The Reserve Bank conducts a six-monthly survey of banks on aspects of credit conditions, trying to get at things not just captured in headline base bank lending rates. The last regular survey was conducted in March but, of course, quite a lot has happened since then. So, to their credit, the Bank has conducted a one-off additional survey in June to try to get a sense of how Covid and the associated economic disruption has changed things. The numbers and the Bank’s write-up are here. There is a good series of summary charts at the back of the write-up, some of which I will be using in what follows.

The survey has both current/backward looking questions and questions about the outlook, differentiated by type of borrower (SME (turnover less than $50m per annum), household, corporate, agriculture, and commercial property). Here is the Bank’s note

The June Survey was completed in the last two weeks of June 2020 by 12 New Zealand registered banks, including all of the five largest banks. The period covers credit conditions observed over the first six months of 2020 and asks how banks expect them to evolve over the second half of the year.

In the face of a severe, unexpected, economic downturn, and a substantial lift in uncertainty about the outlook, you’d probably have expected credit conditions to have tightened. For any given level of interest rates, banks would be less willing to lend. That would be an entirely rational response, even if banks were quite confident about their overall financial health based on the existing loan book. Credit demand – which respondents are also asked about – is a bit more ambiguous: credit demand for new activities might reasonably be expected to take a hit, but some borrowers will have a heightened demand for credit to tide them over a sudden unexpected loss of income.

What we see in the survey is, more or less, what one might have expected. Sadly, the survey hasn’t been running long enough to benchmark the data against developments in previous recessions.

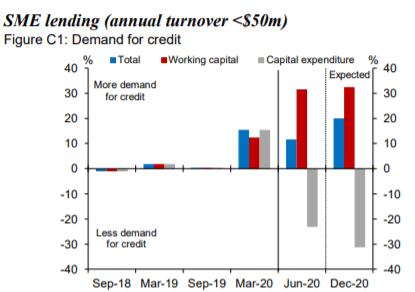

On the demand side, the two competing effects are most visible in the responses for SMEs.

Working capital demand has increased a lot, and is expected to increase a lot more in the second half of the year, while demand to finance capital expenditure has fallen quite a bit and is expected to fall a lot further. The picture for bigger corporates is similar, if perhaps not as stark. Overall demand for credit increased for these two business categories, but fell for all the others. “Credit availability” fell, as one would expect, across all these subsectors, and is expected to tighten further in the second half of the year.

One of the good things about this release write-up is that the Reserve Bank has released detailed disaggregated data from the survey that they do not usually publish. Quite why they don’t publish it routinely is an interesting question, but then this is an organisation not exactly known for its routine transparency – although you’d think that data collected under a statutory mandate, collated at tsaxpayers’ expense, should be routinely published.

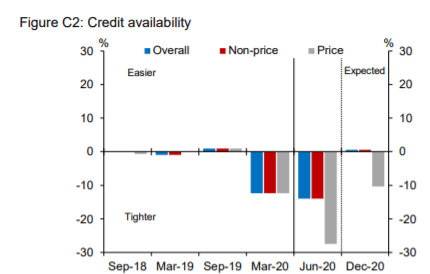

Anyway, the data are there this time. First, there is a distinction between the price and non-price aspects of credit availability, actual and expected. Higher credit spreads will be the key aspect of price.

For households (mortgage and personal lending) all the actual and expected tightening in credit availability took the form of non-price measures, but for all four business categories the price effect (higher credit margins over base lending rates) dominated. Here again, as illustration, is the chart for SMEs.

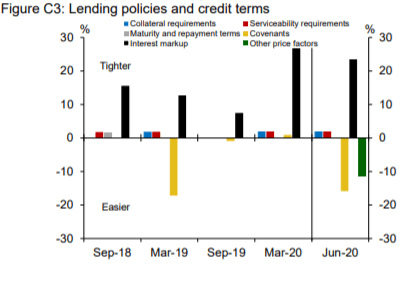

There is a further degree of disaggregation on the aspects of the credit availability responses, but only for the period already been. For each subsector respondents are asked about:

- collateral requirements,

- serviceability requirements,

- maturity and repayment terms,

- covenants,

- interest markups

- other price factors.

For households, the only material changes were (tighter) serviceability requirements. That is interesting – if not too surprising – given (a) slightly lower interest rates, and (b) some temporary easing in the Bank’s LVR restrictions.

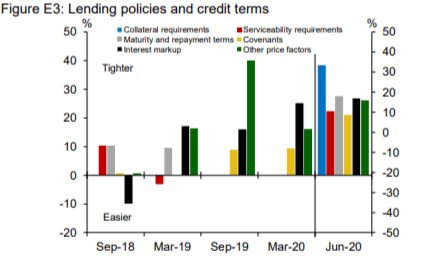

Here is the chart for SMEs

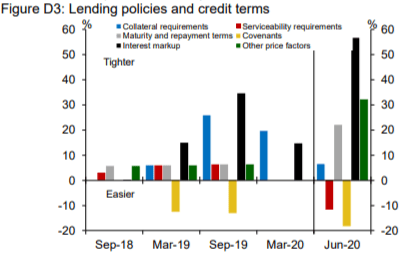

and for larger corporates

There are some interesting differences, but the stark similarity is in the higher interest rate mark-ups. For both subgroups, covenant requirements appear to have eased – one guesses semi-involuntarily as many borrowers will probably have blown through previous loan covenants. I don’t know quite what to make of the differences in the green bars – “other price factors” – but would welcome any comments/suggestions.

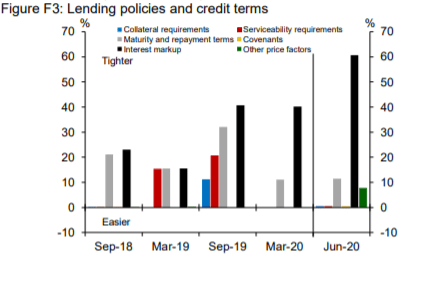

What of commercial property loans?

That’s pretty stark. For every component, policies and conditions have tightened, apparently quite materially. Perhaps not too surprising – and in many past downturns – commercial property loans, especially those on new developments, have been a key source of bank losses- but interesting nonetheless.

And, finally, agricultural loans. Farmers keep farming, and – for the moment anyway – commodity prices have held up. But in any global economic downturn, commodity prices often bear the brunt. In this case, the adjustment by lenders appears to have been mostly in the interest mark-up agricultural borrowers face. As the graph shows, credit spreads have been widening for some time, in the face of some mix of factors including the Bank’s markedly increased capital requirements (farm borrowers tend to have alternative sources of finance).

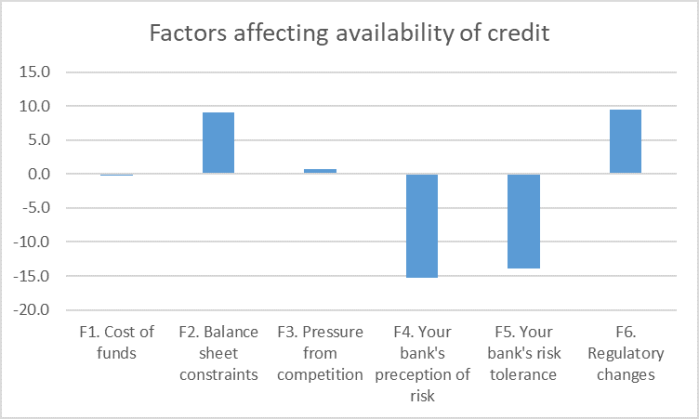

The final component of the survey asks about factors influencing the availability of credit. There isn’t a line for “severe unexpected recession etc”, but here were the interesting aggregate responses to the standard list of items.

Cost of funds is almost invisible as an issue – whether wider credit spreads in funding markets or lower base (OCR etc) rates – and so is any change in competitive pressures.

Respondents suggested that regulatory changes had been helpful – presumably this will refer to the temporary suspension of the OCR restrictions, the temporary delay in the increase in minimum capital ratios, and perhaps the temporary reduction in the minimum core funding ratios. Together these changes have, as one might expect, worked to mitigate a tightening in credit availability, but note the aggregate effect is not that large. On the other side of course, the two material effects are an adverse change in the banks’ assessment of risk, and in the willingness of banks to take any given level of risk. Both seem highly rational and sensible responses in a climate like that of recent months.

What to make of it all? Probably none of the results is terribly surprising, and it will be interesting to see how these results compare with those of the next regular survey in September (when we must hope the Bank will again release more-disaggregated data).

I guess what struck me was the widening in the credit spreads business borrowers have been facing. The published time series data from the Reserve Bank on business lending rate is pretty lousy – a single series for “SME new overdraft rate”. That headline rate has fallen only about 70 basis points this year. That isn’t too surprising – since the OCR has fallen 75 basis points, and floating mortgage and bank bill rates not much more. The credit conditions survey tells us that typical business credit spreads over base rates have risen (probably quite rationally so in the changed economic climate). But we also know that inflation expectations have fallen quite a lot – data from the indexed bond market suggests about 70 basis points this year. In other words, the combination of increased risk perceptions and a passive central bank doing little or nothing, in the face of one of the most severe economic downturns, here and abroad, for many decades, real business lending rates are rising. That is quite insane outcome, but a choice made by Orr and the MPC, and apparently condoned by the government (and the Opposition for that matter). It is quite extraordinary, almost certainly without precedent in a country with (a) a floating exchange rate, and (b) a sound financial system, and (c) sound government finances.

One half of the government’s brain seems to recognise the issue. They just extended the scheme whereby small businesses can get interest-free loans from the government. Quite why they think those favoured few – in many cases, probably some of the worst credits – should be able to borrow at zero while the rest of the economy (but especially the business sector) borrows at materially positive real interest rates, often complemented by tightening non-price conditions is a bit beyond me.

Oh, and remember that this surveys suggest banks expect credit conditions to tighten further from here.