The latest CPI data were released a couple of days ago. Perhaps the only real news was that nothing much seemed to have changed, here or abroad, in the last few months’ data.

Here is a chart of OECD core inflation rates

I’ve shown a few different indicators. Whichever you prefer there isn’t much sign of inflation picking up in the rest of the advanced economies.

Here is the Reserve Bank’s preferred core inflation measure.

If there has been some hint of inflation picking up a little, it remains as excruciatingly slow as ever. In a series with lots of persistence, the 2 per cent target midpoint seems a long way away. And although the Reserve Bank and some outside analysts like to suggest this is all about tradables inflation (a) the gap between the core tradables and non-tradables inflation at present is just around the historical average, and (b) tradables inflation, in New Zealand dollar terms, is at least in part an outcome of monetary policy (the exchange rate directly influences it).

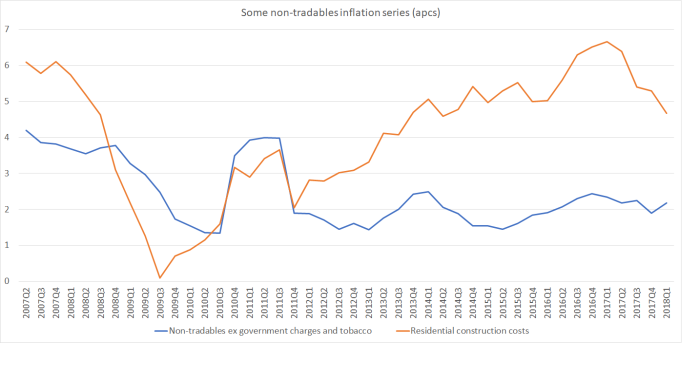

Here are a couple of non-tradables series I’ve shown before.

This measure of core non-tradables remains persisently below the rate (somewhere near 3 per cent) that would be consistent with overall core inflation remaining around the 2 per cent target. The extent to which construction cost inflation has been falling away again is now quite marked: it doesn’t just look like noise.

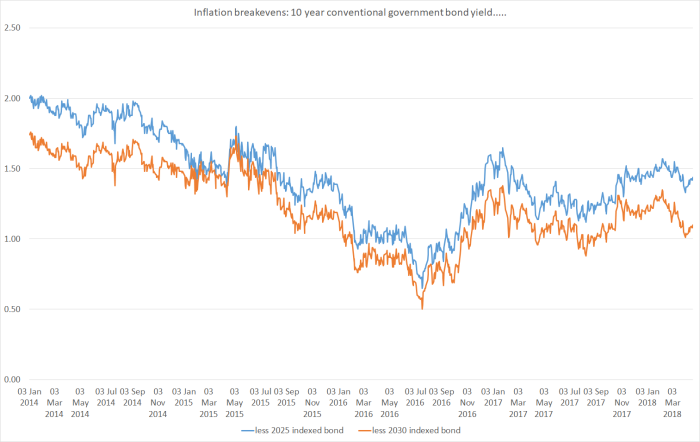

And what of market implied expectations of future inflation from the government bond market?

Nowhere near 2 per cent, and if anything a bit lower than they were three months ago when the last inflation numbers were released.

Nowhere near 2 per cent, and if anything a bit lower than they were three months ago when the last inflation numbers were released.

Pictures like these should be a challenge for the new Governor as he ponders his first OCR decision and associated communications. After all these years, there still isn’t much sign of (core) inflation getting back to 2 per cent, and there doesn’t seem much impetus from either domestic demand (for which construction cost inflation is often an important straw in the wind) or foreign inflation.

Some who have previously been “dovish” now point to higher oil prices as a reason – either directly, or just as a straw in the wind – why perhaps core inflation will finally pick up. Perhaps, but it is hardly been an infallible indicator historically. Others note that our exchange rate has fallen. That’s true too, but at present the TWI is about 2-3 per cent lower than the five-yearly average level (not much more than noise), and historically falling exchange rate have often been associated with falling non-tradables inflation (depending what drives the particular exchange rate move).

Time will tell, but in his RNZ interview the other day I heard the Governor praising the “courage” of central banks internationally for having held interest rates so low for so long, despite very strong growth, to help get the inflation rates back up to target. I wasn’t sure I recognised any element of the description – in the advanced world, central banks have mostly been reluctant to have interest rates low, and growth has rarely been particularly strong (both caveats seem to describe New Zealand). But perhaps the Governor needs to consider displaying some of courage he says he has admired and take steps to get New Zealand inflation securely back to target.