 June. I guess that is what comes of treating words out of the mouth of the Bank, and especially its chair, as having any degree of trustworthiness whatsoever. More fool me.

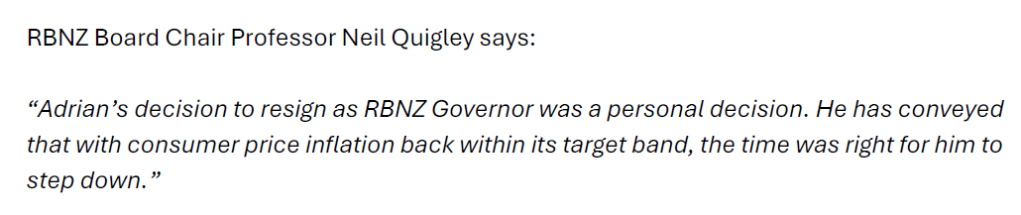

Recall that the first set of statements and Board chair comments on 5 March was clearly intended to lead us to believe there was nothing to see here. It was just a “personal decision”, there were no conduct, performance or policy issues at the heart of it, and really….when a big job was done, why wouldn’t an impressive leader take the opportunity to hand over the reigns. I won’t repeat all the things Quigley said that day, but this statement, issued by the Bank mid-afternoon on 5 March, after many questions had already arisen, rather captures the tone

Cincinnatus and all that. A couple of hours later he told the hastily-called press conference that he personally had still had confidence in Orr, and answered a direct question thus

The Bank spent the next three months blocking OIA requests and refusing to add anything, until the great reveal on 11 June. There was a set of carefully selected papers released (while avoiding anything on whole chunks of what must have gone on) and an official statement, presumably owned by both the Board and the temporary Governor and probably carefully vetted by lawyers (including ones for Orr?).

Having abandoned the 5 March story, this was all now carefully crafted to focus us on (a) that board meeting on 27 February, and b) a policy difference between the Board and the Governor which Orr, somewhat oddly, took so strongly to heart (“caused distress”) that he felt it would be better for him to simply go.

If you go back and read my posts when this release came out, you’ll see I never really bought the framing (which the Bank must have been pleased that much of the media followed) that this was a dispute over the Funding Agreement per se. As I have noted several times, many or most public service chief executives have suffered budgetary disappointment in the last couple of years, and none of them stormed off with no notice. But we were still clearly supposed to believe that whatever really happened, Orr had real agency (it was he who decided to leave, of his own accord, with no notice).

But there were still plenty of clues that it wasn’t the real story. There was, for example, the strident and repeated insistence by the Minister of Finance that it was all nothing to do with her, she knew little or nothing etc (even though she was the person responsible for the Governor, and to whom any resignation actually had to be addressed).

And there was the near-final version of the 11 June statement, which they’d sent out in error to OIA requesters shortly before the official general release time.

The shift from one (near-final) to the other (final) being clearly designed to remove any references to a meeting with the Minister and Treasury, and to draw attention away from them generally (and the earlier wording wasn’t going to have got into a near-final document of this magnitude by accident or the whims and failings of a junior staffer).

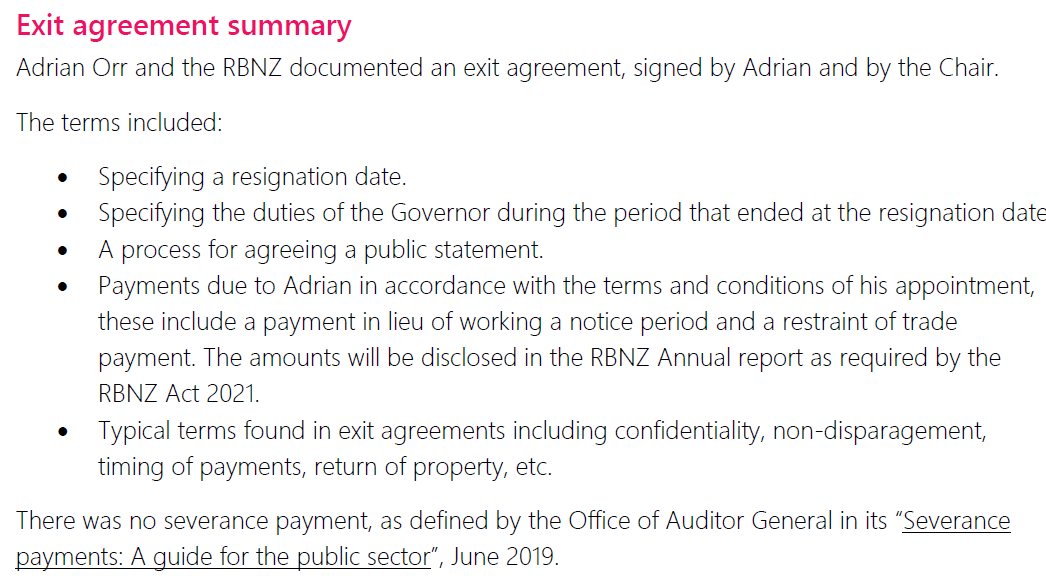

And there was the exit agreement itself, and negotiations being undertaken by “senior counsel” – interesting that that term was explicitly chosen by the Bank when they could easily just have used “lawyers” – for both sides. For an amicable departure, surely a quick chat with HR could have sorted out the application of Orr’s standard resignation terms, and any waivers of notice that might be sought or granted? And there was this summary (from the 11 June statement) of the exit agreement

Who typically has negotiated exit agreements? People being forced out (but not specifically fired). And Quigley has repeatedly referred to legal constraints on his ability to explain things, which can really only have arisen from the terms of this exit agreement, where Orr will have had some negotiating leverage (and were it all Cincinnatus-like there would be nothing for either side to want to hide – and no reason for Orr to have left the office the very day of the resignation, and yet be paid for several more weeks).

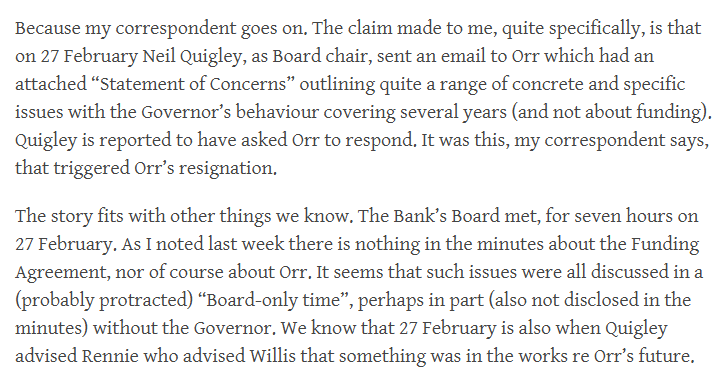

But things hung in limbo – hamstrung in part by the Bank’s obstructiveness over various OIA requests now having been appealed to the Ombudsman – until the account provided to me by someone who was clearly fairly close to events, and reported here. That person’s account was that (a) Orr’s behaviour had been very bad in a meeting with The Treasury on the Funding Agreement issues and then on 24 February in a meeting with both Treasury and the Minister of Finance, and that b) on the 27th, the day of the Bank’s board meeting, Quigley had emailed Orr a Statement of Concerns raising conduct issues stretching back several years and inviting a response. So the story went, at that point Orr decided to resign.

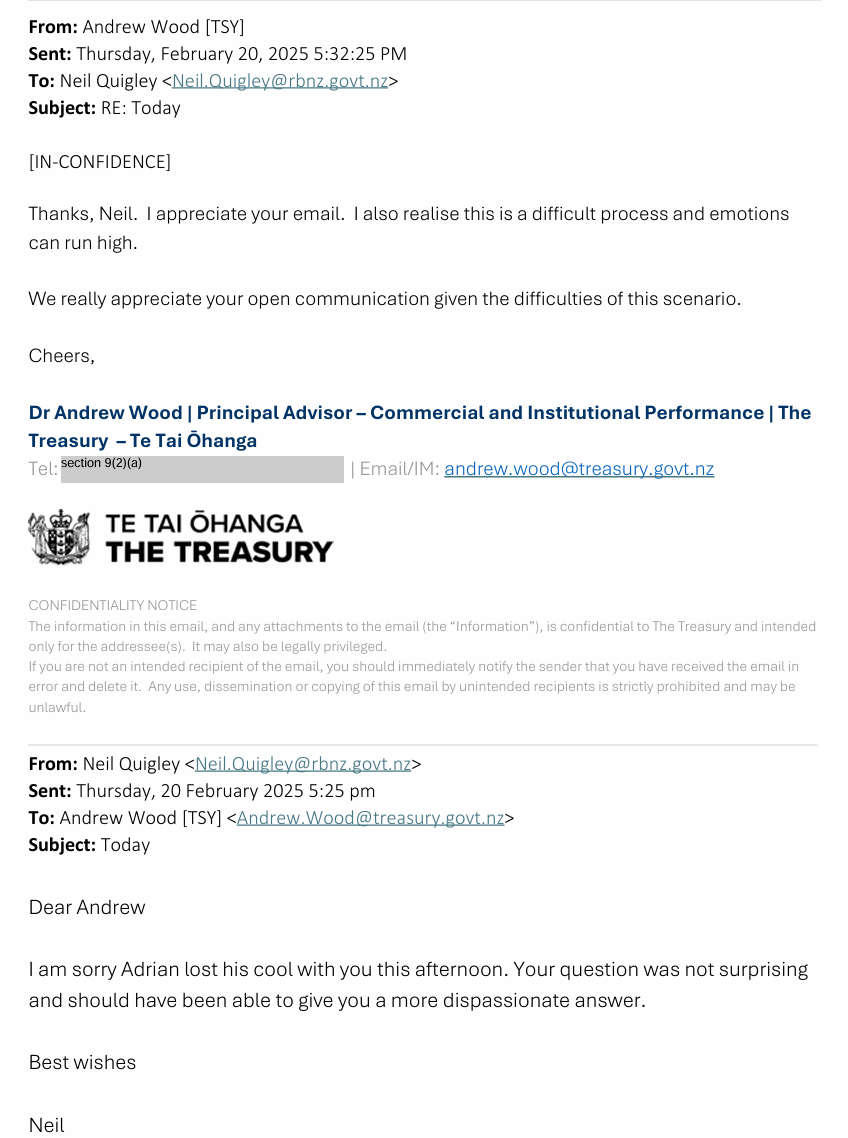

Treasury then disclosed an email sent by Quigley to a mid-level Treasury staffer after a meeting on 20 February apologising to that person that Orr had lost his cool in the meeting, in response to a perfectly reasonable question that Quigley acknowledged should have been anticipated and for which Bank management should have had a dispassionate answer. At a time when negotiations on the Bank’s future five-year funding were approaching climax Orr, in the presence of his chair, had (a) lost it with Treasury, and b) neither then nor later been willing to apologise himself (why otherwise was Quigley doing so, and not even on Orr’s behalf).

Then the Minister confirmed that “emotions were running high” in that meeting on 24 February too (around Funding Agreement disputes), while seeming to confirm that “employment negotiations” had been underway between Orr and the board in the days leading up to the resignation. And while the Bank has refused any further comment, they have also not chosen to deny any of it (including the alleged 27 February email, for which there is still no independent confirmation of its existence). Had there been no substance to any of this, they’d surely have owed it to both Orr and Quigley to (however briefly and tersely) set the record straight. They seem now to be hoping to wait out the Ombudsman.

And so the “engineered” ousting came to seem like the best working hypothesis for what had gone on. Perhaps on the spur of the moment, or perhaps lying in wait for some months, Orr’s conduct seems to have crossed the line (again – perhaps he’d been warned) and they had the leverage to get him to go. No doubt he was disheartened that he was going to lose the Funding Agreement fight and perhaps that made him readier than otherwise to go without much of a fight?

Anyway, having got to that point I decided to go back and reread that package of material the Bank had put out on 11 June, and see if any of it read differently in light of what we had since come to know.

I’d assumed – I think understandably enough – that the Bank’s Board meeting of Thursday 27 February might have been decisive. The 11 June statement seemed to point that way, as did my source’s report that the (apparently) decisive email had been sent to Orr on 27 February, and the fact that the only indications of advice to Treasury or the Minister had dated from then (I’ve now asked the Ombudsman to review the extensive withholdings in that release).

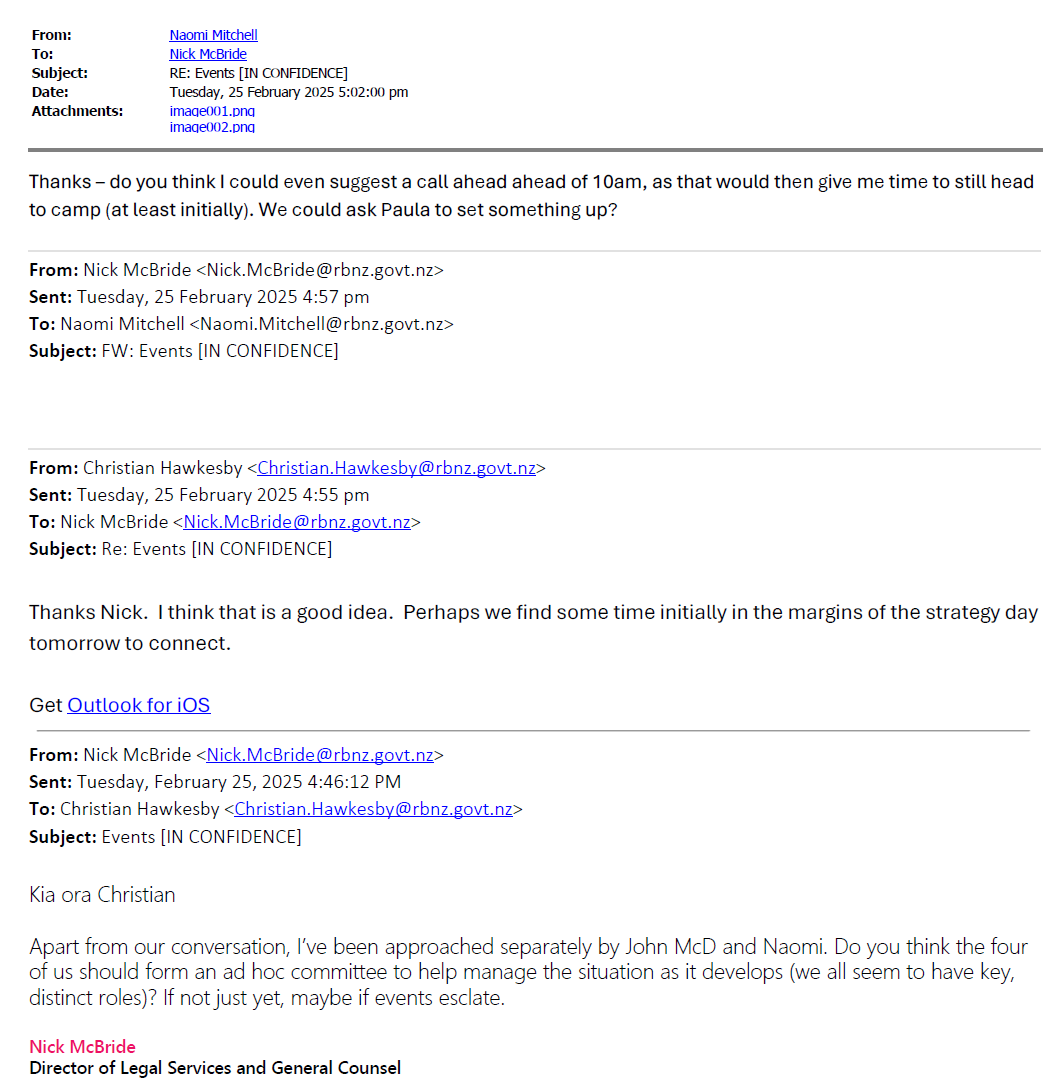

And perhaps there was some sort of final showdown then and a final decision made (to call in the “senior counsel” to negotiate exit terms). But the Bank’s information release pack included this (read from the bottom)

Who are the characters here? Hawkesby was (then) the Deputy Governor, McBride was (and is) the Bank’s General Counsel (but a third tier person, under an Assistant Governor who was also a lawyer), John McDermott was the Assistant Governor responsible for HR matters, and Naomi Mitchell was the (third tier) Director of Communications. And before 4:46pm on Tuesday 25 February [UPDATE: as it turns out, less than 24 hours after Quigley got out of that 24 Feb meeting] they already knew that something was afoot and agreed to the establishment of an “ad hoc committee” to help manage the situation. It seems clear that decisions had not yet been made (“If not just yet, maybe if events escalate.”) but this was two days before the Board meeting and just the day after that (“emotions were running high”) meeting with the Minister and Treasury. Was it Orr who told this group of his managers, or was it Quigley (Board chair)? We don’t know, but whatever had already unfolded – a serious risk of the Governor going presumably – was material enough for a range of key managers, not all direct reports to the CE, to have been brought into the picture (apparently separately/individually) this early. (This group then meets or exchanges messages over the remaining period pre and post resignation that was covered by the release.)

We don’t know what events were on the Statement of Concerns list Quigley is claimed to have sent Orr. As I noted last week, it isn’t as if he would have been short of examples just from material that had found its way into the public domain by then. But I wondered what other events might have been salient for the Minister and/or the Board.

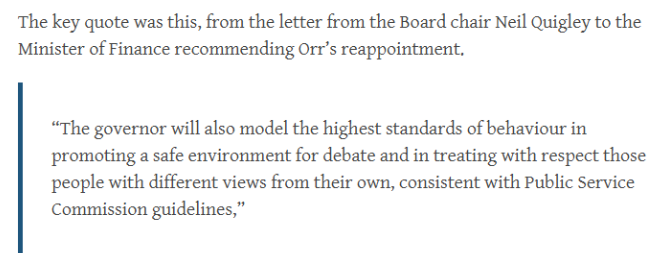

I noted last week that when (with spectacularly poor judgement) Quigley and the Board had recommended Orr’s reappointment in late 2022 there had been this.

When this was first released some time back it seemed like little more than make-believe stuff. But perhaps it had been the basis for conversations with Orr at the time? After all, the Board (and Quigley) can hardly have been oblivious to the long list of concerns and issues, so perhaps there was some attempt at insistence on better behaviour in a second term?

If so, it didn’t go well. Even externally, Orr continued to mislead (or worse) FEC and media. As the Minister noted last week, she’d last year passed a complaint about Orr’s behaviour to a New Zealand Initiative employee to the board to address.

And we learned just yesterday that it seems that the Bank never told the Minister of Finance that they were going to budget in 24/25 for operational spending far in excess of even what Grant Robertson had allowed them for that year (although, to be clear, responsibility for that must lie with both Quigley – as board chair – and Orr, as CEO). Perhaps when Willis finally realised she had been had, she was (and I would hope she was) really annoyed and perhaps, as regards Orr, steel entered her soul (belatedly) at that point. Of itself, not quite dismissal material perhaps (after all, Quigley was responsible too and she’d just reappointed him) but enough to put you on watch.

Who knows if Orr’s conduct at and after those two February meetings was itself enough to lay him open to pressure to go. As yet, we have only quite sanitised comments on how those meetings went down (including the Orr/Wood exchange, where they were both trying to settle things down after the event) but it was repeated behaviour from a very senior figure within days, at a time when the Bank really need to maintain good relationships. If it wasn’t enough in itself, there was other stuff going on at the very same time.

Going back to that period, I realised that it had been on the very morning of 20 February – the day of that unapologetic blow up at Treasury – that Orr had been telling demonstrable untruths again to Parliament’s Finance and Expenditure Committee (at his appearance on the February Monetary Policy Statement). I wrote about it in a post on 21 February, “Orr at it again”. I went back through that post the other day, and listened again to the video of the hearing to check that I’d heard and recorded things correctly. It was, as it turned out, probably his last public appearance as Governor and I counted five outright misrepresentations (two I would go so far as to call worse than that), all on matters where the Governor was either well aware of the truth, or should reasonably have been expected to have known the truth. (And just to be clear that responsibility is shared: at the table with him were his deputy responsible for monetary policy, Karen Silk, and the chief economist Paul Conway. In the row behind Orr you can see Christian Hawkesby, MPC member and Deputy Governor, Naomi Mitchell (Director of Communications), and one of the external MPC members. Not one of them made any attempt to correct Orr on any of these points.

The most egregious of Orr’s claims that day – although not necessarily particularly consequential, just the easiest to unambiguously refute – was the (repeated) claim that the Reserve Bank had been among the first central banks to tighten (when inflation took off a few years previously) and the new, and even more out of step with reality, claim that the Reserve Bank had then been among the first central banks to cut rates.

In my post that day I observed

As I noted, he’d done this sort of thing often enough before, but when I checked my records it seemed to have been the first time since the change of government that he’d been caught in such flagrant attempts to mislead a parliamentary committee (there are plenty documented in the years previously). Had he been less bad for a while, or had I not been paying so much attention? I ended up raising this episode with the Finance and Expenditure Committee the following week (before Orr’s resignation), in time with full chapter and verse – as I recall, I thought it was pointless to raise it with Willis, but the FEC chair was new.

I don’t suppose this particular episode of egregious behaviour – which his senior team seemed to walk by – had anything particularly to do with Orr’s ouster, underway just a few days later. My point is only that if for whatever reason you think what we know of those two private meetings mightn’t really have been serious enough to use as a lever to oust Orr, there was plenty more behaviour that could have, this one visible to anyone who chose to watch/read. If Willis helped engineer the ousting of the Governor, she did us – and standards of public life in New Zealand – a service.

None of which – not NDAs, not nothing – warrants participation in active and repeated, ongoing now, attempts to mislead New Zealanders and obstruct scrutiny. And if – as the Minister suggests – she isn’t overly happy with how the Bank is now handing things, the Board chair serves at her pleasure. If she wants different standards, a good way to signal that would be to replace the chair, now.

If something like what I’ve hypothesised here is what happened back in late February and early March, perhaps the Board and Minister should have insisted on a terse statement along the lines of “Following discussions initiated by the Board, the Governor has resigned and has left office today” and said nothing more that day. It wouldn’t have stopped the questions, or the OIAs. Perhaps it wouldn’t have proved tenable, or Orr wouldn’t have agreed. But there is just no excuse for the deliberate repeated ongoing effort to mislead us.

Or their staff. This was from the package of Q&As sent out by Naomi Mitchell to the entire Bank second and third tier mamagement group first thing in the morning the day after the resignation, for use with staff.

One of the mysteries of the months leading up to (what appears now to have been) Orr’s ousting as Governor, was how the Minister of Finance – apparently very focused last year on spending restraint in central government agencies, especially ones that weren’t really public facing – had let Orr and Quigley (and the rest of the Board) away with 2024/25 operating expenses so far in excess (23 per cent in excess) of the level of spending for that year allowed under the amended Funding Agreement Grant Robertson had signed off shortly before the 2023 election.

The Minister can’t directly control the Bank’s annual budget but the law requires the Bank to produce a Statement of Performance Expectations each year, to be published before the start of each financial year. The Act sets out what has to be included in a Statement of Performance Expectations (SPE)

The Act specifically provides for the Minister of Finance to be provided with the opportunity to comment on a draft of that SPE, and explicitly provides 15 working days for her to provide comments (drawing, no doubt, on advice from The Treasury which, again under the Act, has been made formally the Minister’s monitor of the Reserve Bank). The Minister also has the power of the bully pulpit: she could openly call out excess, if she knew about it.

In a post a couple of weeks ago I revealed that neither the Minister nor the Treasury had raised any concerns about Orr and the Board proposing to run levels of spending miles in excess of allowed levels, at a time when pretty much every other central government agency was facing actual cuts, and when the Minister had already (in early April 2024) reminded the Bank of her “fiscal sustainability programme” in her letter of expectation, in the context of approaching negotiations over a future Funding Agreement.

And when she mentioned reprioritising “before seeking any additional funding” you’d have to suppose that the benchmark against which “additional” would be understood by her was the level of funding her predecessor had approved only eight months earlier.

It seemed pretty surprising, to put it politely, that neither the Minister nor Treasury had raised any concerns when they were offered the opportunity to comment on the draft SPE. But I’d realised that although I had their comments, I didn’t have the draft they were reacting (or not) to. So on 3 July I asked for that and it turned up this morning, in full and unredacted (so should presumably have been supplied weeks ago).

And it turns out that the answer to my question as to why neither the Minister nor The Treasury had raised any concerns about the planned spending levels is that….the Bank just didn’t tell them.

You might find that surprising. I certainly did. You might wonder if I have misread something. But here is chapter and verse from the short covering memo to the Minister of Finance, dated 30 April 2024, and signed out by Simone Robbers, at the time one of Orr’s many deputy chief executives (formally, Assistant Governor, Strategy, Engagement and Sustainability).

It isn’t clear what about the “current operating environment” meant they thought they shouldn’t tell the Minister how much they were planning to spend. But whatever their reason, they didn’t. She didn’t know.

My view of the Minister of Finance has been revised up quite a bit in recent days, and this discovery is one of the reasons.

If you were being uncharitable you might think that the Minister should have asked, or the political advisers in her office should have asked, or – when it was sent on to them – The Treasury should have asked. And perhaps they should. But in the Minister’s case it was her first year in office, she had sent that Letter of Expectation just a few weeks previously, and she’d have had absolutely no prior reason to suspect that the Bank was going to adopt a budget with operating spending levels so far in excess of the elevated levels for 2024/25 Grant Robertson had approved the previous year. Who would? After all, this was Mr “cool your jets” Orr himself, who talked of fiscal restraint assisting in getting inflation down.

Perhaps The Treasury is more culpable, but I expect that the people reviewing the draft Statement of Performance Expectations were by nature more focused on the structures of documents and getting the Bank to jump through the right bureaucratic hoops. They won’t have been fiscal focused, and again….why would they suspect the Bank would just decide to blow out spending way beyond approved levels?

In bureaucrat land, “no surprises” is a big thing. But the Bank (Orr and Quigley) seem to have consciously chosen to run a great big surprise for the Minister of Finance. Perhaps the budgets were not quite locked down on 30 April (probably they weren’t) but if they’d been planning to stay within Funding Agreement limits it would have been easy enough to have included a brief mention that the forecast statement of comprehensive revenue and expense would include in-scope spending at levels consistent with the Funding Agreement allowance for 2024/25. Or, if they really thought they somehow had authority to spend so far beyond, they could at least have given the Minister an indicative range, and explained how it related to the (then) Funding Agreement limits. Instead, they seem to have told her nothing.

It is really quite extraordinary.

And one is left wondering when the Minister finally realised she’d been had. Perhaps it wasn’t until Treasury, many months later, got inside the Bank’s opening bid for the 2025-30 Funding Agreement, ran the numbers and realised that while the Bank purported to be offering up modest cuts, in fact they were from a level far above what had been allowed in the previous Funding Agreement; an inflated, bloated, baseline of their extravagant creation.

(It is always possible there is some other advice somewhere in which all this was pointed out early to the Minister, but if such advice exists the Bank has had every reason to helpfully – to them – disclose it. For the moment, it seems very unlikely that they were straightforward with her.)

And if the ousting of Orr has been accomplished, the board chair Neil Quigley remains in office. It wasn’t his signature on that 30 April advice to the Minister, but it was his Board that approved both the egregious 24/25 budget and the equally egregious 2025-30 Funding Agreement bid. Useful as he may have been to the Minister in late February and early March, there is no way he should still be in office.

The Bank purports to pride itself on integrity

But there has been little or none on display through any of this.

(By way of curiosity: I don’t usually pay much attention to which countries my readers come from, but I have noticed in the last few days quite an upsurge – from a vanishingly small base – in views from the Cook Islands. Perhaps some Wellington public servants need to find some lighter reading for their winter holidays, or is the former Governor now a quiet reader? Who knows.)

In the last day or so I’ve seen or heard two sets of comments from the Minister of Finance on the Orr/Quigley/Reserve Bank/Treasury/Willis – and it is now about all of them – business.

The first, that I want to deal with only briefly, was in The Post this morning under the heading “Willis dismay with RBNZ” (online here).

The journalist was obviously a bit of an Orr fan, as this article is the second time in two days The Post has talked of Orr’s “reputation for being charming”. No doubt he could and did turn it on when he chose, but not, surely, ever to anyone who ever challenged or disagreed with him (that included – very evidently – Nicola Willis when on occasion as Opposition finance spokesperson she asked Orr a slightly uncomfortable question at FEC hearings).

Much of what is in the article was also covered in my post yesterday. So I wanted to mention only this snippet

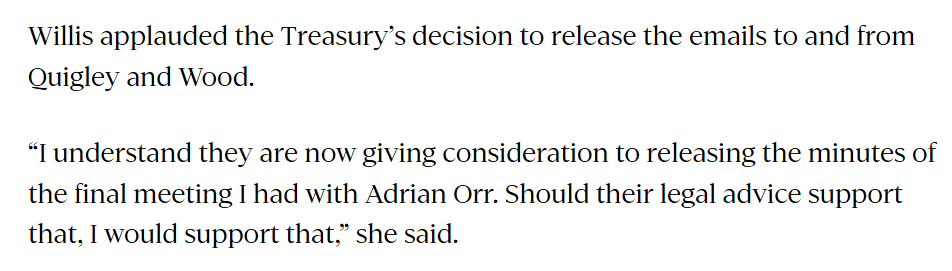

I guess she’d have looked a bit silly to have objected, but it is good to see her explicitly welcoming that Treasury release. On the second bit of that extract, it refers to the meeting on 24 February involving Quigley, Orr, Hawkesby, and senior Treasury people as well as the Minister herself. It is good to know that Treasury is considering releasing the minute of the meeting given that my request for it was lodged with them more than a month ago (as part of a larger request on Funding Agreement issues) but I presume there have been other requests, including since Tuesday when I reported the claim by my source that Quigley had been apoplectic and had complained to Treasury when he’d learned that such a minute existed. Again, it is good to know the Minister thinks Treasury should comply with the law, and we will look forward to the release.

The Minister’s more substantive comments were in an interview yesterday afternoon with Heather du Plessis-Allan. The audio is here and my transcript is here

Why do I bother doing the transcript? Partly for future reference and partly as a way of focusing my mind on all the lines Willis used in answering (and avoiding answering) questions. There were things I hadn’t really noticed when I listened live.

What do we learn from the interview? First that “emotions were running high” (the no doubt carefully chosen phrase for something like Adrian Orr losing his cool again) in the 24 February meeting she attended (although apparently there was no swearing) and she’d “heard reports” of the 20 February meeting between the Bank and Treasury where again “emotions ran high”. About, of all things, the Funding Agreement…..as if almost every single agency in Wellington hadn’t already been facing budget cuts (and it presumably wasn’t as if anyone was proposing cutting out the role of Governor).

Recall that Quigley email to Treasury (reproduced in yesterday’s post). The Governor was so ill-disciplined and out of control that in response to what Quigley recognised was a perfectly reasonable question from a mid-level Treasury official, Orr lost it, and then wouldn’t apologise, either immediately or after the meeting (instead Quigley was left to go and make his own apologies for Adrian). And sufficiently out of control, and unresponsive to what must have been feedback from his own chair, that the “losing his cool”, “emotions running high” behaviour was on display again several days later to a meeting with the Minister himself. In a normal employee such behaviour, especially repeated and without prompt and full apology, might of itself almost have been grounds for dismissal. (Humans make mistakes, even public sector chief executives, sometimes provoked, sometimes not. But when made aware you apologise, ensure it won’t happen again, or….you really aren’t fit to lead people and public organisations.)

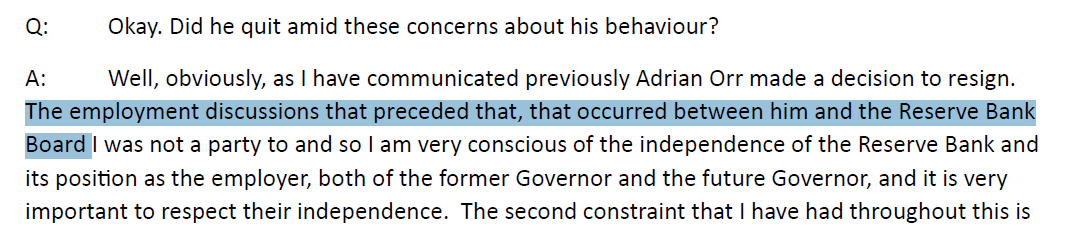

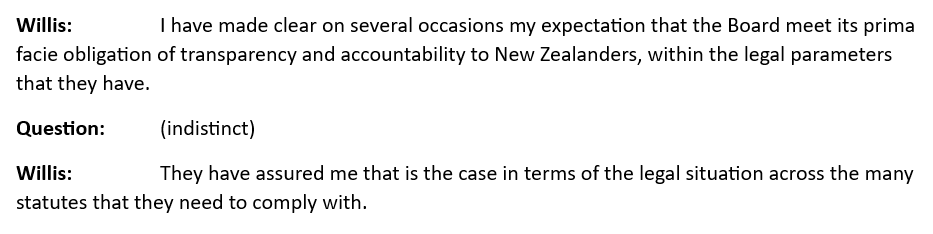

Willis was again at pains to suggest that the employment of the Governor was nothing to do with her, but purely something for the Reserve Bank Board. As a matter of law it simply isn’t so (I ran through the relevant provisions a couple of days ago), and the fact that it isn’t so has nothing to do – contrary to the Minister’s claim – with the “independence” of the Reserve Bank. There are plenty of roles and powers for the Minister of Finance in the Reserve Bank Act (as well as appointing and dismissing and receiving resignations from the Governor). For example, the Reserve Bank has what is known as “operational autonomy” on monetary policy, but they work to an inflation target by the Minister. In banking supervision and crisis management, some powers are exercised wholly by the Bank while others need ministerial approval. The Minister is directly party to the Funding Agreement. Parliament could have chosen to give the Minister no role re the Governor’s appointment etc but it never has (fortunately or there would be no political accountability at all). The Minister is responsible for the Governor, while the Board – whose chair is removable at will be the Minister – monitors etc the Governor, accountable to her.

At the very end of the interview Willis is asked

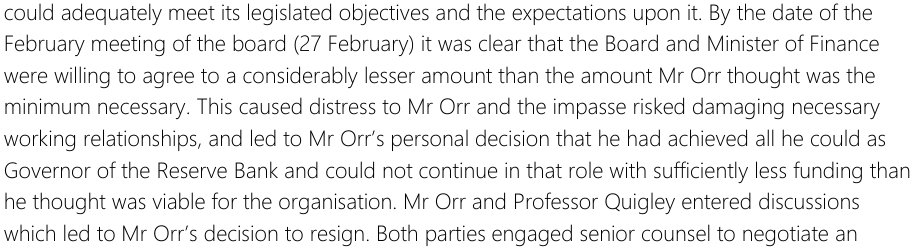

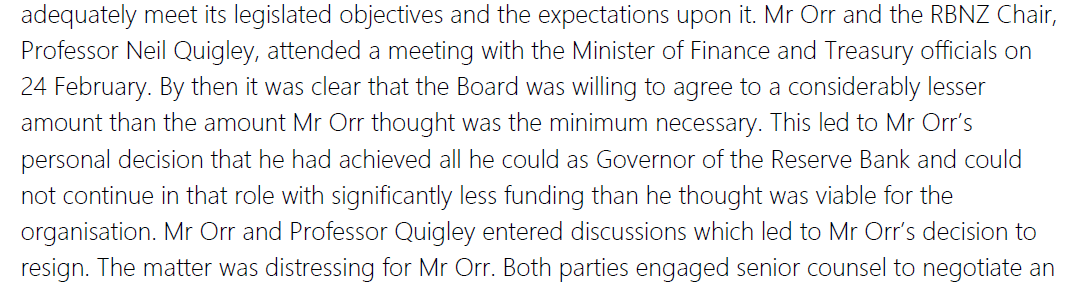

So far, we’ve had two quite different stories from Quigley, neither of which appears to be the truth. First, back on 5 March we were assured it was just “a personal decision”, with denials of any policy or conduct or similar issues being involved. We were intended to believe the man was tired, the job was done, and it was time to do something else. Then on 11 June, the Bank’s carefully crafted statement told us a new story. In this story there had indeed been material differences between the Board and the Governor over what they could live with in the next Funding Agreement. This we were told

“caused distress to Mr Orr and the impasse risked damaging necessary working relationships, and led to Mr Orr’s personal decision [ that term again] that he had achieved all he could as Governor of the Reserve Bank and could not continue in that role with sufficiently less funding than he thought was viable for the organisation”.

This time we were clearly intended to believe that the “personal decision” [which in a narrow and formal sense it was] was really just about (strongly felt) policy and resourcing differences.

Had you read either or both of those accounts, you might have believed (and were clearly supposed to) that the very first the Minister of Finance would have known that anything so dramatic was afoot was when on 27 February Quigley advised Iain Rennie of something briefly (words were withheld), who in turn advised the Minister briefly (words were withheld), who responded (puzzlingly) with nothing much more than something like “thanks for the update”.

But look at what the Minister said yesterday afternoon

You don’t usually have “employment discussions” when someone comes to you and says their job is done and they are going to leave, and even when the CE comes out of a Board discussion on funding and concludes it might be better for everyone if he, the CE, moves on. There will have been standard resignation and notice provisions in the Governor’s contract. Easy enough to have HR put those in train.

“Employment discussions” between the Governor and the Board preceding his resignation strongly suggest that serious issues were raised by the Board with the Governor, serious enough to have potential implications for whether they would be happy for him to continue as Governor. Which would be consistent with my source’s story, from the post on Tuesday:

And you can well understand why it might trigger Orr’s resignation, since getting to such a point clearly indicated a serious loss of confidence in the Governor, and quite possibly an almost irreparable breakdown of trust.

The Minister continues to state that she does not know the contents of the exit agreement then negotiated between expensive senior lawyers for both the Board and Orr. Which, on her account of what went on, should be simply extraordinary, because (a) the resignation would have to come to her, and b) she is the only guardian of the public interest here, and the one who would, in principle, have to account to Parliament for any deals done. She and her office, or at very least Treasury, should have been all over any terms – especially around non-disclosure matters – Quigley was agreeing with her (outgoing) Governor. And yet we must presumably take her at her word that she was not, and the OIAed paper trail suggests no Treasury advice on such matters at all.