I was tempted to head-up this belated MPS post “Je ne regrette rien”, as that – I regret nothing (about last year’s monetary policy) – was what Orr told yesterday’s press conference as he was getting rattled towards the end. He should regret quite a bit – notably the $5.7 billion of taxpayer losses on the LSAP, and the ongoing huge risks (neither were points he was willing to engage on, whether in the MPS, in the press conference, or at FEC this morning – indeed he actively played distraction). But that isn’t really where I want to focus my thoughts on the Monetary Policy Statement.

I thought the MPC should have raised the OCR by 50 points. The MPC disagreed, and moved by only 25 points. That is their choice of course, but – once again – I was struck by just how lacking and inadequate the supporting analysis and argumentation were, on their own terms (ie relative to their own published forecasts). No informed reader – and there won’t be many other readers of their 56 pages – will have come away feeling persuaded by the insights and analysis the Bank’s big team of macroeconomists had generated. There was nothing new or insightful, at least that I could see. And much that wasn’t convincing.

As I’ve noted on various previous occasions, when there are big starting point surprises, surely we expect to hear from the MPC (a) why they think they got things wrong, and (b) what that mistake – and mistakes are inevitable in such areas – has taught them about how the economy is behaving and how, if at all, it changes their view about the road ahead. But once again, there was none of that (in fact, in the press conference again played distraction suggesting that the surprise was the lockdowns after August, whereas the September quarter unemployment and (core) inflation surprises really had nothing much to do with those lockdowns (which will, of course, have a big impact on September and December GDP). Their August projections/discussion had suggested something fairly unproblematic on core inflation, and instead they suddenly found themselves with outcomes near the very top of the range, and so on.

Their discussion of inflation expectations also lacked structure, consistency, and any sense of authority. In the minutes of the MPC meeting we were told

The Committee noted that near-term inflation expectations tend to move with actual inflation. Medium-term measures provide a better gauge of whether inflation expectations remain anchored, and these remain close to the target midpoint.

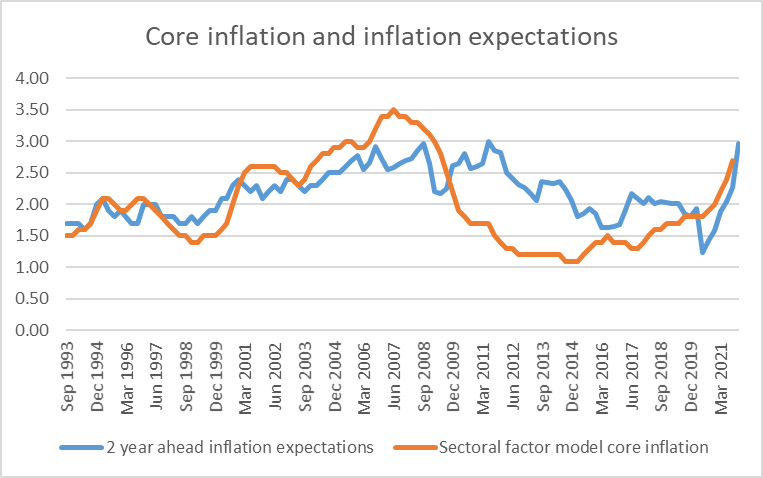

The message seems to be one of nothing to worry about at all. But even the story is misleading, at best. It is certainly true that year-ahead survey measures of inflation expectations seem to be very driven by fluctuations in headline inflation, but here is the two year ahead measure (from the Bank’s own survey) lined up against their (historically) preferred – and most stable – measure of core inflation. Inflation expectations – over almost 30 years – have typically fluctuated through materially narrower ranges than core inflation itself. The exception – potentially important exception – has been the last two years. If anything, the two year ahead expectation could be disconcertingly high already, given the extent of the rise in core inflation itself.

Then there is that claim that all is fine because long-term inflation expectations haven’t changed much. The Bank asks about expectations five and ten years ahead, and outcomes are not far from 2 per cent – as you would hope, given the target, but only because respondents presumably expect the MPC to act sufficiently aggressive to keep inflation near the centre of the target range. If those five and ten year expectations started moving up sharply there really would be cause for concern, but the fact they are still near 2 per cent shouldn’t be telling MPC anything about the appropriate policy stance now.

At the press conference one offshore questioner asked the Governor about the MPC’s response to the big increase in inflation expectations, given the Risk Appetite Statement included in the MPC in which they asserted that “they had a low appetite for policies or decisions that could cause inflation expectations to become unanchored”. This was greeted with a glib and dismissive response from Orr along the lines of “we have reacted and raised the OCR”, not even engaging with the fact that (for example) two year ahead expectations are now a full per cent higher than they were in February, and yet the OCR has been increased by only 50 basis points over that time, there isn’t another review until February, and the MPC has stated that they prefer to move in 25 point bites. At best, it will be the end of March before the OCR will have been raised by 100 basis points, but even that won’t have raised real interest rates at all relative to the start of this year (let alone relative to the start of last year). Perhaps expectations will have moved even higher – outside the target range in the meantime. Perhaps not, but surely we should have expected a more thoughtful nuanced and engaged treatment of the issues and risks? Core inflation has, after all, already increased a lot (and – which we will come to – even they seem to expect it to increase further).

Similarly, we are told that the Bank’s projections have the OCR rising to above (the Bank’s estimate of) the neutral OCR. They seem to base that on this portrayal of neutral.

But this chart seems not to have taken any account at all of a jump in inflation expectations. The Governor said they mattered – and that the Bank had responded – but there is no sign they do so in this estimate of neutral. Given the Bank’s inflation forecasts it seems unlikely that medium-term inflation expectations will be dropping any time soon, and if those survey numbers are capturing something real, doesn’t that mean the OCR needs to go (quite a bit) higher than they might otherwise have thought. Now personally I’m very sceptical of the value of medium-term projections, but it is the Bank that uses them as a storytelling device and yet quite a material (and identifiable) part of the story seems to be have been left out.

And so it goes on. The best question I’ve heard about yesterday’s MPS was from a first year economics student, who wanted to know how the Bank could claim to be fulfilling its mandate when it projects that inflation next year will be 3.3 per cent. I haven’t seen any attention paid to what that number means. Recall that it is now November 2021. Nothing about the year to December 2022 has happened yet. So the Bank’s forecasts for inflation next year must be very close to a forecast of core inflation (they don’t know the inevitable one-off shocks – up or down – and they assume the exchange rate is fairly stable). Core inflation is currently about 2.7 per cent and the Bank is quite content to see it rise to 3.3 per cent – outside the target range. When a press conference questioner asked a similar question, she again got a dismissive (and obfuscatory answer). It might be one thing to take things slowly if the unemployment rate was still lingering high, but the Bank is quite open that at present the unemployment rate is below a sustainable level. So raising the OCR more and more quickly wouldn’t be kicking the economy into recession – the Governor’s claim – but would just get both dimensions of their dual mandate back towards desired levels sooner (and with less risk to those pesky inflation expectations). As it is, the Bank’s forecast for the unemployment rate in March 2022 is a tough lower than it was in the latest official release. This is an economy that – on their numbers – has been overheating, and they can’t even manage of Taylor principle scale of response, not even when the unemployment rate is – on their telling -unsustainably low. Perhaps there is a case to be made for their choice, but neither the MPC nor the Governor made it.

I could go on at some length on other matters, but just a few bullet points instead:

- it is sobering to see how pessimistic the Bank now is about productivity prospects (0.5 to 0.6 per cent for annum across the forecast horizon). The Bank has no particular expertise in productivity, but they just now take for granted our woeful performance

- it was curious to see a lengthy Risk Appetite Statement in the document. Doubly curious in that more space was given to (for example) the risk of an MPC member missing a meeting than to (nothing at all) the huge financial risks decisions like the LSAP programme expose the taxpayer too,

- the Bank is all over the place on the LSAP (all while refusing to seriously address the losses, just waving the hands about “overall gains). They seem oblivious to the international research that suggests the stock of bonds held is what makes any useful macro difference, asserting that the programme was previously making a big difference, but now makes only a small difference. And once again they refused any serious answers about the future of the LSAP, claiming that a document is coming in February. Similarly, they make laughable claims about why the Funding for Lending Programme needs to be kept open, Orr even suggesting to FEC that were they to close this crisis tool now (a year or more after the crisis) it might pose a future financial stability threat,

- there were pages and pages on climate change. As far as I could tell, all they seemed to focus on was direct price effects, and even then had nothing to say other than “some relative prices will rise”. No doubt and – by definition – others will fall. Orr claimed there was going to be unusual volality in headline inflation relative to core, but offered not a shred of analysis in support of his claim (we’ve had lots of shocks and policy reforms in decades past). And, somewhat surprisingly, they didn’t even touch on any effects on the neutral interest rates – if there is any effect (and I suspect that any effect will be vanishingly small) it is likely to lower neutral rates a bit.

- remarkably, there was almost nothing in the document offering insights based on the experiences of other countries. Again, with a big team of economists and access to overseas central banks you’d hope that the Bank’s thinking would be informed by the diverse experiences other central banks are observing. But there was nothing.

All in all, it was a fairly typically poor Reserve Bank performance, perhaps undershooting even my low expectations. It was good that some questions were asked – at the press conference and at FEC – about the high turnover at the top of the Bank, even if Orr was allowed to get away much too easily with ludicrous claims about what a desirable place the Bank was to work, what an abundance of talent they had available etc etc. It certainly wasn’t on display in this document.

(On the turnover question, one almost had to feel sorry for the Chief Economist who has been restructured out: asked by MPs about what was going on Orr rashly talked about how Yuong Ha “has chosen to go into a far more challenging role. What are you going to be doing?” There was a noticeable, whereupon Ha lamely responded “Coaching my son’s cricket team. Taking a break”. Orr seemed to display all the sensitivity and personnel management skill of, say, a Judith Collins.)

Reblogged this on Utopia, you are standing in it!.

LikeLiked by 1 person

It would seem that the Governor is vying to outdo Boris Johnson’s ‘Peppa Pig Farm’ performance….Apparently off to Zealandia we must go….“arum arum aaaaaaaaag”..in the words of Boris.

LikeLiked by 2 people

You underestimate the problems of running a children’s cricket team. I wouldn’t touch that job with a bargepole whereas once a month tweaking something I don’t understand called the OCR and waiting to see what happens is well within my capabilities. Being paid to do it would be a bonus.

LikeLiked by 2 people

No doubt true re the cricket teams….

That said, the chief economist role is mostly a fairly big mgmt job, with endless endless meetings.

LikeLiked by 2 people

Thank You, Michael for your mail , We are indebted.

DJB

LikeLiked by 1 person

Circa 67% of fixed rate mortgages to reset over the next year….that’ll crimp demand…especially as bank widen spreads to maintain ROE…given the ‘E’ is moving higher.

LikeLike

It is one of the things I agree with Orr on: monetary policy works. It is just that on their own numbers having moved only 50bps this year should not be enough.

LikeLike

Really interesting analysis.

A couple of comments

The impact of MP on productivity seems really important.

NZ productivity has been abysmal for decades,which seems to follow inversely the interest / exchange rates.

Small incremental lifts in the OCR are not likely to address inflation effectively ,particularly if economic lag isn’t considered.

Do these comments have validity in your view?

.Thanks

LikeLike

I don’t think mon pol is responsible for our productivity problems, even though I think persistently high average real interest and exchange rates are (mon pol affects those variables in the short-term, but the fundamental influences matter in 5-30 year horizons).

On your second point, yes if one believes the Bank’s story it seems at best risky to think that in these circs slow gradual OCR rises are the best way to go. Anything could happen – shocks happen – but the data as we see it now supports something stronger earlier.

LikeLike

Wow, that media conference is hard to watch. When the governor gets questions that are even mildly critical of the RB’s performance he is very abrasive, dismissive and downright rude. He really needs to adjust his personal style. If that is the accountability process playing out, then it is not working.

LikeLike

He wasn’t much better -altho had to be a little more polite – FEC. He relishes being a cheerleader and then brings all the bonhomie to the table, but challenge or questioning he just does not cope well with (and seems unwilling/unable even to mask it).

LikeLike

Climate Change

Michael, I enjoy reding your writings. What Orr would know about climate change I suspect you could write on the back of a stamp with a felt pen! What on earth it has to do with the bank’s projections, I fail to see. Perhaps a good way to keep in with the woke brigade.

I have recently written an article for the CountryWide magazine, attached .. keep up the good work.

Jock Jock Allison 9 Arthur St., Dunedin, 9016, New Zealand. Phone 6434772903 Mobile 6421363337 email jock.allison85@gmail.com

On Thu, Nov 25, 2021 at 3:52 PM croaking cassandra wrote:

> Michael Reddell posted: ” I was tempted to head-up this belated MPS post > “Je ne regrette rien”, as that – I regret nothing (about last year’s > monetary policy) – was what Orr told yesterday’s press conference as he was > getting rattled towards the end. He should regret quite a b” >

LikeLike

I read the Bank’s justification for their 25 bp decision and it seemed to be well argued and prudent. After all, interest rates, most notably mortgage rates, have already risen – spectacularly – irrespective of the OCR. The ongoing uncertainty over Covid has knocked business confidence, the mindless, authoritarian and seemingly arbitrary Government measures being foisted upon a highly vaccinated public are worrying about the future, not to mention the financial pain and uncertainty being felt by swathes of the business community, all point to a 25 bp move and a slow but steady approach.

Very little seems to be being said about the types of inflation afflicting us. A lot of the inflation we are seeing is imported, and exacerbated by supply chain woes. Higher interest rates won’t directly affect this kind of inflation will it? In addition, won’t higher interest rates just make the appetite for business investment – in these uncertain times – even weaker? Interest rates seem an incredibly blunt tool in circumstances where you have sections of the working population whose incomes are fine, even growing; while others sectors are still suffering amid uncertainty. The lockdowns themselves surely take part of the inflationary blame with lockdowns constricting economic activity and supply without constricting demand as much, given the billions being paid out. It seems to me one concrete way of getting things back to normal and perhaps even reduce supply-side induced inflation – which should be possible given high vaccination rates – is to restore all freedoms and remove all restrictions immediately.

Just some thoughts, anyway.

LikeLike

Re your second para, I guess that is why it is important to keep clear the distinction between headline and core inflation. I mostly focus on the latters. On your final point, I’m not sure what the effect of removing all controls would be, since presumably it would be accompanied with an upsurge in fear about a significant virus outbreak.

LikeLike