Fifteen years ago now Parliament passed an amendment to the Public Finance Act requiring that every four years or so

the Treasury must prepare a statement on the long-term fiscal position

There is nothing in the Act as to what these long-term statement should cover, just a minimum time horizon” “at least 40 consecutive financial years”.

This wasn’t a pathbreaking fiscal reform by New Zealand. By the time our amendment was enacted a fair range of other OECD countries had somewhat similar requirements (see table on page 4).

Fifteeen years ago I probably thought this new requirement was a good thing. I’m much more sceptical now It is unlikely that such reports do much harm, but:

- they cost a lot to do (at least as Treasury typically does them – the legal requirements could probably be met with a two page report),

- come around much more frequently than any underlying issues change, and

- there is little sign that long-term fiscal management is any better for them existing.

There are fiscally reckless countries and fiscally cautious countries, and there were both types before and after the introduction of long-term fiscal reports. It isn’t obvious which country has switched sides (or moved much at all) as a result of these sorts of reports. New Zealand, after all, introduced the requirement when our own fiscal surpluses were around an all-time high already.

What is more, the underlying issues are really pretty obvious to blind Freddy. Here is what I wrote when the last Long-Term Fiscal Statement was released in late 2016

The Treasury yesterday released its latest Long-Term Fiscal Statement. These documents, in some form or other, are now required under the Public Finance Act to be published at least every four years. I was once a fan, but I’ve become progressively more sceptical about their value. There is a requirement to focus at least 40 years ahead, which sounds very prudent and responsible. But, in fact, it doesn’t take much analysis to realise that (a) permanently increasing the share of government expenditure without increasing commensurately government revenue will, over time, run government finances into trouble, and (b) that offering a flat universal pension payment to an ever-increasing share of the population is a good example of a policy that increases the share of government expenditure in GDP. We all know that. Even politicians know that. And although Treasury often produces an interesting range of background analysis, there really isn’t much more to it than that. Changes in productivity growth rate assumptions don’t matter much (long-term fiscally) and nor do changes in immigration assumptions. What matters is permanent (well, long-term) spending and revenue choices.

There really isn’t much more to it than that.

That statement was released in November 2016, which means – time flying as it does – the next report is due next year. A Treasury that wanted impact might reasonably be expected to publish before the election, and if they do that they need to be sufficiently early in the year not to be caught up in the immediate highly partisan pre-election period.

As it happens I went to an event at Victoria University the other day at which one of Treasury’s researchers was presenting some modelling results of work done for the next Long-Term Fiscal Statement. I can’t tell you about those results, but it did get me thinking about some of the past Statements and wondering how they looked with the passage of time.

In my excerpt above I referred only to spending on New Zealand Superannuation which, on current policies, will rise indefinitely as a share of GDP so long as life expectancy keeps increasing. But the other big issue – which sage Treasury officials will sometimes suggest is really the bigger one – is health spending. There are new technologies and drugs, rising public demand, not much productivity growth (at least in the health sector in New Zealand), and an ageing population itself seems likely to create additional cost pressures.

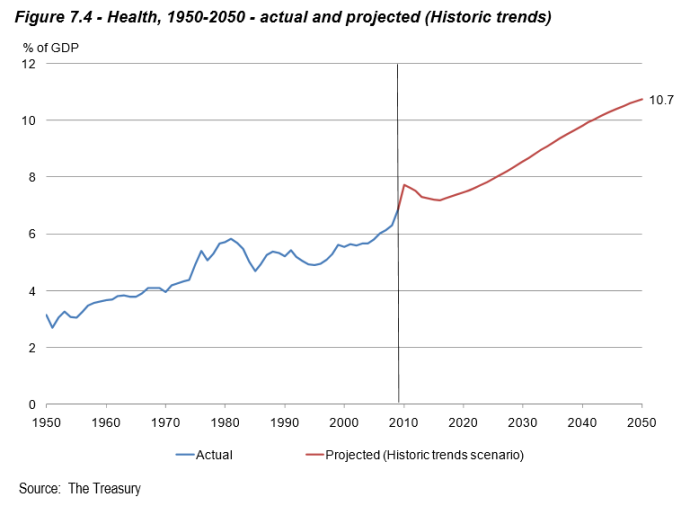

This is the sort of chart The Treasury likes to show, from the background papers to the 2009 Long-Term Fiscal Statement.

On those numbers, health would be a simply huge fiscal pressure, and the case for higher taxes might be hard to resist.

I’ve always been a bit more sceptical that health is quite the issue it is sometimes made out to be. That is mostly because there are so many more dimensions on which government health spending can be adjusted than there are around NZS (for the latter, one can play with the age of eligibility, the rate, and the indexation formula, all of which get a lot of attention) and the societally-accepted boundaries are fuzzier (whose GP visits should be free or heavily subsidised, how much should be spent on drugs, how much other rationing should there be).

Anyway, on that 2009 Treasury chart, the projecting forward of historical trends (as Treasury did it) would have had government health spending by now (year to June 2020) well in excess of 7 per cent of GDP (eyeballing the chart suggests about 7.3 per cent). Here is a chart from a recent post including budget numbers for the current (to June 2020) year.

Government health spending now is sitting just on 6 per cent. It was about 6 per cent in the year to June 2008 (just prior to the recession) and not much below 6 per cent forty years (note that period – the LTFS statutory focus) ago.

Now, quite possibly there is a totally unsustainable huge shortfall in government health spending at present. But if so, none of the political parties is making that case (notwithstanding the rhetoric from Labour in the last campaign) or doing anything very much about, and since the issues around fiscal policy are really political in nature (how easy/hard is it to make decent choices in a timely way) it does suggest that the margins are more fluid, the fiscal outlook more readily malleable, than the quadrennial publications from The Treasury are sometimes taken as suggesting. The system copes, and adjusts, perhaps less elegantly than officials might like, but that it does so nonetheless. That is consistent with, now, 30 years of fairly sensible, often quite conservative, fiscal management by governments led by both main parties. Adjustment rarely, if ever, occurs in response to projections 30 or 40 years ahead, but to pressures that become apparent within much more near-term windows.

As for NZS itself, personally I’m not overly interested in arguing the case for reform on fiscal grounds but on a rather more moral ground. Even if we could afford it, even if there were no productive costs from the deadweight costs of the associated taxes, there just seems something wrong to me in providing a universal liveable income to every person aged 65 or over (subject only to undemanding residence requirements). 45 per cent of those 65-69 are now in the labour force – suggesting they are physically able to work – which is substantially greater than the 30 per cent of those aged 60-64 who were in the labour force 30 years ago when NZS eligibility was at age 60.

I don’t consider myself a welfare hardliner. I think society should treat quite generously those genuinely unable to work, especially those who find themselves in that position unforeseeably. Old age isn’t one of those (unforeseeable) conditions, but personally, I have no particular problem with something like the current flat rate of NZS, or even of indexing it to wage movements (which would be likely to happen over time anytime, whether it was the formal mechanism from year to year), from some age where we can generally agree a large proportion of the population might not be able to hold down much of a job. I don’t have a problem with not being overly demanding in tests for those finding work increasingly physicallydifficult beyond, say, 60. But what is right or fair about a universal flat rate paid – by the rest of the population – to a group where almost half are working anyway? It is why I would favour raising the NZS age to, say, 68 now (in pretty short order) and then indexing the age in line with further improvements in life expectancy, and I’d favour that approach even if long-term fiscal forecasts showed large surpluses for decades to come. At the margin, I’d reinforce that policy change with a provision that you have to have lived in New Zealand for 30 years after age 20 to be eligible for full NZS (a pro-rated payment for people with, say, between 10 and 30 years of actual residence). Why? Because in general you should only be expected to be supported by the people of New Zealand, unconditionally, in your old age, if most of your adult life was spent as part of this society.

Reasonable people can, of course, debate these suggestions. But they are where I think the debate should be – about what sort of society we should be, what sort of mix between self-reliance and public provision there should be, even about what mix of family support and public support there should be, or what (if any) stigma should attach to be funded by the taxpayer in old age – not, mostly, about long-term fiscal forecasts.

“I went to an event at Victoria University the other day at which one of Treasury’s researchers was presenting some modelling results of work done for the next Long-Term Fiscal Statement. I can’t tell you about those results”

Why not?

That is the second time in the space of 4 weeks you have referred to such addresses

Is this chinese walls territory. How carefully are the attendees selected. How many attend? How sensitive is the material?

It’s troublesome. Alarm bells

LikeLike

It was a research day (mostly geeky papers in draft) run by the Chair in Public Finance. Anyone on their mailing list was invited. Most attendees (30 or so in total) were academics and public servants, with a few retired people like me, and a couple of pte sector people on the attendee list.

Were I Treasury I would probably be hesitant about presenting such material to such a forum, but on the other hand there is merit in govt depts testing their draft thinking and work with selected people outside govt, provided it isn’t – as this wasn’t – market-sensitive. And the public finance chair is partly funded by Treasury.

https://www.victoria.ac.nz/sacl/centres-and-institutes/chair-in-public-finance

LikeLike

I cannot find any room to disagree with you about increasing NZS age to 68 and “” indexing the age in line with further improvements in life expectancy “”. Clearly it should be controlled by anticipated lifespan.

There can be quibbles about the specific age of 68 ~ I can imagine my working wife would complain about having to work for longer than I did but that could be handled by variations in the rate so leaving her when retired getting more than me.

Is your proposal to have a pro-rata payment for people with between 10 and 30 years living in NZ the same as the current system in the UK? If so does it work there? I expect you will get objections that it discriminates against immigrants from 3rd world countries since immigrants from more advanced countries will be bringing their state pension with them to NZ (where it is deducted from NZS).

What is your opinion of NZ having a lower married rate? Surely it is nudging couples to break up before they retire (the accommodation supplement benefit works in much the same way). For the mental and physical health of New Zealanders the govt should be going out of its way to keep families together (and I don’t mean the current reality of having rents so high that children never leave home).

LikeLike

I don’t know about the UK system. It might lead to complaints of “discrimination” as you suggest, but they’d be ill-founded: it isn’t NZ’s responsibility to provide for people who come to NZ fairly late in life, and any reduced NZ pension is one of the things they should take account of in deciding to immigrate.

I don’t have any problem with the married NZS rate being lower than two single rates: living costs are less for two together than for one alone. Since the “married” rate applies to non-married partners too, a couple would have to totally separate and not get together with anyone else for it to be a financial benefit…..and one might feel more sorry than anything for anyone mad enough to do it (of people who were on the brink of breaking up anyway, it is hard to imagine the NZS rate really being the straw that finally broke the camel’s back).

All that sort, I’m a strong proponent of marriage, and go as far as lamening that neither main political party will ever say they believe it is desirable/helpful/fundamental unit of society etc etc.

LikeLike

I am a strong proponent of marriage too. The evidence is overwhelming that in general it works. Many obvious exceptions but if we want a society which minimises mental health problems, drugs addiction, crime, etc then marriage is then best solution. Therefore I object to any govt tax or benefit that persuades people and especially parents to be apart. If you are poor it does make a difference ref: “”The co-leader of the New Zealand Green party Metiria Turei has resigned citing unbearable pressure after she revealed that she had lied to claim more benefits as a single mother more than twenty years ago.””

The word ‘marriage’ has changed – 15 years ago even the most radical would have defined it using the words ‘male’ and ‘female’. The main feature across all cultures is marriage being a public statement of commitment. Given that marriage is a highly desirable, fundamental unit of society the govt should say so and reward it. How about a $5,000 marriage present from the govt for each first marriage and then permitting sharing of incomes for tax purposes if married and cohabiting. Surely a wiser idea than subsidising buying a first home.

LikeLike

Of course Turei’s issue was a bit different than an NZS one, as in the latter case both partners are individually entitled to a benefit, just a slightly smaller one.

LikeLike