The latest CPI data were released a couple of days ago. Perhaps the only real news was that nothing much seemed to have changed, here or abroad, in the last few months’ data.

Here is a chart of OECD core inflation rates

I’ve shown a few different indicators. Whichever you prefer there isn’t much sign of inflation picking up in the rest of the advanced economies.

Here is the Reserve Bank’s preferred core inflation measure.

If there has been some hint of inflation picking up a little, it remains as excruciatingly slow as ever. In a series with lots of persistence, the 2 per cent target midpoint seems a long way away. And although the Reserve Bank and some outside analysts like to suggest this is all about tradables inflation (a) the gap between the core tradables and non-tradables inflation at present is just around the historical average, and (b) tradables inflation, in New Zealand dollar terms, is at least in part an outcome of monetary policy (the exchange rate directly influences it).

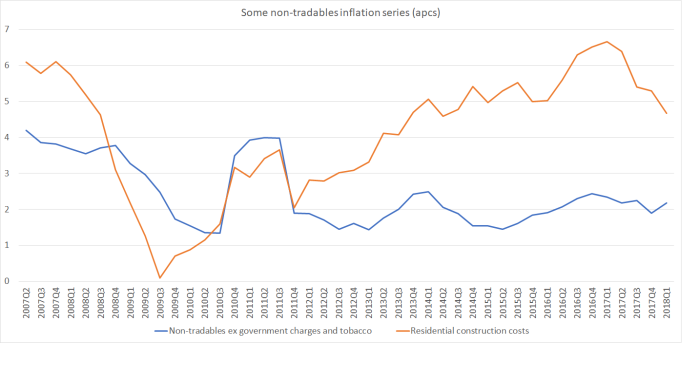

Here are a couple of non-tradables series I’ve shown before.

This measure of core non-tradables remains persisently below the rate (somewhere near 3 per cent) that would be consistent with overall core inflation remaining around the 2 per cent target. The extent to which construction cost inflation has been falling away again is now quite marked: it doesn’t just look like noise.

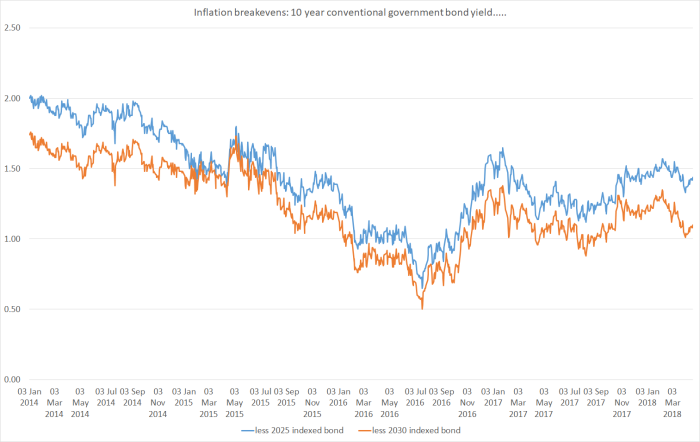

And what of market implied expectations of future inflation from the government bond market?

Nowhere near 2 per cent, and if anything a bit lower than they were three months ago when the last inflation numbers were released.

Nowhere near 2 per cent, and if anything a bit lower than they were three months ago when the last inflation numbers were released.

Pictures like these should be a challenge for the new Governor as he ponders his first OCR decision and associated communications. After all these years, there still isn’t much sign of (core) inflation getting back to 2 per cent, and there doesn’t seem much impetus from either domestic demand (for which construction cost inflation is often an important straw in the wind) or foreign inflation.

Some who have previously been “dovish” now point to higher oil prices as a reason – either directly, or just as a straw in the wind – why perhaps core inflation will finally pick up. Perhaps, but it is hardly been an infallible indicator historically. Others note that our exchange rate has fallen. That’s true too, but at present the TWI is about 2-3 per cent lower than the five-yearly average level (not much more than noise), and historically falling exchange rate have often been associated with falling non-tradables inflation (depending what drives the particular exchange rate move).

Time will tell, but in his RNZ interview the other day I heard the Governor praising the “courage” of central banks internationally for having held interest rates so low for so long, despite very strong growth, to help get the inflation rates back up to target. I wasn’t sure I recognised any element of the description – in the advanced world, central banks have mostly been reluctant to have interest rates low, and growth has rarely been particularly strong (both caveats seem to describe New Zealand). But perhaps the Governor needs to consider displaying some of courage he says he has admired and take steps to get New Zealand inflation securely back to target.

Am I the only one who thinks that low inflation is literally an impossible problem? If inflation is too low then just credit the treasury a few 100 million or whatever and ask them to spend it on whatever (as long as the money passes through non-finance entities at some point); if this doesn’t happen then it the only obvious conclusion is that whoever is in charge doesn’t think low inflation is actually a problem…

Apart from a small time delay from measurement to action inflation being too low is literally impossible.

LikeLike

You have to factor in Global consumer products production capacity and the visibility that the internet technology provides to prices of products available from around the world. Sites like Amazon and Alibaba give buyers access to the cheapest products available. Our retailers and manufacturers do not have any pricing power.

LikeLike

This is where brand loyalty and brand exclusiveness still command a premium price. I was looking at a pair of ladies plastic slip on shoes in QV just last week on my holiday in Melbourne in a store branded M Dreams in QV and they were retailing at AUS $85 a pair. Any other store like the Warehouse in Auckland and they retail at $15. Cost to produce likely $1.

LikeLike

Does the amount of money not influence the value of that money? Does the law of supply and demand not apply to money? Of course the velocity of the money is also an important factor, that is why QE didn’t impact inflation much.

Industry doesn’t affect inflation, only banks can do that.

LikeLike

You can pump the economy with more money as most of the large Central Banks have been doing but at the moment most of that increased money supply has either gone towards repaying debt or increasing the value of assets. It is the price of consumer products that affect inflation and it does require industry to have pricing power to create inflation. if we have production oversupply then prices are not likely to inflate.

LikeLike

Inflation is the product of the quantity of money and the velocity of money. Prices are the outcome, not the cause. Prices can deviate from market forces, creating localised disturbances in the general inflation rate, only over the short term.

QE didn’t cause much inflation because the velocity of all that new money was almost zero.

LikeLike

It could be done. Additional govt spending on real goods and services – unsterilised (ie printing money) is one of the more reliable ways to boost the economy and inflation when conventiona, monetary policy capacity is exhausted. But the political constraints tend to be quite significant – and the lags aren’t short either (one can issue cheques to everyone easily, but finding things to buy is a different challege).

LikeLike

My problem is I don’t bother myself with what is politically possible, I only think about what is actually possible.

The poorest quartile would have no trouble finding things to buy I reckon, getting money to them gives it the highest velocity.

LikeLike

It has always been there on the list of last resort instruments.

LikeLike

Finding cash to buy things do not create inflation. It is the supplier that creates inflation through pricing their products.

LikeLike

I think something is wrong with the model of inflation. We should have much higher inflation by now given supposedly low unemployment and low interest rates according to the models. They keep saying its going up – and it never does. Japan also this week I believe. Perhaps if interest rates were even lower inflation would pick up? Or perhaps it would do little (I certainly wouldn’t spend any more given a few dollars less a week on the mortgage interest). Now if the government lifted public sector wages and boosted our household income finally, or say school fees and prescription and medical charges were abolished (affecting our family a lot) well that might mean the odd night out at a family restaurant, a new freezer, a Winter holiday like we used to afford do back in the 2000s and weekend fun that actually involves money. Fiscal policy involves spending and spending can boost prices (though it might just raise output – which would be good). But here alas Robertson is running mini-austerity for ideological reasons.

LikeLike

Is the theory that increased demand increases prices? Make sense if supply is limited or restricted but with globalisation our economy is attached to the rest of the world so there is an almost infinite supply. Even a dramatic increase is NZ demand would barely affect the world’s supply and demand. So logically there will be more inflation in NZ unique items: a bach, rugby players income, lawyers wages but not for those items that arrive from overseas and frequently sold by recent immigrants (fast food, petrol stations, supermarkets, hardware stores).

Stopping low wage immigration (both residents and working visas) would cause wages to rise and inflation to increase. It would impact exports that are dependent on immigrants labour such as fruit picking.

Inflation would be bad for me now I’m living on savings but if it didn’t get out of hand maybe beneficial for an equitable NZ. And if I understand correctly it give the government more freedom to handle the impact in NZ of the next world wide recession.

LikeLike

There is nothing wrong with the model of inflation. It is just that economists do not understand what are the real price drivers.

LikeLike

Someone sent me this:

Time for a mature conversation about immigration

SHAMUBEEL EAQUB

https://www.stuff.co.nz/business/opinion-analysis/103232322/time-for-a-mature-conversation-about-immigration

It links to this

Click to access Shaping-a-Nation-1.pdf

I wonder how many of those high earners are in real estate services since the growth seems to be in “construction and services”. It comes across as advocacy (and I have as much faith in Scanlon as I do Paul Spoonley).

Then I found this:

https://www.macrobusiness.com.au/2018/04/stop-the-presses-australian-treasury-likes-mass-immigration/

LikeLike

The question is – Who do you believe

Australian Productivity Commission 2006

Australian Productivity Commission 2016

Shamubeel Eaqub

Leith van Onselen

Macrobusiness

Australian Treasury

Malcolm Turnbull

Scott Morrison

https://croakingcassandra.com/2018/04/14/population-size-and-gdp-per-capita-us-states/#comment-24001

One thing for certain is when the subject arises you will be swamped with a lot of warm words and squirt articles that attempt to influence with eloquence. Of course Shamubeel has to refer to Australian data because there is no NZ equivalent data or research

Correspondingly the NZ prattlers claim the AU bankers are crooks while the NZ Bankers are cleaner than clean White Knights

Who do you believe?

LikeLike

It takes a thief to catch a thief. It is unfair for media outlets to give oxygen to one side only.

LikeLike

My respect for Shamubeel Eaqub went out the window when in the start of a bull cycle in property around 2002 to 2005 he was ranting about how people should just rent instead of buying property. Then again recently with telling public media that Phil Twyford’s target of 100,000 properties in 10 years should be 500,000 properties in 10 years. I am not sure if he lives in NZ or he lives on Mars with that sort of wayout comments that makes zero common sense and has zero fundamentals.

LikeLike

Read “Why Theresa May is to blame for the Windrush scandal” by Brendan O’Neill (find via google) for a passionate article that ends with poll data evidence that wanting immigration to be controlled is totally different from disliking other ethnicities.

The leader of Wellington chamber of commerce was on the radio this morning saying INZ is making it difficult to recruit skilled staff. Either this means a sensible definition of ‘skilled’ is being used or else it is the same old bureaucracy gone mad that caused this Windrush scandal and 35 years ago made it very difficult for skilled IT staff to get their green cards so they could work in the USA while simultaneously sucking in great numbers of illiterate Hispanics into California for fruit picking and general exploitation.

Read the Eaqub article; some of the comments were examples of the mature conversation he is asking for. Now we need politicians who are brave enough to discuss the subject without resorting to sound-bites.

LikeLike