There have been a couple of odd comments this week about the use of macroeconomic policy tools in New Zealand.

In his weekly column yesterday, Brian Fallow suggested that it had been unwise to have put so much emphasis on getting the budget back to balance, and that it was time for more fiscal stimulus. Of course, there is nothing sacrosanct about getting back to balance by any particular date, but if anything I thought our government had been rather too slow to get there. With the benefit of record – and probably unsustainable – terms of trade – there wasn’t really much excuse for having run deficits in the last few years. And a tighter stance of fiscal policy should, at the margin, have eased the upward pressure on demand, the OCR, and the exchange rate.

Fallow draws on the generalised advice of the IMF to advanced economies. But most of those advanced countries can’t do anything much with conventional monetary policy even if they wanted to. Quite a few advanced countries (including the euro area) already have negative policy interest rates, and many of the others – US, UK, and Japan among them – are essentially at zero. Perhaps new rounds of QE might make some difference – I rather doubt they could do much – but to all intents and purposes monetary policy options are exhausted. That is partly the fault of central banks and finance ministries that have done nothing material over eight years to remove the near-zero lower bound on nominal interest rates but, choice or not, it is the situation today.

If there is still excess capacity in many of those countries, and if many of them face widening output gaps if world activity growth continues to slow, the appeal of looking to fiscal policy for stimulus is understandable. In general, I’m not sure it is a call that should be heeded to any great extent, as most of the larger countries already have rather sick fiscal positions – made considerably worse when those countries resorted to fiscal stimulus, to loud cheering from the IMF, in 2008/09.

New Zealand – and some other advanced countries such as Sweden, Finland, Estonia, Australia, and Switzerland – is in the fortunate position of having a low level of public debt. That means we do have some room to use fiscal policy if such stimulus is required. But even that potential isn’t limitless. Faced with another severe recession, even allowing the automatic stabilisers to work would add materially to the government’s debt over several years. In such a downturn, it is probable that the government’s speculative investment vehicle – the New Zealand Superannuation Fund – would lose a lot of money. And for those who worry about the financial stability risks of the house prices more than I think warranted, bear in mind the potential need to bail out banks and their creditors. If there is a severe downturn, we need the political room to allow those buffers to work, not to have to resort to pro-cylical fiscal policy

Fallow – and many international commentators – have favoured additional government spending because interest rates are low. But remember that interest rates are low for a reason – it isn’t just some number thrown up by a random number generator. I’ve argued previously that the effective cost of capital the government should be using in deciding on even good quality projects is probably in excess of 10 per cent (the sort of standard private businesses use), not something close to the government bond rate. And all this is before the questions that must be asked about the poor quality of too much government spending.

There are distinct political limits to how much fiscal stimulus any government can do, even in a crisis. Why fritter away that potential now, when our OCR is still 2.75 per cent? New Zealand has far more monetary policy headroom still open to it than most other countries do. There are real macroeconomic issues in New Zealand – as Fallow points out, the high and rising unemployment rate suggests that the economy continues to run below capacity – but as Eric Crampton noted in his response to Fallow yesterday, it is not as if monetary policy has been tried and failed. Rather, because of the repeated mistaken calls by the Reserve Bank, monetary policy has barely been tried.

ANZ advocated fiscal stimulus back in July. I set out here the reasons why I thought that was the wrong call. I don’t think I’d resile today from anything in that piece.

But the other odd comment on New Zealand macroeconomic policy came from someone who really should have known better. In his speech on Wednesday, the Governor of the Reserve Bank

It is important also to consider whether borrowing costs are constraining investment, and the need to have sufficient capacity to cut interest rates if the global economy slows significantly.

I’ll largely ignore the first part of the sentence (although if inflation is low and unemployment still high, isn’t more private sector investment generally likely to be a good thing?). It was the second half of the sentence that really reads oddly – and arguably, worse than oddly.

This idea of keeping some powder dry in case there is a renewed sharp slowdown pops up from time to time in international commentary. We’ve even seen the argument made that the Federal Reserve should raise interest rates now so that it has room to cut them if there is a future slowdown. But it is a deeply flawed argument. It may have some merit on the fiscal side – higher public debt now leaves less room to run up more debt later on – but in respect of monetary policy it is just wrong.

Monetary policy that is tighter than strictly necessary (in terms of the PTA) now, is likely to both weaken the economy (relative to the counterfactual) over the coming 12-18 months, and further low inflation and inflation expectations. Lower inflation is undesirable (in terms of the PTA itself) and low inflation expectations are deeply problematic. Lower inflation expectations, all else equal, raise real interest rates for any given nominal interest rate. The experience of advanced world since 2007 says that one of the biggest macro management problems of a sharp slowdown in the presence of low inflation is getting real interest rates low enough. It was easy to get real interest rates materially negative in the high inflation 1980s but it is almost impossible to do so now. In other words, holding up nominal interest rates now increases, perhaps materially, how much one might need to cut rates if a severe downturn happens, while doing nothing to create that extra space.

The Governor has rather reluctantly come to acknowledge that global deflationary risks. The last thing anyone in his position should be doing right now is making choices that would make it harder to handle the next sharp slowdown. But that is what he appears to be set to do.

If anything, those countries that still have monetary policy room to move should be doing so now. Real interest rates should be as low as possible, consistent with the PTA – and perhaps especially in a country that starts with the highest real interest rates in the advanced world. Rather than core inflation of 1.5 per cent or less, the Governor should be rather more comfortable with core inflation around 2.5 per cent. The best way to get that sort of outcome would be to have cut the OCR over the last couple of years, not raised it.

As a commenter here the other day put it, this idea that we should hold the OCR up now so that it can be cut later “is like keeping your shoe laces tied so tightly that it cuts off your circulation, just so it feels good to loosen your laces later.”

Between the failure to do anything about the zero lower bound – which the Governor now (belatedly) implicitly acknowledges to be an issue – or, absent that, to consider a higher inflation target, the Governor and the Minister have left New Zealand less well placed than it could have been if there is a new sharp global slowdown in the next few years. But the decisions that keep on delivering such unnecessarily low rates of core inflation (and high unemployment) are those of the Governor alone.

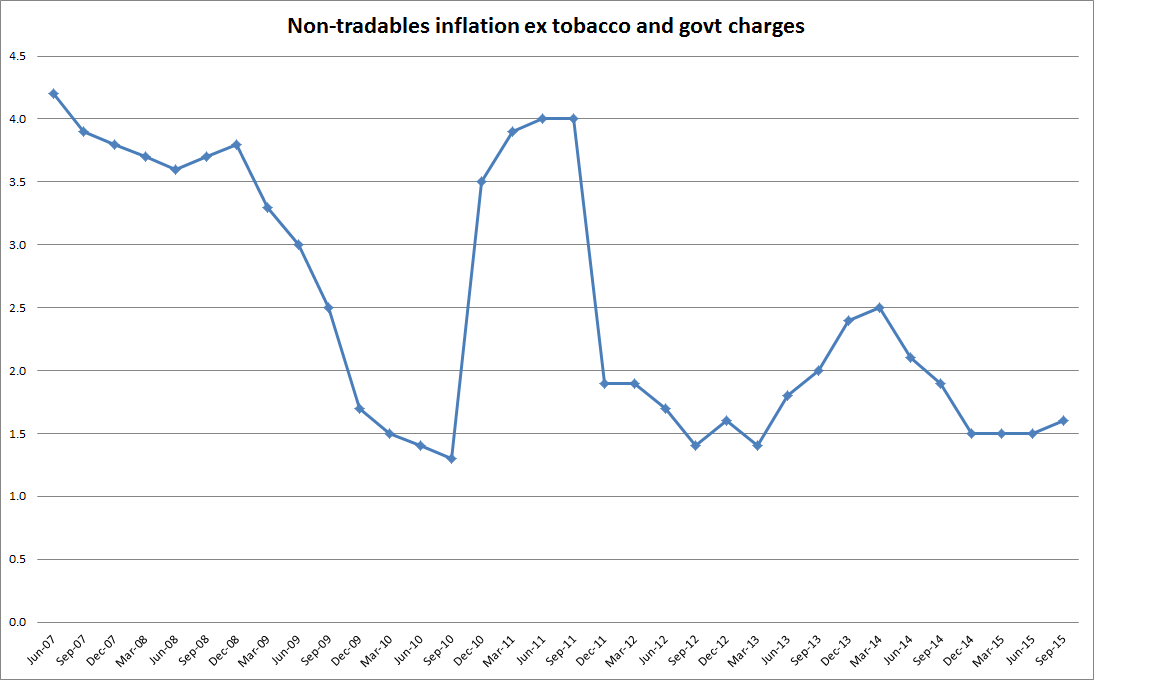

Plenty of market economists have commented on yesterday’s inflation numbers. My only contribution is a simple chart of a new series Statistics New Zealand has just started publishing.

Non-tradables inflation has long been the focus for analysis of the underlying inflation position. Tradables inflation is thrown around by short-term swings in international oil prices and level shifts in the exchange rate, and non-tradables inflation should provide a better guide to underlying inflationary pressures. But non-tradables inflation is made harder to read because of repeated tax increases (notably tobacco taxes) and changes in government charges – which don’t reflect anything about the state of the domestic economy. It is quite common internationally for statistical agencies to publish series excluding taxes and government charges. And now SNZ has provided us with this series for New Zealand. It has the advantage, over the Bank’s sectoral core factor model measure, that it is not prone to revisions.

Note that this measure of non-tradables inflation is running at only 1.6 per cent, barely above recessionary low. Non-tradables inflation should be expected to run above tradables inflation on average over time (there is typically more scope for productivity gains in tradables than in many non-tradables). Indeed, if CPI inflation was going to average around 2 per cent – the Bank’s target – non-tradables inflation shoiuld probably average somewhere in the 2.5-3 per cent range (and perhaps tradables might be in the 1-1.5 per cent range). Non-tradables inflation is extremely low in New Zealand – it is too low and should, as a matter of active policy, be raised.

No doubt the Governor and his economists will say that that is what they have been trying to do. But if so, they have repeatedly failed. Becoming reluctant to cut the OCR further because of the housing market (one of the channels through which lower interest rates work – a buoyant housing market is a desired feature not a bug) or for fear of hitting zero in a global downturn is a recipe for continuing the mistakes of the last few years.

To repeat Eric Crampton’s line: monetary policy has scarcely been tried. It should be.