The NCEA level 2 economics exam took place yesterday afternoon. I’d been helping my son with his revision and preparation, in the course of which he’d shown me various exams papers from recent years, and some guidance they’d been given on how to answer some of those (past) questions: what might get Achieved, what Merit, and what Excellence.

I wasn’t exactly reassured by what I saw.

As one example, consider this question from last year’s paper 91222 “Analyse inflation using economic concepts and models”.

The first questions were introduced with this statement

The Quantity Theory of Money states that the quantity of money circulating in the economy is equal to the monetary value of the goods and services available in the economy.

The quantity theory of money starts from the identity – for thus it is – MV=PT, where

M = some measure of the money supply,

P = some measure of the price level,

T= some measure of real economic activity (you could think of real GDP, but it generalises – think volume of transactions), and

V = the velocity of money (or how frequently the stock of money – as defined – turns over (“is spent”) in the period in question. It is generally derived residually.

All that identity is saying is that the amount of money that is spent (stock multiplied by times it is used) equals value of transactions in the money economy. The amount of money that is spent = the value of what it is spent on. Necessarily. By definition. Change your definition of money – the Reserve Bank publishes several, and there are others – and your V will change too.

As a New Zealand example, nominal GDP in the year to March 2019 was $300.994 billion. The Reserve Bank’s broad money measure averaged $304.193 billion over that year and its narrow money measure was $68.375 billion. So, on this measure of nominal activity, V(b) (“broad money velocity”) was 0.99 and V(n) (“narrow money velocity”) was 4.4.

MV=PT is really known as the equation of exchange, and it only turns into a theory (about behaviour) when expressed in the idea that if you change the quantity of money most of the effect will typically be seen in the price level (or that most changes in the price level stem from changes in “the money supply”). In the extreme, it is a simple enough idea – in massive hyperinflations there is lots more “money” around (on any measure) and much higher prices/inflation rates (on any measure. But the theory was mostly used in simpler stabler times (since in the midst of hyperinflations, not only does the velocity typically accelerate – no one wants to hold money longer than they have to – but real economic activity is also typically shrinking, perhaps rather a lot).

So what disconcerted me about the NZQA efforts?

Well, go back and look at that definition of the quantity theory of money. Does it mention the idea of velocity? No, not at all.

And then it talks of the “monetary value of the goods and services available”, which has a fairly strong sense of stocks, not flows. Any serious description of this equation/identity would stress that it is about transactions/turnover, not stuff that just happens to be around (whether sitting unsold on shop shelves, in factory inventories, or in the cupboards at home).

Now, in fairness to NZQA the very first question asks the students to label each of M, V, P, and T, so probably people wouldn’t be too misled by the omission of any sense of velocity in the introductory description. But shouldn’t our teachers/examiners be taking care to be as precise and careful as possible, both to set a good example, and so as not to risk confusing or distracting kids who have read/thought a bit deeper?

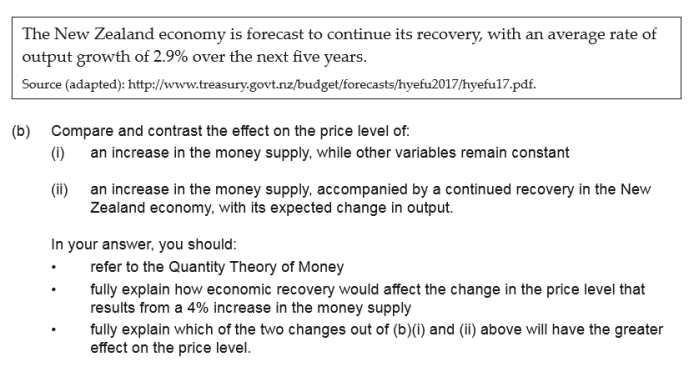

The next question reads

Using the Quantity Theory of Money equation, fully explain how a 4% increase in the money supply could affect the price level, assuming other variables are constant.

As I pointed out earlier that MV=PT is an identity, I hope you can see why this question isn’t written anywhere near as carefully as it should (and quite easily could) have been. In an identity with four variables, if one of those variables changes and two are held constant by assumptions, there is no “could” about what happens, but a “must”. If V and T are held constant and M increses by 4 per cent then. by definition, P increases by 4 per cent. Of necessity.

I checked the NZQA marking guide and it is clear that the examiners know this: they talk explicitly about how prices “will” rise by 4 per cent. But then why muddy the waters for the students? It isn’t even as if the marking guide says something like “students will get extra credit for pointing out that the 4 per cent price increase is a necessary implication, and there is no “could” about it.

The questions continue, with the third question designed to better winnow out the Excellence and Merit students from the Achieved ones. The third question starts with a quote from a Treasury document

You’ll notice that the Treasury projections quoted are for an average annual growth rate over the next five years. By contrast, the assumed exogenous increase in the money supply is a one-off levels increase.

The examiners don’t appear to have noticed the difference. It is clear what they are trying to get at (P will increase less if T is also rising than if it isn’t). That’s the answer to the third bullet above. But the marking schedule makes it clear that they expect the students to answer that in that growth scenario the price level will rise by (about) 1.1 per cent. But that isn’t the case at all: instead in the first year the price level would rise by about 1.1 per cent and then it each subsequent year it would fall by (about) 2.9 per cent (since T is changing and M no longer is). But, again, there is no hint that markers should give additional credit to students who point this out. (Although they do give extra credit to students who point out the V might change – perhaps rise – in a recovery.)

Again, there is really no excuse for questions this badly worded (for 16 year olds). They could easily have posed the questions as “if the money suppply increases by 4 per cent per annum, what will happen to the inflation rate if (a) all else (V) is constant and (b) if real economic growth (in T) happens per the Treasury projections”.

It is sloppy and loose, and suggests that the examiners (and those reviewing their drafts) just haven’t thought carefully enough. And that is even without posing questions about whether introducing year 12 kids to inflation using models that rely on exogenous money supply increases (when most increases in the money supply these days are actually endogonous – arise simultaneously with economic activity and the credit creation process) is that most helpful way to structure the curriculum.

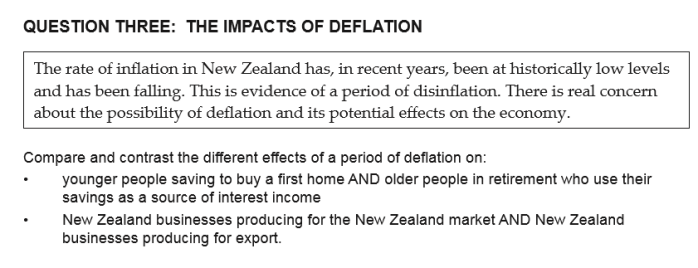

The other one that disconcerted was from the 2016 exam for the same level 2 NCEA standard (I didn’t go through them all systematically – these were just ones my son asked about). This was a question about deflation.

Here what disconcerted me (a lot) was the answers NZQA was looking for in its guidelines for markers. But the question wasn’t great either.

The key starting point for thinking about the effects of inflation/deflation is that, broadly speaking, there is long-run neutrality (most real variables won’t be much affected by trend inflation/deflation), but that distributional effects can be quite powerful in respect of unexpected inflation/deflation. Broadly speaking, (unexpected) deflation is great for people with fixed-term/rate bank deposits (the real purchasing power of their money rises) and dreadful for people with fixed-term/rate nominal debt (the real value of what they owe rises). Otherwise, all else equal, prices, wage, interest rates etc should all adjust to whatever the inflation/deflation rate is, and to much the same extent.

The questions don’t distinguish between expected and unexpected deflation. Perhaps that isn’t unreasonable for most year 12 students, (but what about those who had read on, or thought more deeply, perhaps even read an MPS?) but it does make quite a bit of difference, and it isn’t obvious that even the markers recognise the difference.

This is the sort of thing I mean. In answering the first part of the question, the markers are looking for this to get Achieved

Explains the effects of deflation in New Zealand on younger people saving for their first home (e.g. Deflation will mean that people saving to buy their first home will have a lower cost of living and be able to save more).

But this is simply nonsense since one would normally expect that wage inflation would be similarly lower and the real incomes of those young savers wouldn’t be affected, and nor (generally) would the real cost of the house they were saving for. But to the extent they already had saved some money – and especially if it was on a long-term fixed rate deposit – the real purchasing power of what they’ve saved will rise.

What about the old people. Again, the Achieved standard answer

Explains the effects of deflation on older people in retirement who use their savings to provide them with income (e.g. Older people may find that they receive lower interest income if interest rates fall to offset deflation).

Indeed they may, but…..the cost of living will be lower too. And, in fact, the real value of those bank deposits will actually increase in this scenario.

The marking guide goes on to elaborate points students would need to make to get Merit or Excellence. But it doesn’t really improve

Fully explains the effects of deflation on younger people saving for their first home (e.g. Younger people saving for their first home may benefit from deflation because it might increase the purchasing power of their income. This may mean that they can save more of their income to put towards the purchase of their home. It may also mean that the home may become cheaper. Deflation may also lead to lower interest rates and, therefore, make loan repayments more affordable).

That final point is fair (since mortgages are nominal the upfront servicing burden is a little easier), but it is something of a distraction because it doesn’t alter the servicing burden over the full life of the loan. And these guidance notes suggest the examiners have no sense that wage inflation will also typically be lower if there is price deflation.

Fully explains the effects of deflation on older people in retirement who use their savings to provide them with income (e.g. Older people in retirement who use their savings to provide them with income may find that the value of their assets falls, which means that selling those assets will result in less earnings. Also, if interest rates fall even though prices may have dropped, the people will receive less income and, therefore, may have falling purchasing power).

And this is worse. There is no hint that people with fixed nominal assets are those who gain from unexpected periods of deflation. And if the value of other assets (eg houses) they are selling falls, those falls will generally (all else equal) just be in line with the fall in the price level. That fall does not make old people (or any other seller) worse off. And, yes, nominal interest may fall, but there is no particular reason to expect real interest rates to fall (or thus for real purchasing power to fall).

The NZQA guidance answers to the second half of the question are only a little less bad. In fact for the “firms producing for the local market” I’m more or less okay with the required answer (as a year 12 simplification).

Fully explains the effects of deflation on NZ businesses producing for the local market (e.g. NZ businesses producing for the local market will find that the prices that they receive for their product may fall. They may also find that their costs of production fall and, therefore, the outcome may be either slightly worse off or neutral).

All else equal- and on a simple model – you would expect both costs and selling prices to be commensurately lower and such firms to be no better or worse off on this count. A really smart student might point out that if these firms had material debt outstanding, the real value of that debt would rise, but that is probably a complication too far for year 12 and this bit of the question didn’t mention debt.

But the exporting firms answer is more troubling

Fully explains the effects of deflation on NZ businesses producing for export (e.g. NZ businesses producing for export may also face falling costs of production; but if their markets do not have (or have less) deflation, then they may find that their profit margin rises and, therefore, they may be relatively better off).

But…….our exchange rate has been floating for 35+ years now, and I know year 12 kids get introduced to the exchange rate, and yet this suggested answer implies that the competitive position of our exporters can be improved by a period of deflation. Over any sustained period deflation here – not matched in other countries – would be expected, on simple models, to see an appreciation of our exchange rate, leaving New Zealand producers neither better nor worse off as a result. (These adjustments do actually tend to happen – you can see it in the trend appreciation of the NZD/AUD consistent with the slightly lower inflation target here than in Australia.)

You’d have to hope that a smart kid – or just moderately well-read or alert one (they do get exercises that involve looking at real world documents like MPSs – who made these points would get considerable credit from the markers, but if even the examiners don’t seem to be aware of the point, how many of the markers could be counted on to exercise some independent judgement.

Not one of the points I’ve made here is any sort of highly subtle or technical points. These are just the simple implications of pretty simple models – ie the sort of standard one might be looking for year 12 kids to be taught, and to be able to understand and repeat in examinations. But it isn’t clear, that on these questions at least, even the examiners quite understand what they are saying or asking, or how even a simple model works.

I haven’t engaged in a systematic study of all the recent economics exam papers (let alone those in other subjects, most of which I know less well). I’d really like to think that these two sets of questions I’ve highlighted in this post are exceptions and everything else is just fine. But, as we used to say in PNG when we saw a dead snake on the road, the real issue wasn’t so much welcoming the dead snake as wondering at all those still lurking in the same neighbourhood.

The New Zealand Initiative was out earlier this week calling for more emphasis on teaching specific bodies of knowledge in the various academic disciplines. I don’t really disagree with them, but when exams for upper-level kids have the sorts of weaknesses highlighted here it suggests there is quite a long way to go in even getting teachers equipped to offer a systematically better offering. As things stand, NZQA should be upping its game. Clear questions and correct answers (to guide markers) would be a good start.

Michael I am being a bit off topic and cheeky. But if you are interested would you mind commenting on or ‘marking’ the economics of my paper discussing carbon zero reforms?

View at Medium.com

LikeLike

Maslow’s hierarchy of needs refer to “Shelter” not warm and dry. The problem with warm and dry is utopia in a country as damp as NZ with 98% humidity. It makes it even more difficult when tenants cook and dry their clothing indoors. Yes you can run a dehumidifier or put in a heat pump but when the electricity bill starts ramping upwards these are left turned off and a basketball hoop hung at the end of it.

It all adds costs to the rental which in turn pushes up rents. There is no such thing as a free lunch. Someone pays for it.

LikeLike

Personally I do not have a heat pump, instead I use a dehumidifier for $800 and a duck feather/down blanket for $40 from the Warehouse but my Property Manager is asking for a heat pump which costs $3k for tenants.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

Interesting Michael.

last week I was sent a series of questions on macroeconomics from a client here, whose daughter is studying at a university in Australia and he wanted me to help him understand the questions she’d been asked. I went through them – Quantity Theory, IS-LM etc and the questions were so badly drafted, I ended up going back to him and saying, nope, can’t help. I was shocked at how loose and general the questions were and basically you couldn’t actually answer any of them given the information provided.

No wonder students don’t want to study economics anymore…

LikeLike

Sounds pretty bad. I’m going to be keeping a close eye on the NCEA paper this year. Having told Jonathan about what was wrong with the deflation answers in the mock answers the teacher had shown them, he came out of yesterday’s exam telling me there was a similar question this year.

LikeLike

Deflation seems to be put across as a positive for young people in lowering costs and increasing savings. Certainly I think NCEA have lost the plot because the fear of deflation is that economic activity falls. It comes down to purchasing behavior. If prices are falling, I can defer my buying until later to get a cheaper price. If everyone defers their buying activity waiting for a better price then you do not an economy. An economy requires people to buy and sell.

Not too sure why savings would be increasing as interest rates fall. As we have seen so far, as interest rates fall investment values rise as savings get put into investments rather than into savings. Although Balanced Funds do put 50% of those managed funds back into savings.

Can’t see how house prices would fall as interest rates fall it encourages diverting savings to housing investments.

LikeLike

Hi Michael I wonder if you might like to comment on this: https://www.interest.co.nz/opinion/102303/yao-yang-argues-basic-ingredients-sustained-growth-are-long-established-classical Thanks Dave

On Sat, 23 Nov 2019 at 12:30 PM, croaking cassandra wrote:

> Michael Reddell posted: “The NCEA level 2 economics exam took place > yesterday afternoon. I’d been helping my son with his revision and > preparation, in the course of which he’d shown me various exams papers from > recent years, and some guidance they’d been given on how to answer s” >

LikeLike

I have a fair amount of sympathy with his perspective – others have made a similar point – altho it is worth pointing out (as I do here every so often) that China is no better than a middle income country and doesn’t appear to have learned the lessons that would enable it to match, say, the far greater success of places like Taiwan, Singapore or even S Korea.

LikeLike

What China has done is similar to what those poor Asian countries have done before it. It invited rich western capital by providing low cost labour which increased western corporate margins. At the same time Intellectual property was required to be shared to use that cheap labour. Although Trump argues IP theft it is much simpler. When you train a person to do a job you inevitably pass on that IP knowledge base.

It pegged its currency to the USD so that it continued to enjoy a lower cost and gave western companies and their few shareholders their incredible wealth. But these countries clipped the ticket along the way through providing their labour for return of wages. Therein lies the preoccupation with savings because these savings is effectively the wealth transferred from wealthy western nations.

I met a retired general of the Red Army and he said they captured a French Exocet missile and gave it to their top scientists to reverse engineer. After a year of trying, their chief scientist replied they did not have a clue. Their top brass panicked and decided they were so far behind the knowledge curve they had nothing to hide behind the bamboo curtain so they opened up for their people to initially study in foreign universities and that led to inviting foreign capital after sending thousands of chinese administrators to spend some time in Singapore.

LikeLike

And it wasn’t just economics:

https://i.stuff.co.nz/national/education/117701992/what-was-wrong-with-the-ncea-level-2-maths-problem

LikeLike