I’ve been pondering a post on land taxes for some time, but was prompted to jot something down today by a couple of recent pieces, including in today’s Herald by two lecturers in politics at AUT, Nicholas Smith and Zbigniew Dumienski. Sub-editors present their arguments under the headline “Land tax best fit for housing crisis”, and the authors’ own conclusion is only a little more nuanced.

Given the multiple problems stemming from Auckland’s housing crisis, an LVT stands out as the best-rounded of the policy options on the table. Not only would it address house price inflation, it could also result in a more efficient use of land, mitigate urban sprawl, lower the burden on the natural environment and reduce the risk of real estate bubbles; all without undermining the foundations of economic growth.

I’m not a land tax expert, but I’m no longer so convinced.

Which doesn’t mean that I’m inherently unsympathetic to the argument for a land tax. In fact, I once wrote a Treasury paper on overall economic policy direction, that ended up on Bill English’s desk, and which was, with hindsight, rather too readily enthusiastic about a land tax.

In principle, taxing things that are in fixed supply has some theoretical and practical appeal. Collection is pretty easy – every piece of land has an identifiable owner. And whereas if one taxes business profits (say) heavily there will be less investment taking place, taxing land won’t make much difference to how much land there is (it will make some difference because the value of land is partly about work done to it (drainage etc).

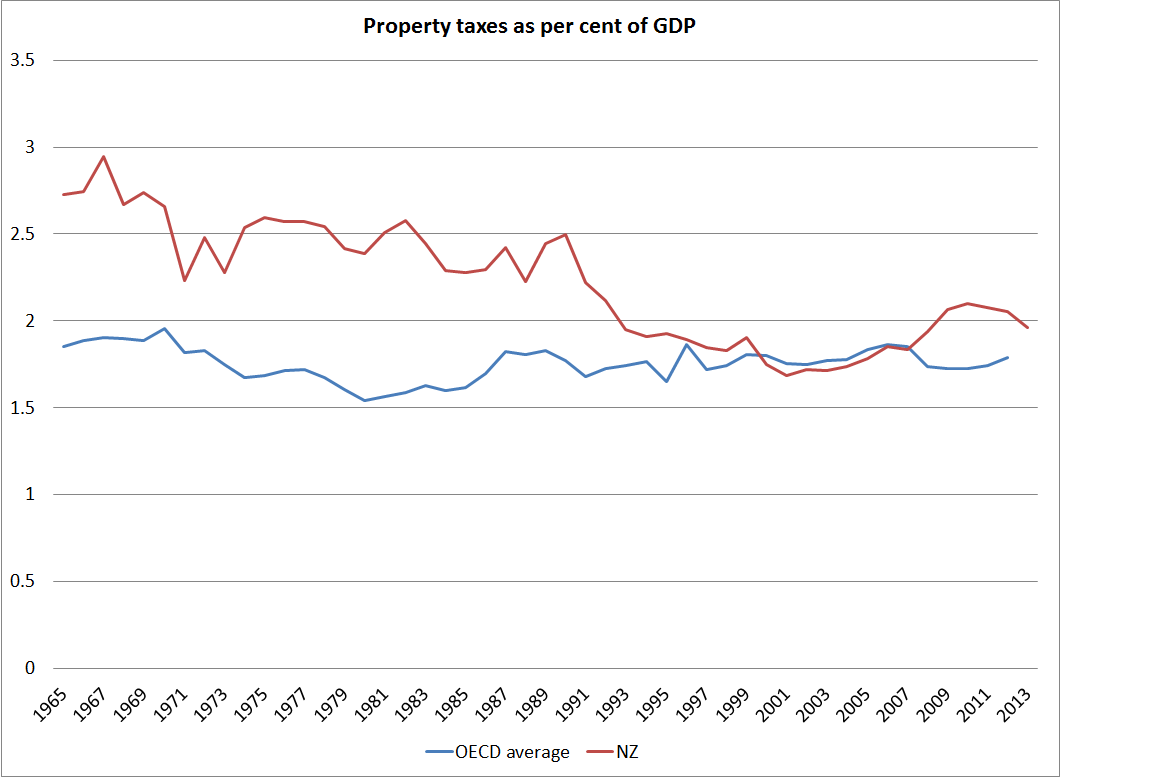

And, of course, as the authors point out we’ve had a land tax previously – it finally disappeared in the early 1990s, by when it apparently applied mainly to land under urban business districts. And we still have, in effect, some partial land taxes: in some areas, local authority rates are levied on the basis of land values, and in many places (especially Auckland) even the capital value rating system have come a lot closer to a land tax as the land share of a typical “house + land” has climbed sharply. And OECD data show the New Zealand property taxes, as a share of GDP, are already a bit above the OECD average.

Had we put a land tax on in 1840, and kept it in place ever since, I’m not sure I’d be arguing for abolition now. But the historical track record of the tax we had was not that good. Apart from anything else, the rules kept changing (and changing), with the base being progressively whittled down. Smith and Dumienski note that “it was arguably an important factor contributing to New Zealand’s once-famed egalitarian character”. I’d be keen to see the evidence for that claim. New Zealand economic historians, at least those I’ve read, don’t seem to have seen the land tax in quite those terms.

Any material change in the tax system involves significant redistributive consequences (or big compensation packages). No doubt there isn’t much public sympathy for “land bankers” in and around our cities (and since these people are mainly profiting from other regulatory distortions, I wouldn’t have much sympathy either). But what, say, about the sheep farmer, in an area where values haven’t been much affected by dairy conversion opportunities?

I’m also not quite sure what sort of tax rate the advocates of a land tax have in mind. People often glibly talk (and I have in the past) of a 1 per cent annual land tax as if this is a pretty small amount. But real risk-free returns are not what they were. New Zealand has probably the highest real interest rates among advanced economies and a long-term real interest rate here (20 year inflation indexed bond) is still just under 2.5 per cent. The comparable US yield when I checked this morning was 1.1 per cent, and that is now quite a common sort of rate internationally. People (especially central bankers) keep talking about interest rates “normalising”, but real interest rates have been trending down now for decades, and no one really knows with any confidence whether the process has ended, let alone whether it will be materially reversed. In this climate, a land tax of anywhere 1 per cent would seem quite incredibly burdensome (in a way that it might not have seemed in New Zealand in the 1990s when real risk-free interest rates were touching 6 per cent). Even if one could make a theoretical case for such an onerous tax, the political economy suggests that it could not be sustained (and would not be expected to be sustained).

Perhaps we could have a rather lower rate of land tax? Perhaps a half or a quarter of a per cent land tax could be politically sustained? But then one is left asking whether it is really all worth it. Bearing in mind that urban land is already taxed, would it make that much difference to the cost of urban land – the issue Smith and Dumienski are driving at – or allow a material gain in economic efficiency from shifting away from more distortionary taxes (eg lowering our high taxes on capital income)? After all, most people now agree that the real issues around urban land prices are not ultimately the tax system, but the regulatory restrictions on land use that central and local governments facilitate. To some small extent, those restrictions seem endogenous to land prices – ie when land prices get sky high (or least rise rapidly) there is pressure to ease the land use restrictions. If so, perhaps a land tax would just allow Councils to keep tighter restrictions in place for longer, undermining any possible efficiency gains from a land tax.

But let’s get back, in conclusion, to the Smith/Dumienski list of benefits. They argue that a land tax would

- address house price inflation,

- result in a more efficient use of land,

- mitigate urban sprawl,

- lower the burden on the natural environment and

- reduce the risk of real estate bubbles;

All without undermining the foundations of economic growth.

What’s not to like? Well, first, in principle a land tax should lower the value of land (ie a one-off shift in the price). But it is not obvious that it will have much impact on either house price cycles, or trend pressures resulting from, say, the interaction of population pressures and land use restrictions. Perhaps the authors have in mind some more sophisticated land tax that would effectively be a capital gains tax, but they don’t suggest so in their article. And as we know, real world capital gains taxes don’t appear to have done much to improve the functioning of housing and urban land markets

Would it result in a more efficient use of land? I suppose that depends on one’s model, but I’d have thought that taxing an asset will result in a more intensive use of that asset, with no necessary presumption that the more intensive use is more efficient. Of course, it might be less inefficient than the alternative possible taxes, but that is a different issue surely?

Relatedly, if land (across the country, not just in cities) is used more intensively, why is there a “lower burden on the natural environment”? Land in its natural state poses no such burden, but if (say) farmers need to use marginal land more intensively, to maximise profit subject to a land tax, I’m not sure why this is an environmental gain.

And I simply don’t see the argument made that to “mitigate urban sprawl” is an appropriate public policy objective. As is well known, urban areas in New Zealand make up a very small proportion of New Zealand’s total land area, and I’d have thought that revealed preference (reflected in prices) suggested that the most valuable use of land on the fringes of cities was typically for housing, rather than for agriculture. “Sprawl” is just the pejorative term for “space” – most people seem to want some (and historically as cities get richer they have gotten less dense) much though the planners might disapprove of their preferences.

To repeat, I’m not in principle opposed to a land tax, but I’m:

- sceptical that it could be imposed, in an efficient way, on an enduring basis

- sceptical that it would allow much effective tax system rebalancing

- and doubtful that, on the scale at which it could be imposed, it would really make much sustained difference to urban land prices, and trends in them over time.

There is no great secret to why New Zealand urban land prices are high. It is largely down to the impact of the central and local government regulatory restrictions on land use. Far better to tackle those at source, and give freedom back to landowners. Competitive market processes could then be expected to produce affordable houses, as they have in much of the United States (which doesn’t mean Mt Eden prices will ever be the same as Invercargill ones). Of course, one can reasonably argue that such reforms themselves might not prove durable, and if reform were totally “open slather” that would probably be true, but whether or not we have a land tax is simply not at the heart of the urban land price issues.

I’d welcome comments and thoughts on this issue, and if (for example) Andrew Coleman, at Otago, felt inclined to add one of his occasional, typically very insightful, comments drawing on his own past work (eg here) in the area I’d be very interested to read it.