Yesterday was the Reserve Bank’s six-monthly Financial Stability Report. It might these days almost be almost better labelled the “Make the financial system ever less efficient report”, and with little real challenge or scrutiny from the assembled media.

With the Governor off sick it was left to the Deputy Governor Geoff Bascand to front the press conference. He seemed ill-at-ease and a bit uncomfortable in the spotlight – surprising in one who has held senior positions for so long – and often offered answers that were longwinded without actually saying much.

One of the questions he was asked on several occasions was about the reforms announced last week, and whether they reduced or increased the powers of the Minister of Finance and/or the Bank when it came to imposing direct controls on lending. Bascand never once answered the questions directly, delivering lines about how the new law would provide “greater clarity” but in what he said, and in what he didn’t say, he more or less confirmed the interpretation I ran in a post last week that the de facto powers of the Minister will be reduced – since the Minister will have no say on which tools the Bank can use, whereas under the ad hoc convention of the last decade the macroprudential Memorandum of Understanding between the Bank and the Minister governed that. Under the planned new legislation the Minister will be able to stop the Bank putting in place controls on broad classes of lending (eg residential mortgages) but at least under this government that will be an empty power, since the government is already content with the Bank having LVR restrictions, and the Bank will be free to apply any other controls it likes, whenever it likes. You might think that is a good thing. The Bank probably does. But it hands over much too much power to an unelected unaccountable Board.

But what I really wanted to focus on in this post was the area the Bank itself (and much of the media coverage) focused on: housing.

You would barely get the idea from any of the material that the Bank has no responsibility for housing at all. Its financial regulatory powers over banks have to be exercised to promote the maintenance of a sound and efficient the financial system. And that is pretty much it. The government is in the process of reforming the law to downplay the efficiency dimension, but (a) the law today is as it is, and (b) even under their new law the focus is supposed to be on the soundness of the financial system. A couple of months ago, as is his right, the Minister of Finance issued a direction to the Bank requiring them to “have regard to” this government policy:

But this direction alters neither the statutory purposes the Bank must exercise its powers for, nor alters the Bank’s statutory powers. The Governor promised that the Bank would explain quite what import this section 68b direction actually had, but it appears that that would have been embarrassing or awkward, because no such explanation is offered or attempted in the FSR. In fact, they both misrepresent the substance of the direction, and then do more than suggest that it “aligns well with the Reserve Bank’s objective to promote the maintenance of a sound and efficient financial system”. But bear in mind that not even the Cabinet paper that discussed this direction (and the equally empty change to the monetary policy Remit) envisaged much effect on anything much.

But this direction alters neither the statutory purposes the Bank must exercise its powers for, nor alters the Bank’s statutory powers. The Governor promised that the Bank would explain quite what import this section 68b direction actually had, but it appears that that would have been embarrassing or awkward, because no such explanation is offered or attempted in the FSR. In fact, they both misrepresent the substance of the direction, and then do more than suggest that it “aligns well with the Reserve Bank’s objective to promote the maintenance of a sound and efficient financial system”. But bear in mind that not even the Cabinet paper that discussed this direction (and the equally empty change to the monetary policy Remit) envisaged much effect on anything much.

So we are simply left with those twin goals of maintaining a sound and efficient financial system. But amid all their talk of housing financing restrictions, old, new, and foreshadowed, there is barely a mention of the efficiency of the financial system. Which is probably just as well (for them) as there is no conceivable way that there most recent restrictions, described here, do anything but seriously impede the efficiency of the financial system.

The Bank hasn’t even attempted to make an efficiency case for almost completely banning any loans to residential rental property providers in excess of 60 per cent of the value of the property (all the while allowing much easier access to credit for owner-occupiers). If there are any real differences in the riskiness of such loans, not already factored into pricing and capital requirements, they are small relative to these differences in rules. So what we have isn’t a set of rules that is about either soundness (which capital requirements already manage) or efficiency – in a banking system that has proved itself robust over many years – but purely political interventions, resting on no sound statutory foundations, to attempt to skew the playing field in the housing market, consistent with Labour Party wishes and political preferences. Thanks to the Reserve Bank the market in houses will function less well, and the market in housing finance will be much less efficient and effective (and that without even addressing the “new homes” carve-outs, which again are all about politics and not at all about risk – new developments tend to be riskier – or efficiency).

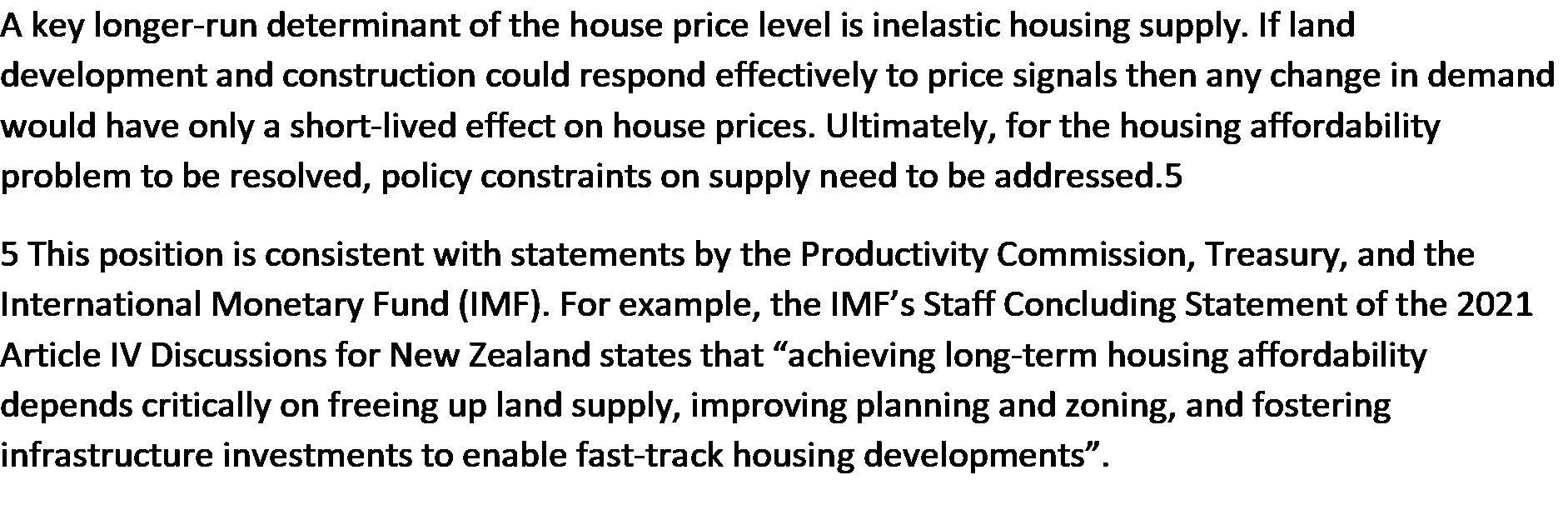

Now, on a good day there are still some shreds of economic rationality and logic buried somewhere in the Bank. Deep in the FSR we find this good paragraph

I especially liked that slightly desperate footnote “see it isn’t only us”.

Now the Reserve Bank can’t fix any of that stuff – it is all about central and and local government failure – but they are nonetheless quite happy to operate beyond their legitimate sphere and powers to feed a government narrative and paper over symptoms. providing aid and comfort to the government doing little to get to the heart of the issue (the government that disavows any suggestion that perhaps house/land prices should fall). But that’s Orr for you.

Now perhaps you are thinking “but isn’t the financial system imperilled by these higher house/land prices?” Well, the Bank itself doesn’t think so and in the rest of the report they are at pains to stress how resilient the system is, how sound the banks are – even while being just about to resume their never-well-justified drive to push further up capital ratios that are, in effect, already among the very highest in the world. At the press conference, the Bank was at pains to note that the system could cope quite well with even a large fall in house prices. The Deputy Governor rightly highlighted that if prices fell recent borrowers might be in a difficult position, especially if for some reason the unemployment rate was to rise a lot at the same time but…….that simply isn’t a financial system soundness issue.

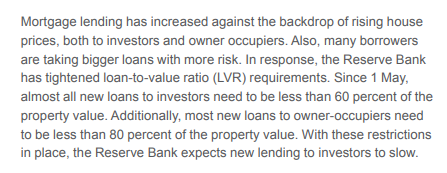

Much of the discussion in the document and in the press conference etc was about what fresh horrors – housing finance interventions – the Reserve Bank might be cooking up, in league with the government. Unsurprisingly perhaps – since they’ve wanted this tool for years – their preference seems to a debt to income limit (or a series of them, perhaps further impairing the efficiency of the system by picking favourites). Even the Bank seems to recognise that LVR limits are already so tight, especially on residential rental providers, that it might be embarrassingly inconsistent with their mandate to go further, and (sensibly) they don’t seem at all keen on banning interest-only mortgages. It is all a bit hypothetical at present – since as they note the latest LVR controls only came into effect last week – but there is no stopping a bureaucrat with an agenda (Bascand used to be regarded as a fairly pro-market economist), so we heard lots of talk about what they’d be prepared to do “if needed”. There were no criteria outlined for what might warrant further interventions, let alone criteria grounded in the Bank’s act. It really was handwaving stuff, of the sort we might once have been familiar with under people like Walter Nash or the later Muldoon.

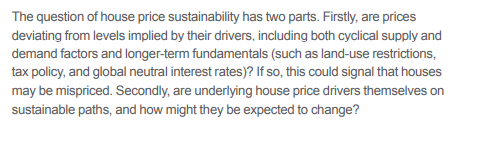

You will note that the Minister’s direction referred to the government’s desire to support “more sustainable house prices”. The Bank has picked up that line and has clearly been toying with how to give it substance – but appeared to have made little or not progress, one of their staff even suggesting it was a new phrase and there wasn’t much research around about it. All the FSR itself says is this

And that’s it. And it didn’t seem to have taken them far. Bascand claimed to be optimistic that in time the Bank would be in a position to opine regularly on whether house/land prices were above, below, or close to sustainable levels, but he offered no real hint of what he thought sustainability might mean in this context, let alone attempting to tie it back to the Bank’s actual role, around the soundness of the system. For now – clearly keen not to get out of step with his political masters – he couldn’t even bring himself to suggest that lower house prices would be a good thing, although for some reason he did claim (on RNZ this morning) that a gradual fall would be better than a sharp one (offering no clue on why the death from a thousand cuts might be preferable, and for whom).

And, from the few hints he offered, his concept of sustainability seemed idiosyncratic to say the least. Apparently if the population was trending up it was okay for house prices to rise and stay up – quite why was never stated (and he ran this population line several times). We heard a lot about interest rates, but no real suggestion as to why low long-term global neutral interest rates supposedly mean higher house prices (they don’t seem to in much of the US, places where it is easy to bring land into development). It was just a muddle. I guess he couldn’t bring himself to say that no sustained fall in house/land prices was likely unless/until the government sorted out the regulatory dysfunction around land use, nor could he easily own up to the fact that if such laws seemed set to remain problematic then, with well-capitalised banks, what was any of this to do with the Reserve Bank.

It really was all over the place, not well-grounded in any of the Bank’s statutory roles, and yet…….these are the people the government wants to hand more discretionary power to, to further mess up access to finance. It was all too characteristic of the pervasive decline in the quality of policymakers (political and official) and policy advisory institutions in this country.

The sprawling burble continued with questions about whether banks should lend more to things other than housing – one veteran journalist apparently being exercised that a large private bank had freely made choices that meant 69 per cent of its loan were for houses. Instead of simply pushing back and noting that how banks ran their businesses and which borrowers they lend to, for what purposes, was really a matter for them and their shareholders – subject, of course, to overall Reserve Bank capital requirements – we got handwringing about New Zealand savings choices etc etc, none of which – even if there were any analytical foundation to it – has anything to do with the Bank. (He did, in fairness, note that there wasn’t much sign of strong business credit demand.) But I guess once you start down the path of the highly regulatory and intrusive state, it is hard to get free of the tar baby – in fact, bureaucratic life then selects for the sort of people who relish this stuff.

On a quite different topic, there was a box in the FSR on what was described as “Maori access to capital”. The Bank has apparently decided that, with no evidence whatever that there are distinctive Maori issues around either monetary policy or financial stability, to spend scarce public resources promoting this sort of stuff. Again, it is all highly non-analytical – no sense, for example, of why these ill-identified so-called Maori issues (in the ambit of the Bank’s functions) might be different than those of (say) ethnic Indians or Chinese, Catholics or atheists, left-handers, ethnic Samoans, women, men or whoever. It is all just a political whim, pursuing the personal ideological agendas of the Governor and at least some of his senior management (one of his offsiders has an extraordinarily political speech out this morning).

Anyway, we are told that

This work aims to use the Te Ao Māori strategy to incorporate a long-term, intergenerational view of wellbeing into the Reserve Bank’s core functions. It will also inform the Reserve Bank’s financial inclusion work and the allocative efficiency elements of its monetary policy and financial stability mandates. The Reserve Bank is treating this work as a high priority within its strategic work programme.

So with no serious problem identification, no serious grounding in the Bank’s statutory functions (which incidentally have no “intergenerational” character at all) all this is – in the Governor’s view – a high priority use of scarce public resources.

One can’t help feel that the Bank’s core functions might be in need of any spare resources they happen to have.

Michael, you refer to the Bank’s Te Ao Maori Strategy. https://www.rbnz.govt.nz/about-us/te-ao-maori-strategy

In that, the RBNZ claims to be guardians of our economy as well as our financial system and says its “core mandate” is to “promote the wellbeing and prosperity of all New Zealanders.”

Hard to see how that aligns with its statutory mandate? Slight overreach perhaps?

LikeLike

And even its “core mandate” misrepresents the statute. The key words in the second line of this is “by” – ie they are supposed to do mon pol and advance a sound financial system, which – of course – is stated by Parliament to be for the good of NZers. Wellbeing etc is not some independent role or goal

1APurpose

(1) The purpose of this Act is to promote the prosperity and well-being of New Zealanders, and contribute to a sustainable and productive economy, by providing for the Reserve Bank of New Zealand, as the central bank, to be responsible for—

(a) formulating and implementing monetary policy directed to the economic objectives set out in subsection (1A), while recognising the Crown’s right to determine economic policy; and

(b) promoting the maintenance of a sound and efficient financial system; and

(c) issuing bank notes and coins in New Zealand to meet the needs of the public; and

(d) carrying out other functions, and exercising powers, specified in this Act.

(1A) The economic objectives are—

(a) achieving and maintaining stability in the general level of prices over the medium term; and

(b) supporting maximum sustainable employment.

LikeLike

I guess there could be some element of the RB trying to save people from themselves even if the banks can afford to lose money from loans going bad?

I do query whether the government can really stop house prices falling when supply catches up with demand?

LikeLike

I’m sure there is something to what you say in your first sentence, but (a) it isn’t their job, and (b) perhaps more importantly, says he soberly and conscious of his own past, the Bank has run such lines for decades (someone the other day dug out a newspaper article of Alan Bollard in 2003 issuing such warnings to recent buyers, and I’m pretty sure we were anguishing back in 96/97 as well). We didn’t have a good model in mind then (of course we didn’t realise that) and there is little sign the Bank does now.

LikeLike

Once again we fiddle. Interventions beget further interventions to correct the prior. Picking over the bones of legislation pertaining to the reserve bank does not give any clarity of direction and purpose. The RB is a child of political play,perhaps dressups could be the game. I am sure as the agenda of a dual state becomes more apparant the act(s) governing the RB will be morphed some social arm of government policy. At least those with skin in the game , the trading banks and lesser intermediaries will know not to rely on the RB in any event. Culture dominates politics and politics trumps economics. The cultural stench will trickle down to the engine room soon enough. Capital flight will cause more interventions – wait and see..

LikeLike

To me the non-answers to

1) Jenee’s question on empirical evidence of the hot housing market putting financial stability at risk, and

2) Bernard’s question on the definition of long term sustainability or the measure of “stretched”

summarized it all.

Underwhelming.

LikeLike

The real test of sustainability in terms of being able to afford a mortgage as well as the other essential costs of living and owning property can be determined as follows, Gross income less tax, less food heating travel insurance rates clothing etc the sum left is available to service a mortgage/ It used to be 30-40% of gross income plus say half a partners income, this allowed some margin as not all (increasingly so now) couples have children so some adjustment for this and the longer term mortgages and lower interest rates is required. This is of course a form of loan to income calculation but in my view superior to loan to value as any significant reduction in property values impacts both lender and borrower.

A 20% deposit does insure a lender against a reduction of a similar figure (adjusted for any prior value increase) beyond that borrower and lender are both impacted and social issues mount as a result – check out UK negative equity in the early 1990’s so we may already be beyond the point at which an asset de valuation combined with a liquidity crisis will cause a massive disruption throughout the world and the spectre of a world food shortage may be the trigger that finalises the same, “Let them eat cake” scenario of Frustration/Anger/Hate into violence globally as is already being seen at various levels – USA/Europe/Russia/parts of Asia. I hope for a managed rational solution but fear chaos and revenge to repeat history’s lessons we have failed to understand.

LikeLike