There was stuff to like in yesterday’s Monetary Policy Statement and the associated press conference.

There was the remarkable statement from the Governor that “we don’t comment on government policy”, which we can only hope – unrealistically – heralds a new policy for the Governor (as it was it simply got him off the hook of answering an inappropriate question about lockdown policy etc).

More seriously, there was some sense that the MPC and the Bank were beginning to appreciate just how poor the world economic outlook is. I wouldn’t go quite as far as ANZ”s chief economist whom I saw reported in the paper this morning saying “it was hard to imagine a more dovish sets of policies and commentary today”, but my own initial comment to a journalist re the commentary etc was

The overall tone – downside risks, worrying world economy situation – is encouraging

It is a step in the right direction, even if there is little depth to the analysis (and, for example, no links to more-rigorous supporting analysis). And of course even the Bank was caught out between the projections being finalised (on the 5th) and released: they’d idly assumed a “level 1” regime from June on. Perhaps they had little choice in the central track, but there was far too little about the risks of new “lockdowns” and (a) the associated real income/output losses, and (b) associated addition to the already high level of uncertainty facing firms and households – whether about the virus, the wider economy, or the government’s chosen response.

There was even some recognition that inflation expectations had been falling, usually a sign – at least if starting at or below the inflation target midpoint – that people don’t think the Reserve Bank is doing its job. It was all rather played down – with more emphasis on risks of further falls than the large falls we’ve already seen – and, as almost always, they chose to totally ignore whatever information is in the inflation breakevens derived from the government bond market.

And yet what did the Bank actually do, that might affect real interest and exchange rates, credit conditions or whatever – in ways that might make a real difference to the inflation and employment/output outlook? Nothing. And that is the problem.

There was plenty of renewed talk of the possibility of negative interest rates. (This was in conjunction with some possible new instrument – Funding for Lending – which is unlikely to have very much effect at all: the Governor nicely articulated in the press conference why buying foreign assets wasn’t a good – likely to be effective – option at present, and a very similar analysis could be presented for his scheme of lending to banks – banks (a) not notably being short of funds, and (b) not being known for being keen on dependence on central bank funding, at least outside the immediate white-heat of a crisis. )

But there was no action (not even on the new idea tool). In fact, the Governor reiterated the commitment that the MPC had made back in mid March not to change the OCR for a year. And that is even though, as the Governor himself noted, “March feels like a long time ago”. It isn’t of course, but a great deal has changed since the MPC made that rash commitment – notably, the MPC itself has belatedly come to appreciate the severity and duration of the economic downturn. No one expected them to walk away from the commitment yesterday, but it would have been good – good policy – if they had. Central bankers should no more be encouraged to keep rash promises than moody teenagers who in a moment of upset threaten to run away from home, or perhaps kill themselves, should be encouraged to keep those rash promises. From the evidence we have – what the Bank choses to make available – little more thought seem to go into the former pledge than into pledges of the latter sort.

Of course, the MPC did pledge to buy a whole lot more government bonds, over the next couple of years. They still to seem to believe that such actions make a real-world difference to things that affect the inflation/output outlook. But they are wrong to do so. As it happens, I’ve this week been reading Stephanie Kelton’s MMT tract. The Deficit Myth. Much of it is a socialist tract, beloved no doubt by Bernie Sanders (her former boss) and Alexandria Ocasio-Cortez, but a fair bit of the first half is a (really clearly written, if somewhat loaded in interpretation) articulation of how fiat money systems work. It is all stuff most serious central bankers know, even if they don’t use her language. One of her arguments that it really doesn’t make much difference whether the government pays for its activities by creating settlement account balances at the central bank or by selling bonds (she calls one “yellow Treasurys” and one “green Treasurys”). And in the current context that is much the same as my argument: the Reserve Bank buying tens of billions of government bonds (generally yielding less than 1 per cent) and issuing tens of billions of dollars of settlement account balances earning, currently, 0.25 per cent just doesn’t – and wouldn’t reasonably be expected to – make much useful difference to anything. It is just an asset swap, doing little more than shifting around interest rate risk (the Crown is now quite highly exposed if something dramatic happens and interest rates need to rise a lot in the next few years).

The Bank continues to claim otherwise. But it is just a claim. They have a substantial research and analysis operation but have published nothing that would support their claim, nothing that could be externally scrutinised. I guess they believe it, but they’ve gone out on quite a limb with the LSAP so of course they would.

The Bank claims that “the LSAP has [note the certainty] helped keep the New Zealand dollar exchange rate lower than it would have been otherwise”. They do acknowledge that it is hard to tell but then tell us – with no supporting analysis – that they think “the exchange rate is 4-10 per cent lower than it would have been without the LSAP programme”. To which my response would be:

- well perhaps, but the real exchange rate is still – as you yourselves acknowledge – where it was at the start of the year, so that even if the LSAP has kept the exchange rate down a bit, there is no absolute easing in this component of monetary conditions (despite a really big slump, and a shutting down of two major export industries),

- much depends on the counterfactual. I reckon there is a reasonable argument that the LSAP has left the exchange rate higher than otherwise, since the prime alternative policy – a zero or negative OCR – would have taken the TWI lower, and

- yesterday’s announcement wasn’t great for the Bank’s story: the exchange rate barely moving.

They also claim that the LSAP has made a big difference to bond yields: “we estimate that NZGB yields are at least 50 bps lower, and potentially more than 100bps lower, than they would have been without the LSAP programm”. They present no analysis – at all – in support of this claim, not even telling us which point on the yield curve they are referring to (the shorter-end will be strongly anchored by the expectation that the OCR won’t be raised for several years). And perhaps more importantly:

- if it is the long end they are referring to (where the LSAP has been concentrated) they’ve never articulated a convincing story for how, in New Zealand, long-term bond rates affect the transmission mechanism (long rates may be lower – probably are to some extent – but so what, and are we sure this isn’t an unwise distortion, at least if the Bank believes monetary policy is going to work and in a few years we will be back to a neutral OCR, according to them in excess of 2 per cent?), and

- even if the LSAP has somehow imparted a great deal of stimulus – and yesterday’s announcement didn’t move market prices much further, the Governor acknowledging diminishing returns to LSAP – there is the small point of a pretty worrying outlook for the economy and inflation. With all that estimated stimulus included, inflation is still at or below the bottom of the target range until the end of 2022, and the unemployment rate was still forecast to be 6 per cent by then. And the Bank was emphasising downside risks, even before the new lockdowns.

I’m pretty sure I heard the Governor say that there was quite a bit more to do. And yet, they did nothing.

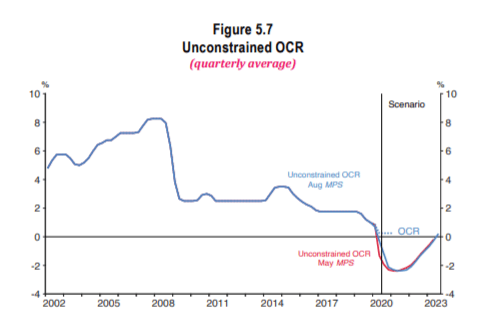

At the last MPS the MPC chose not to publish projections for the OCR itself, but instead to publish a chart showing an “Unconstrained OCR”, apparently estimated by letting the forecasting model run and give us an estimate of “the broad level of stimulus needed to achieve the Reserve Bank’s employment and inflation objectives”. This was yesterday’s chart.

Throw in a whole lot more fiscal deficits and a whole lot more announced bond buying since May and the model still reckons the OCR should be at some below -2 per cent. Instead, it sits and sits and sits at 0.25 per cent. On their own numbers, they aren’t doing their job. In the presence of self-acknowledging downside risks to activity, inflation, and inflation expectations.

So I discovered this morning, it was a year yesterday since the Governor’s extensive interview with Newsroom was published, in which he championed negative interest rates as the preferred policy tool in the next serious downturn. It was a good – informative, thoughtful – interview and we’ve never had an explanation for why he changed his mind (or, less probably, was overruled). We do know, of course, that he and his staff did nothing to ensure that banks’ systems were ready and able, despite years of advanced notice, and now we are left with any serious monetary policy apparently dependent on how accommodating the Governor is of bank preferences – and we know banks aren’t keen. There is evidence that the Reserve Bank now has a serious work programme – see this response to an OIA request someone else lodged (which the Bank said it was going to post on its website but did not do so)

but they fiddle – move banks slowly ahead – while the economy – real people, real firms – suffer unnecessarily.

It is simply inconceivable that at any other time, presented with projections this weak, downside risks, and serious new adverse news on the eve of the announcement, that the Bank would not have cut the OCR, perhaps by quite a lot – not just fooling around with handwaving instruments that they can’t even demonstrate are making a material difference especially at the margin.

Jim Bolger has been in the news briefly this week – for his irrelevant suggestion that the government bonds held by the Bank be “written off”, which would change precisely nothing of macroeconomic significance – but he was Prime Minister in early 1991 when the Bank was very reluctant to ease monetary conditions. There was significant political pressure – with hindsight quite warranted really – brought to bear on the Bank – and Don Brash had been advised to watch his back when he went overseas. But this time? We have a Prime Minister and Minister of Finance who simply seen indifferent, whose innate conservatism seems to extend to not rocking the boat even when officials aren’t doing their job (and when the Minister of Finance has formal delegated intervention powers).

Once again yesterday, the MPC seemed keen to fob off responsibility to fiscal policy. But whatever the MMTers may wish, under New Zealand law fiscal policy does its own thing and then monetary policy – the MPC – is charged with the residual stabilisation (full employment and all that). The Bank has the effects of huge fiscal deficits included in its projections – including that unconstrained OCR chart – and it presents a nice chart showing that the estimated fiscal stimulus peaks this quarter and tails off from there (with neither main political party appearing keen on further increases in deficits from here). Fiscal policy has played the ball – wisely, responsibly, appropriately or not – and responsibility now rests with the Bank and the MPC. Who are doing nothing, and seem more interested in giving little lectures to banks are to how they should run themselves than in using the tools Parliament has put at their disposal. Perhaps they’ll do so next year – still seven months away at least – but they should have been acting much more decisively not just now but months ago.

Two final notes:

- it was interesting to see the updated Bank forecast for the GDP contraction in the June quarter. They expect a fall of 14.3 per cent following the March quarter fall of 1.6 per cent. No one really knows and there are likely to be big revisions through time, but it was sobering to contrast these estimates with the falls in hours worked recorded in the HLFS, up 1.0 per cent in March and down 10.3 per cent in June. That is a cumulative estimated fall in GDP of 16.1 per cent and a cumulative fall in hours worked of 9.4 per cent. In other words, on the face of it, a huge fall in productivity. Since both sets of numbers are probably not that much more than educated guesses, perhaps the truth was less bad, but – properly measured – it seems almost certain that productivity in the June quarter would have been far lower than usual. And yet, optimistic as ever, if anything the Bank is forecasting trend productivity growth in the next couple of years a bit higher than it has been in recent years,

- I mentioned Stephanie Kelton’s book, MMT and all that. This morning I recorded an interview with Radio New Zealand’s Jim Mora on monetary policy, fiscal policy, MMT, the Bank and so on, in the current New Zealand context. It is scheduled to be broadcast on Sunday morning, although at present I’m not sure when specifically. My previous post on MMT still seems about right to me, although Kelton’s approach is more radical than the presentation from, and discussion with, Bill Mitchell that the previous post was built on. There is a macro policy dimension to Kelton, but her real agenda is big government across the board – an explicitly political agenda that doesn’t have much to do with the best design for macro policy.

Maybe you can educate Adrian about how unsterilised FX intervention works. Judging from the press conference, it’s a mystery to him.

LikeLike

He doesn’t read me…..

He did seem to be talking from a sterilised intervention playbook, altho when the Bank is paying a high – relative to macro circs – rate on unlimited settlement account balances I’m probably less convinced than you that there is that much difference.

LikeLike

Yes, his answer was clearly from the Eckhld (2005) playbook. Certainly in normal times I would agree with his assessment, although I don’t buy the argument that the NZD is cheap, relative to its BIS REER, it’s about 10-12% above its past 56 year average.

But I am a bit more optimistic that unsterilised FX intervention would bring down the kiwi, especially if done in conjunction with negative rates. Excess settlement cash balances are not going to weigh on kiwi from here but direct buying via a tender process would shift supply-demand in the FX market.

The bottom line really is that this statement did nothing to ease monetary and credit conditions.

With unemployment rising, banks are going to become increasingly discerning about credit allocation to residential mortgage borrowers, especially given the likely extension of the mortgage holidays and conversion to interest-only. Debt serviceability is going to be a key challenge.

LikeLike

I’d probably agree with negative rates.

LikeLike

How can you talk about the level of the real exchange rate in isolation of the terms of trade, which is still reaching record highs? Given that the real exchange rate has been falling over the last few years while terms of trade have been steadily increasing point to the fact that the NZD is under-valued not over-valued?

I’d like to quote BNZ’s (Jason Wong) recent article, which pretty much demolishes your arguments on the exchange rate needing to come down:

“There seems little economic justification to drive the NZD weaker. With no global tourism, a weaker NZD would not see an influx of visitors. We’re currently in a period where the economy is less sensitive to the exchange rate than usual.

“And NZ commodity exporters, in general, are in no need of a helping hand. NZ’s export commodity price index is close to average over the past decade and is higher than average when measured in NZD terms. In other words, commodity export returns are currently better than average.

“With global tourism grounded to a halt, a weaker NZD would likely have more impact on NZ’s import sector than export sector at this juncture, adding to import costs and therefore the cost of doing business or resulting in reduced spending power for consumers. A weaker NZD wouldn’t offer much so-called “stimulus” to the economy in the current environment. ”

Click to access 200812_The+futility+of+intervention3.pdf

His arguments seem to be absolutely intuitive and sensible, but are diametrically opposed to yours. His third para in particular a point I have been trying to get you to respond to without success for a long time.

LikeLike

Jason appears to have a different view certainly. I don’t sense any “demolition” (altho I certainly don’t favour fx intervention). Mine is a macroeconomic argument: we had significant unemployed resources, and we need policy settings that will quickly reabsorb them. in the face of continuing border restrictions and a v weak world economy. Of course, some bits of the tradables sector can’t respond at present – in fact they are completely moribund – but given our ongoing taste for imports even in a tradeable sector only focus, that would be more likely to argue for a deeper depreciation than for none at all.

LikeLike

The Bank really delivered nothing. They plan to keep doing LSAP at a slightly faster pace than before, so maybe the 2s10s spread flattens another 5bp, but no one borrows that long in NZ and the impact on the exchange rate was trivial.

Then there’s the recommitment to their foolish 0.25% forward guidance. How’s that workin’ for ya Adrian?

They’ve pretty much ruled out adding foreign assets to LSAP before cutting rates so that’s off the table.

So what rabbit is he gonna pull from his hat in November? Intervention in swaps? So what? More excess settlement cash ? It’s all a farce, just like the labour survey.

We are going to yo-yo between lockdowns on a failing policy all the time destroying our economy and we will still end up with the virus, alongside mass unemployment, 50% taxes and riots.

Nice work….

LikeLiked by 2 people

Having just locked in residential loans at 2.55% for 12 months which have just come off fixed at 4.5%, I can only say, great job Adrian Orr.

LikeLike

It seems to me you both are making macroeconomic arguments, but his points are perhaps inconvenient to your wider narrative of wanting to force a rebalancing the economy through engineering a much lower exchange rate (i.e. restructuring).

One of the arguments against depreciation is that NZ is still enjoying very high terms of trade, which is an important factor when judging the the relative degree of over or under valuation of the real exchange rate – more important I would say than how it currently compares to some arbitrarily defined long-term average. This is a point also raised in the article which you’ve not addressed. If you had time to add a brief response to this point that would be appreciated.

LikeLike

I guess my response would be that I’m not really relying comparisons with some long-term average or – for these cyclical purposes – relying on arguments about under or overvaluation. This is a narrower point: since we learned about Covid, we’ve lost major export industries (and other domestic spending), the terms of trade haven’t really changed and neither has the exchange rate. That isn’t a recipe for getting back to full employment quickly, at least unless fiscal policy is deployed really quite aqggressively from here (something neither main party is promising).

LikeLike

Michael

Are there any adults in the room that have a plan beyond continuous lockdowns? Fiddling with monetary policy is all very well, but as we are presently destroying large sections of the economy with no realistic end in sight, it’s past time we asked some basic questions:

a) Is this virus really any more deadly than the flu where no perfect vaccine exists and likely never will? More contagious yes, but more deadly?

b) If we have to live with covid-19 as opposed to our failed attempts to eradicate it, what practical measures would we take, while keeping businesses open and the economy functioning?

c) Is saving face for our politicians more important than saving the economy?

By this I mean, have they persisted so long with the present (failing) strategy, that to stop and change direction now would be too humiliating? Are they preferring to ‘stay strong’ and be wrong than change course?

d) Why have we not ordered and distributed millions of “10 minute” self test kits that have 98% accuracy?

Realistically, if the answer to (c) is ‘yes’ then the rest is just background noise.

LikeLiked by 1 person

Indeed. As I read the evidence this virus is more deadly, altho mostly to very old people. As in the previous lockdown there is likely to be no serious attempt at a cost benefit analysis undertaken by officials.

And of course monetary policy is at the margins, but still needs to do what it can, aggressively, given the rest of the mess.

LikeLike

Not monetary but worth a read. Why we cannot eliminate the covid nor any other virus.

https://theconversation.com/does-coronavirus-linger-in-the-body-what-we-know-about-how-viruses-in-general-hang-on-in-the-brain-and-testicles-142878?fbclid=IwAR3ChsMFv9e7giQjH2uARXsIH7Y1TW5Xw9Hoi0jRVlaNy7jznjWeNtwrPkM

Viruses are sleepers and there are quite a few. Malaria, Ross rRiver Fever ,HIV, Ebola, Chicken Pox and many others.

The world and humans are never going to be rid of them.

Really good explanation of things virus.

LikeLike

Really interesting thanks – and more than you might have expected since the reason for the much-reduced frequency of the blog for the last couple of months is that I have a recurring bug exactly like that – every five years or so for the last twenty, untraceable by doctors, and eventually v slowly goes away again. Sounds exactly like one of those latency things.

LikeLike

The elimination of covid 19 is just a fools dream. Basically Kiwis have been conned by Jacinda Ardern, the greatest liar we have ever had as a Prime Minister.

100,000 kiwibuilt homes a lie.

1 billion trees planted is a lie

Auckland intercity rail is a lie

Reduce child poverty is a lie

No new taxes is a lie

Reduce the queue for social housing is a lie

Transparent government is a lie

Etc etc lies.

LikeLike

And…

“Better healthcare. Let’s do this.” A lie (my neighbour’s campaign hoarding at the last election).

“Let’s keep moving.” Cleverly unfalsifiable (this election’s).

LikeLike

Did it really take the RBNZ 17 hours to write that OIA response?

LikeLike

You might well wonder – I did too. I recently had one where they estimated 4-6 hours for doing nothing of substance it all. I presume the numbers are supposed to intimidate people with what they might be charged if it weren’t for the grace and favour of the Bank.

LikeLike

I seem to recall on previous occasions the RBNZ has referred to a “Shadow” OCR, the so called Wu-Xia measure. This is supposed to show what the OCR would be if alternative policy actions, such as asset purchases, were taken into account. I think this calculation by the RBNZ for New Zealand showed our shadow rate at about -2%. But the “Unconstrained OCR” graph and commentary in this MPS seems to suggest that the actual OCR itself, not just the shadow rate, needs to be at that level if the RBNZ’s inflation and employment goals are to be achieved. Is that correct Michael ? BTW, i have a graph showing that the shadow rate for the UK is now -7.5% (but it seems graphs can’t be uploaded here..).

LikeLike

Leo Krippner developed a shadow short rate for NZ and a bunch of other advanced countries, which tries to take account of the QE impact. https://www.ljkmfa.com/test-test/international-ssrs/

On his model, NZ is currently equivalent to -1.1 and the UK -1.2.

I wrote about Leo’s model, and some of the limitations here

https://croakingcassandra.com/2020/04/02/measure-what-is-measurable-and-make-measurable-what-is-not-so/

The unconstrained OCR estimate is supposed to be just the OCR itself, since the effects of QE etc on the exchange rate and longer-term rates should already be factored in to the econ projections, leaving the OCR adjustment itself required to get medium-term inflation back to 2%.

LikeLike

China is flooded with excess inventory. Don’t bet on monetary policy to influence inflation.

LikeLike