Presumably someone pointed the Retirement Commissioner to my post yesterday ,as I gather the online version of the triennial report now has a “Foreword”, rather than the “Forward” that appeared until yesterday. We all make mistakes, typos, and literals, but you’d suppose that well-funded government agencies would have prominent parts of high-profile documents proofread. Anyway, enough of that (perhaps rather petty) point.

One other aspect of the Commissioner’s report that caught my eye was the bit about “ethical investment”. This was prompted by the government, which had asked the Commissioner to report on

Information about the public’s perception and understanding of ethical investments

in KiwiSaver, including:

a) The kinds of investments that New Zealanders may want to see excluded

by KiwiSaver providers; and

b) The range of KiwiSaver funds with an ethical investment mandate.

As I noted yesterday, there is a make-work element to the Commissioner’s role (and his supporting office, the so-called Commission for Financial Capability). You might have supposed that firms operating Kiwisaver schemes, or attempting to sell their products to managers of Kiwisaver funds, might be best placed to work out what, if any, investments “New Zealanders” didn’t want to invest in. It is a (potential) marketing opportunity, and one the providers are strongly-incentivised to tap. They also get to experiment, and see which products actually attract (or turn off) savers – revealed preference often being quite different than (say) idle costless, perhaps even virtue-signalling, response to surveys.

Strangely, the Retirement Commissioner starts this section of the report by mischaracterising the terms of reference

In term of reference five, the Government asked us to provide information about the public’s perception and understanding of ethical investment.

Except that (see above) that wasn’t what was asked for at all.

Anyway, they commissioned a report from consultants at KPMG. KPMG appear not to like the notion of “ethical” investment, and prefer “responsible investment” instead. I guess if you poll people and ask if they want “responsible investment” you’ll probably get 100 per cent saying yes. It all rapidly becomes rather empty – your “responsible” is, often enough, my “deeply corrosive”, and vice versa. You can read the KPMG report and all the discussion of how funds can/do try to take account of ESG (environmental, social, governance) considerations. But there isn’t really much there – in my observation (as trustee of a couple of funds) much of it is marketing hype. Perhaps the one bit of the KPMG report that caught my eye.

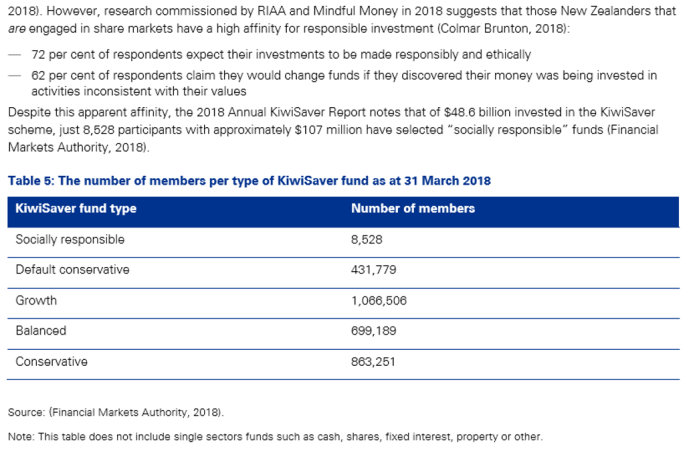

The key sentence is that one just above the table. It (and the data in the table) do not make into the Retirement Commissioner’s report.

The Retirement Commissioner’s report then moves on to public opinion noting that

In addition to the KPMG work, CFFC includes ethical investment in its own regular surveys of the public.

There is a footnote there to this internal note, but unfortunately there is no link to the full results of the poll, including either the exact wording of the questions or the respondent comments (selected ones of which are quoted in the report, but with no way to judge how representative these observations are).

They are keen to talk up the results

From this, we know that ethical investment is important to the majority of

respondents, with only 26% of overall respondents, and 18% of contributing KiwiSaver members, stating that they are NOT interested in ethical investment.

Actually, I was little surprised that 18 per cent of respondents were prepared to tell a survey taker that they had no interest in an ethical approach to their investments. But just saying it just doesn’t mean much.

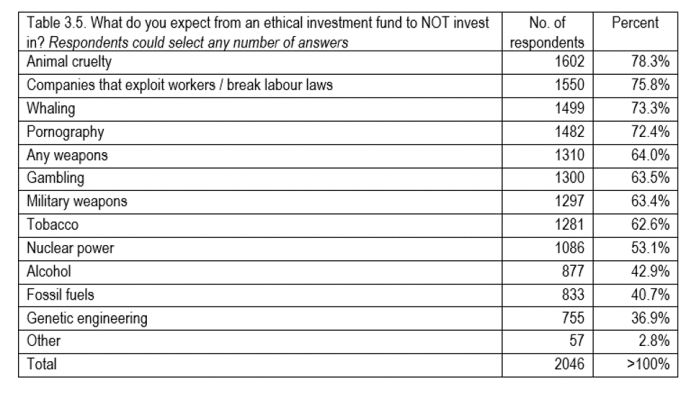

Anyway, this was the main table on specific types of industries (although it isn’t clear whether respondents were prompted – I’m guessing so – with this particular list, or whether everyone came up with their own preferences).

The Commissioner writes about this table thus

We also know that:

• In terms of which investment most want excluded from investments, animal cruelty, worker exploitation, whaling and pornography top the list, with over 70% of

respondents agreeing these are exclusion priorities.

But without knowing the precise wording of the question, we can’t even be sure that is right. The Commissioner seems to interpret the results as meaning people don’t want to invest in these industries, but the description in the table suggests the question might have along the lines of “if there were an “ethical investment fund which industries should be excluded”. They are two quite different things, as revealed preference seems to confirm. It is, for example, hard to believe that 43 per cent of New Zealanders really don’t want beer or wine company shares in their Kiwisaver investment – it not being 1918, and the near vote for Prohibition, actual teetollars being probably no more than 20 per cent of the population. But perhaps they think it is what an “ethical investment fund” might exclude? And since parties supporting disbanding the military are notable by their absence, one might also be a little sceptical about what people actually had in mind – feel-goodness apart – in their weapons answers.

(There is some interesting demographic data, notably that in all the categories above women were more likely to favour exclusion than men.)

Then it starts to get a bit awkward

A majority of respondents are satisfied with available ethical investment options within KiwiSaver and of those contributing, 70% are satisfied with the range of ethical investment options.

This high level of satisfaction is a surprise because most ethical investment funds do

not meet the expectations reported by survey participants.

But perhaps not so much, because in the internal research note – but not in the published report – we find this

However, only a minority selected ethical investment when asked about the criteria for selecting a fund. A possible explanation is that respondents show social desirability bias (select the “right” answer) when asked about ethical investment directly, but their actual behaviour shows limited consideration of ethical investment in KiwiSaver funds.

Revealed preference seems to be that the public don’t really care much at all (and/or, it might be hard/costly to evaluate funds for your own preferences).

But despite all this, the one recommendation in this section of the report is

PUBLICLY FUND MINDFUL MONEY TO ERASE ANY POTENTIAL CONFLICTS

OF INTEREST: INTRODUCE TAXPAYER FUNDING FOR MINDFUL MONEY TO GUARANTEE THE CHARITY CONTINUES TO PUBLISH UNBIASED, RESPONSIBLE INVESTMENT INFORMATION.

Of Mindful Money

Mindful Money is a charity that promotes ethical investment, and was recently

launched (September 2019) in response to the public demand for more knowledge

and options to invest ethically. Mindful Money’s mission statement is to: ‘empower

investors and make investment a force for good. Over the next five years we aim to

switch $6 billion of investment funds away from pollution, exploitation and inequality towards a low emissions, sustainable and inclusive economy.’

It is run by someone who was a Green Party MP until the last election.

So, the public show little practical sign of caring very much, civil society has set up its own entity (which has managed to attract some commissions for referrals) and yet one well-funded government agency’s proposal is that yet more public money should be pushed in the direction of this charity.

As they recognise, simply funnelling money to one brand-new private charity would be unusual

While conscious that the regular process would be to go to tender first, we think in

terms of efficiency and cost, and considering that the public want information now so that they can make informed choices that align with their personal values, funding Mindful Money is the most efficient and simple step for the Government to take.

Oh well, never mind about good process, or whether Mindful Money might just be channelling a particular subset of distastes….toss them some public money. Barry Coates must have welcomed the report.

As I noted at the start, the Retirement Commissioner was landed with this particular term of reference, so they had to write something. But how they responded was up to them, and it simply wasn’t particular thoughtful or rigorous, more about how do we get on the bandwagon.

In truth, ethical investment is hard, and something of challenge to each of us as to how much we care about particular issues. Personally, if I were buying company shares directly, I would refuse to purchase companies operating in the small handful of the sectors listed in the CFFC table above (gambling, pornography, and – depending on definition – animal cruelty). But there are plenty of other activites I would also refuse to invest in (including hospital companies providing abortions, any PRC company, companies that actively facilitate the interests of the worst regimes on the planet – including the PRC). That is easy to say, and actually fairly easy to do.

But once you get into collective investment vehicles – where the diversification gains and low transactions costs (and even PIE tax rates) are very real advantages – it quickly becomes very difficult. For example, much of my retirement savings is in a scheme I joined – as a manadatory condition of service – almost 40 years ago. My ethical views aren’t necessarily those of other members, and even though I’m a trustee of the scheme I have legal constraints on my ability to make what seem like ethical choices to me (and that is probably as it should be). I’d find it all but impossible to find a Kiwisaver vehicle offering my list of exclusions – and, on the other hand, I’m very happy to have an interest in shares in arms companies, oil companies etc – and so, in practice, I do not do anything about the issue. I’m a trustee of another pension fund – where there might actually be some commonality of ethical preferences among members – but even then it is difficult to get members to reveal those preferences consistently and (again) legal constraints.

But all of these issues are yet another reason why I favour winding up the New Zealand Superannuation Fund. Holding a particular Kiwisaver fund is strictly voluntary (you might not find an ideal fund, but there is quite a bit of choice), but your exposure or mine to the assets held in the New Zealand Superannuation is inescapable. They like to boast about what “responsible” investors they are, but all that really tells you is that they line up with the personal political/ethical preferences of Matt Whineray and his Board (or Adrian Orr before that). We simply should not have money coercively taken from us and invested in causes and companies we individually find distasteful, even reprehensible. That is true whether your burning concern (so to speak) is fossil fuels, pornography, marijuana, abortion, the whales, or whatever. There is no compelling public policy case for the fund, and the way its investment policy trespasses – ignores – the ethical preferences of many citizens simply further undermines that case.

Some thoughtful discussion of issues like that might usefully have found a place in the Retirement Commissioner’s report. It didn’t of course. Some hardheaded analysis of just how much people really valued “ethical investing” might have made it into the report. But it didn’t either.

It was a pretty disappointing report all round.

Of that list, I only see two that I wouldn’t count as non-ethical investment areas – genetic engineering and nuclear power. These two things are, at the very least, powerful tools to mitigate, if not militate against climate change. Regarding weapons, if ‘weapons’ was synonymous with cluster bombs or land mines I’d agree, but ‘weapons’ is not synonymous with cluster bombs or land mines. Besides, I hold to the maxim for nation states (not individuals) espoused by Winston Churchill: “peace-loving, pacifist to the core, but armed to the teeth”, because I have learned my lesson from history.

LikeLiked by 2 people

Delighted and mighty surprised to read your comment because I was just about to write the same. Investment in nuclear power is vital; it is an investment gamble but the only one that solves the basic climate change concern without abandoning the undeveloped world to perpetual poverty and deepening misery. Similarly genetic engineering is also a risky business investment but it is our best opportunity to feed an ever growing world population. I see investing in those two areas as a positive moral obligation. If the civilised world chooses not to invest in them then the uncivilised world will and then the risks multiply greatly.

LikeLike

The organic lobby would have you believe that GE is risky. Modern GE is indistinguishable in many cases from natural mutations, but the organic lobby hasn’t altered its arguments as technology improves. So “green” investments don’t always mean “scientific”.

LikeLike

As you say everyone has their definition of ethical, and the list is debatable but I’m surprised Michael that you didn’t include worker exploitation given:

Malachi 3:5

“Then I will draw near to you for judgement. I will be a swift witness against… those who oppress the hired worker in his wages”

Micah 6:8 “And what does the Lord require of you? To act justly and to love mercy…”

or James 5:4 “Behold, the wages of the labourers who mowed your fields, which you kept back by fraud, are crying out against you, and the cries of the harvesters have reached the ears of the Lord of hosts.”

Micah 6:8 in its totality is a personal creed of mine, and worker exploitation fits in this, even if the various measures of exploitation define exploitation more broadly than I would.

LikeLike

I don’t disagree, altho the ability of an outsider to judge what rises to the standard of exploitation is limited (the main reason I didn’t include it on my list).

LikeLike

I figured it would be something like that. I suppose that in the end there will always be people who are glad of sweat shop clothes (for example) because that is all they can afford, just as sweated workers may be glad that they have a job at all for any number of reasons, even if the job is hellish. Things are always greyer than polemicists would have us believe they are.

LikeLiked by 1 person

Yep… pretty ordinary stuff really.., investors care about their returns and not much else…

I expect thé hurray Harry crowd on LinkedIn will be full of praise for this poor effort and KPMG get to bank some smugness points for all of this too… Not to mention the cash..

A small data point explaining the Productivity gap in NZ.., sigh..,,

LikeLike

A small point but if phoned by Colmar Brunton and asked “if I expect my investments to be made responsibly and ethically” I would assume it related to how the investments were made not the nature of the business that the investment was in. I would assume ‘responsible’ would exclude investment managers who select a investment by throwing darts at a list, tossing dice or selecting the stock with the shortest name to make their paperwork easier. And ethically I’d assume owners of businesses were not paying them back-handers to inflate the value of the shares. As I discovered when reading specs and writing computer programs for a living the English language is dangerously ambiguous.

When my sister studied philosophy she told me that belief is judged by action not words; her example was an office manager who when asked said he believed men and women were equal but who then always employed the male candidates. You have to be very careful with surveys; in some cultures the answer is almost always what they think you want to hear and of course some awkward people (Scots and Kiwis IMHO) do the opposite. As you say the best way of judging ethical investment is to see what investors actually buy; that discloses both how significant the issue is to them and also what they consider ethical.

LikeLike

I would hire a woman but I would not work for a woman boss personally. Men and women have different strengths and weaknesses. Women tend to be far more detailed and less forgiving on errors and worry about minutae detail which leads to a more stressful work environment. Men tend to be more percentage driven and more forgiving on errors which leads to be a less stressful work environment.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

For most it is about the money. Ask if an investor would be prepared to take a 20% drop in returns for a fund where someone else chose what is considered ethical.

The numbers choosing an ethical fund in the table shown gives a good answer. Not many. However publicly, most pretend they care rather than risk an attack of fained outrage.

LikeLike

Guilty. I was very happy when I checked that my Kiwisaver returns this year jumped to 18% and dropped more money in without any questions. If it was a 20% drop I would have not put more money into Kiwisaver.

LikeLike

Kiwisaver Funds are managed index funds that are required to meet specific benchmarks in the investments they invest in – generally speaking they don’t/can’t invest in unlisted companies – Index Funds usually have a definition of their aims, purpose and activity

Table 3.5

How many listed NZ companies are involved in

1. Animal Cruelty

2. Whaling

3. Pornography

4. Nuclear Power

5. Companies that exploit workers

LikeLike

Mindful Money is a joke

LikeLike

Dear Michael, Don’t know if you’re aware, or for that matter, interested in the arrest of Dr Charles Lieber the chair of Harvard’s Chemistry Department and a pioneer in Nano technology; as reported in the Economist. Regards, Lyall Benjamin

LikeLike