In the last few days speeches by two of the Reserve Bank’s senior managers have been published. The first was from the Deputy Governor Geoff Bascand – delivered on no obvious occasion to “banking industry representatives in Wellington” – and the second by Toby Fiennes, formerly head of supervision (operations and policy) but now reduced to Head of Financial System Policy Analysis, at one of those commercial training ventures that are always keen to have (free) speakers from places like the Bank.

Bascand and Fiennes have often been among the better people in the upper reaches of the Reserve Bank. I’ve been on record suggesting – before the appointment and since – that Bascand, if not ideal, would have been a better appointee as Governor. His speeches have typically been quite materially better than those of his senior management colleagues – more akin to what we see from people at Deputy Governor level in other advanced country central banks – although that is true more of his speeches on economic topics than those on banking and financial stability. Perhaps that isn’t surprising – his background was in economics, and he had no background in financial stability or regulation until he took up something like his current job three or four years ago.

In this post I want to focus mostly on Bascand’s speech. He is the more senior figure and is across all the functions of the Bank – including apparently enjoying the confidence of the Minister as a member of the statutory Monetary Policy Committee. And if Fiennes’s speech raises one or two points, Bascand’s is really quite egregious in places.

As befits one of Orr’s deputies, the speech pays due obeisance to the public sector employees’ campaign to change the name of the country. The title? “Banking the economy in post-COVID Aotearoa”. As it happens, they the drop one more “Aotearoa” into the first page before reverting, almost without exception, to “New Zealand” (actual name of the country, actual name of the Reserve Bank of New Zealand) for the rest of the speech.

The bottom line message of the speech, however, seemed to be an injunction to banks to lend more. So much so that, as per the title of this post, one was left wondering why if Messrs Orr and Bascand know so well what the profitable risk-adjusted opportunities are they don’t step down from their secure and quite highly-paid public sector perches and start a bank, or at least offer their services to the credit and risk departments of some existing insurgent bank.

It starts on the first page

In the face of these challenges, the banking sector could choose to hunker down and seek to ride out the storm until the good times roll again. Or, the banking system could continue to step up and play a crucial part in supporting New Zealand’s economic recovery and maximise its potential competitive advantage of relationship lending and customer information. …..

Maintaining institutional resilience while continuing to serve customers in an uncertain environment will demand expertise, courage and an unwavering belief that the people and businesses of Aotearoa will find a way to come out of these challenges.

In periods of extreme uncertainty, isn’t the rational – and prudent – response of most people to “hunker down”? And this is an environment of really quite extreme uncertainty – a point I’m sure we will hear emphasised (again) by Orr and Bascand next week when they put their monetary policy hats on and deliver the Monetary Policy Statement.

But here – playing with other peoples’ money – they want bank managers to ride blindly – but “courageously”- into the cannon fire, as if they (Orr and Bascand) either know better than the shareholders what is in those shareholders’ interests, or just don’t care. And it is pretty rich coming from people who, with their monetary policy hat on (the tool actually designed to support recoveries) are doing almost nothing.

It is really remarkable for the lack of nuance and subtlety. I scrawled in the margin against that first paragraph “presumably some mix?” I doubt there has ever been a market-oriented banking system that- in a severe downturn – has ever either called in every loan possible at the first sign of trouble, or rushed out boldly to encourage a wide range of borrowers to take more credit. But there is nothing of this in Bascand’s speech, nothing either about how serious downturns should prompt both lenders and borrowers to reassess the assumptions they were working on, in turn prompting greater caution – the more so, the more uncertain the path ahead. Thus it is fine for central bankers to fling out rhetoric about “unwavering belief”, but no one knows which forward path the economy will actually take, how long it will take to get securely on that path, or what crevices there might yet be along the road. It will make quite a difference to plenty of credit assessments – whether for existing debt, or those interested in taking on new debt (around many of whom there may be adverse selection risks).

A bit later on there is an entire section of the speech on “Reserve Bank actions to support bank lending”. It is about as thin.

For example, we get overblown claims like this

Cash flow and confidence became key to New Zealand’s financial stability.

I know “cash flow and confidence” was a mantra of the Governor’s but – and as the Bank itself would tell us any other time – the financial system’s soundness was much greater than implied by this assertion of Bascand’s, reinforced a sentence later when he tries to claim that various initiatives had “kept the financial system stable”. These measures, apparently, included the small cut in the OCR (virtually no change in real terms), whatever the LSAP did to long-term rates, and a list of other regulatory measures which – useful as most may have been – will have done little or nothing to “keep the financial system stable”. System stability is mostly about disciplined lending in the good times. All evidence suggests – and other Reserve Bank commentary suggests they agree – we had that. One of the risks at present is that if anyone in the banks paid much heed to the Reserve Bank’s rhetoric, those lending standards could be considerably debauched now.

Bascand goes on, being really rather self-congratulatory

Taken together – and without being too self-congratulatory – these initiatives have had a significant impact on supporting the short-term financial needs of households and businesses. This was important to limit failures of businesses with good long-term income prospects, and prevent mortgage defaults and foreclosures for borrowers facing temporary decreases in income.

All this without a shred of evidence to support his claims to have made much difference at all. In this Bascand world, banks would have been rushing into mortgagee sales, closing businesses galore, without any regard at all for longer-term relationship prospects etc, if it hadn’t been for the Reserve Bank. It is the same spin we used to get from the Governor, and the same lack of evidence. We’ve had fairly sound and well-managed banks for 100 years or more – recall that the closest to a bank failure in the immediate post-liberalisation period were two government-owned entities- but the Governor and his Deputy believe that they are the hope and salvation.

Bascand goes on to talk threateningly about banks retaining their “social licence to operate” – if there is such a thing, it is really no business of a central bank charged only with prudential supervision of banks. And then we get to what seems to be the climax of his lecture on lending

But a key determinant of the success of New Zealand’s economic recovery to come will be the willingness of banks to lend to productive, job-rich sectors of the economy so that we can collectively take advantage of New Zealand’s enviable position of having eliminated community transmission. Now is the time for banks to prudently drawdown on their buffers to support their customers. Shareholders will have to be patient for longer-term payoffs, but this forward-thinking, long-term approach will stand bank customers, banks, shareholders, the financial system and Aotearoa in the best position.

Given banks are anticipating a deterioration of their loan portfolios, hunkering down and tightening lending standards may seem to them to be the optimal response to perceived increased risk. However, given banks dominant role in New Zealand’s financial system a synchronised lending contraction across the banking sector would risk a ‘credit crunch’ amplifying the economic downturn (Figure D). Therefore ultimately it is in banks’ own interest to maintain the flow of credit and contribute to the long-term stability of the banking system by preventing large scale borrower defaults and disorderly corrections in asset markets.

There is so much problematic about this it is difficult to know where to start. There is. for example, the small point that highly productive sectors tend – almost by definition, and it is a good thing – not to be ‘job rich”. For the rest, as noted earlier, you get the impression that people with no experience in banking at all – or indeed in Bascand’s case any in business at all – are best-placed to tell private businesses and their shareholders what is in their own best interests. Based on what evidence, what analysis? And isn’t it all rather lacking in nuance, since few of these sorts of decisions are ever all or nothing. And despite the wider economic responsibilities of the Bank, it isn’t even obvious where Bascand thinks these profitable creditworthy projects are to be found – or how he could be confident of his judgement even if he and his staff could identify some. Surely a more general answer would be that private agents (banks and other firms and households) are best placed to make their own assessments about choices and risks, but that macro policy (and perhaps now public health policy) can provide the best possible supporting climate for those private decisions to be made. As it is, even later in this speech Bascand concedes that “our economic challenges remain severe”. Not exactly a climate for much private sector risk-taking, whether by banks, firms or households. But it might, for example, be time for a monetary policy central bank to start doing its job.

Risking other peoples’ money was the theme of that bit of the speech. But Bascand also took the opportunity to comment on the Governor’s bank capital review – the one that will require a huge increase in bank capital to support the existing level of business. The one that banks, and many outside experts – not, contrary to the Governor’s claims, just those paid by banks – warned would lead to some credit contraction, some disintermediation from the banking system, and some higher costs.

Likewise, capital metrics were strong going into this crisis, boosted by Basel III regulatory requirements, a number of years of favourable economic performance, and preparations for the impending implementation of the Reserve Bank’s Capital Review. The COVID-19 crisis has underscored the importance of banks having sound capital buffers; increased provisions for expected credit losses have, so far, been easily absorbed by existing capital buffers. Healthy capital buffers are necessary not only to ensure banks survive crises, but to ensure banks survive ‘well’ and are able to continue to lend to creditworthy borrowers throughout a downturn. The Reserve Bank remains committed to fully implementing the outcomes of the Capital Review. However, as we indicated this past March, this will be delayed one year and not occur until July 20212. We expect to communicate further on the implementation of the Capital Review by the end of the year.

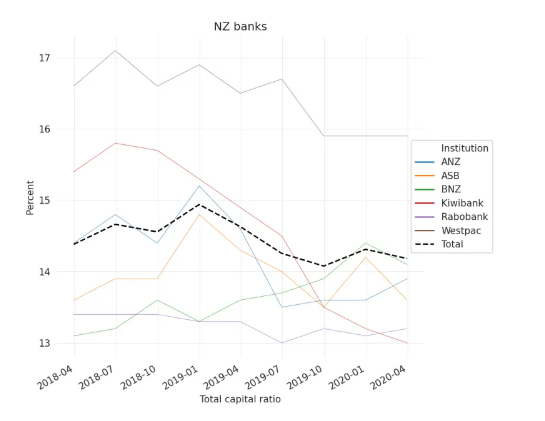

There are really two main points here. The first is the claim – that Orr has made repeatedly – that banks were well-positioned this year partly because they had been acting preemptively to raise more capital in anticipation of the higher capital requirements, which were supposed to be phased in from this year. Victoria University banking academic Martien Lubberink has addressed directly this claim in a post on his blog. As everyone recognises, capital ratios have increased since prior to the previous (2008/09) recession, under the influence of some mix of regulatory and market/ratings agency pressure. But here is Martien’s chart showing total capital ratios for several of main banks operating here for the period, in early 2018, since Orr took office.

He has another chart showing core (CET1) capital ratios, which also suggests no lift in capital ratios over the last couple of years.

The Bank has been attempting a difficult balancing act: trying to assure us (of what is almost certainly true) that the local banks are very sound, but at the same time trying to get cover for the scheduled large increase in capital requirements. There would be some reconciliation if banks had been raising actual capital in anticipation of those new requirements but….the Bank’s own data, the useful dashboard, confirms that it just isn’t so. It is just spin, it is a lot worse than that.

Oh, and note that Bascand reaffirms that the Bank is still committed to moving ahead with the higher capital requirements – even though it expects the banks to come through the current severe test just fine. The implementation was delayed by a year back in March, but that is now five months ago, and July 2021 really isn’t far away – particularly in a climate of heightened uncertainty, including about likely loan losses out of the current recession. So on the one hand the Deputy Governor and his boss are out their urging banks – almost suggesting it is some sort of moral duty – to lend more freely, and on the other hand they are still pushing ahead with their plans to hugely increase actual capital requirements, something even their own modelling suggested would have adverse transitional effects in more-normal times. (Oh, and did I mention all while doing nothing to actually lower real interest rates across the economy, in ways that might improve servicing capacity on current debt, and provide a boost to aggregate demand and – over time – to credit demand.)

And here I want to refer to the other speech, by Toby Fiennes; in particular this extract (emphasis added)

At the end of May we released our six monthly Financial Stability Report (FSR) which assesses the health of the financial system. This assessment presents particular challenges during more volatile and uncertain times; we want to report openly and fully about the state of financial stability and the risks that we see, but we have to be mindful of the risk of exacerbating the situation, and further undermining confidence.

We used stress tests to inform ourselves and our audience about banks’ and insurers’ resilience. We developed two scenarios to test the banking system, which had similar economic projections to the Treasury’s COVID-19 scenarios 4. Results from our modelling indicated banks would be able to maintain capital above their minimum capital requirements under a scenario where unemployment increased to over 13 percent and house prices fell by a third. However, a second more severe scenario showed the limits of bank resilience. Under this scenario with unemployment of over 18 percent and house prices falling by half, banks would likely fall below minimum capital requirements without significant mitigating actions.

I should note that bank capital buffers have increased significantly in the past decade, in response to actual and forthcoming increases in regulatory requirements; therefore the banks entered the Covid-19 pandemic in a sound position. Additionally, since early April the Reserve Bank has prohibited banks from paying dividends to their shareholders, which further supported the capital positions of New Zealand banks. This gives banks headroom to continue to supply credit, which will play a large role in supporting the economic recovery.

Note that he repeats the same outright misrepresentation – the bolded phrase – as his boss.

But it was the rest I was more interested in. He highlights again the updated stress tests reported in the FSR. I might be more pessimistic than most economists, so I reckon the 13 per cent unemployment scenario sounds like a good and demanding test. As with previous similar RB stress tests, Fiennes reports that the banks come through just fine – at least so long as they don’t markedly lower their lending standards in response to regulatory pressure. But again – as was argued during the capital review debates last year – if the system is resilent to such an adverse shock before capital ratios are raised, what possible credible case can their be for markedly further raising capital requirements? Especially when the Bank is trying to twist banks’ arms to maintain/increase new lending? There is just no apparent rigour or coherence to the Bank’s position.

Much the same goes for the line about prohibiting dividends. I didn’t have too much problem with the temporary ban when it was announced – on good prudential grounds that in the very unlikely event that our banks got into serious trouble we didn’t want resources being transferred back to the parent, leaving larger losses for New Zealand creditors and taxpayers. But it is just bizarre to suppose that banning banks from paying dividends will increase their willingness to make new good loans. If anything, it is only likely to reinforce unease about doing business in New Zealand (at the margin), and since credit demand has fallen notably – a point Bascand acknowledges- and actual capital ratios were well above current regulatory minima it isn’t obvious that some shortage of capital in the New Zealand business was likely to be a big influence on lending policy just now. The suggestion that suspending dividends will “play a large role in supporting the economic recovery” is without support, and if seriously intended is almost laughable.

There is more in Bascand’s speech I could devote space to. At least what I’ve covered up to here is within the Bank’s statutory mandate re the soundness of the financial system as a whole. The same can’t be said for this stuff, pursuing the Governor’s personal political agendas on issues where there may be real issues, but they have nothing to do with the Bank’s mandate or powers.

Financial inclusion has become an increasingly important part of the Reserve Bank’s policy agenda in our capacity as a Council of Financial Regulator member and our own Te Ao Māori strategy. The Strategy helps to guide the bank in understanding the unique prospects of the Māori economy, how Māori businesses operate, and what lessons the Bank may learn in setting systemically-important policy with this view in mind. An important part of the Strategy is making clearer the unintended consequences of our policies on unique economies like the Māori economy.

Or one of the Governor’s favourites, climate change. Here I will just quote one line from the speech

Managing major and systemic risks to the economy, such as climate change, sits squarely within our core mandates.

It simply doesn’t The Bank has an important, but narrow, statutory role and set of powers around the soundness of the financial system. Climate change(and policy responses to it) may well represent a significant threat to our economy, our way of life, and so on. But unless – and even then only to the extent – it poses a threat to financial stability, not taken account of by private borrowers and lenders, it is really no particular business of the Bank. Any more than other serious risks – management of Covid itself as just a contemporary example – are anything much to do with the Bank.

But the Governor has personal ideological agendas to pursue, and (ab)uses public resources and staff to pursue them.

Standing back from the Bascand speech, what is really rather striking – and disappointing – is the lack of an overall framework, the lack of any real rigour or discipline, and a lack of straightforwardness. Clearly his boss has a cause – more lending – to pursue, but like Orr Bascand offers no reason to suppose, or evidence to support the implication, that banks are not acting prudently or appropriately. And never seriously engages with the implication that if the banking system is sound now and has plenty of headroom, why would it make sense for the Bank to be imposing big new capital requirements, which will assuredly be reducing the willingness of banks to lend.

But, as I noted earlier, if the opportunities are so real no one is stopping Orr and Bascand leaving their safe official perches and starting – or joining – a risk-taking bank. A good supervisor would, however, be keeping a very close eye on any bank riding courageously into the cannon fire – of extreme economic uncertainty, severe challenges – in the way Bascand appears to suggest.

Perhaps better if Orr and Bascand turned their minds, and attention, to using monetary policy in the way it was designed to be used, instead of sitting idly by six months into a severe economic shock, with real interest rates barely changed, and the real exchange rate not changed at all.

Orr, during the FSR presentation, mentioned that the Capital plans would require a longer phase-in. With three years of diminishing capital ratios going forward, we need three years to return to the position we were in around December 2019. Add 7 years of phase-in. Hence expect the capital plans to be fully phased-in in 2033. I am probably retired by then, if not the Capital plans.

LikeLike

Makes sense, altho it means 13 years of the capital requirements dragging on bank lending, pricing etc.

Fortunately Adrian should also be long gone by 2033.

LikeLike

I’m not sure after reading this whether the previous post title could equally have been “The bastard central bank” or “The central bank bastard” or “The central bank bastards”.

The Guv must be 58ish, so potentially 2 more electoral cycles until he’s eligible for Super.

A 2016 dated biographic interview at (https://e-tangata.co.nz/korero/adrian-orr-our-31-billion-dollar-man/ ) had some now familiar themes:

“Yeah, well, we’ve built from scratch what is widely considered the world’s best performing sovereign wealth fund, which is the NZ Super Fund. We’re more famous around the rest of the world than we are in this country. And we’ve done that not only in financial performance but also in responsible investing.”

LikeLike

Lend for the good of the Government of the day… we need growth badly because the Covid lockdown has screwed the productive sector badly…..and if they fail were will our tax funded salaries and perks come from!

Could have been the title of their speeches.

It all indicates a desire to move to a place of crony state capitalism with a Marxist inspired supervising government a la China. We truly have a bunch if halfwit socialists in charge… on the Treasury benches and in charge of all the major state ministries.

1970s stagnation here we come

LikeLiked by 1 person

I read a book called prince’s of the yen. And it would seem the central banks may want the banks to go crazy with lending so they go bust.. Then step in the reserve bank to take over the entire system.

LikeLike

What are the benefits of foreign property investment Michael. It sounds like scrapping the bottom of the barrel?

https://www.newstalkzb.co.nz/on-air/heather-du-plessis-allan-drive/audio/sir-john-key-unemployment-figures-are-not-accurate

LikeLike

Not a lot, altho as I understand Key his proposal involved allowing foreigners to build new houses. Given that he is strongly pro- immigration I guess it makes some sense (internal consistency), but if one is suspicious of our politicians just wanting to open the floodgates again, just as soon as it is safe, it seems like an idea to stay clear of.

LikeLiked by 1 person

I see trust is low in politicians and journalists. Paul Spoonley claimed it was high (Spinoff). I checked: that was advertising. Eg seeing something advertised online versus radio/tv/newspaper (which makes sense).

…..

I’m wondering if there could be a standard for reporting economics. For example: skills – what skills? Also “the economy”. They are talking about assistance for the tourist industry when each new job made us poorer as a nation. We get a massaged picture?

LikeLike