A passing comment in a post the other day about the labour force participation rates of older people prompted me to pull down the fuller data and see what we could see about various participation rates over the decades since the HLFS began in 1986. As it happens, the unemployment rate in 1986 averaged 4.2 per cent, exactly the same as the current unemployment rate, so cyclical factors shouldn’t materially mess up long-term comparisons.

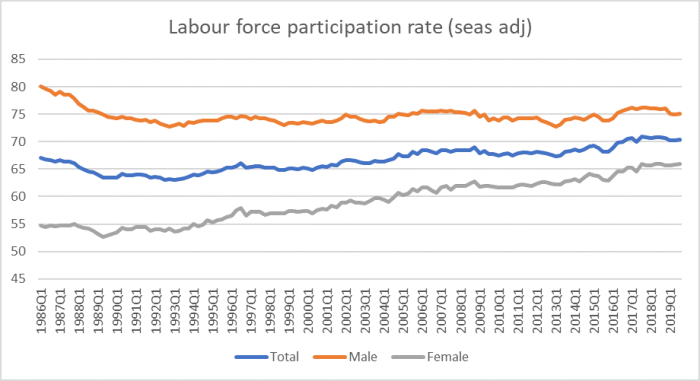

Here are the quarterly participation rates (employed plus unemployed as a percentage of the working age (15+) population.

From which I’d make only three quick observations:

- how stable the male participation rate has been since the end of the 1980s (even through a couple of very nasty recessions),

- the strong upward trend in the female participation rate, and

- while there is some modest cyclicality in the overall participation rate, it isn’t a stable or reliable cyclical indicator (eg the peak in the 00s was a year after the recession started, while the 90s peak was a year or so before the recession started).

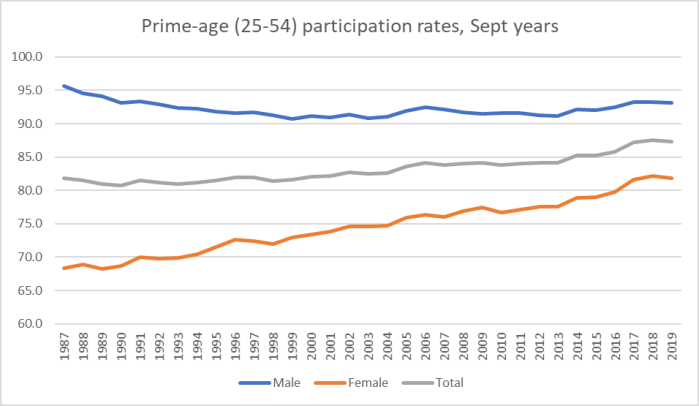

But aggregates can mask a lot of interesting patterns, and around participation rates that has been particularly so for men (the female participation rates are just dominated by the strong upward underlying trend). From here on, I’m using annual data (years to September), as there is less noise and more data reliability for some of the small age groupings.

Here is the data on participation rate for what you often see referred to as “prime age” people, those aged 25-54.

Prime-age male participation isn’t back to where it was in the 1980s but over the last couple of years it has been higher than the 2000s peak.

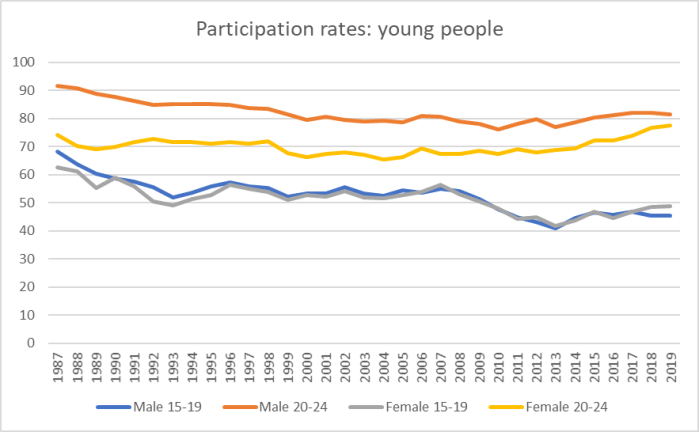

What about the two youngest age bands?

In the 1980s (until 1989), people could leave school at 15, but I was interested – and a bit surprised – in the further step down in the participation rates of the 15-19 year olds ver the last 15 years or so. Presumably there is some mix of factors at work: kids being less likely these days to have after-school jobs that was once the case, minimum wage changes, and…… Given the cost of tertiary education now (relative to say the 1980s) it still surprises me though.

Perhaps the bigger surprise though (at least to me) is that only around 80 per cent of 20-24 year olds are in the labour force. You only need to have done one hour’s paid work in the reference week, or to have actively looked for work, to be included in this measure.

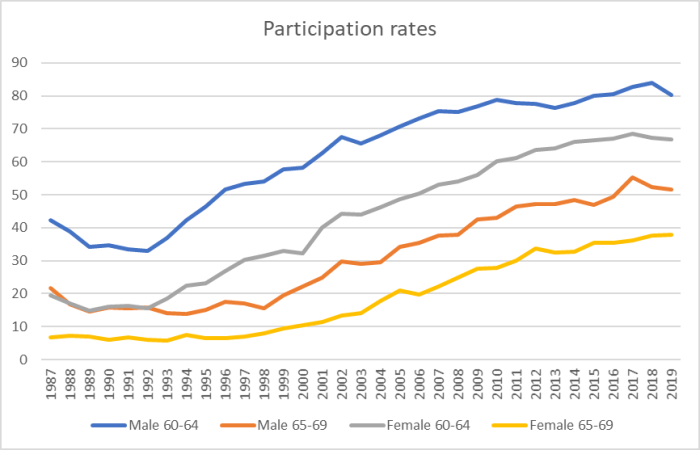

What sparked the post initially was participation rates of those in the older age groups. Here are those for the 55-64 age.

Participation rates for this age group are much higher than they were for both men and women. When the data start, the full rate of New Zealand Superannuation was available at age 60 (at, if I recall correctly, a higher rate relative to wages than is the case now). I was a little surprised to note the dip in participation rates in the last couple of years: for this group of women the latest observation was lower than in any year since 2013.

Participation rates for this age group are much higher than they were for both men and women. When the data start, the full rate of New Zealand Superannuation was available at age 60 (at, if I recall correctly, a higher rate relative to wages than is the case now). I was a little surprised to note the dip in participation rates in the last couple of years: for this group of women the latest observation was lower than in any year since 2013.

And what about the participation rates of those 65 and over, almost all of whom have been eligible for NZS throughout?

There has been some increase in participarion rates for those aged 70 and over, but the really striking movement has been in the 65-69 age group. More than half of men, and almost 40 per cent of women, in this first NZS recipient age group, are still in the labour force. (Interestingly, the gap between male and female participation rates for this age group hasn’t materially changed over the 30+ years of the chart.)

And here is the comparisons between those aged 60-64 and those aged 65-69.

In my post last week, I noted that the participation rates of those now aged 65-69 were higher than those for people aged 60-64 when the survey started, at a time when the NZS eligibility age was still 60. I see this as a fact buttressing the case for raising the NZS eligibility age now (to, say, 68, and life expectancy indexing beyond that). By some mix of revealed preference to work, and of need, large proportions of the population went on working for some years after being eligible for a universal pension, suggesting not only that they were physically capable of doing so, but that many of their peers who chose not to work would also be physically capable of doing so.

However, the comparative story over time is complicated at least a little by changing norms and expectations around female participation. In 1987 under 20 per cent of women aged 60-64 were in the labour force: these were women born in the 1920s, (mostly) mothers of the first baby boomers at a time when female prime-age employment wasn’t that common. Now almost 40 per cent of women 65-69 are in the labour force, almost as high a share as for the 60-64 year old males in the late 80s. The increase in participation rates among males – today’s 65-69 year old compared with 1987’s 60-64 year olds is real, but less dramatic – up from just over 40 per cent to just over 50 per cent.

And just to end, a couple of international comparisons charts re participation rates for those aged 65-69.

Here is the participation rate in 2018

It really is an astonishing range. It isn’t correlated with prosperity (there are poor performers at either end of the chart) or, that I could see, with life expectancy or health status. I suspect – but haven’t checked – it is pretty strongly correlated with the abatement regimes (if any) around state pension. One of the best things about the New Zealand system is that although NZS provides an income effect encouraging people to think about stopping work, there is no relative price or substitution effect: as an older person you can work as much as you like and it doesn’t affect how much NZS you receive. In many countries, the rules aren’t like that; it often isn’t economically attractive to go working.

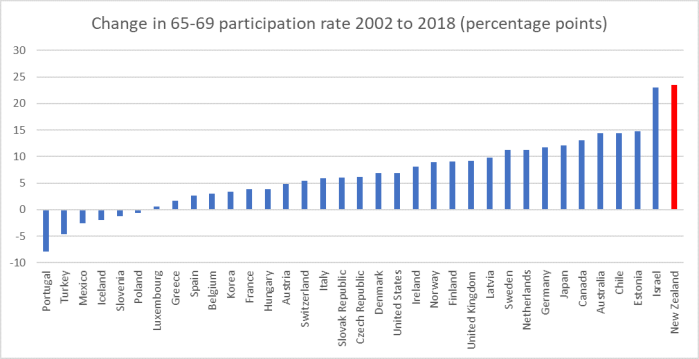

And what about the change over time in the proportion of those 65-69 in the labour force? The OECD has complete date only since 2002 so here is the change since then.

What I found interesting about that statistic for New Zealand is that that further large increase in the 65 to 69 participation rate has been exclusively in the years since the NZS eligibility age got to 65 (in 2002). You can see in the chart above that our participation rates for those 60-64 also increased markedly over that period.

I’m not one of those inclined to celebrate (paid) labour for labour’s sake. I don’t think I was when I was in the paid workforce and I’m certainly not now. But when the alternative is state income support then I do take a harder line view. If you are able to work and are financially able not to, that is almost entirely a matter of individual/family choice, but you (generally) shouldn’t be eligible for long-term state income support. New Zealand’s experience suggests that the overwhelming bulk of those aged, say, 65-67 are well able to work (we don’t have the data, but presumably – given what happens from 70 on (see above) – participation rates of those 68 and 69 are materially lower than those for people 65-67). Against that backdrop, there is something just wrong about having a universal pension paid to them – well, me not that many years hence on current policy – simply on the basis of having got to that age.

Fans of a Universal Basic Income will, of course, not agree. I am not a fan, having both practical and moral objections to a UBI.

Unfortunately state assistance is so pitiful that the old cannot afford to retire but have to continue to slog on at a much reduced pace and at a much reduced wage to supplement the Universal Super payments.

LikeLiked by 3 people

National Super already costs the country $10 billion a year and you call it pitiful – cry me a river!

LikeLike

The fact that it costs $10B/year does not negate the fact that it is inadequate. I know many people in that situation. Progressives are so concentrated on identity politics that they think the white working class doesn’t matter.

https://blogs.lse.ac.uk/researchingsociology/2016/11/17/sociology-has-a-trump-problem

LikeLike

Actually the 2019 budget NZ Super it is more like $15 billion or 55% of the Social Welfare Development budget. That is why we need a growing population. A shrinking tax pool does not quite cut it.

LikeLike

From my experience, many in my age group (now over 70) expected to retire at around 60 on a good ‘defined benefit’ pension. The 1987 crash which hit NZ harder than elsewhere resulted in many such pension funds being closed down, or disappearing along with the rest of the bankruptcy losses. So many of us had to start again to prepare financially for retirement. In the United States there is a looming financial problem for those expecting a pension from their employer, the latter who only added IOUs to the fund rather than actual cash for independent investment. The ‘pension deficit’ world-wide is real … I quote “According to a Citibank report from 2016, the 20 largest OECD countries alone have a US$78 trillion shortfall in funding pay-as-you-go and defined benefit public pensions’ obligations. This shortfall is far from trivial. It is equivalent to about 1.8 times the value of these countries’ collective national debt.” (downloaded 11 November 2019, http://theconversation.com/huge-pension-fund-deficits-are-a-global-crisis-in-waiting-88420).

It really annoys me when there are calls/statements/musing that people should forego State pensions if they are still in employment. We still pay taxes on our earnings and the Nat Sup is subject to the top marginal rate, so there is an abatement factor. My few months salting away my Nat Sup before retirement allowed me to keep up my health insurance. The public system has been saved the $100,000 plus that my prostate cancer treatments have run to, which is substantially more than the Nat Sup for a couple of years post 65.

Many employees and employers use the Nat Sup availability for staff to ease into retirement, reducing their hours but still making their institutional knowledge available to the employer.

And it is not as though the recipients burn the extra money received – it goes into reinvestment, savings and consumption – so the economy does not lose it. And don’t get me on to central banks screwing our savings by driving down interest rates to near zero, with the threat of negative returns. And after we have chewed through our capital, what then? Oh, I forgot. We have the Nat Sup to fall back on.

LikeLiked by 2 people

I know people my age and less in Australia who are very careful not to earn or hide what they do. I started a small business three years ago and am earning a good amount by any standard and pay provisional tax. I am 82 female and plan to continue while I can into the forseeable future. It certainly pays for a lot more. I have upgraded lots around our 30 year old house, employ more trades people, have taken more holidays and helped family.

LikeLiked by 1 person

Your graphs underestimate the number of pensioners working. Our high streets are full of charity shops; far more than when i grew up; and they are full of unpaid pensioners stacking and selling the goods.

Maybe you are not actually comparing like with like. A typical pensioner fifty years ago was surveying their grave plot now they are booking cruise liners and cycling holidays. It would be interesting to see graphs for the last ten years of life; that might compare the 1980s 65-75 year olds with todays 75-85 year olds.

My comments support your point that superannuation should start 15 years before averge life span. We would have to ignore arguments for different retirement ages men -v- women, European -v- Maori -v- Asian, smokers -v- non-smokers and even left -v- right handedness.

LikeLike

Re your first point, yes volunteering is pretty common and also (often) demonstrates physical capacity. Not sure if there is more volunteering than there was in decades past, but it takes different forms (notably, as you say, charity shops now).

I would probably be prepared to defend a system in which we only paid a universal pension at age 80+ and for anyone younger than that support would depend on demonstrating physical incapacity to work. 80 might be a bit high, but my point is to focus us on the idea that if we are paying out conditional only on age it should be an age where the clear majority are really beyond doing anything like a 35 hour week (and at that point I’d err on the generous side).

LikeLike

Our previous retirement commissioner pointed out if you are a manual labourer then on avrage fifty is too old to hold down your job. They are at another disadvantage – you cannot easily change from manual labour to an office job whereas given sufficient fitness the reverse is possible.

Universal benefits work – there is minimum admin and minimal fiddles. Delaying to 80 would lead to significant claims for special needs benefits – the incentive would be to reduce savings to a minimum either by riotous living, hiding cash or presents for the kids. The current system with those who chose working and getting their superannuation works – it is just the age limit and the accommodation allowances that need reviewing. I can imagine a system where a universal benefit is introduced in stages – 20% at 65, 40% at 66, etc.

LikeLike

I have always supported something along the lines of Peter Dunne’s proposal that you can get National Super at a younger age (from 60 onwards) but at a lower rate (which would still be better than the unemployment benefit) and get it at a higher rate if you delay taking it until you are over 65 because you are still earning a good income. Dunne had the maximum age to delay to as 70 but I would set it much higher.

I know there would be a self selection bias to those who live longer so the extra reward for delay should calculated very conservatively. I think such a system would encourage a significant number of over 65s to delay collecting their National Super.

LikeLike

So what is the biggest factor in house prices immigration or baby boomers? Eaqub being a cheerleader for immigration?

https://www.stuff.co.nz/business/property/117270716/home-ownership-at-lowest-level-in-70-years-economist-says-baby-boomers-to-blame

LikeLike

I take it from your comment that the participation stat only requires a small threshold of work before it counts as participation? If so, my own impression (purely anecdotal, based on my parents and their cohort that I see) is that while many are still working, the hours are not full time fixed, but more consulting based and flexible. Are there accessible data showing average earnings for this cohort? Surely that would give a rough picture on how much they are working?

In Germany it is extremely uncommon for people to work post retirement age. From my understanding the basic law would provide you continue contributing to your “retirement insurance” and “elderly care insurance” but without any improvement in your retirement payment (prior to 65, everything you contribute reflects in the post retirement pay). On top, numerous collective agreements provide for other benefits like early retirement – if you take that its on the condition you do not work again.

The lower rate of participation for 15-19 is interesting – I would suggest the missing group are winding up on sickness benefit. This seems the popular dumping ground for the unemployable – medicalising the general social malaise leading to their unemployability (e.g. “marijuana addiction” preventing them from working)…

LikeLike

In the tourist industry there are 80 year olds driving buses (14 hour days). Like London taxi drivers that part of the brain seems to expand.

LikeLike

Having 80 year olds drive a bus is a major health and safety concern. I have watched a 70 year old run a red light and slammed into me because he thought a green left turn traffic light sign looked the same as a green light to go straight. After lodging a dangerous driver report with police for them to take further action, I found that this same driver had run the same traffic light 3 times already over the last 12 months. Because no one was injured so far the police allowed him to continue to drive. I was lucky that I did not sideswipe a whole bunch of pedestrians as he hit me on my back wheel and spun my car around 360 degrees.

LikeLike

I hear you but this driver trains other drivers and negotiated all the earthquake paraphernalia in a 13 meter bus on the annual training run. The initial issue for a coach company is not damaging the hardware. The worry is a driver having a sudden heart attack – (or stroke). Stress can bring on heart erythema in a healthy person.

LikeLike

not erythema ….. arrhythmia

LikeLike

That participation rates for the NZ 65+ cohort are greater than AU is both surprising and unsurprising. Australia’s Centrelink is ruthless in administering the Old Age Pension. $250,000 is the capped amount for receiving the full pension entitlement. Thereafter it is reduced up to a limit of $750,000 when it ceases. The compulsory superannuation has been running for 35 years now and many/most who have been in the scheme since 1986 would ineligible by now as having greater than $1 million (at least) in cash equivalents from the compulsory superannuation. So a great success in that regard. With that sort of cash assets there is not a lot of incentive to continue working.

The greater incentive comes from those who for reasons of unemployment or ill health have not benefitted from compulsory superannuation, are dependent on the Centrelink Pension and are pressed to continue to work to meet their needs

Given similar conditions, the gap between Australia and New Zealand must increase for many years to come. NZ Super is not a lot to survive on and there are a lot of people who do not voluntarily participate in Kiwisaver in addition to those who cant

LikeLike

Omitted to say the Australian Pension is means tested

LikeLike

Given reasonable health we all want to live longer. Scientists are searching for ways to achieve it. What if the succeed and do so soon? Any solution will be somewhere on the spectrum of cheap to very expensive (for example tweaking the cells DNA to make it young could be immensely expensive or possibly just a simple injection); either way it would destroy our current system of superannuation and impact NZ’s population plan (if one exists). Worth having the discussion before it happens.

LikeLiked by 1 person