Watching last night’s party leaders’ debate had its entertaining moments, but mostly if it was clarifying it was so in a pretty depressing way. And one of these two will be Prime Minister for the next three years.

There was the sight of both party leaders falling over themselves to disavow any notion that house prices should fall. Apparently, a $1 million average house price (or the less headline-grabbing but still obscene median price of $800000+) in Auckland is just fine. I suppose we should be grateful that on the one hand the National Party has moved on from the nauseating talk of how these house prices were a “sign of success” or a “quality problem”, and on the other hand that Labour’s housing spokesman will openly talk of an aspiration to having house prices averaging perhaps 3 to 4 times income. Perhaps both party leaders really would prefer that Auckland house prices hadn’t increased very substantially in the last five years, but now they both seem content to simply treat it as a bygone – as if we should simply live with $1 million house prices indefinitely until, some decades hence, a combination of inflation (mostly) and real income growth, might render home-owning in our largest city once again affordable to new entrants.

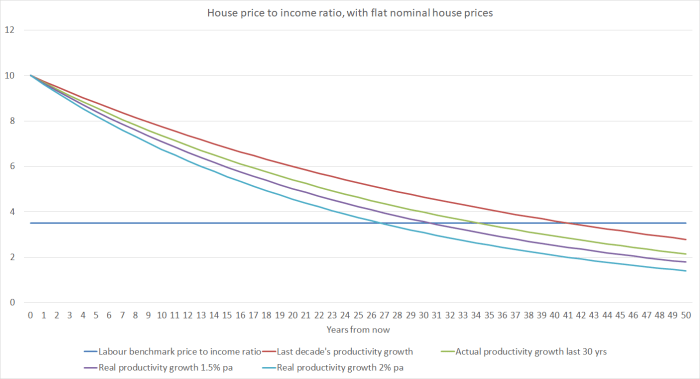

A couple of weeks ago I showed this chart. Starting from a price to income ratio of 10 – roughly that in Auckland now – it traces out how house price to income ratios would evolve if nominal house prices were unchanged from here on (something both party leaders now appear regard as a good outcome).

Just focus on the green line. If we have inflation averaging two per cent, and productivity growth matching the performance of the last 30 years (quite a step up from where we are now) it would take almost 25 years to get price to income ratios down to even around five times income. The Prime Minister talked of this being an issue for his kids. The solution, to the extent there is one, seems to be aimed at his grandchildren.

Ardern seemed to try to have it both ways with the talk of “we just need to build more affordable houses”. Lay members of my household responded “well, wouldn’t building more houses lower prices, which she just said she didn’t want?”. Actually, it is unlikely to make very much difference, unless she is serious about freeing up land supply. Without that, the overall affordability of the housing stock won’t change much, and any new houses built by or for the state will largely displace others that would have been built by the private sector. And yet, although on paper Labour’s policy on improving land supply looks promising, the current Leader of the Opposition continues in path trod by her predecessor and simply never mentions the land issue – even though everyone recognises that in Auckland in particular, the price of land is the largest component of a house+land. Relative to that, further extending capital gains taxes is just a third order distraction. At any plausible rate – in today’s low interest rate environment – so is a land tax.

Sadly, I suspect there is an element of dishonesty about both party leaders’ responses. If their housing policies really worked, I can’t imagine that either one would have a problem if house prices fell by, say, 20 per cent all else equal. That alone would lower price to income ratios in Auckland to eight times. It seems unlikely that that sort of fall would put anyone much in severe financial difficulty – not that many people recently have been able to borrow at LVRs over 80 per cent anyway, and servicing capacity mostly depends on continued employment. Continuing to talk of stable nominal house prices perhaps avoids (a) scaring the many people whose equity would be wiped out if house prices fell by 50 per cent, and (b) leaving themselves open to scare stories about how falling houses inevitably mean terrible economic times. But it also makes a hard to develop a constituency for the sort of changes that might, in time, make a real difference, and enable this generation of young people – ordinary working families – to afford a decent home.

If that was bad enough, Jacinda Ardern’s superannuation pledge was worse. John Key’s pledge to resign rather than increase the NZS eligibility age was cynical – he was quite open to Treasury that the age would rise, just not under his watch – but perhaps almost understandable in the context of the 2008 campaign. Helen Clark would have run the “secret agenda to raise the age” line, at a time when Labour itself had no intention of raising the age, and had established the NZSF to buttress the political messaging. But in this election, the incumbent Prime Minister leads a party which intends to legislate to increase the NZS age – by a little, and some decades down the track. It could hardly attack Labour for leaving open the possibility. Even if Labour didn’t want to increase the NZS age itself now, what would have been wrong with a simple pledge that “no, we don’t see a need to raise the NZS age at present. I don’t envisage it happening, but if at some point that judgement changes, I pledge that we won’t change the age without taking it to the public first as an election campaign promise”?

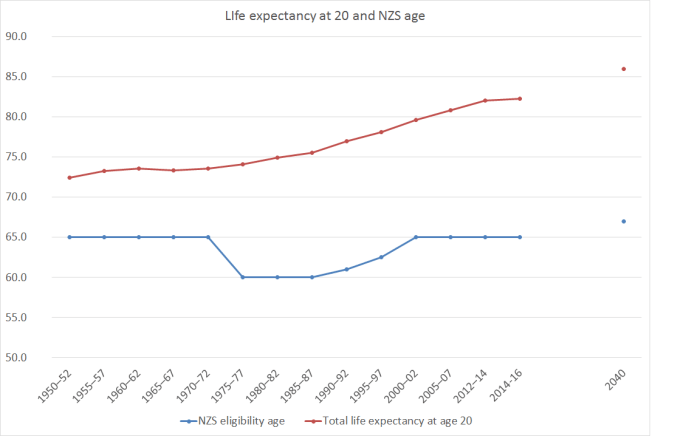

When the Prime Minister announced his NZS policy back in March, I ran this chart

Here is a chart showing life expectancy at 20, and the NZS eligibility age. The final two dots are what might have happened by 2040 if the life expectancy gains continue at the same rate as since 1950, and the NZS eligibility age if yesterday’s National Party policy proposal comes to pass.

Over that full period, 90 years, the NZS eligibility age would have risen by two years, and adult life expectancy (those getting to 20) would have increased by about 13.5 years. By 2040 it will be amost 40 years since the NZS age got back to 65. In that time, adult life expectancy is likely to have risen by 5 to 6 years, and yet the NZS age will have risen only by two years, if the new National Party policy is implemented.

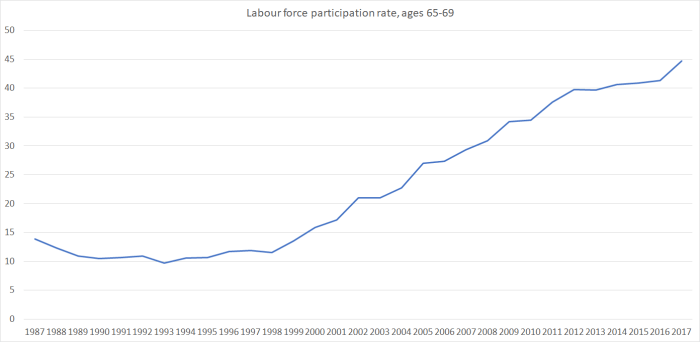

How has a New Zealand politics got so febrile that parties that claim they want to use scarce fiscal resources to solve child poverty are reduced to this? We can be pretty sure Bill English won’t be Prime Minister in 2037, so the NZS age won’t actually increase on his watch – he’ll just foreshadow change decades down the track – so in effect both candidates to be Prime Minister are refusing to increase the age while they are PM. Old people vote of course, but this isn’t an issue about today’s old people – it is about today’s middle-aged and younger people. Even among today’s older people, almost half of those aged 65 to 69 are still in the labour force.

Personally, I support a modest universal age-pension, but not one that cuts in at an age when a huge proportion of the recipients are still working, and are physically capable of doing so. And how come we can scarcely even have that political debate even though all manner of other advanced countries have been willing to take steps to increase the eligibility age? In Australia, for example, the age pension eligibility age will be 67 by 2024 – and technically, all those Australians, and (a more plausible possibility) the New Zealanders living in Australia, would be eligible to relocate to New Zealand and claim our NZS, with no prior residence requirement, at age 65.

I found the “debate” around child poverty almost as depressing. Neither party is actually willing to campaign for lower house prices – even though housing costs have been a big factor in the material and financial challenges some face. And all the talk was of how much money (other people’s money) the government could throw at the problem, with no mention at all of the possibility that improved economic performance might be the best way to lift living standards for everyone. But then neither party seems to have a serious idea as to how to lift our economic performance – or even to care much about doing so (the Prime Minister just makes up stuff about the current performance of the economy). And the Prime Minister was very keen to talk up how he, lots of data, and some public servants, are going to solve all manner of social problems. Which, on the one hand, displays a touching faith in the capability of politicians and bureaucrats – usually shared only by politicians and bureaucrats, and with little in past experience to support it – and on the other simply refuses to address the likelihood that cultural factors are part of the story in dysfunction and deprivation. I don’t really expect it from today’s Labour Party, but the Prime Minister is a self-described social conservative.

And then there was the wages debate. On that one, I reckon the Prime Minister is right on the facts – real wages have been rising, and faster than productivity has – and I was disappointed to see the Leader of the Opposition still running here “its how people feel that matters”. It might be uncomfortable to face it but wage inflation running ahead of productivity (and even than terms of trade gains) is one of the symptoms of an overvalued real exchange rate. Plenty of observers – including the outgoing Governor – have highlighted that as a serious challenge for New Zealand. It is part of the reason why Treasury forecast that exports will be shrinking as a share of GDP on current policies. (If this whole point is obscure, it is partly a teaser for a forthcoming post.)

UPDATE: On further reflection I’ve deleted the final paragraph. I wrote it based on reading various commentaries, but before digging into the numbers myself (a salutary lesson that I shouldn’t need). Understanding better both the Labour numbers and the National claims, I’d now take a more nuanced stance.

And, of course, there was the $11 billion fiscal hole that wasn’t. Perhaps the National Party really believed their story when they put it out yesterday morning. By debate time, it was pretty clear to anyone without an axe to grind that there was little or nothing there. Wouldn’t an honourable Prime Minister have simply quietly let the issue slide, and addressed the real challenges New Zealand faces, including real and legitimate questions about his own government’s performance over nine years, and about the aspirations and specific proposals the Labour Party is now outlining.

They would be okay for the next few years, but once you get even 10 years out from here, there would need to be a lot of other expenditure cut to keep spending to around 30 per cent of GDP, even if (a) the two parties resume NZSF contributions soon, and (b) investment returns proved to be pretty good. I’m genuinely puzzled how they propose to square that circle.

They would be okay for the next few years, but once you get even 10 years out from here, there would need to be a lot of other expenditure cut to keep spending to around 30 per cent of GDP, even if (a) the two parties resume NZSF contributions soon, and (b) investment returns proved to be pretty good. I’m genuinely puzzled how they propose to square that circle.