Brian Fallow’s weekly column in the Herald yesterday was fairly pointed.

Some further easing in the official cash rate seems likely, Reserve Bank governor Graeme Wheeler reiterated last week.

Well, good.

Because the case for more easing is compelling.

I agree with him. Whatever measure of inflation one uses – headline, exclusion measures, filtered measures – inflation has been persistently below where the Governor agreed to keep it, and shows no sign of rising (much or for long) any time soon. On the Reserve Bank’s own numbers, the output gap is still modestly negative, and the unemployment rate has risen and is above any sort of NAIRU estimate.

But that wasn’t my reason for writing. Instead, Brian notes a few considerations, including those mentioned in the Governor’s recent speech, that might hold the Governor back

Housing is the first. The Governor appears to have reversed himself, and gone back to thinking that (Auckland) house prices should be a factor in setting monetary policy. But the Minister of Finance mandated him to target the medium trend in consumer price inflation, and New Zealand’s measure of consumer price inflation does not – rightly in my view (and that of most others) – include existing house prices or land prices. House price inflation in Auckland is certainly scandalous, but the responsibility for that outcome is directly attributable to the choices of elected central and local governments. The Reserve Bank’s role should simply be – and in statute is – to ensure that banks are sufficiently resilient to cope if nominal house prices ever fall sharply.

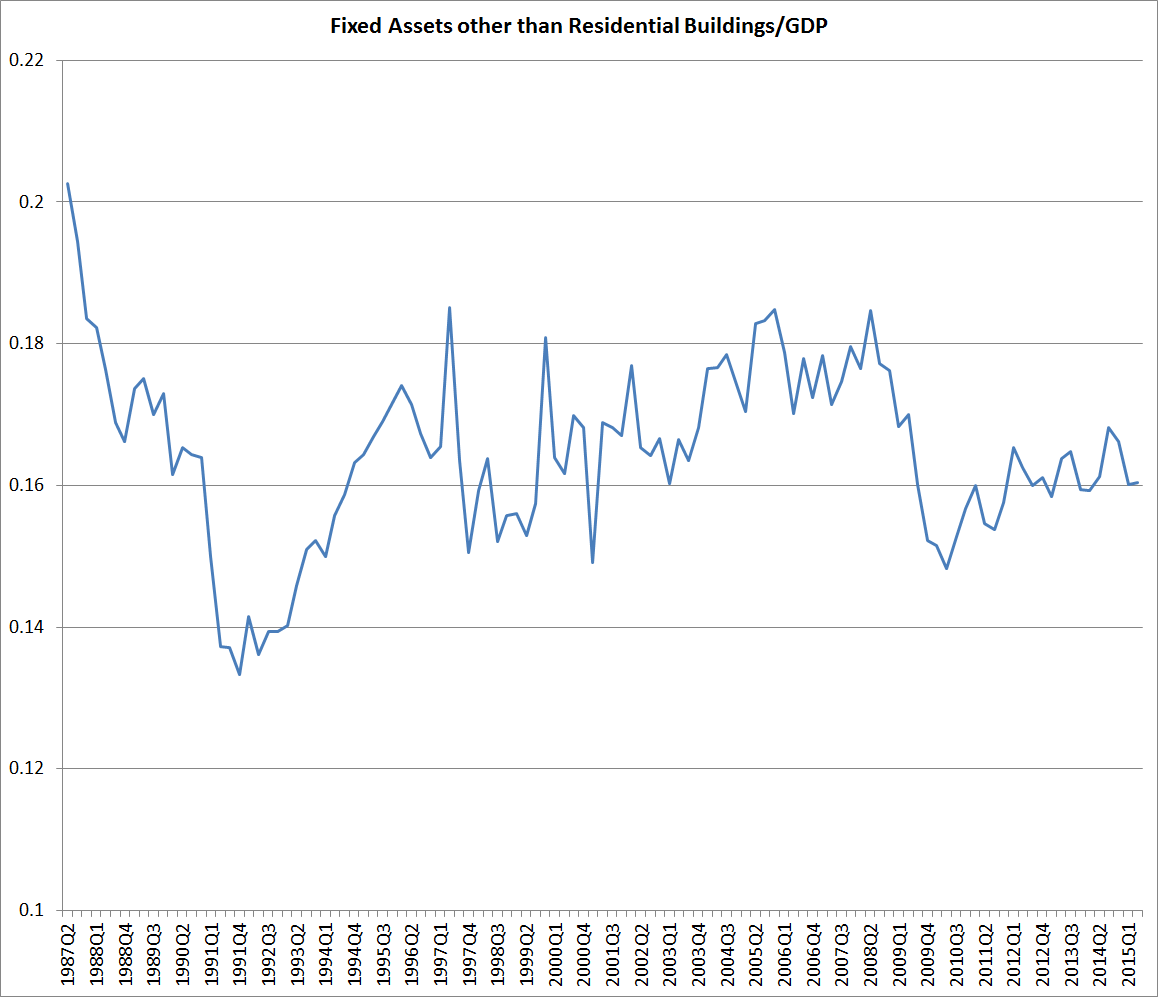

The second issue related to investment. The Governor had suggested that the Bank needed to ask “whether borrowing costs are constraining investment”. It isn’t clear why the Governor regards that as a relevant consideration – absent some wild investment excess (1987 perhaps?), more private sector investment is generally a good thing. Brian Fallow suggests that investment is sufficiently strong that there is no issue on that score anyway. I’m not sure I agree. Excluding residential investment, investment as a share of GDP remains pretty subdued. Historically, business investment as a share of GDP has been surprisingly low in New Zealand relative to that in other advanced countries, given our faster trend rate of population growth, and now investment is low even relative to that history. And that despite the rapid rate of population growth in the last couple of years.

Not that the government’s ambitious export growth target is any concern of the Reserve Bank’s, but it is difficult to see anything like the targeted transformation in export performance occurring with these sorts of investment rates. Of course, the big issue there is likely to be the real exchange rate – still sufficiently high that even the Governor seems to comment on it whenever he can.

I touched last week on how odd it is to think of holding back on cuts now to save ammunition in case things get really bad again. But Brian comes back to this issue by another angle.

But we can’t forget that New Zealand remains abjectly reliant on importing the savings of foreigners. The risk premium they demand to keep on doing that puts a floor under banks’ funding costs and the interest rates borrowers see, regardless of how low the OCR might go.

Here I think he is wrong. I’ve dealt previously with the question of whether foreign lenders typically demand a “risk premium” for lending to New Zealanders (in NZ dollars). The evidence strongly suggests that they don’t – and haven’t. But if they were particularly concerned about New Zealand risk, there are two ways to get compensated for that risk. The first would be to seek a higher interest rate. They couldn’t typically get it at the short end, since the Reserve Bank itself directly sets the OCR based on domestic conditions. They might perhaps get it on longer-dated assets (bonds), but expectations of the future OCR typically play the most important role in influencing the level of longer-term interest rates.

A much more plausible place to see any risk premium, in a floating exchange rate country, would be in the level of the exchange rate – in other words, a surprisingly weak exchange rate. Nervous foreign investors would be reluctant to buy NZD instruments at the interest rate set on those assets by domestic economic conditions. But they might be happier to do so if the exchange rate were lower. A lower exchange rate today, all else equal, means more prospect of some appreciation (and extra returns) in future. It is a bit like the share market – if concerns about a company, or the whole market rise, investors get compensation for the additional risk through a lower share price. The lower exchange rate, in turn, helps rebalance the economy and reduces, over time, perceptions of risk.

But in thirty years of a floating exchange rate, I can think of only a handful of occasions when New Zealand’s exchange rate has been surprisingly weak (relative to New Zealand cyclical fundamentals) – most obviously at the height of the global crisis in 2008/09. Global risk aversion was then at its height, and the NZD was caught in the backwash. It isn’t a remotely typical story, and there is no sign that it is relevant now. As the Governor keeps noting, the exchange rate is still rather high.

A materially lower OCR would lower domestic borrowing rates, which would provide a little support to lift investment. But even if it did nothing at all on the score, it would work by lowering the exchange rate, in turn boosting returns to actual and prospective exporters. Yes, it would increase the cost of domestic consumption a little, but the trade-off would be a stronger recovery, more resilient against any new wave of adverse shocks, lower unemployment, and – not at all incidentally – measures of medium-term inflation which would be rather nearer the rate the Minister of Finance asked the Governor to achieve.

The Reserve Bank apparently agonised for a while in 2008/09 about this idea that a too-low OCR might somehow create troubles with foreign investors. Given the pace of the fall in the exchange rate during the international crisis, and the novelty of such low interest rates, they were perhaps understandable questions then. But I doubt it is a factor that weighs much in the Governor’s deliberations now. We shouldn’t welcome foreign investor concerns or heightened perceptions of risk – they are a real cost – but if those concerns exist, we are likely to be much better off absorbing them in a depreciated exchange rate, than trying to lean against them with unnecessarily high interest rates. The alternative (‘lean against”) approach has usually been damaging, or disastrous, wherever it has been tried (think of all too many emerging market crises).

In the end, I think Brian agrees.

Even so, rather than keeping powder dry, the better way of mitigating the effects of another negative shock from the rest of the world might be for the bank to impart as much momentum as it can to the economy before the headwinds turn gale force.

It isn’t always and everywhere good advice, but given our continuing anaemic economic performance, it seems like very good advice right now, whether or not the headwinds ever gain further strength. The debate probably shouldn’t be around whether the OCR should be 2.75 or 2.5, but why it should not quickly be cut to something more like 1.75 per cent.

Wheeler is really at a loss.

He must decide if he is pro economic activity which means to lower interest rates. NZ Household cash deposits almost equate NZ Household debt which means raising interest rates or dropping interest rates do not affect the overall consumption spending of NZ Households.

Lower interest rates do stimulate businesses that are reliant on debt(eg the building industry which should be encouraged) and lowers the cost of government debt whoch encourages council and governmrnt infrastructure spending. NZ infrastructure spending is far too low and we need to update and upgrade.

It also lowers the NZD that allows our exporters to grow and earn a higher margin on their export sales currently struggling in pricing and the high NZD affects margins that affect farm investment.

Wheeler needs to get back to economics 101 taught in high school. When he and Spencer dabbled in taxation and called for a CGT. The government responded under RBNZ pressure with a 2 Year Bright line test. He has just worsened the situation because in effect he has introduced a 2 year distortion in that everyone who wanted to sell would now wait 2 years. What is that going to do to supply??

As long as banks do not go back to the bad old days of low documentation loans (2002 to 2007) bank stability is not at risk. With global interest rates so low, banks must be disciplined in their lending practices as they have access to too much low cost funds which they have to lend out in order to maintain a margin.

The highest risk that banks face is when interest rates turn up. Their lending practices become looser as interest rates rises.

LikeLike

In order to maintain Bank stability it is imperative that RBNZ maintains the LVR restrictions. If Wheeler has a concern about bank stability then he should continue to raise the equity requirements to 30% for the whole of NZ rather than just restricting it to Auckland.

LikeLike