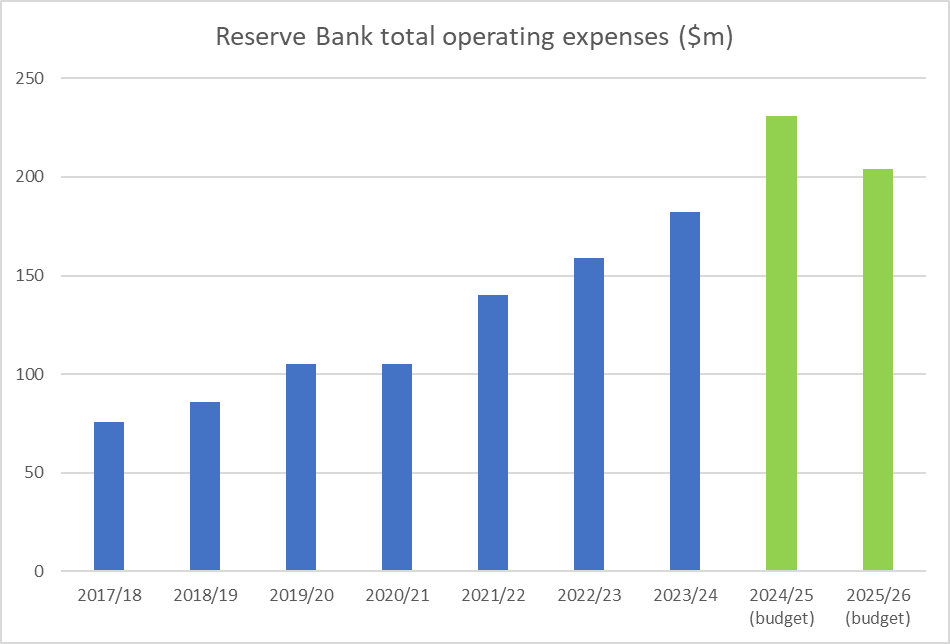

One of the mysteries of the months leading up to (what appears now to have been) Orr’s ousting as Governor, was how the Minister of Finance – apparently very focused last year on spending restraint in central government agencies, especially ones that weren’t really public facing – had let Orr and Quigley (and the rest of the Board) away with 2024/25 operating expenses so far in excess (23 per cent in excess) of the level of spending for that year allowed under the amended Funding Agreement Grant Robertson had signed off shortly before the 2023 election.

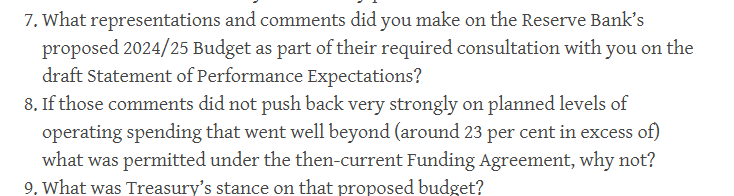

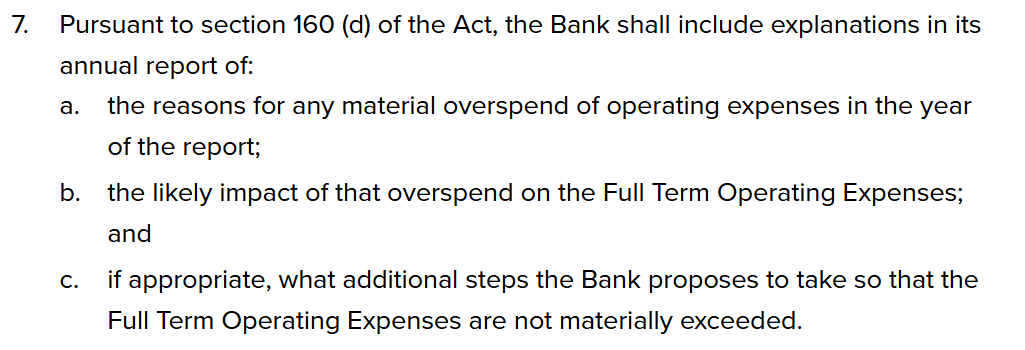

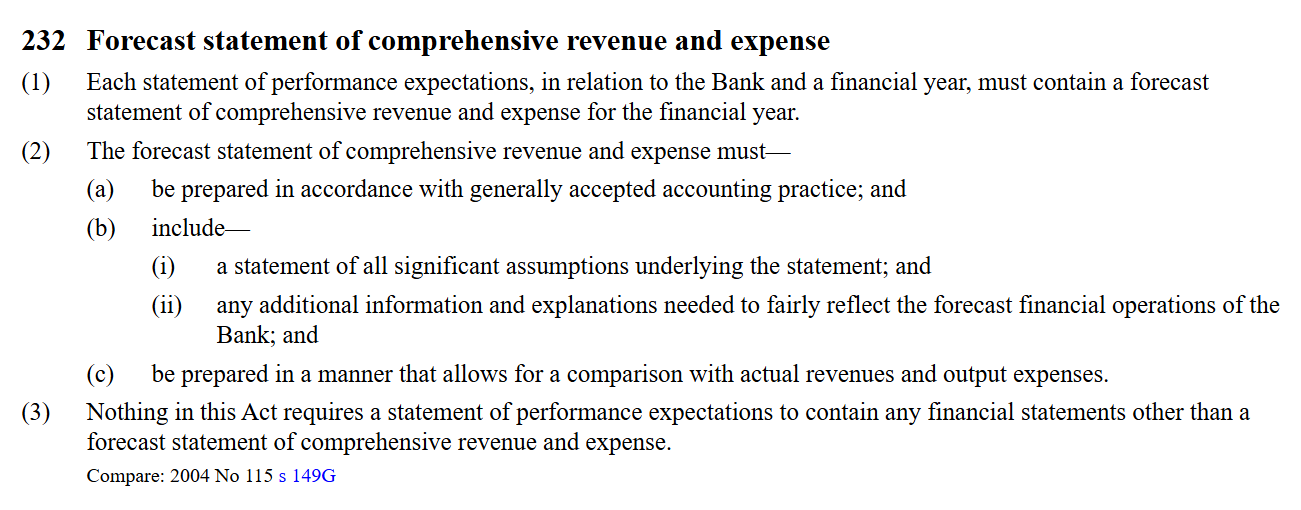

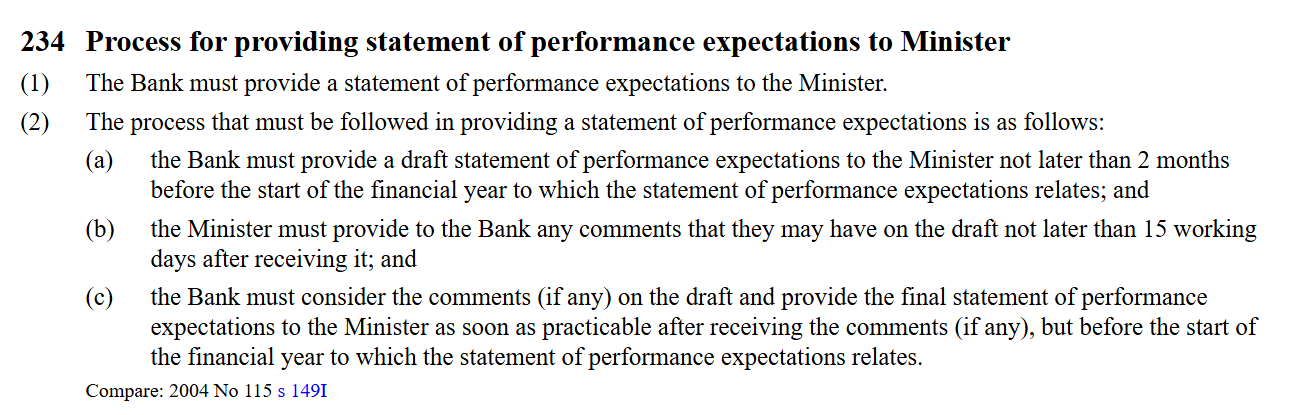

The Minister can’t directly control the Bank’s annual budget but the law requires the Bank to produce a Statement of Performance Expectations each year, to be published before the start of each financial year. The Act sets out what has to be included in a Statement of Performance Expectations (SPE)

The Act specifically provides for the Minister of Finance to be provided with the opportunity to comment on a draft of that SPE, and explicitly provides 15 working days for her to provide comments (drawing, no doubt, on advice from The Treasury which, again under the Act, has been made formally the Minister’s monitor of the Reserve Bank). The Minister also has the power of the bully pulpit: she could openly call out excess, if she knew about it.

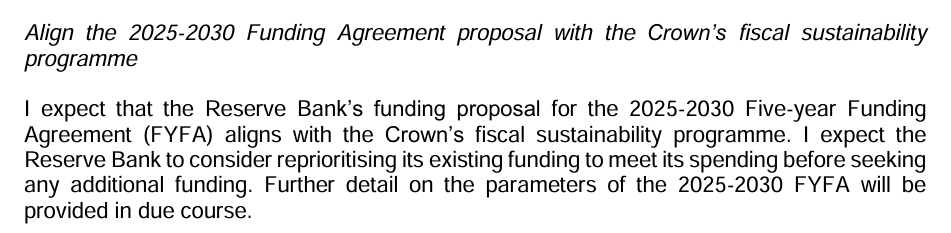

In a post a couple of weeks ago I revealed that neither the Minister nor the Treasury had raised any concerns about Orr and the Board proposing to run levels of spending miles in excess of allowed levels, at a time when pretty much every other central government agency was facing actual cuts, and when the Minister had already (in early April 2024) reminded the Bank of her “fiscal sustainability programme” in her letter of expectation, in the context of approaching negotiations over a future Funding Agreement.

And when she mentioned reprioritising “before seeking any additional funding” you’d have to suppose that the benchmark against which “additional” would be understood by her was the level of funding her predecessor had approved only eight months earlier.

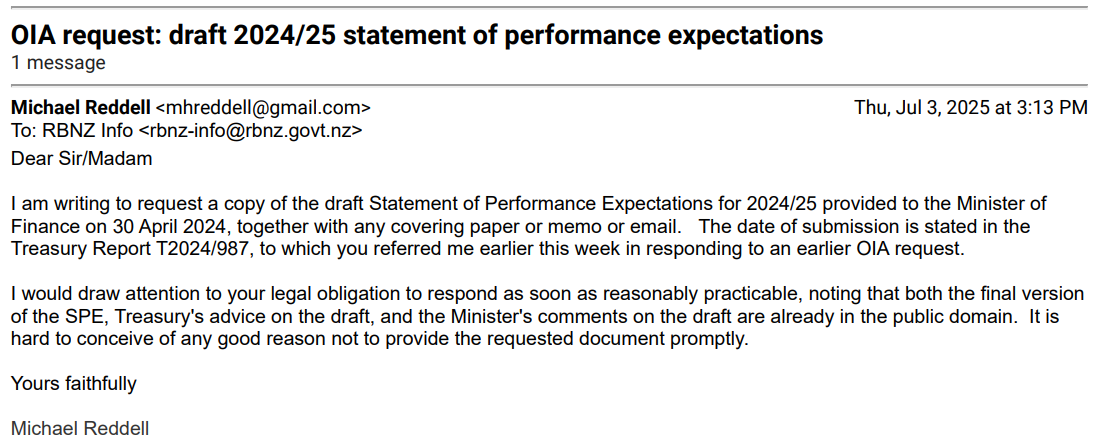

It seemed pretty surprising, to put it politely, that neither the Minister nor Treasury had raised any concerns when they were offered the opportunity to comment on the draft SPE. But I’d realised that although I had their comments, I didn’t have the draft they were reacting (or not) to. So on 3 July I asked for that and it turned up this morning, in full and unredacted (so should presumably have been supplied weeks ago).

And it turns out that the answer to my question as to why neither the Minister nor The Treasury had raised any concerns about the planned spending levels is that….the Bank just didn’t tell them.

You might find that surprising. I certainly did. You might wonder if I have misread something. But here is chapter and verse from the short covering memo to the Minister of Finance, dated 30 April 2024, and signed out by Simone Robbers, at the time one of Orr’s many deputy chief executives (formally, Assistant Governor, Strategy, Engagement and Sustainability).

It isn’t clear what about the “current operating environment” meant they thought they shouldn’t tell the Minister how much they were planning to spend. But whatever their reason, they didn’t. She didn’t know.

My view of the Minister of Finance has been revised up quite a bit in recent days, and this discovery is one of the reasons.

If you were being uncharitable you might think that the Minister should have asked, or the political advisers in her office should have asked, or – when it was sent on to them – The Treasury should have asked. And perhaps they should. But in the Minister’s case it was her first year in office, she had sent that Letter of Expectation just a few weeks previously, and she’d have had absolutely no prior reason to suspect that the Bank was going to adopt a budget with operating spending levels so far in excess of the elevated levels for 2024/25 Grant Robertson had approved the previous year. Who would? After all, this was Mr “cool your jets” Orr himself, who talked of fiscal restraint assisting in getting inflation down.

Perhaps The Treasury is more culpable, but I expect that the people reviewing the draft Statement of Performance Expectations were by nature more focused on the structures of documents and getting the Bank to jump through the right bureaucratic hoops. They won’t have been fiscal focused, and again….why would they suspect the Bank would just decide to blow out spending way beyond approved levels?

In bureaucrat land, “no surprises” is a big thing. But the Bank (Orr and Quigley) seem to have consciously chosen to run a great big surprise for the Minister of Finance. Perhaps the budgets were not quite locked down on 30 April (probably they weren’t) but if they’d been planning to stay within Funding Agreement limits it would have been easy enough to have included a brief mention that the forecast statement of comprehensive revenue and expense would include in-scope spending at levels consistent with the Funding Agreement allowance for 2024/25. Or, if they really thought they somehow had authority to spend so far beyond, they could at least have given the Minister an indicative range, and explained how it related to the (then) Funding Agreement limits. Instead, they seem to have told her nothing.

It is really quite extraordinary.

And one is left wondering when the Minister finally realised she’d been had. Perhaps it wasn’t until Treasury, many months later, got inside the Bank’s opening bid for the 2025-30 Funding Agreement, ran the numbers and realised that while the Bank purported to be offering up modest cuts, in fact they were from a level far above what had been allowed in the previous Funding Agreement; an inflated, bloated, baseline of their extravagant creation.

(It is always possible there is some other advice somewhere in which all this was pointed out early to the Minister, but if such advice exists the Bank has had every reason to helpfully – to them – disclose it. For the moment, it seems very unlikely that they were straightforward with her.)

And if the ousting of Orr has been accomplished, the board chair Neil Quigley remains in office. It wasn’t his signature on that 30 April advice to the Minister, but it was his Board that approved both the egregious 24/25 budget and the equally egregious 2025-30 Funding Agreement bid. Useful as he may have been to the Minister in late February and early March, there is no way he should still be in office.

The Bank purports to pride itself on integrity

But there has been little or none on display through any of this.

(By way of curiosity: I don’t usually pay much attention to which countries my readers come from, but I have noticed in the last few days quite an upsurge – from a vanishingly small base – in views from the Cook Islands. Perhaps some Wellington public servants need to find some lighter reading for their winter holidays, or is the former Governor now a quiet reader? Who knows.)

In the last day or so I’ve seen or heard two sets of comments from the Minister of Finance on the Orr/Quigley/Reserve Bank/Treasury/Willis – and it is now about all of them – business.

The first, that I want to deal with only briefly, was in The Post this morning under the heading “Willis dismay with RBNZ” (online here).

The journalist was obviously a bit of an Orr fan, as this article is the second time in two days The Post has talked of Orr’s “reputation for being charming”. No doubt he could and did turn it on when he chose, but not, surely, ever to anyone who ever challenged or disagreed with him (that included – very evidently – Nicola Willis when on occasion as Opposition finance spokesperson she asked Orr a slightly uncomfortable question at FEC hearings).

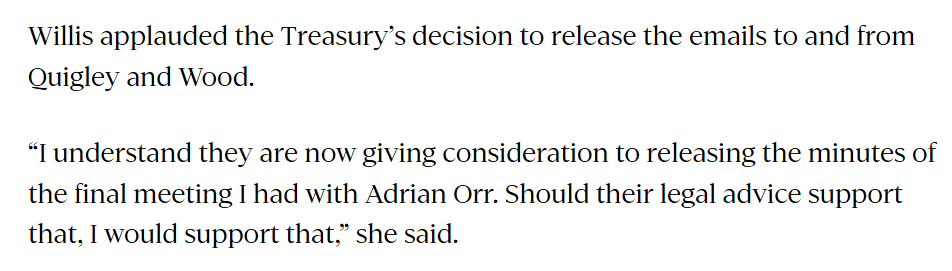

Much of what is in the article was also covered in my post yesterday. So I wanted to mention only this snippet

I guess she’d have looked a bit silly to have objected, but it is good to see her explicitly welcoming that Treasury release. On the second bit of that extract, it refers to the meeting on 24 February involving Quigley, Orr, Hawkesby, and senior Treasury people as well as the Minister herself. It is good to know that Treasury is considering releasing the minute of the meeting given that my request for it was lodged with them more than a month ago (as part of a larger request on Funding Agreement issues) but I presume there have been other requests, including since Tuesday when I reported the claim by my source that Quigley had been apoplectic and had complained to Treasury when he’d learned that such a minute existed. Again, it is good to know the Minister thinks Treasury should comply with the law, and we will look forward to the release.

The Minister’s more substantive comments were in an interview yesterday afternoon with Heather du Plessis-Allan. The audio is here and my transcript is here

Why do I bother doing the transcript? Partly for future reference and partly as a way of focusing my mind on all the lines Willis used in answering (and avoiding answering) questions. There were things I hadn’t really noticed when I listened live.

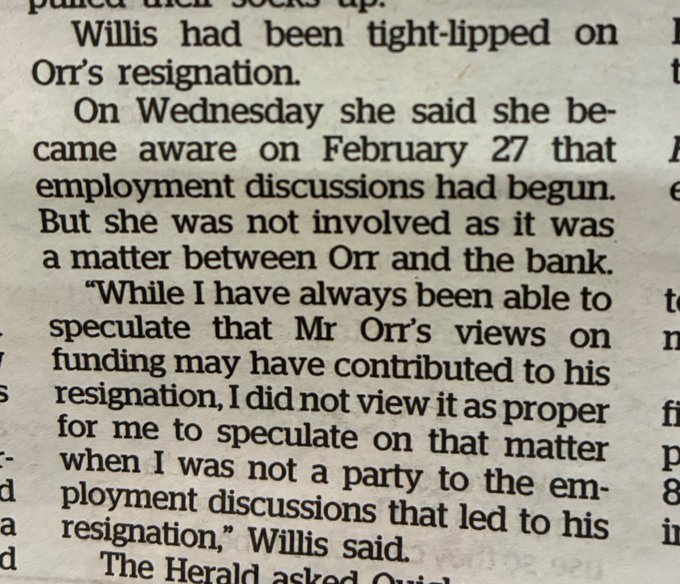

What do we learn from the interview? First that “emotions were running high” (the no doubt carefully chosen phrase for something like Adrian Orr losing his cool again) in the 24 February meeting she attended (although apparently there was no swearing) and she’d “heard reports” of the 20 February meeting between the Bank and Treasury where again “emotions ran high”. About, of all things, the Funding Agreement…..as if almost every single agency in Wellington hadn’t already been facing budget cuts (and it presumably wasn’t as if anyone was proposing cutting out the role of Governor).

Recall that Quigley email to Treasury (reproduced in yesterday’s post). The Governor was so ill-disciplined and out of control that in response to what Quigley recognised was a perfectly reasonable question from a mid-level Treasury official, Orr lost it, and then wouldn’t apologise, either immediately or after the meeting (instead Quigley was left to go and make his own apologies for Adrian). And sufficiently out of control, and unresponsive to what must have been feedback from his own chair, that the “losing his cool”, “emotions running high” behaviour was on display again several days later to a meeting with the Minister himself. In a normal employee such behaviour, especially repeated and without prompt and full apology, might of itself almost have been grounds for dismissal. (Humans make mistakes, even public sector chief executives, sometimes provoked, sometimes not. But when made aware you apologise, ensure it won’t happen again, or….you really aren’t fit to lead people and public organisations.)

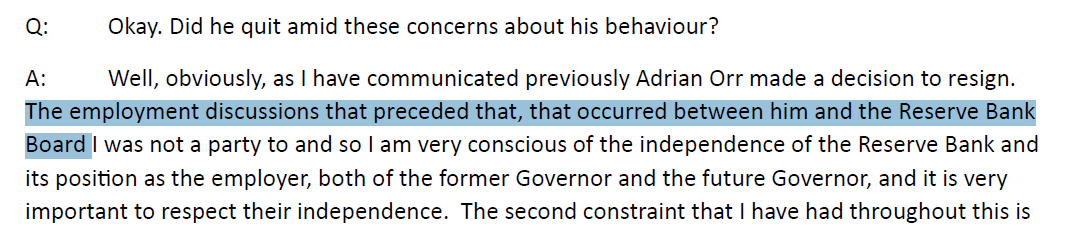

Willis was again at pains to suggest that the employment of the Governor was nothing to do with her, but purely something for the Reserve Bank Board. As a matter of law it simply isn’t so (I ran through the relevant provisions a couple of days ago), and the fact that it isn’t so has nothing to do – contrary to the Minister’s claim – with the “independence” of the Reserve Bank. There are plenty of roles and powers for the Minister of Finance in the Reserve Bank Act (as well as appointing and dismissing and receiving resignations from the Governor). For example, the Reserve Bank has what is known as “operational autonomy” on monetary policy, but they work to an inflation target by the Minister. In banking supervision and crisis management, some powers are exercised wholly by the Bank while others need ministerial approval. The Minister is directly party to the Funding Agreement. Parliament could have chosen to give the Minister no role re the Governor’s appointment etc but it never has (fortunately or there would be no political accountability at all). The Minister is responsible for the Governor, while the Board – whose chair is removable at will be the Minister – monitors etc the Governor, accountable to her.

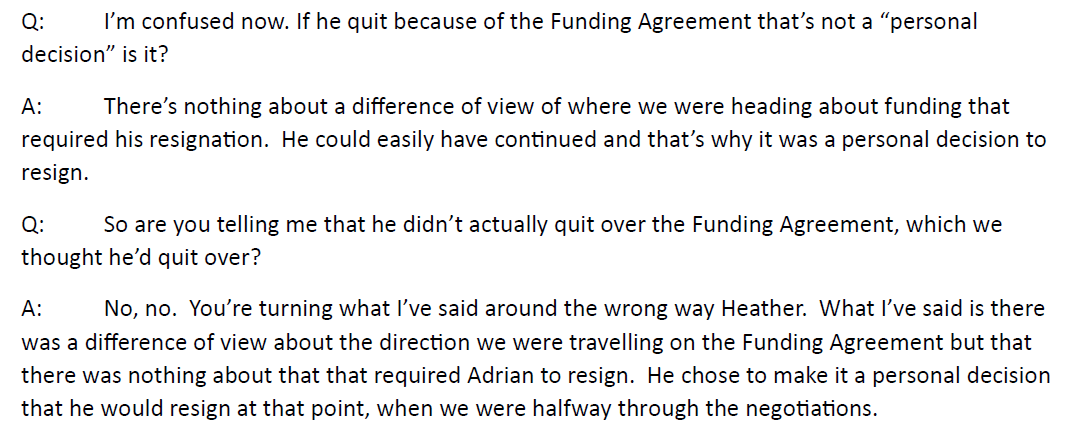

At the very end of the interview Willis is asked

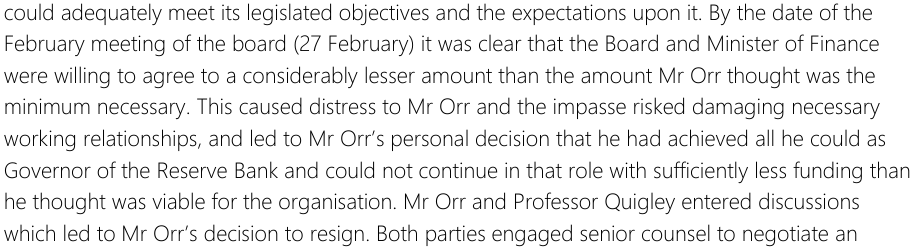

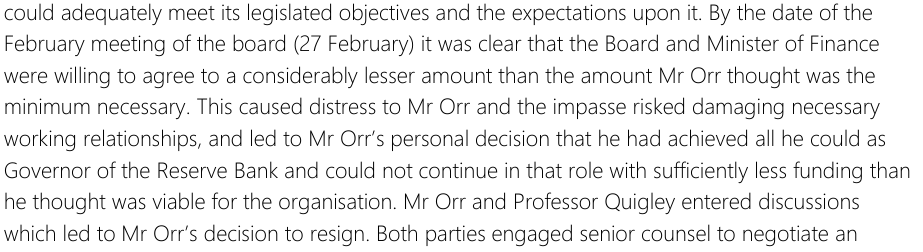

So far, we’ve had two quite different stories from Quigley, neither of which appears to be the truth. First, back on 5 March we were assured it was just “a personal decision”, with denials of any policy or conduct or similar issues being involved. We were intended to believe the man was tired, the job was done, and it was time to do something else. Then on 11 June, the Bank’s carefully crafted statement told us a new story. In this story there had indeed been material differences between the Board and the Governor over what they could live with in the next Funding Agreement. This we were told

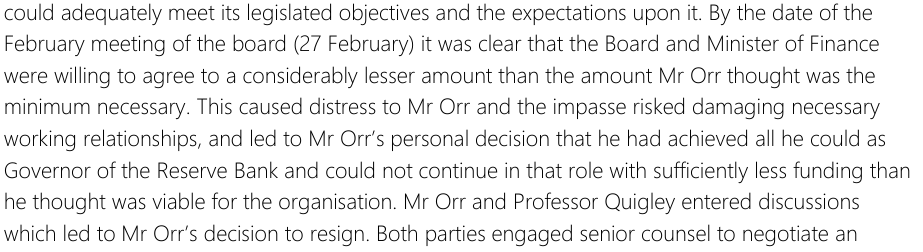

“caused distress to Mr Orr and the impasse risked damaging necessary working relationships, and led to Mr Orr’s personal decision [ that term again] that he had achieved all he could as Governor of the Reserve Bank and could not continue in that role with sufficiently less funding than he thought was viable for the organisation”.

This time we were clearly intended to believe that the “personal decision” [which in a narrow and formal sense it was] was really just about (strongly felt) policy and resourcing differences.

Had you read either or both of those accounts, you might have believed (and were clearly supposed to) that the very first the Minister of Finance would have known that anything so dramatic was afoot was when on 27 February Quigley advised Iain Rennie of something briefly (words were withheld), who in turn advised the Minister briefly (words were withheld), who responded (puzzlingly) with nothing much more than something like “thanks for the update”.

But look at what the Minister said yesterday afternoon

You don’t usually have “employment discussions” when someone comes to you and says their job is done and they are going to leave, and even when the CE comes out of a Board discussion on funding and concludes it might be better for everyone if he, the CE, moves on. There will have been standard resignation and notice provisions in the Governor’s contract. Easy enough to have HR put those in train.

“Employment discussions” between the Governor and the Board preceding his resignation strongly suggest that serious issues were raised by the Board with the Governor, serious enough to have potential implications for whether they would be happy for him to continue as Governor. Which would be consistent with my source’s story, from the post on Tuesday:

And you can well understand why it might trigger Orr’s resignation, since getting to such a point clearly indicated a serious loss of confidence in the Governor, and quite possibly an almost irreparable breakdown of trust.

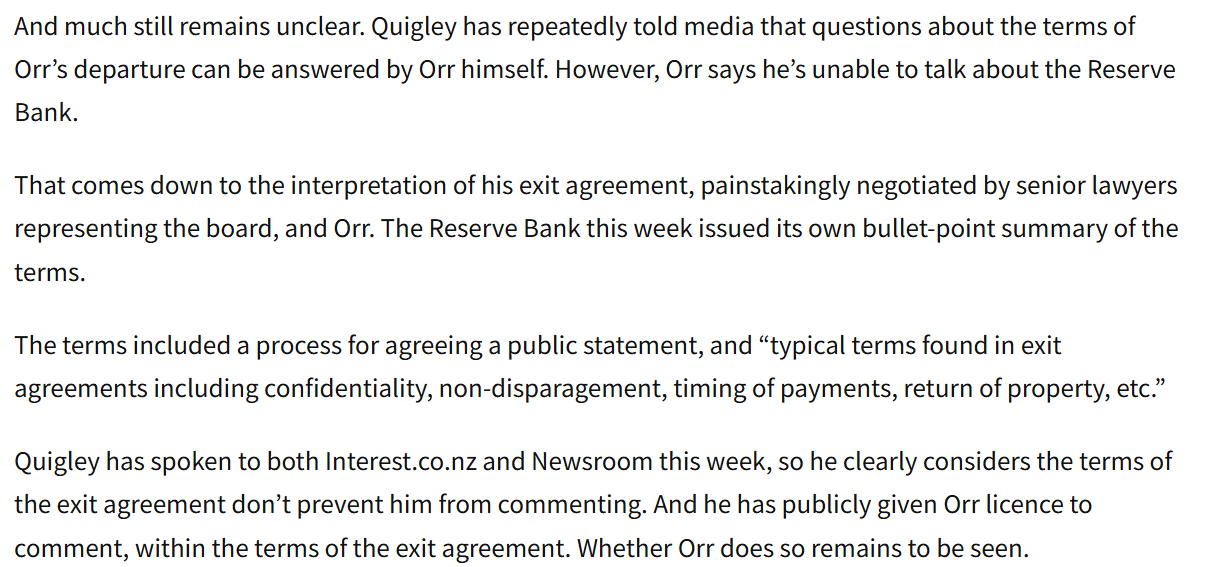

The Minister continues to state that she does not know the contents of the exit agreement then negotiated between expensive senior lawyers for both the Board and Orr. Which, on her account of what went on, should be simply extraordinary, because (a) the resignation would have to come to her, and b) she is the only guardian of the public interest here, and the one who would, in principle, have to account to Parliament for any deals done. She and her office, or at very least Treasury, should have been all over any terms – especially around non-disclosure matters – Quigley was agreeing with her (outgoing) Governor. And yet we must presumably take her at her word that she was not, and the OIAed paper trail suggests no Treasury advice on such matters at all.

One of the things that has puzzled me in the last few weeks is the absence of advice from either Treasury or the Board chair (or Board generally) to the Minister on the looming resignation. Last month I had an OIA response from Treasury (briefly written up and linked to at the end of this post), with almost nothing there (not withheld, just nothing there).

And then on 30 June I had a response to an OIA to the Bank. The relevant bit of the request was this

and their response was

Which isn’t exactly what you’d have expected if the initial Quigley spin had been anything like the truth or if the 11 June statement had been anything like the full story.

But it would make a lot more sense if the Minister of Finance had been the one initiating/prompting the actions that led directly to Orr’s “personal decision” to resign.

There is no direct evidence of that at this point. But something along those lines might explain rather a lot.

Let’s go back to that meeting on 24 February between the Minister, the top Bank people, and (presumably) very senior Treasury people. If Adrian had again lost his cool (“emotions were running high”) what do we supposed happened afterwards? Every one just put it down to a bad day and moved on? It doesn’t seem very likely. After all, we know that a few days previously Quigley had taken the initiative to apologise for Orr’s conduct to a mid-level Treasury staffer. Was he likely to have done much less after his CE blew up in a meeting with the Minister herself? As for the Minister, surely she’d have debriefed with her political advisers – “can you believe that?” sort of thing (of course, they probably could because Orr’s behaviour and style has been well known, including to the Minister, for years), or “we have to do something about him/something has to be done about him”. Perhaps she had a chat with Iain Rennie, or perhaps people in her office passed on the reports of the Treasury meeting a few days previously?

It doesn’t seem at all impossible – and I’m not sure any OIA so far (that I’ve heard of) would have captured this – that she, or someone senior acting on her behalf, got hold of Quigley (keeping Rennie in the loop) and indicated that Orr’s performance was intolerable, and that he really had to go. The specific incidents may have been like a heaven-sent opportunity, with Orr laying himself open, by having openly embarrassed the Board chair and Board as a whole, at a very delicate time re the Funding Agreement, by egregious behaviour – unacceptable in any official – in front of the two groups (MInister and Treasury) they needed to avoid antagonising to try to get a decent settlement. Perhaps Quigley intimated that he had a long list of behavioural issues re Orr that he’d built up over several years, and reckoned the Board would probably have had enongh too. Both sides will have known that only the Minister could fire the Governor – and she wouldn’t want to have done that directly – but it will have become apparent that they had leverage and could put pressure on, that would be likely to result in his “personal decision” to leave. And if something like that is what went on, maybe the Minister – conscious of maintaining semi-plausible deniability – indicated that whatever it took should be done, and don’t bother me with (or show me) the details.

It fits the facts we have better than any other story so far, including in making sense of why Willis has been so over the top in her disavowal of any involvement and insisting (contrary to the law) that hiring and firing etc Governors was just a matter for the Board, nothing to do with her. And, of course, of why there was an exit agreement – negotiated by senior counsel at all – with gag orders etc: they wouldn’t have been willing, probably, to directly fire Orr (judicial review has always been a risk too), and so he could insist on (some) terms, but it isn’t clear that Quigley isn’t using them to protect himself too.

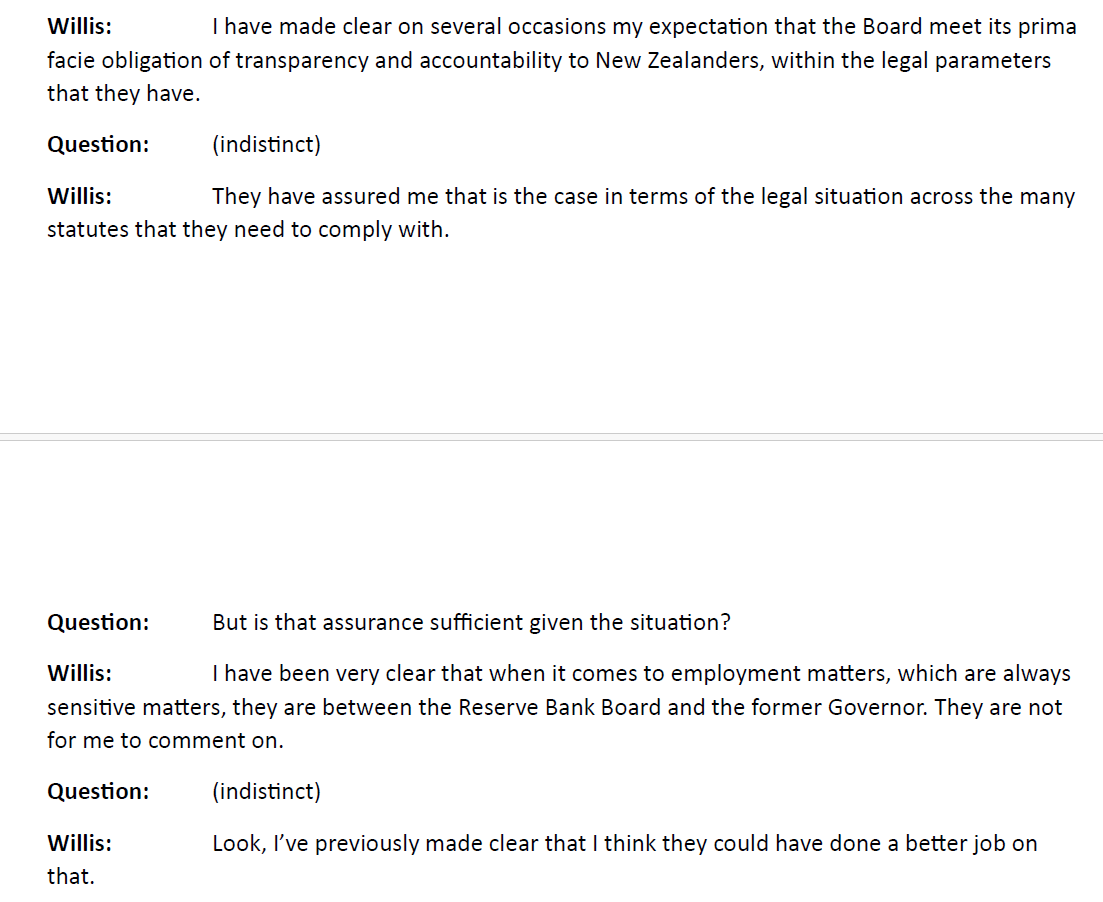

If the truth is anything like this – another layer behind the story from my source, which itself so far looks sound – perhaps where they (the Minister in particular) misjudged was in putting too much confidence in Quigley to deal with the public side of things (if so, pretty inexcusable on her part as Quigley has no track record of being a deft and effective or trustworthy communicator). Both after 11 June and again yesterday the Minister has indicated that she isn’t satisfied with what the Board has said (or not said). From the interview yesterday

“I have also however previously shared my disappointment at the way information on this matter has been shared with New Zealanders. Today I had a prescheduled meeting with the entire Board of the Reserve Bank and at that meeting I sought to convey to everyone present that I was disappointed with the way that this matter had been handled given the ongoing public speculation because it is in New Zealand’s interest that the Reserve Bank maintains its reputation at all times and I think with better handling we would not still be having these interviews and this discussion.‘

Well, indeed, but what did you expect? They never seem to have had lines that they’d effectively stress-tested (to stand up for more than a few minutes – 5 March – or hours – 11 June) and hadn’t even got the process straight (witness what the Bank has already confirmed that the Minister was putting pressure on on the afternoon of 5 March for Quigley to do a press conference he didn’t really want to do – something surely that should have been sorted out in advance and properly rehearsed). The Minister clearly now isn’t that happy with the ongoing OIA obstructionism, and she is quite right to suggest that better handling of this whole thing would have seen it as yesterday’s story, one for next history of the RB, pretty quickly, perhaps within a week or two of 5 March. Instead, here we are, months on, and so many unanswered questions, including from the Minister herself, and with the Ombudsman all over the issues.

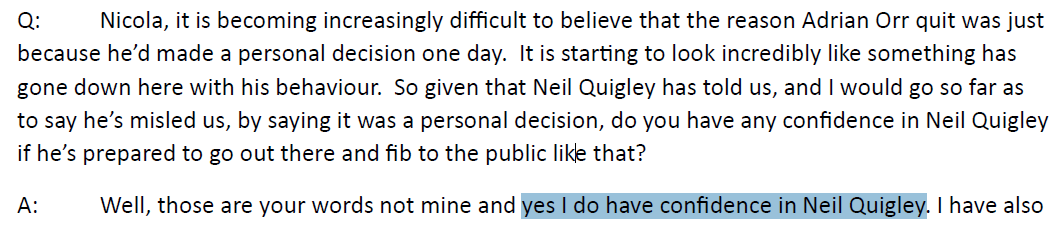

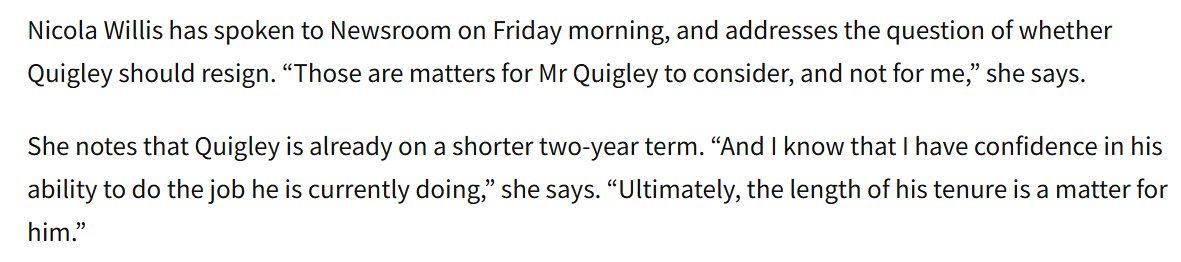

The Minister’s main message yesterday – to various outlets – was that she still had confidence in Neil Quigley as Board chair (which since she could have fired him at will and hasn’t we pretty well knew that by revealed preference).

But why? Some speculate that perhaps it has to do with the medical school – might not be a good look, might undermine confidence, to toss Quigley out the very week the government had granted him his controversial new medical school.

But it might also be that in some sense in fact she is deeply grateful to Neil Quigley, for having done the dirty work, possibly at her own bidding, and got rid of Orr. Perhaps somehow that compensates for the Clouseau-like performance over months since – only worse than Clouseau because it is quite clear that Quigley wasn’t just bad at this stuff, but that he had, and has, consciously and repeatedly set out to mislead New Zealanders.

In one of those quotes a little way back up the page the Minister rightly stressed the importance of the reputation of a central bank. The Bank knows it too. This is from their recent Statement of Performance Expectations

But the problem is that we (and they) are starting from things as they are, and it is hard to see anyone with even a modicum of interest could have any trust at all in our powerful independent central bank and those who run it. There have been repeated policy failures, bloated budgets (and spending last year left to run wild while the Minister did nothing to rein in the Governor or Board chair), lies to Parliament, lies to the Treasury (see final bit of this post on Quigley and the first MPC), pretty weak (or worse) policy communications, top tiers of management currently held by people simply not fit for the job, a Governor with serious behavioural issues left unchecked for years, and now all this……the active misleading, the cover-up, and (from the chair) the sheer disdain for any sense of public accountability or interest. Oh, and a Minister who did nothing about any of this for her first year or so in office – about conduct, about fiscal excesses, about replacing the chair, about filling board vacancies, about simply insisting on something a lot closer to both excellence and openness.

And that is among the reason why Quigley really should resign or be sacked now. There will be a new Governor later in the year. That person will need to sweep clean. But how can we have any initial confidence in a new Governor – whether some stray Canadian hand-me-down not likely ever to make Governor at home, as speculated in the press the other day, or whoever – when that person has been selected by a process led by the same chap who delivered us Orr in the first place, who championed his reappointment despite all failings being evident by then, who presided over that budget-blowing (well Funding Agreement blowing) last year, and who can’t or won’t even give a straight story – somewhat diplomatic as it might have to be – about the early departure of the last Governor.

Anyway, some questions to ask. Perhaps the story here is also nothing like the truth. But it is beyond time for the truth to be told and a clean breast to be made of things. And if what happened is something like what is suggested here, it should mean some very serious questions indeed for the Minister of Finance as regards her part in misleading New Zealanders. Not exactly a sound basis for trust.

(UPDATE: To be clear, if the Minister did engineer Orr’s departure along these sorts of lines, then well done her – found an opportunity and seized it – and there should be no harrumphing about affronts to central bank independence. But the subsequent spin, misdirection etc would still raise very real questions.)

Since I published the post on Tuesday, reporting what an anonymous (currently or recently former) insider had told me about events around the Adrian Orr resignation, what new we’ve heard or learned seems (to say the least) not inconsistent with the substance of that person’s story.

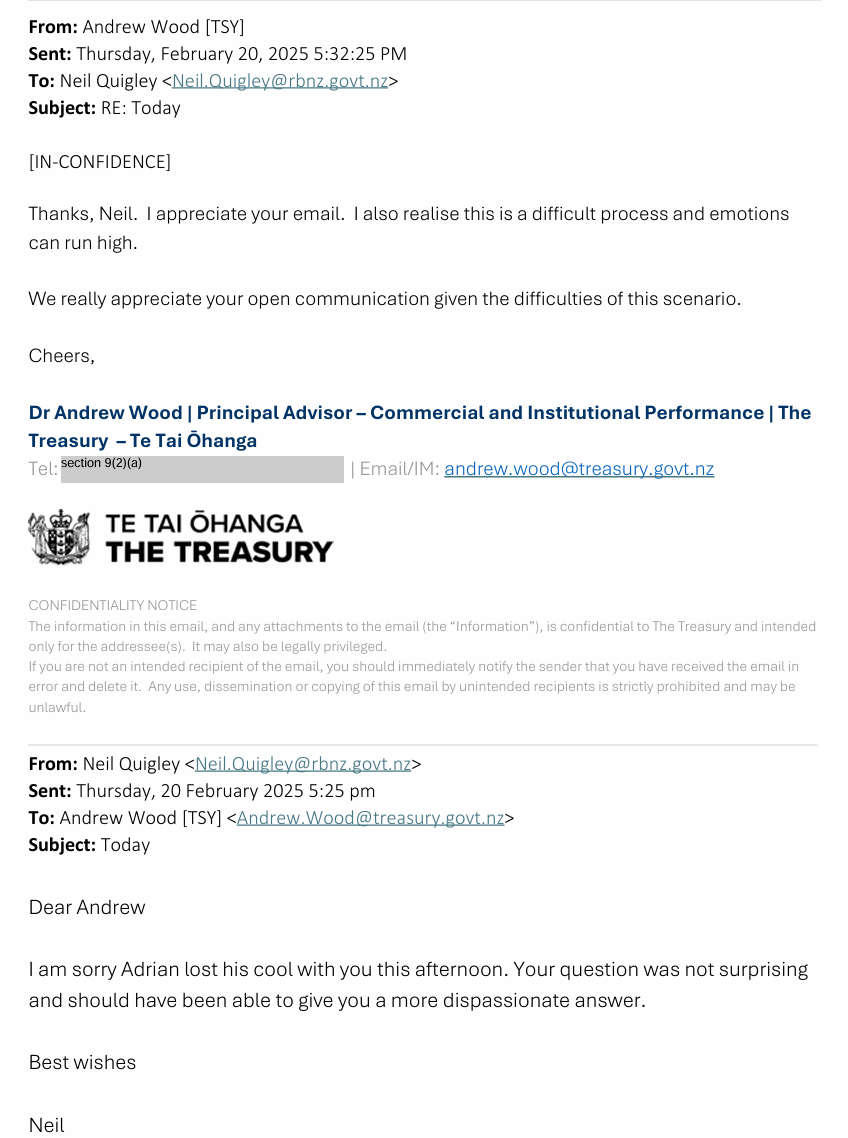

As it happened, the one concrete revelation may almost have come about by accident. In my post on Tuesday I’d written that Board chair Neil Quigley had contacted Treasury quite agitated about a Treasury record of a meeting between senior Bank and Treasury people on 21 February. It was only yesterday I reread my source and realised I’d made a mistake, and that bit of the story related to the meeting between the Bank, Treasury, and Minister of Finance on 24 February. But by then the Herald had asked Treasury about the earlier meeting (which was actually on the 20th). Treasury could, fairly easily, have stonewalled, but in fact they confirmed that Neil Quigley had emailed one of their staff after the meeting in respect of the Governor’s behaviour at that meeting. Today they have released that email exchange.

We don’t know how bad it got but…..things have to have been pretty bad for the Board chair to have taken that initiative (and notice the Treasury official’s “emotions can run high” – about funding debates, among normal disciplined people???), presumably having failed to persuade his chief executive, the Governor, that he himself needed to apologise. So, if we don’t yet know a lot with certainty about the 24 February meeting, and the record thereof, we now definitely know that Orr’s conduct was a significant issue just days before the exit agreement negotiations started, following the Board meeting on the 27th.

We don’t know with certainty that Quigley emailed Orr on the 27th attaching a statement of behavioural/conduct issues going back several years, and asking for a response, but…..the Reserve Bank refuses to deny the existence of such a document (there are multiple OIAs from people trying to smoke it out). Even allowing for their dogmatic “we’ve said all we are saying or legally can say” line, if the story was simply untrue, and had no basis in fact, surely it would be in both Orr’s and Quigley’s interests to have it denied in no uncertain terms (free opportunity to tar me as well I guess). The obstructiveness is, almost certainly, pure choice. And despite their claims otherwise, there has been no evidence of good faith dealing with legitimate public interest at almost any time since 5 March, when Quigley began his unsuccessful attempt to mislead us into believing that it was just “a personal decision’ [as in one sense it was: Orr is a person, he did decide] of someone who was tired or thought a big job had now been done and it was just time for a change.

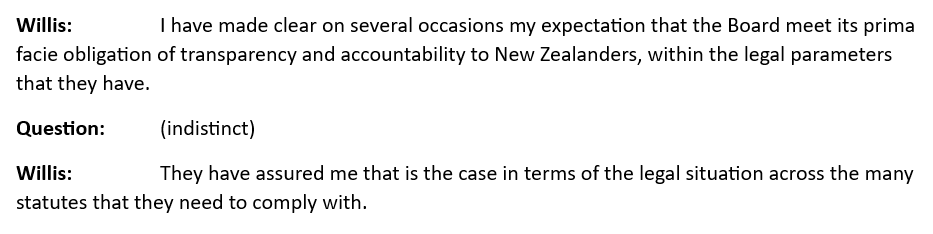

The Reserve Bank and its Board appear to be attempting to hide behind claims that there are legal restrictions on what they can say, including in response to OIAs (and remember that any request for information can in technical terms be considered an Official Information Act request whether it is answered on the spot or months later). This was a line they have also fed to the Minister who said the other day:

First, consider the Official Information Act itself.

There are conclusive reasons for withholding information. But they relate to national security, diplomacy, and one the Bank has occasionally used on me (very dubiously even then), things that if released could

What was going on around the unexpected sudden departure of the Governor just does not count.

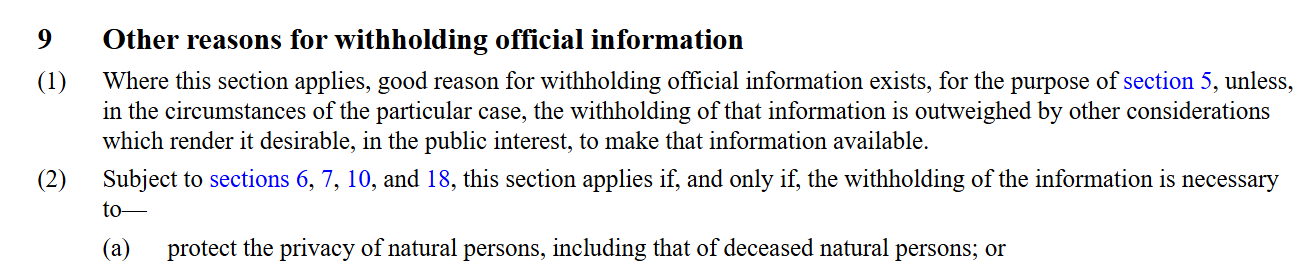

So then we are down to section 9 which has a whole long list of other reasons why information can be withheld, all prefaced with the public interest override. It seems probable that 9(2)(a) is what they will be relying on

although whether it is Orr or Quigley, or perhaps both, they are trying to protect is perhaps open to question. For Quigley, of course, there would no case at all – embarrassment of someone who appears to have actively, deliberately, and repeatedly sought to mislead the public from his highly paid perch as chair of a government board is exceptionally unlikely to count as decent grounds.

Employees are a different matter. If some junior employee was quietly exited you’d expect 9(2)(a) to apply, in all but the most extreme circumstances (if I recall correctly I was once – possibly still – a party to such an arrangement – as manager that is, not employee). But on this occasion we are talking about the utterly unexpected no notice departure of one of the most senior, powerful, and controversial public officials. And it is also clear that the Bank – and its board chair – have already sought to obstruct understanding, transparency and accountability on repeated occasions. Not just by trying to convince us it was just “a personal decision” (tired, job done etc) but by obstructing (for months) and still OIA requests that included requests for material that cannot be any stretch of the imagination come wholly under 9(2)(a) at all (eg there are four board meetings in March – one the day the resignation was announced – where they have not even acknowledged the request for the minutes, let alone provided those minutes, even heavily redacted). They are trying to stonewall and obstruct understanding, and they should not be allowed to do so. 9(1) would give them ample grounds to release almost anything that has been requested, if they were at all interested in the public interest (in scrutiny, accountability, transparency….and little things they say they value like trust in an independent central bank). I say “almost everything”. If there really is the “Statement of Concerns” document, with its list of (alleged) behavioural/conduct issues, I don’t feel a need to see it; the fact of its existence and being sent to the Governor with a request for a response would then provide ample certainty, that what actually happened was a negotiated exit in the context of severe relationship breakdown and loss of mutual confidence, brought to a head by actual and recent serious conduct incidents.

The remaining uncertainty is around the exit agreement negotiated with Orr. As I noted weeks ago, if someone resigns because they are tired etc, you don’t need expensive lawyers to negotiate exit agreements. Tired and job done are perfectly legitimate comprehensible reasons, with nothing to hide. You might agree to waive notice, but it doesn’t take a lawyer for that.

But in this case the expensive lawyers (“senior counsel”) were brought in by both sides.

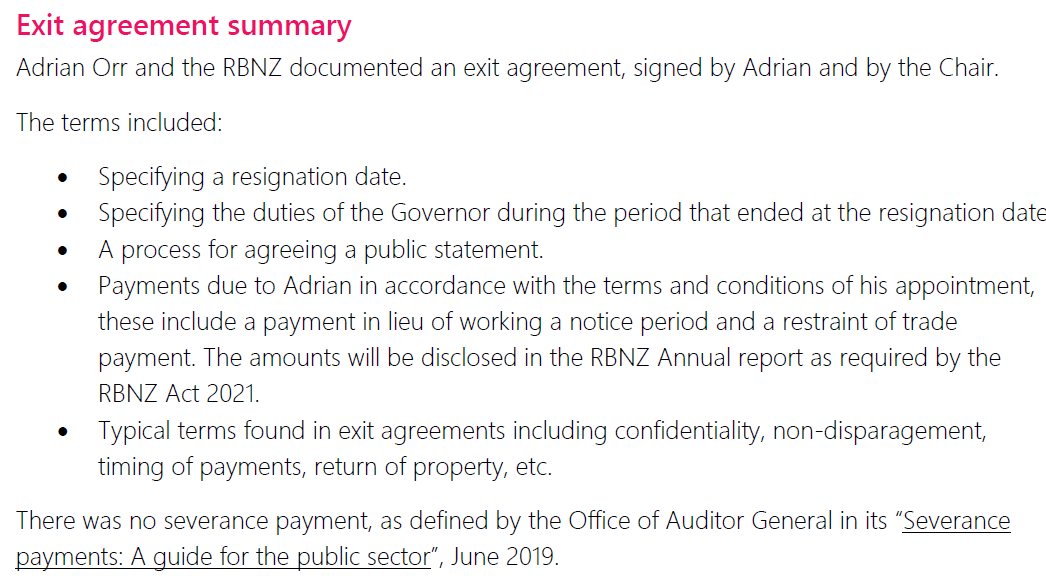

This is what the Bank told us about the agreement on 11 June

I’ve now lodged a request for a copy of the items: “a process for agreeing a public statement”, and terms around “confidentiality, non-disparagement”. These seems likely to be very process oriented (very unlikely to describe whatever bad stuff Orr is claimed to have done) so there shouldn’t be any grounds to withhold, and there is a clear public interest in such a release, given that no one has given clear answers about the parameters of what the Bank promised not to say or why (or, I guess, what Orr promised not to say). I’m not optimistic, but we’ll see.

As far as I can see (but I’m not an OIA lawyer) you can’t just contract out of the OIA by signing an NDA (with quite as broad a reach as suits two people trying to avoid transparency, scrutiny or accountability). Ombudsman guidance notes suggest as much, but who knows. It looks as though whatever the NDA provisions in the exit agreement are, they could still be overridden by the “public interest” test in section 9 (the more so perhaps now, with so much effort to mislead already, than on 5 March). Perhaps the Bank has committed not to do so unless the Ombudsman explicitly rules otherwise – which could be years away, although I’m sure that I like all who’ve appealed related issues to the Ombudsman hope he is going to give this issue some urgency. We don’t know, and it isn’t good enough to simply wave your hands and say “we’ve done all we legally can”, often without even telling us the nature of what they’ve got and have withheld, or to explain what the parameters are of what they contracted to.

If this really is what it increasingly looks like, a negotiated but pressured exit, precipitated by real behavioural/conduct issues, perhaps some limited sort of non-disclosure provisions might have been a price worth paying. But even if so the public interest – transparency, accountability and all that – had to be paramount, and any restrictions had to be very tightly limited. And non-disclosure agreements don’t give license to simply make stuff up, and actively mislead the public. If Quigley is – as he probably is – so tone-deaf and indifferent to wider public interest considerations not to see that (and to recognise that interested parties were not likely to give up easily on seeking answers), the Minister (and Treasury) should have insisted on it. And despite the Minister’s attempt to disclaim all responsibility, recall that Orr’s resignation was to her, she is the only one who could have fired him, the board chair serves at her pleasure, the board operates accountable to her, the board operates within broad parameters in her letter of expectation. If she knew nothing about it, that is on her. She, it seems, had days to ensure that the public interest was being protected, and that real accountability would be protected.

As for the Minister of Finance, what is new from her is that she says that the first she knew of that Quigley email to Treasury was yesterday. Quite possibly so in the specifics, but Treasury is formally charged by her (and funded) to act as monitor on the Reserve Bank. If they had not been keeping her abreast of conduct concerns which weren’t exactly new – and many of them in the public domain anyway – they simply weren’t doing their job.

There isn’t much else to say about the Minister beyond the scepticism I noted in yesterday’s post. Does anyone believe she didn’t know what was going on? But in reflecting on the mystery of her dogmatic insistence that it is all nothing to do her, two old lines did come to mind:

methinks she doth protest too much, and

who will rid me of this turbulent priest [or Governor]?

If somehow she did use an opportunity that Orr created by his behaviour in mid-late February to prompt Quigley and the Board to somehow engineer an exit (that list of behavioural/conduct issues Quigley seems to have had must have been tended and grown over several years) then….well done Minister. If not, well….the mysteries are still there.

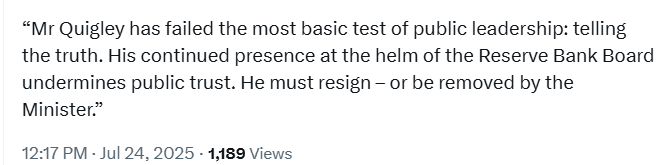

As to Quigley, whether or not the Taxpayers’ Union is generally to your taste, it is hard to disagree with this concluding paragraph of their call this afternoon for Quigley to go.

UPDATE: The one other thing I meant to include here was a suggestion that some journalist might ask the Bank (or other plausible entities where people might have become aware of the relevant bits of information – eg Treasury, or MoF’s office) if they’ve launched a leak inquiry. If it is all make-believe stuff and nothing of substance was true in what my source said then…..there wasn’t a leak. If some or much or all of it was substantively true then, given the Bank’s determination to say nothing more, there was a leak from somewhere. I have no idea where the source works or worked, but there is probably a quite limited range of options, and the Bank must be one of them.

Following on from my post yesterday, two of the key players in the story (one of whom is keen to minimise her role) faced questions.

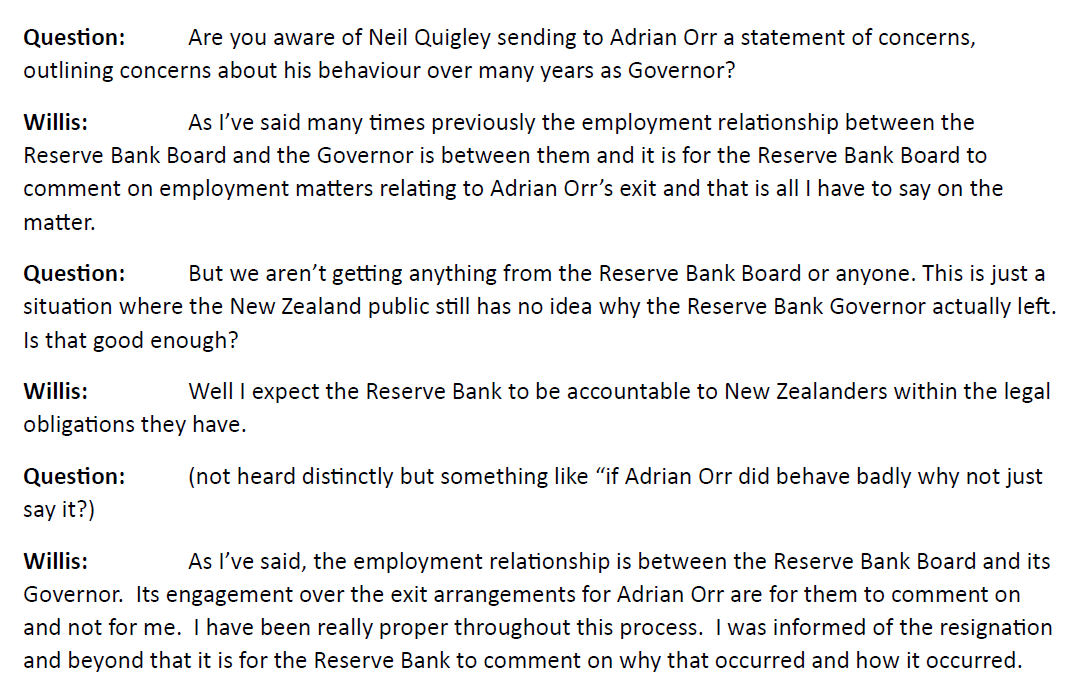

The first was the Minister of Finance who was questioned by a number of journalists before going into Parliament’s debating chamber early yesterday afternoon. The Heraldposted the audio, and I’ve made a transcription here.

Ever since the announcement of Orr’s resignation on 5 March, when he departed with no notice on the very eve of a major international conference he’d been quite ebullient about planning to host, the Minister of Finance has attempted to distance herself from it all.

At times she has asked us to believe that she didn’t actually know any more than we did about why Orr resigned (“I have always been able to speculate” was one of her early lines), which can really only be true if she let it be known to The Treasury and the board chair that she did not want to know, and if Orr himself gave no reasons in the letter of resignation which he had (by law) to have addressed to her (I have asked for a copy of that letter and of any reply). What responsible Minister of Finance, advised by the Secretary to the Treasury (in turn advised by the board chair, Quigley) that Orr had indicated he would resign would not ask (a) why, and b) seek out details of when and on what terms? A resignation with three months notice might be a very different matter (including in terms of temporary replacements etc) than leaving with no notice at all. Someone tired and wanting to retire to his farm very different from someone going following a scandal about to be revealed or an irrevocable breakdown of trust. No one can seriously believe that she didn’t know (even if what paper trail we actually have is thin at best).

The thrust of Willis’s comments yesterday was, again, that it was nothing to do with her and all a matter for the Bank’s Board. That is playing fast and loose with the law.

As a reminder, the Board does not appoint the Governor. The Minister (via Cabinet and the Governor-General) does, albeit she can only appoint someone the Board recommends. The Minister is the only person who can fire the Governor. The Board members are all appointed by the Minister and are, by law, accountable to her for the performance of their duties. Board members can only be dismissed for just cause, but the board chair is not only appointed by the Minister but can be removed by her at will (no substantive cause required although she has to consult the person before dismissing them). Resignations of a Governor are made, again by law, to the Minister of Finance. The Board does not even get to set the Governor’s pay (that is a matter for the Remuneration Authority) although it does get to set the other terms and conditions of employment (presumably including standard resignation and notice provisions in the Governor’s contract).

I noted that only the Minister could fire the Governor (and only for, statutorily identified, ‘just cause’, which doesn’t include policy disputes). The Board has a responsibility to monitor the Governor’s performance and is obliged by law to report to the Minister if they think there is just cause for the removal of the Governor (a couple of grounds – re obstructing the Board – can only be used by the Minister if there is a positive recommendation to act from the Board). They simply do not hire or fire the Governor, notwithstanding the Minister’s attempts to influence the general sense otherwise. The Governor is the Minister’s responsibility. Which is as it should be given (a) how much power Governors wield, and b) that only the Minister is accountable to Parliament and the public.

Instead we get stuff like this (which probably captures the flavour of the rest)

Or

The Board chair serves at your pleasure Minister. If the Board is not being adequately transparent with, and accountable to, New Zealanders, and you do nothing about the chair, that responsibility is on you.

And note that rather than answer the very final question about the non-disclosure agreement apparently signed with Orr – the terms of which we also don’t know – Willis simply walked away.

In an earlier post, I identified a substantial list of questions for Willis. None of them has yet been answered. All remain germane to understanding what happened, and the context for what happened.

I’m almost inclined to wonder if there is not yet one more final layer behind the story in yesterday’s post. Why is the Minister so determined to try to convince us it is all nothing to do with her, when a powerful senior official appointed by the Minister of Finance, dismissable only by her, suddenly ups and leaves with no notice (but several weeks of pay nonetheless)?

The second interview yesterday was one Heather du Plessis-Allan did with board chair Neil Quigley. You might wonder how she got him on her show, given his usual reluctance to engage with journalists on Bank matters, but apparently he wanted to be heard in defence of his medical school, and that provided the opening for questions on Reserve Bank stuff. The audio is here (starting about 4 minutes in) and my transcription is here

I hadn’t previously noticed that the 2021 Reserve Bank Act now requires the Board to operate “in a manner consistent with the spirit of service to the public” (that Peter Hughes phrase that is supposed to guide all the doings of the public sector as a whole). I’d be surprised if anyone thinks that the Board’s approach since lunchtime on 5 March has shown any resemblance to being “consistent with the spirit of service to the public at all” (and probably not in the days prior when they appear to have, with the Minister’s acquiescence or not, signed up to a gag agreement with Orr to protect them, Orr, perhaps the Minister (or all three) but definitely not the public). Quigley last night was in his usual poor form, obstructive, misleading, and still defending the claim that it was just a “personal decision”.

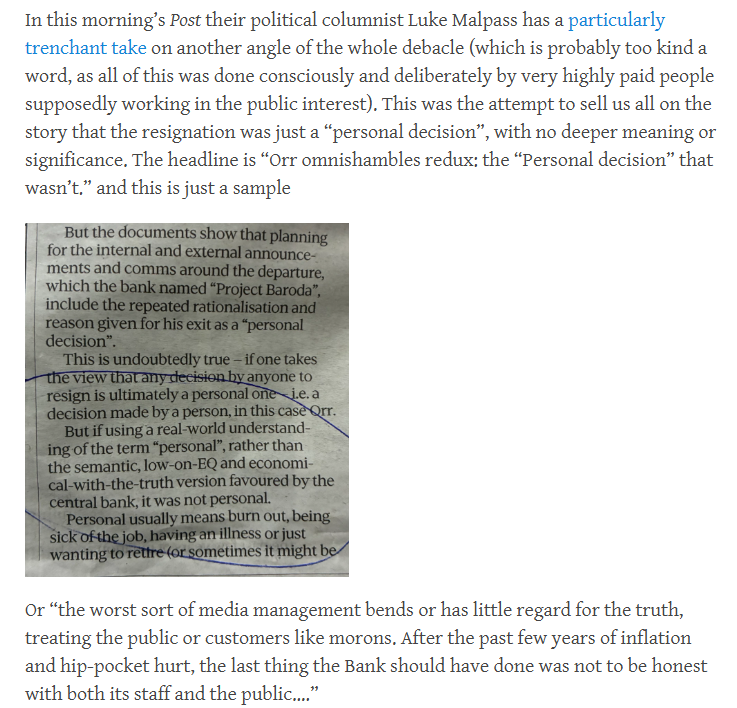

Since it was such a good quote from Luke Malpass, it is a shame not to use it again

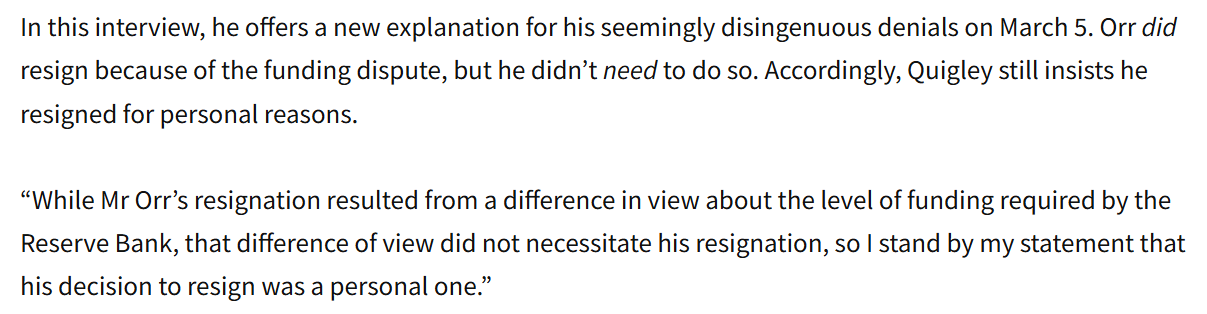

In this particular interview, Quigley spends some time trying to convince the interviewer that there is a material difference between saying that a departure was a “personal decision” (his actual words on 5 March) and saying that it was “for personal reasons”. It is angels-on-the-head-of-a-pin in this context.

In the interview, faced with repeated questions about claims reported in yesterday’s post, Quigley refused to say anything. He refused to say whether Orr had sworn in a meeting with Treasury on 21 February. He refused to say whether Orr had sworn at a meeting with Minister and Treasury on 24 February (he was at both meetings). He refused to say whether he’d sent an email to Orr three days later with the catalogue of conduct/behavioural issues. He attempts to justify his silence on some pretend right that Orr has to privacy, but of course by refusing to comment he confirms the essential truth of the claims. Had they been materially false, sure it was his obligation – having been directly involved or witness to all three, and as chair of the Board – to have refuted the claims in the strongest terms (quite possibly having a go at me as well, as gullible or worse) precisely to protect the former Governor. If none of this happened, surely Orr too would want us to know, lest we think worse of him than he really deserves.

Quigley’s other line was that all this was covered by “an Official Information Act request” (there were actually multiple requests)

This is simply nonsense. The Bank’s 11 June pro-active release covers nothing at all about the meetings on 21 or 24 February, nothing at all about the Board’s deliberations or communications with Orr, nothing about the substance of gag orders (or why they ever made), and nothing (of course) about the (claimed) 27 February email. In addition, the Bank has chosen simply to ignore (not to decline with specific reasons) whole categories of inquiry that made up those Official Information Act requests. What is truer is another a line he used which is basically that we said all we are going to say on 11 June, and tough luck on anything else. Which doesn’t seem like either the “spirit of service” or any sort of spirit of compliance with the Official Information Act itself. We shall one day – perhaps next year, perhaps the following one – what the Ombudsman makes of the defiance of the law.

The final aspect of Quigley’s specific comments I wanted to touch on was the convoluted round-in-circles discussion on the role of differences over the Funding Agreement played. For example

But that is actually quite telling. It goes to the point I have been making since 11 June, that this was not a departure simply over differences around the future Funding Agreement (bureaucrats face those sort of disappointments all the time, especially in the last couple of years). And, actually, the Bank has said as much. Remember this from their statement of 11 June

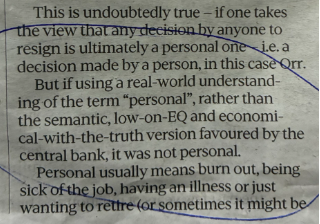

Even if this was true – and it seems increasingly unlikely that it was anything like the essence of the truth – it is such a severe difference of opinion, expressed presumably in ways from which there was no going back (unlike usual robust discussion among peers etc), that it was pretty clear the Governor had to go, that things just wouldn’t work in future if he stayed. That is the clear import of the Bank’s own statement, and the bit they released in error on the morning of 11 June, had tied that breakdown more closely not just to the board but to that meeting with the Minister. Of course, in some sense it was a “personal decision” (as Quigley claimed all along) but it had nothing to do with being tired, sick, or a sense of a job now completed. There is, as my source yesterday implied, a strong element of being pushed (and Quigly himself consistently refuses to shed direct light on that, despite his role supposedly being to serve the public, accountable to the Minister). It wasn’t (as Neil says) the funding discussion per se that “required” Adrian to resign – smart people will have robust arguments about resourcing and then, once settled, move on – but about things much deeper about Orr’s own conduct, quite possibly building on the list of behavioural complaints that Quigley seems to have compiled over several years.

Some straightforward answers would be nice – from the Minister, from the Board chair, perhaps even some board member who might consider breaking ranks (perhaps at the cost of their position) because they think the public deserves to know. The questions are about both substance and about process. Had we had an honest accounting months ago (at absolute latest when the Funding Agreement was signed), the issue would all be water under the bridge by now. Instead….most questions are still unanswered, and Quigley presumably hopes the Ombudsman takes his usual dilatory approach (on usual form, Quigley would be gone next July before we hear anything from the Ombudsman’s office).

On 11 June the Reserve Bank finally (more than three months after his departure) did a pro-active release of carefully selected documents relating to the departure of Adrian Orr. Those documents purported to respond to various OIA requests, although many elements of events around the departure, and many elements of the OIA requests, were simply ignored. It appeared to be a belated attempt to shape the narrative, never mind the law.

I’ve done a number of posts on these issues since 11 June, drawing partly on what the Bank released in that package, and on various interviews, and some other OIA releases, all to try to make more sense of what really went on in the months, days, and weeks leading up to the resignation and sudden departure of the central bank Governor.

That last post, from last Thursday, prompted someone who seems to have been very close to events back in February/March to contact me out of the blue with a number of quite detailed comments about some of what really seems to have happened. I do not know who the person is.

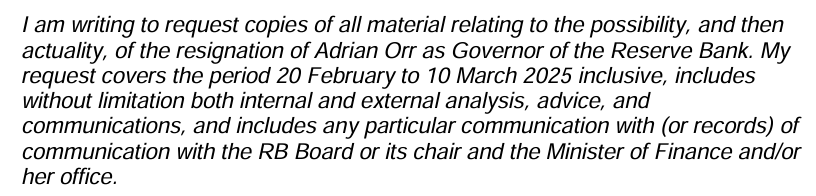

I also cannot directly verify what follows. I have however this morning lodged a series of Official Information Act requests with the Minister of Finance, the Reserve Bank, and The Treasury in an attempt to check key elements of the account. My overall sense is that the account is likely to be trustworthy. It is written in a calm style, in places details fit with other stuff that is already in the public domain, and the author is not black and white (at one point Quigley is defended, on another where part of the account appears to be secondhand, the lack of certainty is explicitly acknowledged). My interactions since suggest someone who, while a little fearful for their own position, is frustrated at the lack of transparency (including abuse of the OIA) and believes more of the story needs to be told. Could I be being played? I suppose so, but on balance I don’t think that is what is happening.

When I was contacted, the person commented positively on what I have written about these events and suggested that they wanted to fill in some gaps. I will step through the various elements of the account I have been given, and will explain how what I was told fits with other stuff we know, or seems to fill gaps. As I noted to the person, their account “isn’t overly surprising unfortunately”.

The person who sent me this account out of the blue asked just that I keep their details confidential (I have barely any). I was still a little unsure what they envisaged or hoped for, so I went back and explicitly asked what, if any, of what they had sent me they would be happy with me using here. I noted that an alternative would simply be that I used what had been provided to shape some more OIAs without referring directly to anything in this correspondence. I also suggested that I might not be the ideal vehicle if they did want the material publicised and explicitly noted that, for example, the Herald had given these issues serious coverage and might be a better vehicle (including – a point I didn’t make explicitly – because they could ring up people in power and ask follow-up questions directly).

I was uneasy about the idea of using direct quotes since, in principle, writing style could be used if someone (a past or present employer) wanted to try to track down the individual. Independent of that unease, my correspondent got back in touch and explicitly indicated that they were okay with me using their information here, subject to using paraphrases rather than direct quotes. They reiterated both an unease about their personal risk and a view that the story should be told. They have made several mentions of the public interest considerations that are supposed to be of importance in dealing with OIAs.

And so here goes:

In last week’s post, I referred to a mention in a recent OIA response from the Reserve Bank that an hour or so after Orr’s resignation had been announced the Minister of Finance’s office had asked Neil Quigley to do a press conference. According to the Bank’s account, “the Minister thought it was important for the chair to front the media and possibly to calm the markets”. I’d noted in another post that no one had made Quigley do this press conference (which proved to be a bit of train wreck).

My correspondent starts by noting that in their view on this point I had been a bit unfair to Quigley. It is claimed that Quigley did not want to talk to the media (something I can quite believe, based both on his past behaviour and his responses to questions on and after 11 June) and had made that clear to management. My correspondent states that it actually took multiple communications, texts and calls with/from both the Minister herself and people in her office, before Quigley finally agreed to do so. There was no hint of any of this in the 11 June Reserve Bank release and my correspondent indicates that it was material that was within-scope for at least some OIA requests on events around the Orr resignation (including, I believe, mine). I still maintain that it was Quigley’s choice to do the press conference, but clearly he was put under considerable pressure.

In and of itself, it is not a revelation of great moment. However, the Minister of Finance has consistently attempted to distance herself from events around the Orr resignation, having claimed variously that she had no knowledge of why Orr resigned (“I have always been able to speculate”) and had no contact with the Board or Board chair on such matters (even though the Governor’s resignation had to be made to her not to the Board and – more a matter of substance than law – this was the very powerful chief executive of one of her main agencies). Perhaps it also points to the chaos of the day: recall that an earlier Herald OIA had revealed that Orr’s resignation had been brought forward on the morning of Wednesday 5 March to that day rather than, as planned until then, the following Monday. One might have supposed that the Bank, the Board chair, and the Minister and her office would have sorted out who would say what when before the resignation statement went out.

The second leg of the story goes to the heart of the resignation itself.

Recall that the Bank has tried to spin us a story that it was all about disputes over the Funding Agreement. This extract is from the (final version of the) statement the Bank published on 11 June.

An earlier (but near-final) draft – which they sent in error that morning to OIA requesters – had tied it more to a meeting between Orr, Quigley, Treasury officials and Willis on 24 February.

I noted then that it clearly wasn’t correct to characterise this as just a dispute over funding (as much media coverage did), since many public service CEOs have had disappointed expectations in the last 18 months and none of them had resigned with no notice. In one of my post 11 June posts I even observed (but briefly and without follow up) that it really wasn’t clear to what extent Orr had chosen to go and to what extent he’d been pushed.

My correspondent suggests there was a very considerable element of push to it, and that funding disputes were really no more than the immediate presenting context.

You may recall that an earlier Herald OIA (reported here) reported some Q&As that the Minister’s staff had prepared for her around the resignation included the telling one “Did the governor ever raise his voice with you?”, which it was suggested she should avoid answering, clearly suggesting that exactly such a “voice raising” had in fact occurred. As David Farrar put it at the time

My correspondent says “raising his voice” was the least of it, reporting that at a meeting with Treasury on 21 February the Governor had completely lost his cool, behaving in a way that was “completely inappropriate and swearing” and that it had been much the same in the 24 February meeting with the Minister.

The timing of these events is pretty clear. The fact of the 24 February meeting has long been known. Of the meeting on the 21st we hadn’t previously heard directly, but it is likely to be the one proposed in this email from Quigley that was in the 11 June release pack

but ended up happening on the 21st rather than the afternoon of the 20th as Neil had proposed. The Bank clearly envisaged by this point that it was going to be smooth sailing on the Funding Agreement from here and that everything could be tied up within a few days. Clearly, that wasn’t what happened…..and as context for Orr completely losing it (if in fact he did) it sounds quite plausible and aligned to the facts.

Now, in this debauched age swearing isn’t uncommon and newspapers have taken to reporting crass and vulgar language directly. If you are less bothered by such behaviour than I am, it was still pretty extraordinary for an official – no matter how senior – to completely lose it in crucial meetings, most particularly with/to the Minister herself. You could see why future working relationships might be impaired – not by differences over approved spending (just the meat and drink of bureaucratic life) but over Orr’s quite extraordinary conduct. Or rather, just the latest episode.

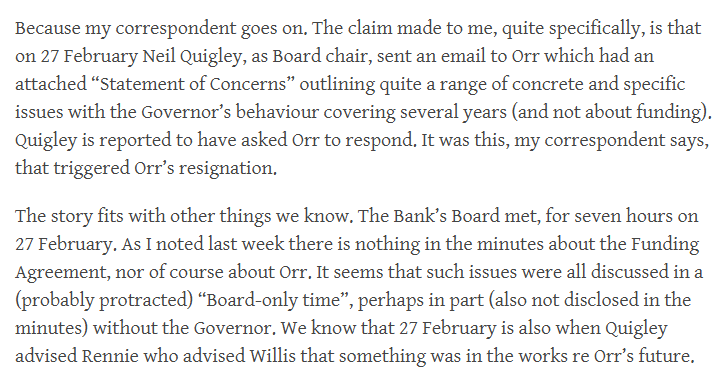

Because my correspondent goes on. The claim made to me, quite specifically, is that on 27 February Neil Quigley, as Board chair, sent an email to Orr which had an attached “Statement of Concerns” outlining quite a range of concrete and specific issues with the Governor’s behaviour covering several years (and not about funding). Quigley is reported to have asked Orr to respond. It was this, my correspondent says, that triggered Orr’s resignation.

The story fits with other things we know. The Bank’s Board met, for seven hours on 27 February. As I noted last week there is nothing in the minutes about the Funding Agreement, nor of course about Orr. It seems that such issues were all discussed in a (probably protracted) “Board-only time”, perhaps in part (also not disclosed in the minutes) without the Governor. We know that 27 February is also when Quigley advised Rennie who advised Willis that something was in the works re Orr’s future. And (although I can’t track it down this minute) if I recall correctly the exit agreement negotiations occurred over the couple of days after 27 February, and were concluded on Monday 3 March.

The story, if true, also goes some way to the mystery of the exit agreement which – we’ve been told – included gag provisions of some sort. When it appeared that the exit had been driven solely from Orr’s side it was very puzzling why the Board agreed to any such restrictions (setting aside the fact that resignation was a matter for which the Minister was responsible for dealing with).

But for the Board – and we must presume that Quigley wouldn’t have been acting without their support – to have presented Orr with a memo documenting behavioural concerns over several years, and explicitly seeking a response, they must have got to the point where, even if they wouldn’t put it in quite so many words, they had lost confidence in the Governor. When things get to that point, exit is a pretty common option (at lower levels, when public servants are told they are going to be put on performance improvement plans it isn’t unheard of them for them to up and resign, saving everyone the pain, and the employee the CV issues, of a dismissal process). But Orr still held a few cards: he was only two years into a second five year term, the Board couldn’t fire him, and (even with serious behavioural concerns) it would not have been easy for the Minister to have fired him (intense scrutiny, political controversy and all). So perhaps he told Quigley “I’ll go, so long as no one tells the truth about what went on”. By then perhaps it seemed cheap at the price to Quigley (bearing in mind, even more mundanely, that Orr’s record was an an empire builder not as a cutter and chopper, adjusting to budgetary restraint and – as the Bank’s 11 June statement notes by then the Board had accepted that much lower budgets were coming).

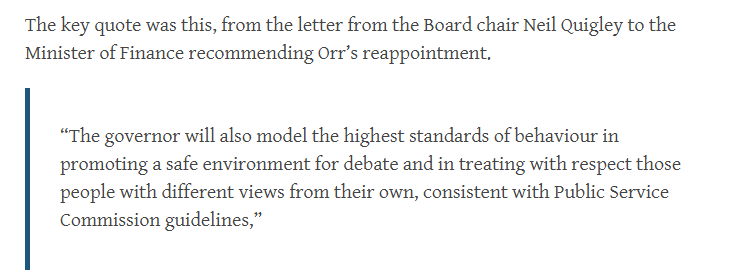

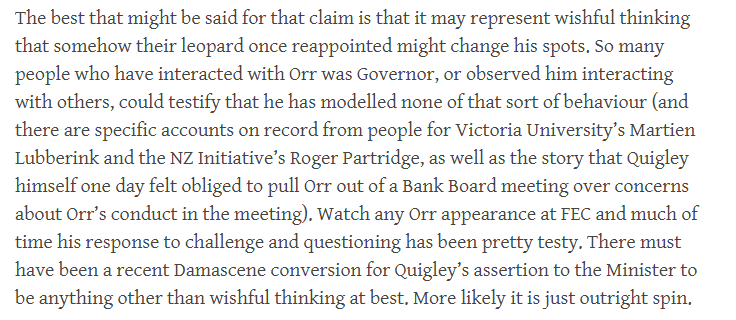

Who knows what items were on that behavioural concerns list, if such there was. Even on the things in the public domain there were so many to choose from over Orr’s time as Governor, let alone all the stories that seep out from those who were there. Why, on the very morning before he’s reported to have completely lost his cool at Treasury, he’d been lying to FEC (again). None of this, sadly, seems very surprising. If there is a surprise it is that the Board had finally – finally – chosen to take a stand. With one exception (new Board member) these board members had all been responsible for recommending Orr’s reappointment in late 2022, when almost all the concerns – well, perhaps not swearing etc at ministers – were already documented. At the time, Quigley signed the recommendation with this

At the time I observed

They must have known then – Quigley more than most (much of the Board was new, but Quigley had been there throughout, chairing the board that first nominated him in 2017) – just how detached from reality that endorsement was. Of course, Robertson will have known too (I’m looking forward to how his book, due out next month, treats Orr).

But, we must be fair, and give the Board some credit for finally acting, possibly under pressure.

What then becomes utterly inexplicable is the decision to lie about what went on.

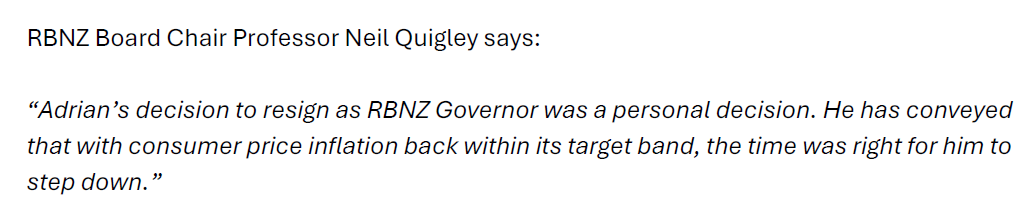

It isn’t just the press release on 5 March which was spin from start to finish, lauding Orr’s contribution, including in “modernising its culture” (losing your cool and swearing?), or Quigley’s statement – released by the Bank – a bit later that afternoon

We were clearly supposed then to believe that a long-serving Governor was, perhaps, tired, and having done his one big job he decided – Cincinnatus-like – to take a step back and return to private life. It seemed unlikely then. It is pretty clearly outrightly false now.

(As previously documented from the 11 June release, the Bank (Hawkesby) ran the same utterly misleading line to staff.)

And if those statements weren’t bad enough, there was the press conference. Even accepting that Quigley was pushed into doing it by the Minister, surely, surely, he must have rehearsed his lines and tested how he was going to answer the inevitable questions he would face?

At the press conference, Quigley started off with “he felt it was just the right time to go” sort of stuff, highlighting all he’d done. Then when he was asked if the Board still had confidence in Adrian he responded – avoiding the specific question

“My relationship with Adrian has been very good, and I have confidence in Adrian. Yes, he and I have been through a lot in my time as board chair of his time as governor, and with the pandemic and everything else, we have very good memories of the challenges that we have confronted.”

I recall noting earlier that interesting juxtaposition (he claimed he still had confidence, avoided answering about the Board), but how can we possibly now believe Quigley was being honest even reporting his own views. You don’t send a written statement of multi-year behavioural concerns by email and ask, by email, for a response when you have confidence in your CEO (a quiet CEO/Chair chat might be a different kettle of fish).

There were then actively misleading answers about the Funding Agreement before we got this

Q: What has been the precipitating factor to what you call this personal decision?

A: I think you have to remember that the job of the Reserve Bank Governor is one where you face unrelenting critique of your actions. You know, no matter what you do, there are near alternatives that other people say that they would have taken. And so there is a time when you think having achieved what you wanted to achieve, that’s That’s enough.

I suppose just possibly he had in mind some “unrelenting critique” that included the Board, but it was clearly a deliberate exercise in deception, all the more so if today’s account is accurate.

It goes on and on (bringing to mind Peter Mahon’s famous line on Air New Zealand) including

Q: Can you just be clear that no, policy, conduct and performance issues are at the center of this resignation?

A: We have issues that we’ve been working through, but there are no issues of that type that are behind this.

You’ll recall that when challenged on some of this after the 11 June release, Quigley first attempted to fob off questions suggesting he wasn’t going to be grilled by a journalist acting like a courtroom lawyer, only to fall back on the excuse of the supposed gag orders (the details of which have never been released). But gag orders do not oblige (or excuse) chairs of powerful government organisations to go out and actively misrepresent what actually was going on. Don’t hold a press conference if you can’t or won’t give straight answers.

So far, we have heard quite a bit about Orr’s conduct. Quigley’s has long been pretty egregious as well, centred on his repeated and deliberate attempts to mislead as regards appointments to the first MPC (summarised again here). My correspondent added some more, on top of the already documented public cover-up and avoidance of scrutiny efforts around the resignation. According to the correspondent, any records of that meeting with Treasury on 21 February were within-scope of at least one of the OIA requests (not mine). It turns out that Treasury staff at the meeting had written up a record of the meeting (which would seem to be a normal thing to do), but that when Quigley learned of this record he went apopolectic (my word, but captures the flavour of my correspondent’s words) – not just internally, but rang Treasury to complain vigorously. It is reported that in meeting some or other OIA request the Bank so heavily redacted that document that an RB comms manager could boast that they’d rendered it useless. [UPDATE 23/7: Rereading my source, this claim is actually about the Treasury record of the meeting of 24 February with the Minister and Treasury.]

On its own, again perhaps not so surprising. Senior public officials often don’t like stuff being written down – discovery risks and all that awkward stuff, scrutiny – but…..the Official Information Act is the law, and there are overriding considerations of public interest. The Bank’s approach (most likely either acquiesced in by the Board chair or driven by him) has been to release absolutely as little as possible, as inconsequential as possible (so note that the 11 June release had quite a few bits and pieces, but most shed no light at all, and almost none of those that might shed light were released at all. OIAs were – and are being – simply ignored.

The final point in my correspondent’s statement related to an issue I wasn’t aware of at all, and isn’t directly related to the Orr departure. The correspondent claims that the Bank is about to move its Auckland office into one of the plusher buildings down near the waterfront (PWC Tower, which seems to boast all sorts of Orr-pleasing green credentials). I have no way of knowing if this is so, but published board minutes certainly reveal that they were planning to shift and suggest that in March negotiations were still ongoing. The suggestion is that the space being leased is “three times” what would be needed for the staff there, the more so after the Funding Agreement cuts. The report from my correspondent is that management – post Orr – suggested reconsidering (optics, job losses, and all that) but that the Board itself refused, and that by the time the final decision was made the Board knew the lower level the new Funding Agreement would be set at. My correspondent seems very confident about all that, but notes that they are not sure of the reasons, reporting only a general sense among Bank people that the Board had wanted fancy spaces for themselves. Staff will speculate, staff may have that one wrong, but it doesn’t sound like a very good look at all. Again, occurring on Quigley’s watch.

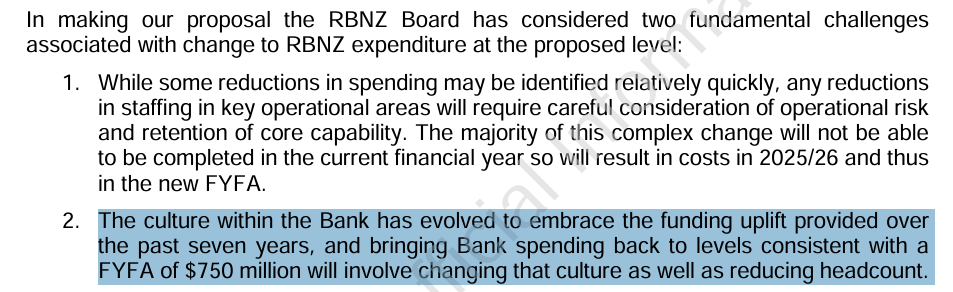

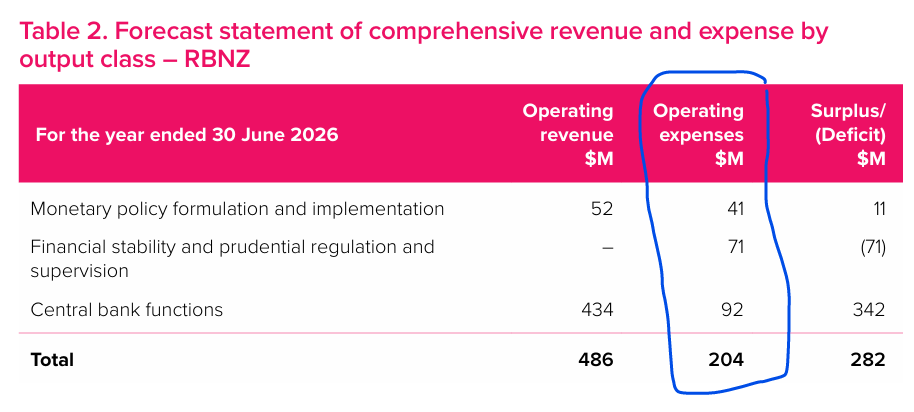

If offence it is, it is certainly one of the lesser ones, but it does point in the direction of the Funding Agreement not actually having been cut to the bone. You’ll recall last week’s post that the Bank’s operating expenses in 2025/26 will be 12 per cent above the level in 2023/24, the last year budgets were set under Labour, and that line about the culture of excess that Quigley had included in his last ditch bid in March to limit the cuts the Minister was going to impose.

This has been a long post. As noted earlier, I have lodged a number of new OIAs, with the aim of trying to verify as much as possible of what is reported here. I expect there will be more obfuscation and outright ignoring of requests, although if so that will be telling in itself.

None of it leaves anyone looking very good (although perhaps it partly redeems the standing, at that late date at least, of the Board members other than Quigley). We have not had straight answers yet from either Quigley or the Minister of Finance (and have heard nothing at all from Orr, which might perhaps be more understandable if he really was close to having been forced out on conduct/behavioural grounds). And OIAs continue to be ignored.

If this were just any junior public servant of course things would be different. There would be no particular public interest in disclosure. But we are talking here about the sudden departure of one of the most powerful and highly paid officials in New Zealand, who had often boasted (mostly not correctly) of how open and transparent he and his institution were. And yet someone who used his office to treat people poorly, in some cases (it seems) abominably, and of course who had such a questionable policy record too – all that (core) inflation, all that economic dislocation, those $11 billion of losses for taxpayers. We deserve some honesty. And it remains almost beyond belief that after all this not only is Neil Quigley still in office, but that he is now leading the search for the nominee for a new Governor. Because his last pick worked out so well?

A month ago, I wrapped up a series of posts on these issues with one posing 41 Questions for the Board, for Quigley, for Willis, for Treasury, and for the temporary Governor Christian Hawkesby. Most remain outstanding.

UPDATE: I hadn’t known there was any accessible footage of Quigley’s 5 March press conference (and some Wilis comments) but here is a link that contains many of his answers. Nothing new beyond what I’ve previously quoted from a written transcript, but fyi.

There are still lots of outstanding questions around the sudden departure of the Reserve Bank Governor, and the handling of those events by the board and the Minister. But, even amid ongoing OIA obstructionism – the Bank simply ignoring the substance of specific requests, in a flagrantly illegal way – some more bits and pieces have emerged.

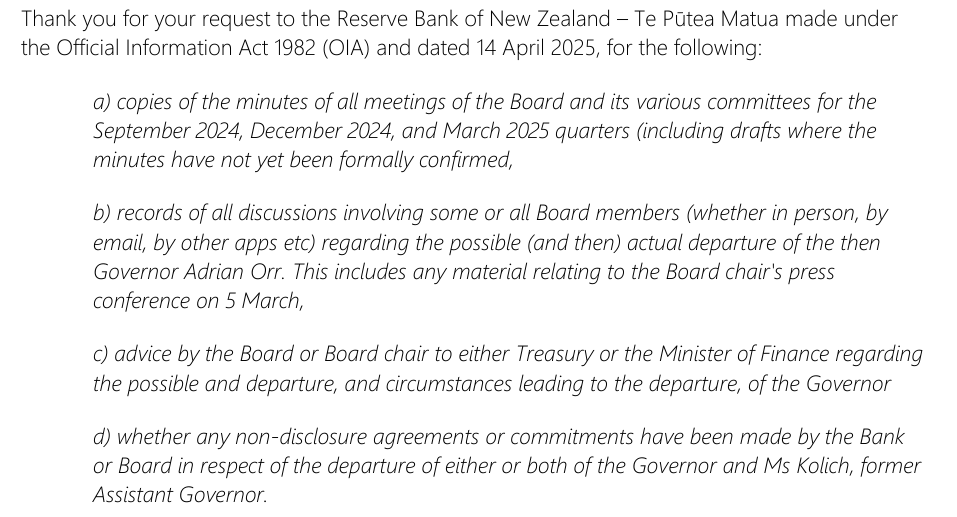

Back in April I lodged these requests

The Bank finally got round to responding on 30 June.

Of those, item a) wasn’t primarily about Orr’s departure (for unrelated reasons I wanted to see how their board committees work). Nonetheless, the response was interesting because although they sent me the committee minutes (with redactions), they didn’t even address the request for the minutes of actual Board meetings. As it happens, the Bank periodically (normally quarterly) releases rather limited and selective minutes of regularly scheduled Board meetings (you can find them here) and I’d lodged the request mostly because by 14 April they hadn’t released any for six months). They’ve since put up more recent ones. The Bank’s usual approach when someone requests something that is already on a website by the time the reply goes out is to point requesters to a link to those documents and then decline the specific request because the document is already publicly available (legitimate grounds for denial). This time, however, there is no mention in the response of the board minutes at all (only a mention that the committee minutes were attached, as they were).

This suggests an (illegal) effort to avoid addressing the specific request. One possible reason might be because it is almost certain that there will have been short-notice board meetings in and immediately around Orr’s resignation, which they don’t want to either acknowledge or disclose the records of. How could it have been otherwise? The Governor tells the board chair he’s thinking of resigning, and the Board does nothing, never meets, never authorises an exit package with gag agreements? Even for an apparently supine board like that of the Reserve Bank it seems very very unlikely. And when the Governor actually resigns – recall it was brought forward at the last minute by several days – there is no short notice Zoom board meeting to discuss what next? Yeah, right. (I’ll come back later to some interesting points in the minutes of the scheduled board meetings).

Another reason to believe that might be the explanation is the Bank’s response to my second item (above). This was it

That is a reference to the belated bulk release (available here), apparently designed to shape how we should think about Orr’s departure. But…..that response to my request by the Bank simply does not address my specific request, because the 11 June release contained precisely nothing about discussions among board members and nothing about the chair’s press conference later on the afternoon of Orr’s resignation (and nothing about any short-notice board meetings). Of course there will have been discussion among board members, and there might be even be some OIA grounds to withhold some of that specifically (in which cases such withholding needs to be justified specifically, item by item), but this response seeks to pretend answers have been provided when in fact the whole issue has been avoided.

Item d) of my request was overtaken by events. I was no longer particularly interested in Kolich’s departure (and the 11 June release suggested it was in train before Orr left), and the 11 June release did tell us there was an NDA with Orr (although we still have no idea what the nature of the gagging provisions were, or why they were imposed or accepted by the Board, or the Minister – you’ll recall from previous posts that a Governor’s resignation is addressed to the Minister not the Board).

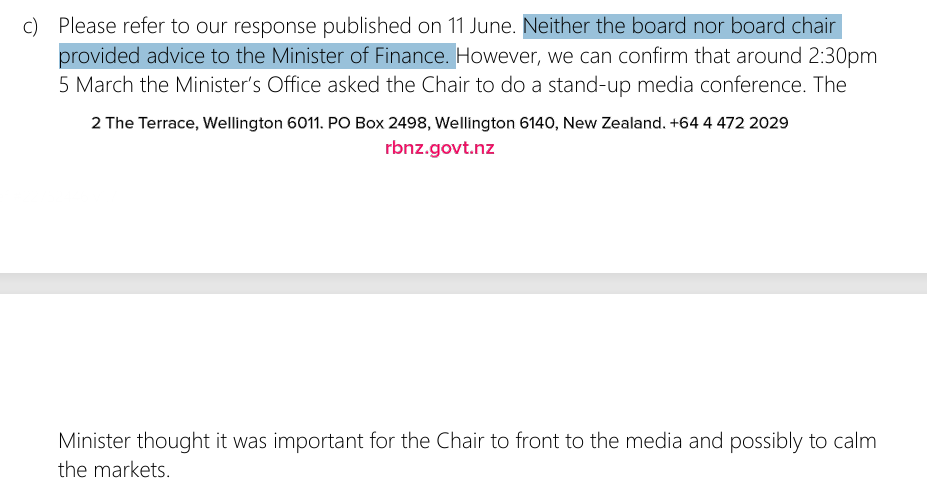

But then there was item c) (above). There is a typo in the request, but the Bank seems to have understood it as intended (about possible and actual departure). This was their response

It is quite extraordinary really. Things had run so far off the rails that the Governor was first talking of resigning then actually planning to resign – partly, the 11 June release tells us, because effective future working relations were so impaired, in the context of the funding agreement disagreements – and neither the Board nor the Board chair initiated any (direct) contact with the Minister of Finance at all; no meetings, no texts, no calls, no written advice, no nothing. If true, and I guess we must assume it is so, it is extraordinary, and something of a dereliction of duty, given that the Board governs the Bank, monitors the Governor etc all on behalf of the Minister, who not only has general responsibility for the Bank but specific responsibility for hiring, firing, and (in this case) receiving a Governor’s resignation. (Other releases show that Quigley had alerted Iain Rennie to what was going on, who’d mentioned it to the Minister). I usually word such requests quite carefully to specifically include “or the minister’s office” and failed to do so this time. I guess it is possible they are hiding behind that and there was contact by Quigley and the Board with senior advisers to the Minister, but on this occasion I doubt that is so because of the final two sentences in that response. It was nice of them to tell me about that but since it was from the Minister, conveyed via her office, it wasn’t specifically within the scope of my request (but one is left wondering why it wasn’t disclosed in the 11 June release).

It just seems astonishing. And not least because of how the Board just seems to assume the freedom to negotiate gag orders with Orr, when a) his resignation had to be made to the Minister not to them, and b) when there would inevitably be intense public questioning and scrutiny of what was going on, and they were proposing even to tie the Minister’s hand without consulting her.

And then the only contact is the ill-judged (as it turned out) request from the Minister’s office for the Board chair to do a press conference. I don’t disagree that both the Board chair and the Minister owed us answers (which we still don’t have) but Quigley is singularly bad at fronting when dealing with challenging questions, and his responses in that press conference ended up raising more questions than answers, at times apparently actively misleading journalists and the public, all while there were no evident market ructions to calm. More questions for the Minister I guess: does she even now know the terms of the gagging agreements entered into? If not, why not? If so, how and why does she defend or justify them?

I noted earlier that the March quarter Board minutes (released on 18 June, conveniently after the 11 June release) had some interesting content (and some telling omissions).

There were records of two meetings. The first was on 27 February (which reports the Board approved minutes of a 14 February special meeting, minutes of which – not disclosed – were clearly within scope of my request). This was the meeting – we were told in the 11 June release – where things crystallised

with the Board taking one view on the future Funding Agreement (bowing to reality) and the Governor refusing to do so. You have to imagine there was quite an extensive and tense discussion. But here is what the Board minutes have to say about discussion of the Funding Agreement and associated negotiations.

That’s right. Precisely nothing. And it is not as if some very sensitive material has been withheld on legitimate OIA grounds (hard to see what now that so much is a) finalised and b) in the public domain). It is just that there is no mention of the Funding Agreement in the 10 pages of minutes of a seven hour meeting.

It is extremely dubious, because it appears like an active effort to mislead readers (of these proactively released documents) and, unless there are secret shadow minutes, a breach of the Public Records Act, which requires public agencies to maintain proper records, including of such consequential meetings and discussions. It seems likely that much of the discussion will have occurred in item 6.2 “Board Only Time”, where nothing is disclosed (or withheld), although even then how plausible is it that all the discussion of the Funding Agreement, where there were major differences, occurred without any other senior management present (CFO or that person’s boss, or the Deputy Governor)? It really is a classic example of minutes theatre: it is good that the Board releases proactively what they do, but this example illustrates again just how selective (and thus dishonest) their approach is.