When the Reserve Bank and Treasury advertised a full-day workshop with the title “Fiscal and Monetary Policy in the wake of COVID”, I immediately signed up to attend. It sounded like a good idea for an event. After all, lots of tools were deployed, some new, some old, some deployed less than usual, some much more. And we’ve had a Budget, and projections from both agencies suggesting that the economy is now getting pretty close to operating at full capacity (albeit a capacity a little diminished by Covid restrictions).

It was just a shame about the execution. Notably, even though monetary policy has been the principal tool for macroeconomic cyclical stabilisation for decades – and not just since 1989 – here and abroad, there was not a single paper looking at the role of monetary policy, past, present or future. The Governor didn’t attend – which is fine – but nothing of substance was heard from any senior Bank figure. Orr’s deputy for macro policy, Christian (“The Future is Maori”) Hawkesby contented himself with opening remarks that had just some bonhomie and his recitation of a Treasury prayer (which, to add to the strangeness, seemed to appreciate “skilled workers” but not the rest of the public), but not a word of substance. There were a couple of technical papers from Reserve Bank researchers in the afternoon session, but one was little more than an early-stage in a research agenda on the distributional aspects of monetary policy (the paper itself couldn’t shed much light when the only asset in the model was bonds), and the other – on dual mandates – didn’t seem to offer any fresh insight.

So the stage was largely left to The Treasury, and particularly a series of three papers (complemented by a presentation from a US academic) that seemed dead-set on making the case for a bigger and more expansive role for fiscal policy and government debt in the new post-Covid world. Bureaucrats making the case for a bigger and more powerful bureau.

First up – and clearly most important – was the Secretary to the Treasury. She spoke for 40 minutes, but then took no questions (and, in an amateur-hour effort, the text of her speech was then not available until more than a day later). The Secretary is still quite new to the country, to the job, and to national economic policy matters. Probably most non-government attendees (of whom there were many, in a well-attended event) had seen and heard little or nothing of her before. So it didn’t speak well of her that she wasn’t willing to engage, despite having made a barely-disguised (“I would stress that we are not making policy recommendations”) bid for quite an upending of the way macro management is done her, in ways that would just happen to favour her agency.

But what of the substance? It was a workmanlike effort (NB with a minor mistake in footnote 2) but hardly persuasive to anyone not already champing at the bit for fiscal policy to do well. For example, there was no serious discussion about the effectiveness of monetary policy. The Governor has previously told us he thinks monetary policy has been as effective as ever. The Secretary seems to disagree, but we can’t be sure – perhaps she just thinks fiscal policy is even better, but she doesn’t make that case either. Much in her case seems to rest on the effective lower bound on nominal interest rates but (a) as the next Treasury speaker acknowledged that is not some immoveable barrier, and (b) she offers no thoughts on the effectiveness or otherwise of things like the LSAP programme. Surely one starting point for thinking about the future might involve some careful diagnostic work reaching a thoughtful view on what roles the various elements of fiscal and monetary policy played in economic outcomes over the last 15 months. But neither she, nor anyone else on the day, attempted anything of that sort. Remarkably no one – from the Bank or Treasury – looked at the options and merits for removing – or greatly easing – the ELB so that at least ministers have effective choices in future severe downturns,

Quite a bit of Treasury’s thinking – or at least their marketing – seems to have been shaped by the success of the wage subsidy scheme. And it was a success – getting money out the door quickly, at a time when the government had just done the unprecedented and (a) shut the borders, and (b) simply compelled most people not to go to work, or do anything much else. It provided immediate income support, and probably had some beneficial effects beyond that (some smart person might attempt to model what difference it has made to outcomes not just last March/April but now). But it isn’t exactly a conventional event of the sort we can expect to see every cycle. And the primary consideration wasn’t really macroeconomic stabilisation at all – the whole point of the lockdowns was to aggressively (but temporarily) reduce activity, including economic activity – but income relief/support (as unemployment benefits have an incidental automatic stabiliser benefit, but aren’t primarily about macroeconomics). There are always going to be one-off events when the the government’s spending capabilities need to come into play – one can think of earthquakes (where fiscal measures and monetary policy will often tend to work in opposite directions, since earthquakes cause real disruptions and significant wealth losses, and but also generate a lot of fresh (reconstruction demand), plagues, wars, and so on. But it is seems like a category error to use such episodes as the basis for some sort of generalised play for more routine use of discretionary fiscal policy with cyclical stabilisation in view, when most recessions are quite different in character.

And even just thinking about the last 15 months or so, neither the Secretary nor her colleagues seemed to make any effort to unpick the effects of the wage subsidy scheme from the rest of the fiscal policy initiatives of the last year. One could easily imagine an alternative world in which the wage subsidy was used much as it was, but otherwise fiscal policy was kept much on the path it had been on at the start of last year, and at the same time the OCR was used more aggressively. How different would the outcomes for the economy have been, in aggregate and sectorally? The fiscal option involves the coercive use of state power, and politicians making discretionary choices playing favourites, while monetary policy adjusts relative prices and then let individuals make choices about how they (personally and individually) are placed to respond. And one thing that was striking about both the Secretary’s speech and the more technical discussion that followed from her colleague Oscar Parkyn is that in all their new enthusiasm for using fiscal policy more aggressively in downturns (and monetary policy less so) is that neither mentioned, even once, the exchange rate – typically a significant element in the adjustment mechanism in New Zealand recessions. New Zealand recessions often see sharp falls in international commodity prices (fortunately not this time) and the lower exchange rate acts as a buffer. But a much heavier routine reliance on fiscal policy will tend, all else equal, to hold up the exchange rate relatively more in downturns. It isn’t obvious – without a lot more analysis – that that would be a good thing.

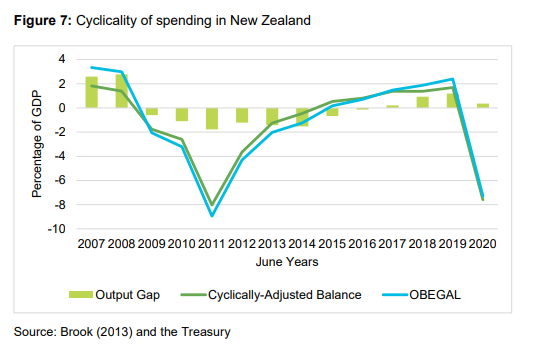

The Secretary included this chart in her speech

It was apparently designed to show that fiscal policy in New Zealand has generally done sensible things. That might be generally true (although if so why change?), even setting aside the huge pressure loosening fiscal policy put on monetary conditions over 2005-2008, but it conveniently ignores where we are right now. This chart, which I’ve shown before, is from the recent Budget documents.

So with the output gap almost closed, the cyclically-adjusted primary balance (deficit) in 2021/22 year is expected to be almost as large as it was in 2019/20 (when the – sensible – big wage subsidy spending was concentrated. Extraordinarily, in a speech bidding for a more active role for fiscal policy in cyclical stabilisation she never mentioned this situation once – let alone engaged with why, from a macro policy perspective, such big deficits make sense now. As sceptic might suggest that this is the real world outcome when the Secretary’s textbook ideas get given some rope.

One could go on. The Treasury is clearly tantalised by the lower interest rates – although not now lower than pre-Covid – and the “appeal” of taking on more debt. But never once did we hear any serious examination of the typical real-world quality of the marginal additional public spending they had in mind (it wasn’t until the panel discussion late in the day that I heard a Treasury official – a temporary one, so perhaps not well-socialised – refer to the Auckland cycleway bridge). There was a paper reporting some model results suggesting, sensibly enough, that fiscal consolidation is most costly to GDP if done via taxes on capital income, but (symmetrically) there wasn’t a sense in the rest of the day that (say) Treasury was champing at the bit to lower company taxes. Rather they seem keen on public infrastructure – which often sounds good on paper, until we get to the concrete ideas. As it was, a discussant cast considerable doubt on one Treasury paper suggesting high payoffs to more government infrastructure spending.

We also never really heard any serious political economy discussion, or even a discussion of how we should think of the government balance sheet – is it a plaything for politicians or should it be best thought of as operating on behalf of citizens, each of whom have to make their own spending and borrowing choices. There wasn’t much about using coercion and compulsion rather than the indirect instruments of monetary policy. And, on the other hand, it was a little surprising that there wasn’t even a mention of MMT – so that in a floating exchange rate, the level of government debt isn’t really likely to be materially constrained by the market, which doesn’t mean that just any level of government debt is a socially good thing.

It was all a bit unsatisfactory really. Perhaps one could say it was just exploratory, and they are wanting to open the issues but (a) the speech was from the Secretary herself and (b) was making a case more than deeply and thoughtfully exploring the issues. We will have to see what more is in the papers they plan to release next week (a draft long-term fiscal statement and a draft insights briefing) but if the energy is with The Treasury at present, it isn’t really clear that they yet have the depth of analysis and engagement to support their enthusiasm.

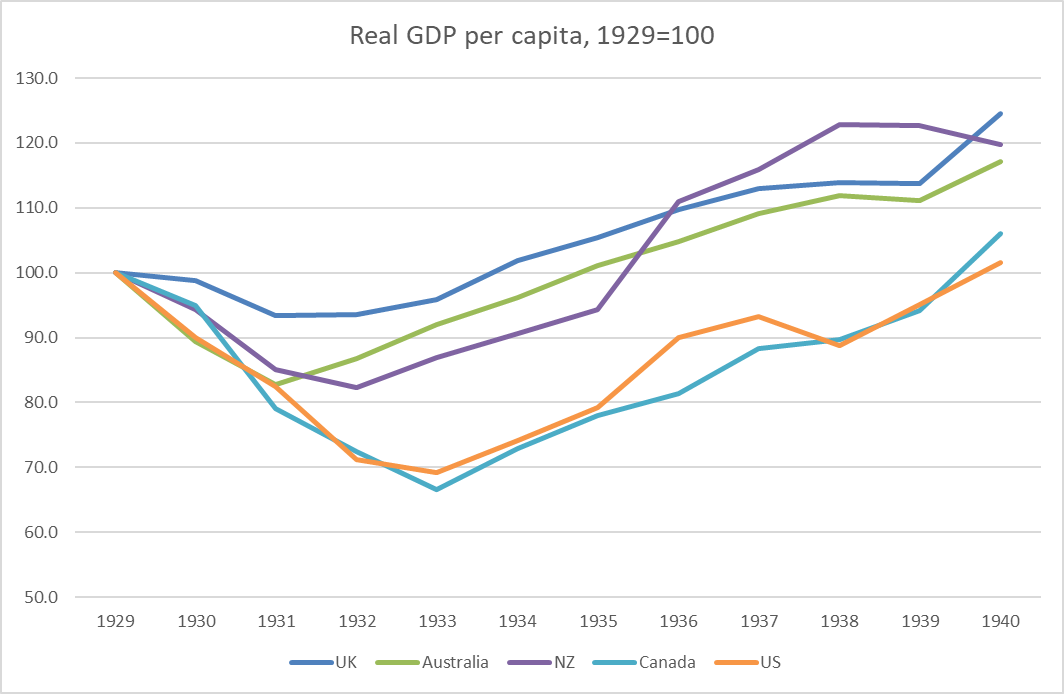

And just finally, they arranged for an American professor, Eric Leeper, to speak, via Zoom, on monetary and fiscal issues. Leeper is pretty highly-regarded and has visited New Zealand previously. He is also very keen on a much greater use of fiscal policy and, it would appear, more debt (for various reasons including, he said. “the rise of the right” which didn’t seem quite relevant to New Zealand, let alone a good basis for official advice). Anyway, after the geeky bits of the presentation, he tried to make his case by reference to the Great Depression. He is clearly a big fan of Franklin Roosevelt, and was talking up the fiscal aspects of Roosevelt’s approach (while barely really mentioning the substantial monetary bits). But it was odd. Here he was talking to a New Zealand audience, championing the use of fiscal policy in the US Great Depression, but seemed quite oblivious to the fact that the US was one of the very last countries to get back to pre-Depression levels of output and unemployment. Here is the experience of the Anglo countries.

Those aren’t small differences. And as anyone who knows New Zealand economic history – or have read my past posts on it – New Zealand’s recovery from the Depression (back to pre-Depression levels by the time Labour took office) was barely at all about fiscal policy. The excellent quote from Keynes that our Minister of Finance of the time recorded in his diary, along the lines of: “if I were you I would no doubt seek to borrow, but if were your bankers I should be very reluctant to lend to you”.

When a half-baked loaf is finished cooking it can be a fine thing, but this loaf seems to need a lot more work before New Zealanders should be rushing to embrace a much more active role for fiscal policy or a lot more public debt. That includes a lot more work on what we reasonably can, and can’t, do with monetary policy.

UPDATE: A former RB colleague, now a lecturer at Sydney University, sent me a link to a paper he and a Reserve Bank researcher have written attempting to evaluate the impact of the New Zealand wage subsidy scheme. I haven’t yet read it, but it looks very interesting. Here is the end of their abstract

We then study the impact of a large-scale wage subsidy scheme implemented during the lockdown. The policy prevents job losses equivalent to 6.8% of steady state employment. Moreover, we find significant heterogeneity in its impact. The subsidy saves 17% of jobs for workers under the age of 30, but just 3% of jobs for those over 50. Nevertheless, our welfare analysis of fiscal alternatives shows that the young prefer increases in unemployment transfers as this enables greater consumption smoothing across employment states