Yesterday’s Herald had an interesting article on the reappointment late last year of Adrian Orr as Governor of the Reserve Bank. The article appeared to have been prompted by the Bank’s response to an OIA I lodged last year asking for background material on the reappointment. A link to that OIA response is now on the Bank website.

The key quote was this, from the letter from the Board chair Neil Quigley to the Minister of Finance recommending Orr’s reappointment.

“The governor will also model the highest standards of behaviour in promoting a safe environment for debate and in treating with respect those people with different views from their own, consistent with Public Service Commission guidelines,”

The best that might be said for that claim is that it may represent wishful thinking that somehow their leopard once reappointed might change his spots. So many people who have interacted with Orr was Governor, or observed him interacting with others, could testify that he has modelled none of that sort of behaviour (and there are specific accounts on record from people for Victoria University’s Martien Lubberink and the NZ Initiative’s Roger Partridge, as well as the story that Quigley himself one day felt obliged to pull Orr out of a Bank Board meeting over concerns about Orr’s conduct in the meeting). Watch any Orr appearance at FEC and much of time his response to challenge and questioning has been pretty testy. There must have been a recent Damascene conversion for Quigley’s assertion to the Minister to be anything other than wishful thinking at best. More likely it is just outright spin.

There was another interesting quote in the Herald article itself, from Chris Eichbaum a Labour-affiliated member of the outgoing board (both the outgoing board and the new Robertson board recommended the reappointment). Eichbaum is quoted as claiming that

An outgoing board member, Chris Eichbaum, confirmed to the Herald the old board went through a “robust and exhaustive”, “backward and forward-looking” process before coming to its decision to endorse Orr.

However, the Bank released summary minutes of the relevant meeting of the non-executive old-Board directors on 12 May last year (which, incidentally, was attended by Rodger Finlay, at the time chair of the majority owner of Kiwibank, the subject of Reserve Bank prudential supervision). The entire meeting lasted only an hour, with five items on the agenda, including the Annual Review for the then Deputy Governor.

“Perfunctory” looks like a more accurate description than “robust and exhaustive” – which isn’t surprising since the old Board had no formal responsibility any more and most of the members were by then probably more interested in their own next opportunities beyond 30 June (I recall one telling us at about that time of the next role he was going to take on once he left the Bank Board). You get the impression that the new Board – on average even less fit for office – must have been even more perfunctory in its deliberations because the Bank neither released nor withheld minutes recording their deliberations on the matter (at their very first meeting on their first day in office, 1 July). Note that not even the Bank’s own self-review of monetary policy was yet available to either Board.

The Reserve Bank OIA response was not, however, the only relevant one. When Orr was reappointed I lodged requests with the Bank, The Treasury, and with the Minister of Finance. They all obviously coordinated their responses since all three were late and all three finally arrived on the same day.

What was interesting in these releases is what wasn’t there (not what was done but withheld, but what appears never to have been done). Thus one of the better aspects of the amended Reserve Bank legislation was supposed to be a heightened and more formalised role for The Treasury in monitoring the Bank on behalf of the Minister of Finance. But there is no advice at all from The Treasury to the Minister of Finance on the substantive pros and cons of reappointing the Governor even though (a) Treasury had just taken on a new heightened role and responsibility, and (b) the question of reappointment was arising amid the biggest monetary policy failure for decades. They drafted the Cabinet paper for the Minister of Finance to reflect the Minister’s own views, but that seems to have been all. There is no sign Treasury was even made aware, let alone asked for advice, when the two Opposition parties raised concerns about the proposed reappointment, even though this was the first time such consultation provisions had existed for a Governor appointment.

As often seems to be the case, the Minister of Finance’s response was fullest, although there were these documents withheld

Intriguing, since there is no sign in any of the other documents of any legal doubts about the ability to reappoint (and all these documents pre-date the letter from Quigley cotaining the Board’s recommendation to reappoint Orr).

The statutory provisions the Minister had inserted require the Minister of Finance to consult other parties in Parliament before recommended to the Governor-General the (re)appointment of a Governor. It was an interesting addition to the legislation (and arguably there is a stronger case for such a provision for the Governor than for Board members, where the record indicates that the Minister had already treated the consultation provision as no more than a cosmetic hoop to jump through on the way to doing whatever he wanted) and certainly suggested an intent that anyone appointed as Governor should at least command the grudging acceptance of other political parties (perhaps especially the major ones) given the huge discretionary power the Governor, Bank and Governor-dominated MPC wield.

Here is the body of the letter sent to the other parties on 19 September

Interestingly, the letter makes no substantive case for the proposed reappointment, addresses nothing (good or ill) about his record etc. I guess parties might be presumed to know Orr, but it still seems a little curious to make not even a one sentence case. But that is the Minister’s choice.

Three of the four non-Labour parties in Parliament responded (the Maori Party did not). This was the response from Genter/Shaw for the Greens

Being an unserious party, they supported reappointment because of things the Bank and Governor have no statutory responsibility for.

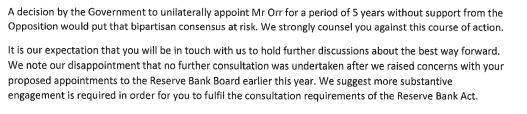

Both National and ACT expressed opposition to the reappointment. The letter from Nicola Willis has been released previously and so I won’t clutter the post by reproducing it all here. Their opposition was on the (deeply flawed) ground that they believed no five year appointment should be made for a term starting in election year (even though the starting date for the second term was in March 2023 and the election then seemed likely to be in October or November). However, Willis ended her letter this way.

Willis has since described the reappointment as “appalling”, but seems to continue to rely on the argument about a five-year term even though (as I’ve pointed out previously) their 2017 comparison is flawed and the legislation has always been designed deliberately not to make it easy for new governments, of whatever stripe, to come in and appoint their own person.

We had known that ACT was opposed to the reappointment but had not seen the body of Seymour’s letter back to Robertson. It is a couple of pages long and raises substantive concerns about both style and policy substance (but rightly not questioning the ability of the government to make a five year appointment). It has a distinctive Seymour style to it (and so even as an Orr sceptic some lines jar with me) but it is an undeniably serious document, in response to the first ever statutorily-required political party consultation over the appointment of a Governor.

But it was all just ignored. This is what little the Minister of Finance told Cabinet

so not even a hint as to the nature of the concerns the Opposition parties had expressed, or any reflection on what expectations (around multi-party acceptance, if not endorsement) the government’s own legislation might have given rise to.

After the Cabinet paper had been lodged, Robertson did write back to Nicola Willis in a fairly substantive letter (the full text of this and other documents is in here)

Robertson OIA on Orr reappointment 2022

The Minister rightly pushes back on the argument about pre-election appointments, highlighting the substantial differences to the 2017 case (and actually makes the interesting point, that I had not noticed, that the law provides for only a single reappointment, so any one year term for Orr would have to have been his final term).

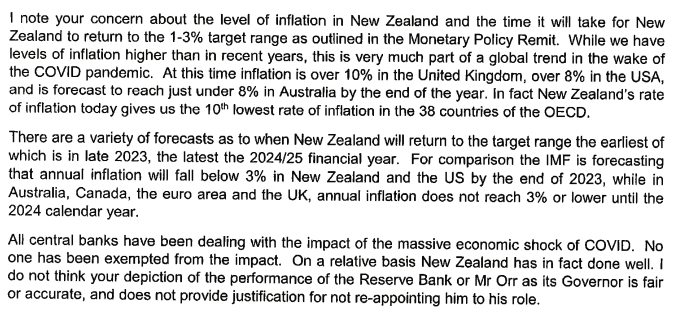

Perhaps of more substantive interest are the comments from the Minister on the Governor’s monetary policy stewardship

A lot more spin than substance, that fails (completely but no doubt deliberately) to distinguish things central banks are responsible for and those they aren’t really, chooses not to distinguish shocks that New Zealand did not face (eg global gas prices), and in the end is simply complacent about the serious core inflation outbreaks here and everywhere else. There is no sense of any accountability.

The Minister’s letter ends this way

Not only has the entire legislative structure long been built around a model in which the Minister of Finance has always been free to reject a nominee (but cannot impose his or her own favourite) but it was Robertson’s own government that added the political party consultation provisions. Rejecting an Orr nomination – especially after both Opposition parties had expressed serious concerns – would not to have been to politicise the process, but would simply have been the Minister of Finance doing his job. As it is, the risk now is that the consultation provisions will come to be regarded just as an empty shell.

Those paragraphs above from the Minister’s letter to Willis are nonetheless of some interest because they are the only material, across three separate OIA responses, even mentioning the conduct of monetary policy on the Governor’s watch. In the Board minutes (see above) there was no sign of any consideration or analytical input (not that none of the Board members really had the capability to provide such an assessment themselves. In the Quigley letter to Robertson there is this

which is not only input-focused (rather than outcomes), focused on March 2020 (rather than the aftermath), but shows no sign of any critical reflection or evaluation. And in the Minister’s paper to Cabinet monetary policy and inflation – let alone $9bn of avoidable losses to the taxpayer – get no mention at all, just burble about Orr as a change manager (leading decline and fall perhaps?)

It was a poor appointment (my long list of reasons was in this post) even if one that was always to have been expected, since Robertson had never displayed any serious interest in accountability or performance, or much in the substance of the Bank’s role at all (and failure to reappoint might have risked raising questions about the government itself). But it is still a little surprising how short on substance, around the key failings of the Governor in recent years (style and substance), the documented parts of the process leading to reappointment seem to have been.

There are, of course, some levers open to a new National/ACT government were they to win the election, but it would be a little surprising if they do much at all. More likely, the decline and fall of a now bloated and unfocused institution will continue through Orr’s second (and apparently final) term.