This morning I wrote about the choice to cut by 50 basis points and the issues it raised, in context, about the Bank’s communications (non-existent speeches being only the most obvious omission). In this post, I want to focus on a few other specific issues that came up in the Monetary Policy Statement itself or in the Governor’s press conference.

The first was around fiscal policy. The Governor is clearly a big fan of the government spending more – “of course the government has to be spending more”. As a centre-left voter, I guess that is his personal prerogative, but it isn’t clear that it is his place to use his official office to weigh on highly political issues for which he is not charged with responsibility. Imagine, if you will, that he was calling for cuts to government spending. It would be equally inappropriate.

But, much as we shouldn’t just slide past the way he abuses the constraints on his office to advance personal causes, that wasn’t really what bothered me yesterday. The much bigger concern was the way the Governor blatantly misrepresented the actual fiscal situation. He claimed to be concerned only that the government wouldn’t be able to spend fast enough (given “capacity constraints”), which might reasonably have prompted a question of why, if government activity would be crowded out, he and his colleagues were slashing the OCR by 50 points in one go.

In fact, it prompted the perfectly reasonable question from Bernard Hickey about whether fiscal policy was actually very stimulatory at all. The standard reference here is The Treasury’s fiscal impulse measure. This is the chart from the Budget documents

It isn’t a perfect measure by any means, and in particular one can argue about some of the historical numbers. In my experience, it is a pretty useful encapsulation of the fiscal impulse (boost to demand) for the forecast period. In fact, the measure was originally developed for the Reserve Bank – which wanted to know how best to translate published forecast plans into estimated effects on domestic demand/activity.

And what do we see. There was a moderately significant fiscal impulse in the year to June 2019. That year ended six weeks ago. For current and next June years, the net fiscal impulse is about zero, and beyond that – which doesn’t mean much at this stage – the impulse is moderately negative. All using the government’s own budget numbers. And consistent with this, operating revenue in 2023 is projected to be higher as a share of GDP than it is now, and operating expenses are projected to be lower (share of GDP) than they are now. The Budget is projected to be in (fairly modest) surplus throughout.

And yet challenged on this, the Governor seemed to be just making things up when he claimed that we had a “very pro-active fiscal authority” and that “the foot is on the fiscal accelerator”. It just isn’t. Orr must know that (after all, he had Treasury’s Deputy Secretary for macro sitting as an observer in this MPS round). One even felt a little sorry for the Bank’s chief economist spluttering to try to square the circle, but basically acknowledging that Hickey’s story was right, not the Governor’s. Perhaps, you might wonder, the Bank thinks the fiscal impulse measure is materially misleading and has its own alternative analysis of the government’s announced fiscal plans. But that can’t be so either: there is no discussion of the issue in the Monetary Policy Statement.

(Incidentally, on Morning Report this morning Grant Robertson tried the same sort of line, only for the presenter to point out to him the fiscal impulse measure, reducing the Minister to spluttering “but we are spending more than the last lot”. That is true, but the material overall fiscal boost was last year – and growth and activity were insipid even then, inflation still undershooting the target.)

Was he being deliberately dishonest or simply making stuff up as he went protraying things as he’d like them to be? You can be the judge, but neither alternative puts our central bank Governor in a good light.

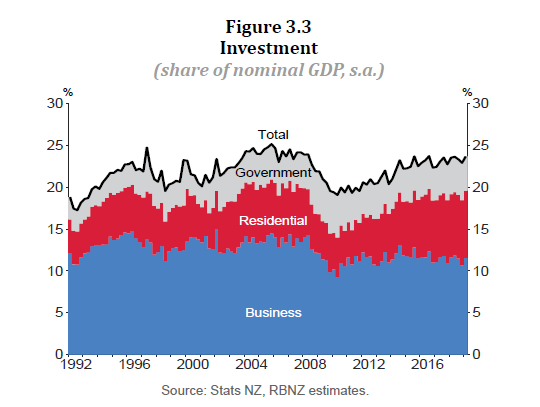

Another joint act – coordinated or not – from the Minister and Governor was around investment. As a nice change, the Bank included a chart of nominal investment as a share of nominal GDP (the approach favoured on this blog)

As I’ve noted here repeatedly, business investment never recovered strongly from the last recession, and if anything (as share of GDP) has been falling back again in the lasdt few years, even as population growth remained strong. It was good to see the Bank focus on the issue.

But despite the feeble business investment performance, the Bank expects business investment to recover from here. There is no hint as to why they believe that is likely – there is talk of more capacity pressure, and yet their output gap forecasts don’t change much from where we’ve been (on their reading) for the last couple of years. If there is any basis for their beliefs it seems to be little more than the repeated claim by the Governor and the Minister that it is “a great time to invest” in New Zealand. But firms didn’t think so over the last five years – even with unexpected population shocks – and surely the reason the Bank is cutting the OCR has quite a bit to do with deteriorating conditions and investment prospects here and abroad? In a country that has had almost no productivity growth for the last five years, and with an exchange rate not forecast to change much from here over the forecast period, and with a deteriorating global backdrop (their own words were “global economic activity continues to weaken”) it seems little more than wishful thinking to expect a resurgence in business investment.

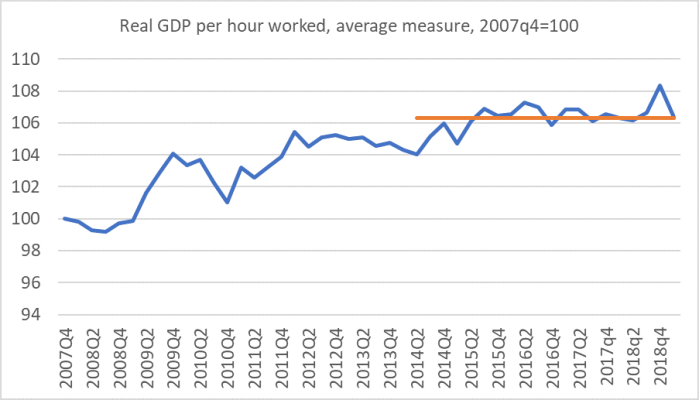

Ah yes, productivity, or the rather the lack of growth in it. Here is my chart, using the two official GDP measures and the two official hours measures.

The orange line in the average for the last five years. There is next to no aggregate productivity growth in New Zealand.

And yet somehow the Bank manages to conjure it up. They report a “trend labour productivity” growth variable, which they claim has grown steadily every year since 2012 (averaging perhaps 0.8 per cent per annum growth), and they forecast that productivity growth will continue – and even accelerate a bit – from here (averaging in excess of 1 per cent per annum growth). It hasn’t happened, and it seems most unlikely to start now – absent any big favourable change in policy or the big relative prices facing firms (eg the exchange rate). The investment opportunities – profitable ones – just don’t seem to be there. But I guess acknowledging that would upset the Governor’s spin about the “great condition” the country is in.

A wise person would then be very sceptical of the Bank’s projections that economic growth picks up from here. In fact, with net migration projected to continue to slow – and with it population growth – it is hard to see why GDP growth over the next year should get even as high as 2 per cent (even assuming the rest of the world doesn’t fall into a hole).

My final point relates to the prospects for policy if the outlook continues to deteriorate. I thought it was quite right for the Governor to note that when you are starting from here then, whatever your central forecast, it wouldn’t be too much of a surprise if the OCR were to need to be set at a negative rate at some stage in the next couple of years. Forecasting just isn’t any more precise than that.

That degree of openness is welcome. What is much less so is the Bank’s secrecy – and perhaps lack of straightforwardness/honesty – around possible options if the limits of conventional monetary policy are reached. As the ANZ pointed out in a note this morning, just three weeks ago the Reserve Bank responded to an OIA request about unconventional tools by (a) stonewalling, and (b) claiming that the work “is at a very early stage”. And yet yesterday, the Governor claimed they were “well-advanced” in their work. Both simply can’t be true (bearing in mind that the last two weeks will have been taken up with this MPS). Which is true I wonder? Who were they trying to deceive?

But again, perhaps worse than playing fast and loose were two things that should bother people more. The first is the way the Bank is keeping all this close to their chest. Responding to that OIA they refused to release anything (“very early stage” or whatever) on the grounds that to release anything would prejudice the “substantial economic interests of New Zealand” – one of those OIA grounds the Ombudsman simply doesn’t have the competence or confidence to challenge agencies on. Yesterday, we were told it all had to be kept very confidential to the Bank, because it was “market-sensitive”.

I’m with the ANZ economists who in a useful note this morning (worth reading, but I can’t see on the website to link to) observed

Let’s hope that a possible plan for unconventional monetary policy is shared publically soon, so that financial market participants and households can be confident of a smooth rollout of extra stimulus. And with the recent cut to 1%, and an even lower OCR widely expected, the clock is ticking.

This isn’t like the situation the Fed faced in late 2008, rushing to make policy on the fly in the middle of crisis, deploying things almost as soon as they were dreamed up. This is contingency planning. No one (I imagine) is wanting the Reserve Bank to tell us exactly what conditions would trigger the use of which instrument (the Bank themselves won’t know anyway, and things will be event-specific) but it is highly desirable that the work on options that the Bank and Treasury are doing should be socialised more broadly, so that (a) it can be challenged and scrutinised (officials have no monopoly on wisdom) and (b) as the ANZ says, to help reinforce confidence – including holding up inflation expectations – going into any serious downturn. The Governor tried to claim again yesterday that the Bank was highly transparent around monetary policy, but this is just another example of how they cling closely to anything of much value (as I’ve put it before, they are usually happy to tell us things they don’t know – eg three year ahead macro forecasts – but not what they do now, such as background analysis papers that feed into monetary policy, or detailed work on options if the nominal lower bound is reached).

Personally – and here I might part company from the ANZ – I remain very uneasy about the potential for unconventional instruments. The Governor has consistently talked up the possibilities, but he has never shared any research or analysis to give us confidence about what difference such tools would make to macro outcomes (have I mentioned that he has given no speeches about monetary policy?). As I’ve noted before just look at how slow the recoveries were in the countries that deployed these unconventional instruments – not issues of underlying productivity growth, but simply closing output and unemployment gaps – and you should be very sceptical too. That is why I keep hammering the point – in yesterday’s post again – that the Bank, the Treasury, and the Minister should be doing work on making the lower bound less binding, and taking the public and markets with them to prepare the ground. All indications are that they are doing nothing. If that is not so, it would be very helpful if they told us – it is, after all, official information and in this context the “substantial economic interests of New Zealand” are being jeopardised by them either not doing the work, or doing it and not telling us.

On which note, it is extraordinary that in an entire 52 page Monetary Policy Statement there is not a word about any of these issues and options. The Governor is right to highlight that we could soon face negative policy rates (as ANZ points, yesterday one of the government indexed bonds almost traded negative – real yield), but he is remiss not to be engaging the public, markets, MPs, and other affected parties (firms and households) on how best to think about handling such an eventuality. “Trust us, we know what we are doing” is a mentality that was supposed to be consigned to history decades ago, but bureaucrats – including ones with a poor track record of achievement – will hoard their little secrets and (it seems) ministers will cover for them. Grant Robertson promised that the reformed Reserve Bank would be more open and accountable. There is little sign of it so far.

Transparency does not matter.

As long as the cheap credit can get into the system and we can invest in fine art.

LikeLike

Regarding business investment this Government is fixated on forcing NZ businesses to invest in things that bring them no benefits. Little wonder enthusiasm and confidence is muted outside of scaffolding and road cone production and deployment.

LikeLike

The only reason we have the Bright Line Test, a 5 year Capital Gains Tax on investment properties is due very much to Alan Bollard as the RB governor at the time blaming his poor performance publicly on the National government not having a Capital Gains Tax.

LikeLiked by 1 person

Well let’s hope with this rates cut more currency can be used to boost asset portfolios.

LikeLike

Agreed, and investment in more property assets in particular. More house price inflation stimulated by aggressive interest rate cuts is just what the economy needs.

LikeLike

concur Matt

Plus massive govt surpluses. This move is a master stroke by orr. By increasing house price inflation and fine art prices it makes us all richer. With luck we will get 20% house price inflation again and our youngest and brightest can use the power of leverage to buy more assets.

LikeLike

Totally agree with your comments on stance of fiscal policy being misrepresented. The fiscal impulse is rough and ready but as you say it’s a workable enough indicator of fiscal stance, and it is currently neutral heading towards mildly contractionary. Spluttering to the contrary doesn’t change the facts.

There’s now a link up to that ANZ piece you quoted:

Click to access ANZ-Economic-Insight-20190808.pdf

LikeLike