Peter Nicholl was the Reserve Bank’s chief economist back when I joined the Bank and later oversaw (from the Bank’s side) the entire overhaul of the Reserve Bank Act in the late 1980s that culminated in the model that governed the Bank for decades (and more recent changes are mostly in the nature of refinements). Peter served as Deputy Governor, on the policy side of the Bank, for a number of years in the 1990s before heading off to be Executive Director (for NZ and a bunch of other countries) at the World Bank. He then became Governor of new central bank of Bosnia. Peter seemed to be in his element there (I’ve heard a few of his stories at times over the years), and after serving as respected Governor there for seven years was a part-time consultant to that central bank for a number of years. He has also been adviser to a number of other central banks. These days, retired in the Waikato, he writes a regular column for a couple of the local papers, and tells me quite a few of them in recent years have touched on Reserve Bank issues.

This is his column for today’s Cambridge News, focusing on the very-evident governance failures for which the entire board is responsible. As he notes, it isn’t written for a geeky economists or Wellington policy nerds but for ordinary heartland readers. It is also focused on the Reserve Bank players rather than the interactions involving the government. He has given me permission to share it.

RBNZ has gone Third World.

I have written two columns previously on stories about what is happening in NZ that I would expect to see in a third world country but not in NZ. As someone who worked in the RBNZ for twenty-two years and was proud of the institution, I never expected to be able to add the RBNZ to my list of NZ third-world stories. In fact, describing what has happened to the governance of the RBNZ over the last few years as third-world is unfair to most third-world countries.

The governance saga came to a dramatic point in March when the Governor, Adrian Orr, suddenly resigned. It hit the headlines again recently when the Chairman of the RBNZ Board, Neil Quigley, also resigned suddenly. But the problems had started building up some years earlier. During the period that Adrian Orr was Governor the staff of the RBNZ rose from 250 to 650. In the early stages, the growth of the public sector was being actively encouraged by the then-Government. But with the change of Government in 2023, the public sector began to be down-sized. Somehow the RBNZ didn’t hear that message-or didn’t think it applied to them. They continued to increase their staff numbers. This is the organization which had been raising interest rates in order to constrain oher people’s expenditure and bring inflation back within its target range. They certainly weren’t saying to people ‘do as we do’. They were saying ‘do as we say’. The spending spree has been largely blamed on Adrian Orr and his empire-building. But the governance question that needs to be asked is where were the Board? Did they agree or were they steam-rolled?

The RBNZ isn’t part of the annual budget cycle. It negotiates a funding agreement with the government every five years. The latest five-yearly negotiations took place early this year. Like Oliver Twist, the RBNZ asked for more – about $ 200 million more. But unlike Oliver Twist, the RBNZ had not been hungry. It was in fact over-weight. The Treasury objected to the request for more and Orr lost his cool and resigned. The Chairman said then that Orr’s sudden departure had nothing to do with the funding negotiations.

It has now become clear that Orr’s departure was caused by the arguments over RBNZ funding and the first arguments were within the RBNZ. Orr and the Board had different views. Despite this, the proposal the RBNZ first put to the government was Orr’s view – a request for $ 200 million more and a further 100 staff. When that was rejected and Orr resigned, I was surprised by how quickly the RBNZ Board was able to come up with a lower request. But it has since been revealed that that was the number the Board thought was appropriate in the first place. The fact that they initially went along with the request for more reflects very poorly on the Board.

The next few months will reveal who will be the next Governor and the next Board Chairman of the RBNZ. They will come into an organization with its reputation in tatters. It is another example of the old adage that good reputations take a long time to gain but can be lost very quickly.

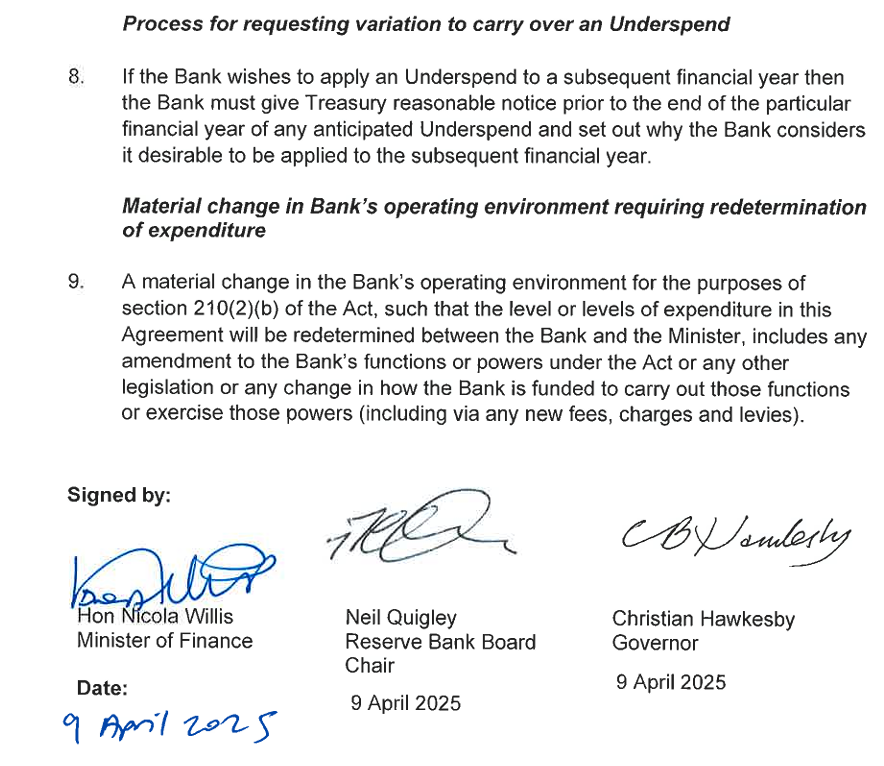

It isn’t impossible that you, readers, are getting tired of the still-unfolding Orr/Quigley/Willis saga. You wouldn’t be alone in that. I have many more intrinsically interesting things to do (spent yesterday writing a review of new academic history of US banking supervision from 1798 to 1980, and am reading a history of little-known sovereign borrowing scandal from the early 19th century) but…..we are still short on answers and on accountability, notably from the Minister of Finance, who may have authorised but certainly enabled the systematic efforts led by Neil Quigley to mislead New Zealanders for months as to what went on. At any point, from and including 5 March (the day Orr’s resignation was announced) she could have a) insisted and b) personally ensured that the truth came out. She didn’t and still hasn’t given us a complete and straight story, or expressed any contrition for anything she was party to in the last six months. Deliberate efforts by, and enabled by, a senior minister to mislead New Zealanders would once, and once brought to light, have been treated as a very serious offence (but then, as I noted here repeatedly, MPs never seemed very bothered when Orr made a mockery of their place in the system and actively misled – or worse – them repeatedly). The rot runs quite deep.

Yesterday saw another OIA response from the Reserve Bank dribble in, and with it one more snippet of information. It exposed, once again, my tendency to look for the least-worst explanation, which has been quite unhelpful in making sense of the mess of recent months.

A couple of weeks ago, the Reserve Bank released to me a Letter of Expectations that the Minister of Finance had sent to the chair of the Bank’s board (Quigley) last year, outlining how the Minister expected that the Board would approach bidding for and negotiations on the next (2025-30) Funding Agreement. The Reserve Bank has a website page where it publishes ministerial letters of expectations. They simply never published this particular letter of expectation on that page, or on the website page gathering together material on the 2025-30 Funding Agreement. Par for the course you might reasonably think, given how obstructive and then slow and partial the Bank has been.

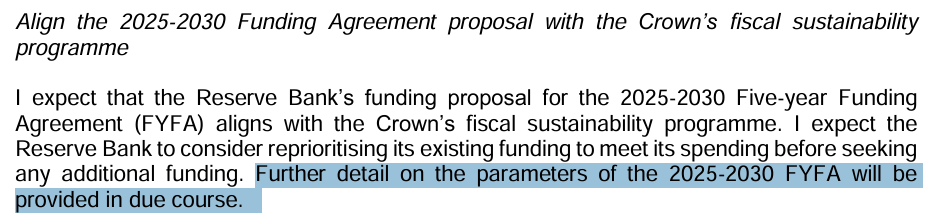

As I noted in that post a couple of weeks ago, the Funding Agreement letter of expectation had made it clear that the Minister was looking for cuts. This was the relevant snippet.

But the version of the letter the Bank was released was undated. The Bank had been quite open about the general 2024 Letter of Expectation, which was dated 3 April 2024. It was fine, but fairly general, noting that further detail relating to the next funding agreement would be coming “in due course”.

I guess I had in mind that perhaps that letter hadn’t been written until much later. After all, the existing Funding Agreement didn’t expire until 30 June 2025 (and when Treasury actually got the Bank’s bid in September 2024, the papers suggest they did nothing with it for months anyway, considering it mainly in the context of this year’s wider government budget)

But what the Bank disclosed to me yesterday was that the funding agreement letter of expectation had also been received by the board chair on 3 April 2024.

And that matters because it was well before the Reserve Bank board made final decisions about the Bank’s 2024/25 budget. Quite possibly, the Governor was already encouraging the Board to agree to a grand spend-up in 2024/25 anyway – on the dubiously legal, but morally outrageous, basis that their total spending over the five years of the 2020-25 Funding Agreement would still be under the total allowed spending in that term (even though a) the agreement and Act specifically referred to individual year limits, b) the limits for each of the last two years had been reset by Grant Robertson just before the 2023 election, and c) there was a wider climate of spending restraint being driven by the Minister of Finance). Perhaps he already planned that such a spend-up would lock in a level of spending/staffing that might make it hard for the Minister to cut much when the new Funding Agreement was finally determined.

But, on 3 April 2024, he had the Minister’s own words for an interpretation that a Funding Agreement bid would be okay if it involved a 7.5 per cent cut relative to the Bank’s budget for 24/25. Wherever that budget happened to be set, apparently. Talk about dangerous incentives….in a system where the Bank sets its own budget, not directly constrained by (eg) parliamentary appropriations…..and the board signed up to this and went along, setting a budget for 24/25 about 23 per cent above what the Robertson Funding Agreement variation had allowed for that year, and then pitching a new Funding Agreement bid just 7.5 per cent below that level (and far above what even Grant Robertson had approved for 24/25). It was a try-on that really amounted to spitting in the face of the Minister, operating in total disregard to the times (let alone to the wellbeing of the staff, if the double or quits gamble went wrong, as eventually it did).

It is breathtaking all round. The Governor and Board attempted to drive a cart and horses through dangerously loose wording. Neither the Treasury nor the Minister of Finance seem to have had the measure of the people they were dealing with, and both were so asleep at the wheel that (a) when the Bank came back with a draft Statement of Performance Expectations in late April 2024 that deliberately left the budget numbers blank, neither followed this up and insisted on straight answers, and b) when the inflated Funding Agreement bid came in a few months later they sat on it for months and did nothing. No one was dismissed, no one was even severely wrapped over the knuckles. A senior political journalist told me last week that in an interview on 30 October the Minister had, unprompted, indicated that she was going to cut Reserve Bank spending……but she’d done absolutely nothing as the board had run rampant for months, including staff numbers still growing markedly. It wouldn’t be until mid-February that things would finally come to a head. As any parent knows the time to deal with bad behaviour is firmly and early, not leaving the offender with the implicit message that Mum and Dad don’t care too much, only to make a fuss belatedly.

Realising that this Funding Agreement letter of expectation had been received as early as 3 April prompted me to dig out the published minutes of Board meetings from the March and June quarter of last year (from which we are told nothing has been withheld) and the Board chair’s response to the (general) 2024 Letter of Expectations (for some mysterious reason known as the Strategic Issues Letter).

Rereading those documents in the light of what we now know, it is interesting how early both the Bank and Treasury had started work on the next Funding Agreement issues (the February 2024 minutes record that a very senior Treasury official – deputy secretary Leilani Frew, now departed – had been named as relationship manager for the funding agrement process, and the board had approved a memo to Treasury “to establish and agree foundational interpretations relating to the funding agreement and the principles underlying our approach to setting our baseline expenditure forecast”). The May Board minutes record Frew and the macro deputy secretary visiting the board and noted that ‘the work towards the next funding agreement, noting that there has been constructive engagement between RBNZ and Treasury an that baseline savings are in the process of being identified” (but presumably neither Frew nor Board, nor their staff, asked the questions that would have revealed the spending spree the Bank was just about to go on with the draft 24/25 budget – the immediately previous item on the Board’s agenda).

You might have supposed that having (a) had two letters of expectation from the (new) Minister of Finance on 3 April, and b) having a deadline to submit to the (new) Minister of Finance, just about to bring down her first government budget in straitened fiscal times, for consultation/comment a draft Statement of Performance Expectations (including budget numbers) by the end of April, that these sets of documents would be the subject of serious discussion by the Board at its April meeting.

But the Board didn’t meet in April 2024 at all. Now, the March minutes record that there was an (unminuted) “workshop” on 23 April “to discuss the next iteration” of the Statement of Performance Expectations and Statement of Intent Refresh, but those minutes also just delegated to the Governor and chair the authority to sign out to MoF for consultation the draft SPE at the end of April. As it happens, the document was signed out by neither, but by one of Orr’s many deputies. Was the Board aware they weren’t planning to tell the Minister about the planned size of the 24/25 Budget? We don’t know, and the (published records) conveniently don’t show. Did they engage with the two letters of expectation then? We don’t know.

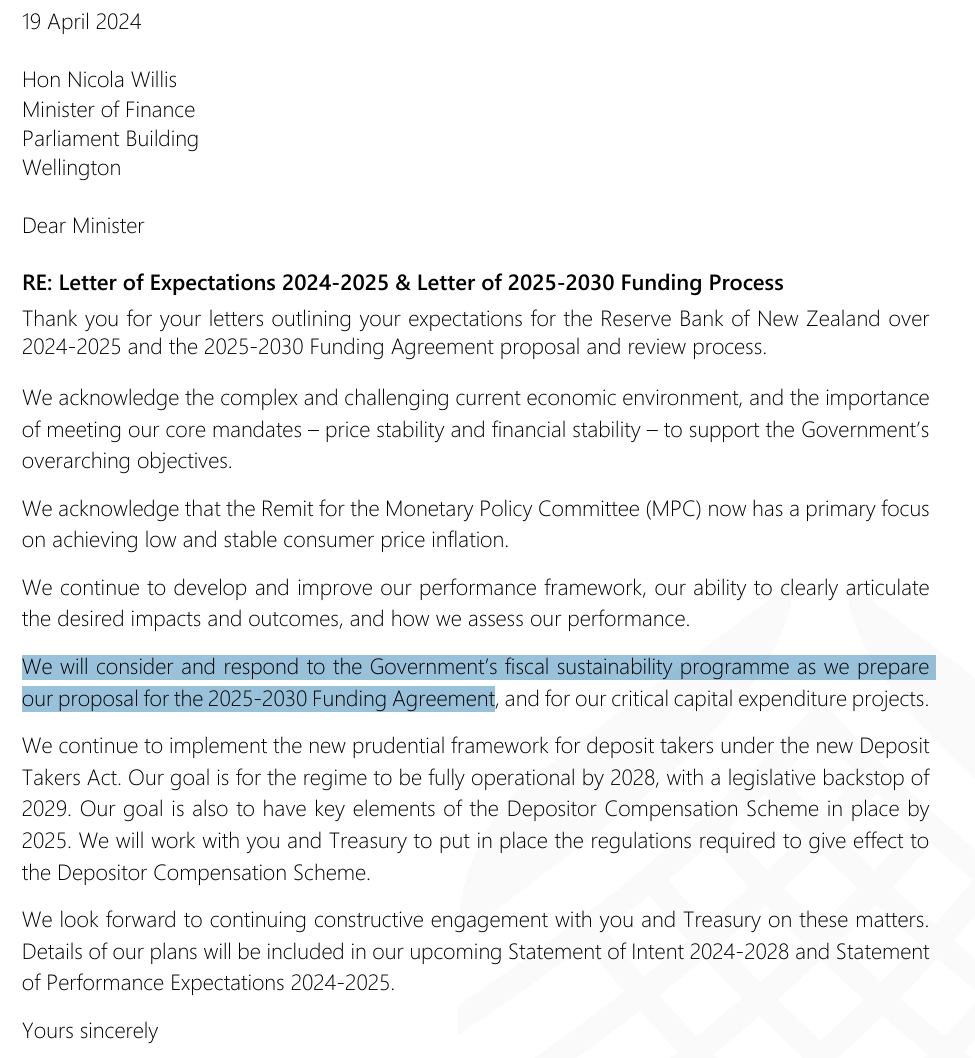

But it seems unlikely, because even if it came up at the 23 April workshop, Quigley had already sent his Strategic Issues Letter back to the Minister on 19 April, purporting to respond to both letters.

Note that he avoided the specifics from the Minister’s letter on the next Funding Agreement and gave only the vaguest indication of a more general approach (“we will consider and respond to”). Surely Treasury (Frew) and the Minister and her advisers should have been put on notice when they got such a vague response? But apparently not, given that they raised no questions/concerns when the budget numbers weren’t included when the draft Statement of Performance Expectations was sent in 10 days later?

There is no suggestion in any of the June quarter minutes from 2024 that the Board ever discussed the Letters of Expectations or thought hard about the implications, or the environment against which they were written. The May minutes do mention the Strategic Issues Letter but only “The Board noted the Strategic Issues Letter”. They seem to have been out on another planet, perhaps led by the nose by Orr, but with no one – Board, Treasury, Minister – providing the sustained vigilance (protecting the public interest and public purse) that was needed. The only Board questions noted in the minutes were looking for assurance that the 24/25 budget was going to be legal – and perhaps Orr’s tame in-house provided some such dubious assurance, as lawyers (in-house and external) are so ready to do for clients – but with not even a hint of a question as to whether such a Funding Agreement blowing budget was right or responsible or was likely to prove sustainable, no stress testing (for example) of what the implications (for people and for the organisation) might be if they did later hit a wall.

It really astonishing (or perhaps not; this is modern NZ) how little serious accountability there is in New Zealand public life. Of course, Orr has gone, but not because of anything he was doing mid-late last year, and Quigley eventually went too – again not because of what he led and did last year but because eventually the post-Orr coverup got a bit embarrassing. I guess too that the relevant Treasury Deputy Secretary has moved on, although there is no hint of that having anything to with being asleep at the (leadership) wheel when the egregious foundations were being laid for the Feb/Mar blowup this year. No board member has been dismissed, or as we understand it even reprimanded, and one was even reappointed this year. The board deputy chair – fully party to last year’s decisions – is holding the fort post-Quigley.

And then there is the Minister of Finance. By far her worst offence was enabling the deliberate deception of New Zealanders for months, when she could have cleared things up at any time she choice (Quigley may have become a nuisance to her, but he was her man, she empowered and enabled him). She still hasn’t been fully straight with New Zealanders. But her role last year – both directly, and in insisting on a more active engaged performance from Treasury – looks pretty culpable. Perhaps if she’d taken a stronger stance from when she first took office, Orr and Quigley would have been reined in much earlier, and the chaos and dishonesty of this year – and damage to her own standing (and the disruption of staff lives) – might have been avoided (many of us were probably glad to see Orr gone in the abstract, but…..no one wanted this).

Remarkably, one other snippet in the May 2024 board minutes is a brief note “the Board discussed the chair’s first meeting with the Minister of Finance”. The government had been sworn in on 27 November 2023, the Minister had been on record with her concerns about Orr personally, and Bank bloat, she’d even promised an independent review of monetary policy. She knew the Funding Agreement had a year to run, but was insisting on immediate cuts elsewhere. It was hardly a quiet and easy corner of her domains and yet she seems not to have bothered meeting with the board chair – her agent, and board wielded the power on prudential policy, where she also had concerns – for months after taking office. You can only shake your head and wonder what she was thinking, and why she made so little effort for so long to use the tools – formal and informal – at her disposal.

I had an OIA response yesterday from the Reserve Bank. There is more obstructionism, so a letter will be going off to the Ombudsman this morning, but there was also some interesting information released.

A while ago the Bank’s Board started publishing proactively minutes (carefully crafted ones) of its meetings. It seemed like (and was) a welcome (if limited) initiative, including because it minimised the number of OIA requests they’d need to deal with. But they leave out a lot, and it also only slowly became clear (to me anyway) that they were only releasing minutes of what they described as the regularly scheduled meetings (more or less monthly). The minutes of the February and March Board meetings included these

Of those this year, only the 27 February meeting was a regularly scheduled one (you can read the minutes of that meeting on their website, although almost all the interesting stuff isn’t included (there is nothing about the Funding Agreement or about the Governor – to be clear, not redacted or withheld on OIA grounds, simply not included in the minutes, despite the Public Records Act). Similarly at the full meeting in late March there is no discussion or debrief on the resignation of Orr, or of communications around it, or on approaches to the various OIAs they had already received. Yeah right.

Anyway I asked for the minutes of the other meetings, and received them (in full) yesterday. There are no redactions. The 5/6 March, 10 March and 13 March ones were done by email circular confirming a) Orr’s exit agreement and b) aspects of the revised Funding Agreement proposal. The meeting of the 18th dealt with the appointment of a temporary Governor, where there appears to have been substantive discussion including on expectations of such a person, but a decision that the only person they would seek an expression of interest from would be Hawkesby.

The one that caught my eye though, and the reason for this post, was the minutes of the 14 February special Board meeting. It was a virtual meeting attended by all board members, but with no other senior management present, just a staff notetaker. Here is the substance of the minutes (not forgetting the opening prayers)

Which seems like a rather important, and deliberate, omission from the carefully chosen set of documents the Bank released on 11 June, when they were still trying to divert us from what actually happened.

What they had released included the following.

From an Orr email of 5 Feb (to senior management, cc’ed to Quigley and Finlay). (I hadn’t previously noticed the rather surprising final bracketed observation – a Governor whose MPC was charged with keeping inflation near 2 per cent worries that inflation could average 3-5 per cent per annum over five years)

And from a long email from Orr to the Board on the morning of the special Board meeting (but before it)

And then an email exchange between Orr and Quigley after the board meeting. This is from Quigley

To which Orr responds with a “Yep all good”.

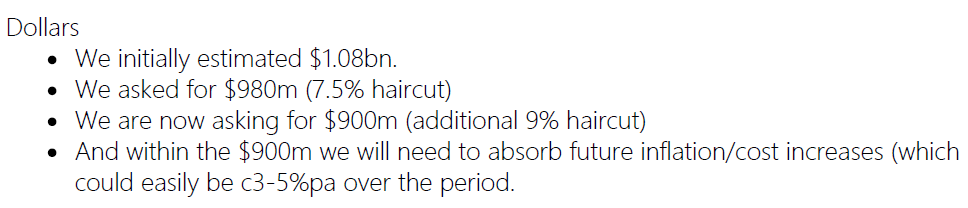

But what they didn’t release was the bit in the middle, which makes the timeline a bit clearer. The Bank had submitted its original Funding Agreement bid back in September, unanimously approved by the Board. This was the egregious one (seeking $981 million over five years), presented as offering savings of 7.5 per cent, but in fact involving materially higher future spending than the Funding Agreement covering the period to 30 June 2025 (variations approved by Grant Robertson had allowed). There is no sign in the minutes of December quarter Board meetings that they’d had any serious blowback (or feedback at all) and the only mention of the Funding Agreement is a discussion of the ‘nature and structure” of the next Funding Agreement when a couple of senior Treasury officials came for a regular visit.

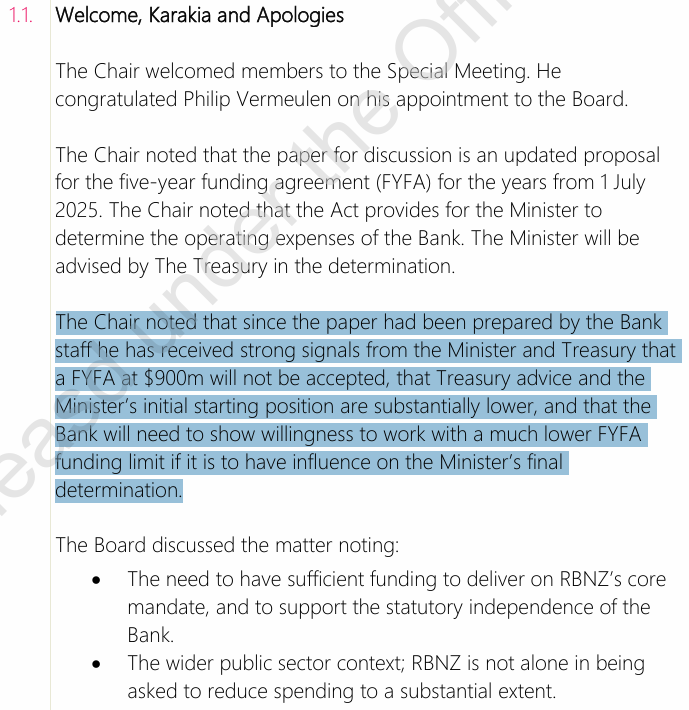

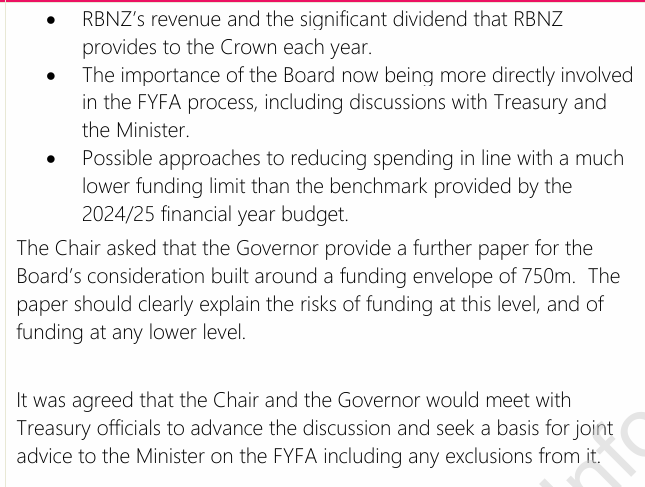

The (still) missing bit is what initially prompted the Bank to propose to revise down its bid. That plan was the paper in front of the Board at the 14 February meeting, in which it appears to have been proposed to lower the bid from $981 million to $900 million. Perhaps there was some initial Treasury pushback, but it cannot have been too strong or clear, because note the chairman’s introductory comments (emphasis added).

The Chair noted that since the paper had been prepared by the Bank staff he has received strong signals from the Minister and Treasury that a FYFA at $900m will not be accepted, that Treasury advice and the Minister’s initial starting position are substantially lower, and that the Bank will need to show willingness to work with a much lower FYFA funding limit if it is to have influence on the Minister’s final determination.

“Strong signals” and from both the Minister herself and from Treasury, that what was probably intended as a compromise offer would come nowhere near meeting the mark. (Which is to the credit of the Minister and Treasury, but why weren’t those messages being sent back almost as soon as the initial dropped into the Secretary to the Treasury’s inbox five months earlier? And why has none of this previously been disclosed?)

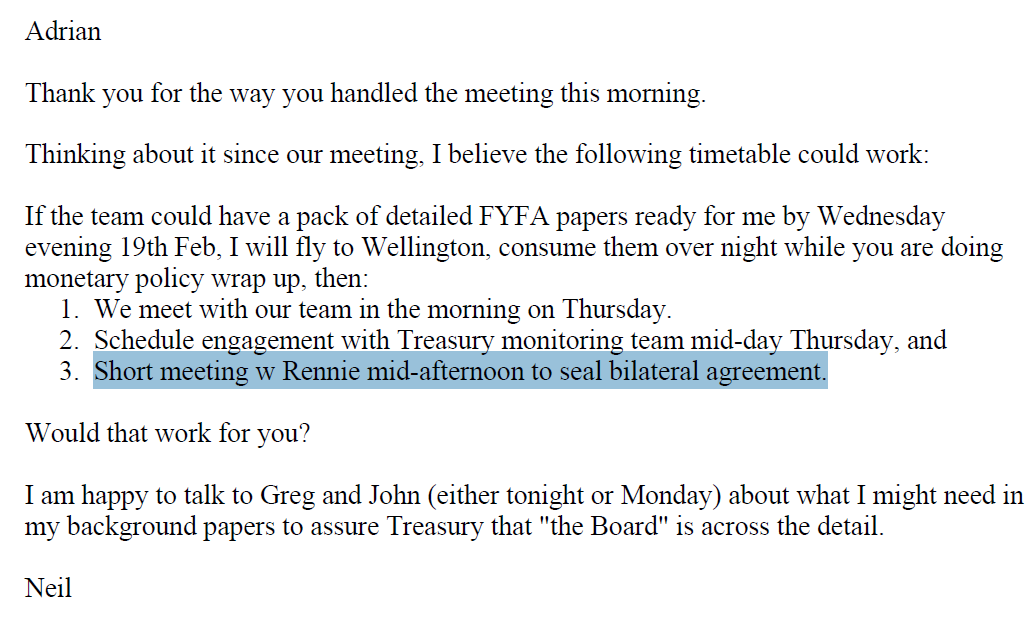

The Board’s response seems, belatedly, quite realistic (noting “RBNZ is not alone in being asked to reduce spending to a substantial extent”) but then you have to wonder how Quigley ever envisaged later that day that they would be able to “seal bilateral agreement” with Rennie at a meeting the following week. Did Orr not disclose to either Quigley or the rest of the board at the meeting on the 14th just how strongly opposed he was to having spending limits pulled back to around the levels in the expiring Funding Agreement? Did it only become clear when Orr lost his cool – and refused to apologise – at that meeting he and Quigley had with mid-level Treasury staffers on the 20th? In the end it wasn’t his call – the Funding Agreement is between the Board and the Minister, and the chief executive is responsible for working within it – but if he hadn’t put his cards on the table, in a calm and rational manner, at a special board meeting on the issue, it is hardly to his credit. And if the goal of the 20 February meeting had really been “joint advice” to the Minister, it is even more reason for Quigley to have regarded Orr’s behaviour as so unacceptable (and utterly counterproductive).

Does any of this greatly matter at this point? Probably not, but it does fill in a few more blanks (and prompt another OIA or two).

UPDATE 5/9 . There must have been quite serious and perhaps robust debate and exploration of issues/options, since the meeting ran for 105 minutes with no staff. Unsurprisingly the minutes don’t record the tenor of the debate but note that that same evening Quigley thanked Orr for the way he’d handled the meeting, so this one can’t have been explosive.

There have been numerous OIA requests around events leading up to and surrounding the (pretty clearly) coerced exit of Adrian Orr on 5 March. The Reserve Bank in particular continues to keep on with a fair amount of delaying and stonewalling, clearly resistant to the idea that the public has any real right to know what happened, in a case involving one of the most powerful officials in New Zealand, with a track record of poor personal behaviour and very costly policy choices. Judging from a couple of their recent responses to me and one I noticed to someone else via fyi.org they seem to be working towards a date around 18 September (at least three requests are extended to that date), perhaps around the expected timing of any final Ombudsman determination on the various appeals already in train. By then it will be well over six months since Orr resigned, and that it is with the Ombudsman apparently taking this matter seriously. It is pretty bad, in both appearances and substance, and had the Bank and the Minister of Finance been at all serious about transparency and accountability we could have had a full reckoning within a couple of weeks of Orr’s departure, and then moved on towards rebuilding the institution and with it its credibility and authority (eg that “social licence” Orr used to like to bang on about).

And yet, various responses do come in. While I was away last week there were responses – each with some information – from the Reserve Bank itself, from The Treasury, and from the Minister of Finance. In their different ways, whether by acts of commission or omission, they do not show any of those three parties in a good light.

You’ll recall that it was the Reserve Bank’s egregious Funding Agreement bid, and the resistance to it by the Minister of Finance and Treasury, that finally sent Orr over the top, resulting in behavioural breakdowns (described in the Herald the other day, with apparent extreme understatement, as “including at least one indecorous outburst”) that led to his coerced resignation.

I’ve been trying for months to get to the bottom of this; both how they ever made such an egregious bid in the first place, and how Treasury and the Minister did so little for so long, such that this only came to a head in late February (the bid having been submitted in September).

We know:

that in her letter of expectation to the Bank’s Board in April 2024 the Minister set out her expectations about future spending. Against the backdrop of what was happening to other agencies most people would read this as suggesting that the Bank could expect less authorised spending under the new Funding Agreement than under the old one.

The Reserve Bank nonetheless went ahead and set its own 24/25 budget (which it could, in law, do) 23 per cent above the amount of operating spending authorised for that year by Grant Robertson in a variation to the previous Funding Agreement made just prior to the 2023 election.

The Reserve Bank did not tell the Minister of Finance this, by the simple device that when – as the law requires – they gave her the opportunity to comment on their 24/25 draft Statement of Performance Expectations, they simply left out the planned budget amount. (It was filled in in the final published version but…..who reads such things).

The Treasury seems not to have raised any concern about this egregious 24/25 budget – it isn’t even clear they asked about it or were aware of it at any time during 2024 – and certainly did not alert the Minister to what had happened.

The Reserve Bank (and note that this was the Board, unanimously, and not just the Governor) in September 2024 lodged a bid for the 2025-30 Funding Agreement that was quite explicitly set on the basis of involving a level of future operating spending 7.5 per cent below their own (grossly inflated) 24/25 budget.

Numbers consistent with this bid found their way into the HYEFU expense tables in December last year (Treasury telling me that they simply took the numbers the Bank gave them).

Treasury appears not to have engaged seriously with the Funding Agreement bid until February this year.

It was pretty much beyond comprehension all round. How could the Reserve Bank Board have the gall to have a) set such an initial budget inconsistent with the recently updated funding agreement and b) then used that as the base for a bid for such a higher level of resources (incidentally going on to commit to large and expensive new office space in Auckland without any certainty as to their future approved spending)? How could the Minister of Finance, who had very evidently been no fan of Orr, have let all this happen (where was her suspicion/curiosity, where was that of her advisers)? And how could The Treasury, supposedly the guardians of the public purse and specifically charged with monitoring the Bank (and Board minutes show Treasury DCEs turning up for chats at Board meetings), have been so oblivious to what was going on (would this have been an acceptable standard in any other government department monitoring its Crown entities)?

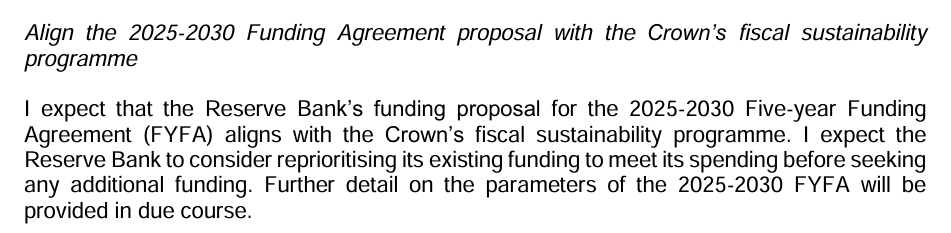

The Bank has been quite obstructive in releasing the relevant material (Treasury, more cooperative, reveals that it really had none) and are still refusing to release the final Funding Agreement bid that went to the Bank’s Board (I really only want it to check whether the Board exercised any discipline on management excess but the minutes suggest not). However, in consultation with Treasury, they have now released a letter of expectation sent by the Minister of Finance to the Board chair headed “Expectations for the 2025-30 Funding Agreement proposal and review process”.

The version they released has no date on it (I asked yesterday, but perhaps they’ll take another 20 working days to reply), but it must have been after the April 2024 general letter of expectation (see above), although perhaps not much after it.

[UPDATE 8/9: The Bank has confirmed to me today that the Board chair received the funding agreement letter of expectation from the Minister of Finance on 3 April 2024.]

If you were dealing with honourable people, it would be a perfectly reasonable letter.

The Minister outlines the general fiscal context:

In pretty much any core government agency the budget for 24/25 would have been the appropriations made by Parliament for that department for that year. The Reserve Bank was different, because it had a five year Funding Agreement, in which approved operational spending for each individual year was specified. The Minister (and Treasury, as drafters of the letter) should still have been safe because you’d surely be able to count on the Bank having set a 24/25 operating expenses budget very much in line with the limits in that previous Funding Agreement for 24/25?

With decent people, but not it appears with the Reserve Bank Board (Quigley, Orr, and the rest). They simply set themselves a budget for 24/25 that bore no relationship at all to what they’d previously been allowed to spend for that year, and then took the Minister at her (literal) word and put in a bid 7.5% lower than that grossly inflated budget. And thus, per the covering Board paper dated 12 August 2024, Bank management (in this case, two of the – very many – deputy chief executives, Greg Smith and Simone Robbers) offer this assurance to the Board

And on the letter of the Minister’s request, it was indeed so. But it was fundamentally dishonest and any half-alert board members (including, but not limited to, Quigley and Orr) must have known that. It is almost inexcusable that any of the Board members involved – both in setting the 24/25 budget itself, and playing fast and loose with the clear intent of the Minister’s letter, in turn leading to the massive dislocation to the organisation and its staff this year – are still in office (driving the determination of the nominee to be the next Governor).

These are the guilty men and women who are still in office, drawing (incidentally) the highest board fees for any non-commercial government agency in New Zealand:

Nei Quigley (who, for reasons apparent to no one else, the Minister continues to express confidence in)

Rodger Finlay, the deputy chair

Jeremy Banks

Susan Paterson

Byron Pepper

Meanwhile, Treasury seems to have been asleep at the wheel, and doing a particularly poor job in pro-active advice to the Minister, in drafting things in a way that ethically challenged people could not drive a cart and horses through, and in undertaking constant and reasonable challenge and scrutiny of the Bank. And the Minister and her team hardly emerge looking good, when they been clear all along that they’d had doubts about Orr.

Where, you might also wonder, were the Opposition and FEC? But the primary responsibility rested with the Board, the Treasury, and the Minister. And if we can’t count on more honest and straightforward behaviour from those charged with monetary stability and the regulation of our financial system, or more effective scrutiny from those responsible for safeguarding the public purse, things are even further gone than this pessimist had come to fear. Mistakes will happen, but then the question is whether those in a position actually take them seriously and do something. There is no sign Nicola Willis has done that (after all, all those board members are still in office, and although their bid was cut back there were no consequences for them for the havoc they wreaked or the ethically-challenged try-on).

The second part of this post skips forward some months. But before we get to that take note of what the Bank and Quigley had done in the earlier section, hardly (one would have thought) conducive to good and trustworthy relationships going forward between the Bank and Treasury, if Treasury now realises they have to dot every i and cross every t, and check every single document that the Bank is not attempting to pull a fast one).

You might remember that a month or so ago I reported what an apparently well-informed insider had told me about what really happened around the Orr departure. Pretty much all of that story has checked out as things unfolded. One element of the story was that Neil Quigley had gone ballistic when he learned that Treasury had kept a fairly full file note of a critical meeting held on 24 February between the Minister of Finance, the Reserve Bank, and the Treasury. So I lodged an OIA request with The Treasury, and this was the response

Personally, having taken many file notes of meetings with Ministers of Finance and Treasury earlier in my career, neither the fact of the file note nor its contents seemed particularly surprising or inappropriate. Major issues (not just the funding agreement but bank regulatory ones) were being discussed, the language is not inflammatory – although the Orr walkout (itself described in muted terms) certainly was.

The fault here seems (and not surprisingly) all with Quigley. As ever with him, there is never a sense of why the Official Information Act exists, or whose interests it is supposed to serve. Instead, we get implied threats of (a) “this will require the full force of RBNZ legal advice to be brought to bear on it”, and b) the suggestion that release would “immediately destroy the goodwill between Treasury and the Bank that I have tried to create over the past few years”. You might wonder how Quigley is feeling now that the full file note has been released, but even set that to one side……goodwill????? This was the same Board chair whose chief executive had behaved so egregiously in a meeting with Treasury that Quigley had felt compelled to provide a written apology, and whose Governor (in that 24 Feb meeting) had (in muted Treasury language) “expressed frustration at the relationship between the RBNZ and the Treasury”. And this was the Board chair who had pulled the wool over Treasury’s eyes by agreeing to a budget for 24/25 quite out of step either (and more importantly) with his own Funding Agreement, or with the spirit of government fiscal policy last year, and then used that abuse as the base for a bid for a big increase in authorised spending for the coming years.

Quigley then puts one of the Bank’s attack dogs, their General Counsel, onto the issue and we have his crucial email as well

So, the Bank’s General Counsel tries to threaten Treasury that the Bank would not in future be willing to hold meetings with Treasury and the Minister of Finance on its future funding? Yeah right, but it is an attempt to intimidate Treasury.

And then, of course, there is that second paragraph. Which goes to the whole point, that the Reserve Bank’s Board appears to have engaged in attempts to make end runs around any serious public scrutiny, including via the OIA, by doing sweet-heart deals with Orr, the terms of which they also refuse to disclose. Fortunately, sweetheart deals done by Quigley et al don’t bind The Treasury, without whom it seems we would have no idea what went on at that critical meeting, when things were so bad that within 24 hours the exit process was getting underway.

Quigley repeatedly displays no regard for the public interest, and any relationship to the truth or straightforwardness on Reserve Bank matters seems entirely incidental (ie whether or not it serves his ends of the moment – see the repeated active misleading of the public, both on 5 March and since).

And, just briefly, one final OIA, this time from Willis herself.

My informant had told me that on the afternoon of 5 March there had been heavy pressure from the Minister’s office for the board chair (Quigley) to do a press conference on the resignation. One of the Bank’s earlier OIAs had also mentioned such approaches. The Minister’s response confirms that there were two conversations that afternoon involving her Senior Press Secretary and the Bank’s communications head to that end, and it also releases the draft press release and Bank comms plan that Neil Quigley had provided to the Minister’s office late on the morning of 5 March which included this: “Recommended media response plan for if [ “if”???? Really?] we get questions: No further comment”. The ill-fated press conference, at which Quigley did so poorly and actively misled the public, was clearly Willis’s initiative.

But that was not my main interest. I also asked for copies of “any material relating to exit conditions for Orr (process or substance)”. The Minister’s response was “No information about the Reserve Bank Governor’s exit conditions is held”. Which really is inexcusable. As a reminder, the Minister (and Cabinet) appoints the Governor, the Minister (and Cabinet) are the only ones who can dismiss the Governor, and the Governor’s resignation has to submitted to her specifically. The Minister is also responsible for the Board, and appoints – and can dismiss at will – the Board chair, and is the only person in the entire mix with any degree of direct public accountability. And yet we are expected to believe she is so incurious as not to enquire at all as to what sort of cover-up arrangements Quigley (and the “senior counsel” both sides engaged) was cooking up with Orr, as the basis for his departure, or even at what cost. And when a key precipitating event was a meeting she was part of?

I’m not sure I really believe it – not “holding material” is likely to be different from no phone calls were made, directly or indirectly, (and there is set of texts involving Iain Rennie on this topic that are still being withheld in full by Willis) – but if it is true it reflects very poorly on her as a steward of the public interest.

(And that is even granting that the wider public interest was almost certainly served by Orr’s departure, a couple of years after he would already have gone had the previous government not, inexplicably, reappointed him.)

All the interest in the Orr-departure story – the background, and the subsequent and ongoing efforts to mislead the public by the Board and the temporary Governor – seems to now centre on the Ombudsman. Various people, including me, have appealed the Bank’s OIA obstructionism on specific requests and the Ombudsman seems to be pursuing the issue reasonably expeditiously. I received a draft of a provisional opinion the other day for comment (which I have now provided extensive comments on) but I’m guessing it might be a couple of weeks before we get a final decision. I’m going to be away for a while so I don’t expect to write anything more after this post for at least a couple of weeks.

For the record, the Herald has an article today on the Reserve Bank staff cuts. Most of it is ground covered in my post last Friday. But the one bit that caught my eye was this

To which there are so many possible thoughts in response:

Surely no serious external observer ever thought they needed what they had bid for to do their statutory duties effectively,

But if the Board is now confident that everything can be done with 20 per cent fewer staff than they had in January, why did they ever bid for so much more money? (And it was the Board’s bid, perhaps championed by the then Governor but he was their agent and they had responsibility for governance, budgets etc),

And if “no work programmes have been cut” [“out altogether” appears from context to be the intended interpretation] a) what were all those people previously doing? and b) given all the non-core stuff the Bank got into under Orr, why on earth not?

It seems like further evidence that the modest cuts Willis imposed relative to what Grant Robertson had allowed the Bank to spend did not go anywhere near deep enough.

And it remains extraordinary that none of the Board members has had the decency to resign and that the Minister continues to express confidence in the chair, whose signature had been on that egregious bid late last year for so much more money, in which he and the Governor stated that that increased funding was what was appropriate “to deliver on our mandate and agreed outcomes”.

So many puzzles and so few explanations when it comes to explaining the last 10 months or so of the Orr tenure, that all ended so ignominiously on 5 March, coverups and all.

But another OIA response came in from The Treasury yesterday (having taken the best part of two months to provide two pages of information (and not withhold or redact anything)). Another of the puzzles around that final year or so is why Treasury appears to have been doing its monitoring role of the Bank so poorly (and this is a formal monitoring role, for which resources are formally allocated, established under the overhauled Reserve Bank Act in 2021).

This had been the request, lodged on 16 June

Some of this had already been overtaken by events because the Reserve Bank had already released to me Treasury’s comments on the draft 2024/25 Statement of Performance Expectations (SPE), and then had released the draft SPE and covering note the Bank had sent to the Minister of Finance.

The mystery, you will recall, was that the Bank had chosen to spend about 23 per cent more in 24/25 on matters covered by its Funding Agreement than the variation approved by Grant Robertson just before the 2023 election had allowed. Surely, it seemed, Treasury and the Minister of Finance would have pushed back strongly on this? But it emerged – all documented in previous posts – that the Bank simply chose to leave out the planned budget numbers from the draft SPE they consulted the Minister on. She simply wasn’t told about this planned excess, and Treasury had not flagged any concerns to her (they’d noted that the draft SPE didn’t have the budget figures in, but raised no particular concerns and simply noted that the numbers would have to be in the final version). They were, but there was no particular reason for the Minister or her office to look closely at the final version because they’d not been alerted to any particular areas of concern, or requested any major changes to the draft. As I’ve noted before, perhaps the Minister and her advisers should have been more suspicious – Willis had scarcely been on record as an Orr fan – but the real fault seemed to lie with Treasury. They are, after all, supposd to be the guardians of the public purse.

So what new do we learn from yesterday’s release? Mostly, it is about gaps – and not in what they released, but in what work never seems to have been done.

There were four limbs to my request.

On the first, it seems that there was no additional analysis or advice internally, and certainly nothing documented outlining any concerns as to what the Bank might be up to or suggesting (say) that they should insist that the Minister was alerted to the planned budget for 24/25. There is no sign in any of the material that Treasury was even aware of the scale of the planned spending blow-out, let alone suspicious of how such a blowout might be used to try and leverage more resources in the forthcoming Funding Agreement bid.

The third limb related to something I’d spotted in this year’s government Budget documents.

A not inconsiderable chunk of the “savings” in this year’s Budget ($144 million in fact) was this item. We were told, reasonably enough, that the figures now included in the 2025 government Budget reflected the new Funding Agreement that had been signed and released in mid-April. But why had figures so much higher ever been included by Treasury in the HYEFU last year? After all, much higher numbers had no warrant in any document any minister had ever seen (eg the draft SPE – see above) or signed (eg the Funding Agreement then still in place covering the period to 24/25). Why, in an environment of fiscal stringency, had Treasury included levels of Reserve Bank spending for the next few years far higher than anything authorised from the centre to that point?

The answer, it appears, is that no one bothered to look or check or think. Treasury told me that “there is no material in scope of the third part of your request”. And went on to tell me that “we note that the RBNZ provides the Treasury with operating expenditure forecasts which are used in the Treasury’s Half Year Economic and Fiscal Update (HYEFU)”. Which seems almost beyond belief. The Bank isn’t a tiny entity (say the Walking Access Commission), but one spending a couple of hundred million dollars a year, and one which had been increasing its spending substantially, and yet Treasury staff simply took whatever the Bank told them it planned to spend for the following few years and stuck it in the formal fiscal forecasts without apparently raising any questions at all. Not exactly a fearsome (or effective) watchdog.

One reason I’d asked about those HYEFU numbers is because I knew that the Bank had lodged its egregious bid for the following five years with the (acting) Secretary to the Treasury on 13 September. I’d assumed that between then and when the HYEFU fiscal numbers were finalised (27 November) somebody at Treasury would have (a) looked even a little closely at the Funding Agreement bid, and b) raised some red flags about a bid that used as a baseline spending levels so far ABOVE what was allowed in the still-current Funding Agreement, and c) perhaps (optimistically) gone back and looked at how the 24/25 budget had been set relative to those Funding Agreement limits. They might even have alerted the Minister.

And that was the gist of the second limb of my request. In fact, it appears that none of this happened. Treasury never actually responds directly to that bit of the request but (a) does not say it is withholding anything, and b) notes that two documents are in scope and soon to be released (as part of the long-delayed pro-active release of papers relating to the 2025 Budget). The first of those is “T2025/3027 Aide Memoire: Preliminary assessment of the Reserve Bank of New Zealand’s funding proposal for the 2025-30 Five Year Funding Agreement”, and is dated 13 February. That appears to be the first time anyone at The Treasury had put anything in writing on an egregious funding bid they’d received five months earlier (from an agency with a chief executive who was well known for his aggression etc). It seems almost unbelievable, but there it is.

I am loathe to accuse Treasury officials of playing fast and loose with the Official Information Act, but in this case it is hard to believe I have been given a straight answer. Why? Because we have the written words of the former Governor to his senior leadership team, cc’ed to the Board chair and deputy chair. This, from 5 February, is from the Bank’s 11 June release

You don’t tell people to “cease and desist negotiating with various Treasury Officials” if there had been no discussions and negotiations. And you don’t pull down your initial bid (see second to last line) if there’d been no prior reaction from Treasury or the Minister, and it is hard to believe that Treasury had put nothing at all in writing prior to then (and had not let the Minister know there was a looming issue).

But I guess it is plausible that no one much at Treasury had turned their minds to Funding Agreement issues for months after receiving the bid. Which doesn’t reflect well on them at all.

The fourth limb of my request covered any material of substance relating to Funding Agreement negotiations from 1 December until the date the Cabinet paper was lodged (1 April as it turns out). I’d narrowed the timeframe because I’d assumed there’d have been initial reactions earlier (after 13 September) but what I was interested in was the stuff that had led to the blow-up with the Governor). Treasury does not directly respond to this limb of my request either, but lists another paper soon to be released, dated 13 March (ie post Orr), a formal Treasury Report on funding agreement issues. And that is all. If Treasury’s responses are at least approximately truthful, it seems that they were very late in getting onto this set of issues (either future Funding Agreement bid, with its artificially high purported baseline, or the 24/25 budget itself, which had blasted through the then Funding Agreement limits).

If so, one might – just possibly, and in a mood of charity – be marginally less unsympathetic to the Governor. Perhaps he really thought he was going to get away with a) the massive 2024/25 overspend, and b) the artificial baseline for the new Funding Agreement. After all, it seems there had been no Treasury challenge or scrutiny at all, and his numbers even seemed to have found their way into the official fiscal forecasts with no challenge or question. It is astonishing that for months – dating all the way back to that draft SPE – there seems to have been no serious pushback, from the Minister or from Treasury. What sort of job were top Treasury officials doing in monitoring this powerful Crown agency? Not much of one it appears. Deputy Secretaries (both now out of the jobs they held then) are recorded as having turned up for chats at Board meetings, but what of it if excess of this sort was allowed to roll on for months unchallenged?

It is always possible that the way my OIA requests were drafted means something of significance has been able to be withheld as not quite falling within the specific scope of those requests. It is certainly difficult – nay impossible – to believe that there was nothing at all prior to 13 February. But it certainly doesn’t look as though Treasury was doing its job in a way citizens, let alone the Minister, might have reasonably expected that they would be.

That is the headline in a story in The Post this morning. After inquiries from Post journalists a Reserve Bank spokesperson said that final decisions on organisational change, advised to staff last week, would mean a net loss of 142 jobs (35 of which were currently vacant; presumably the Bank has had some sort of hiring freeze in place for some months now).

The last public number we had for Reserve Bank staff numbers was in the Minister’s Funding Agreement Cabinet committee paper: 660 FTEs as at 31 January. Presumably a) there were some vacancies even then, and b) the number of jobs was greater than the number of FTEs, but even if there were 700 filled or unfilled jobs in January the recent decisions would still be a cut in excess of 20 per cent. That is brutal in any organisation, especially when its statutory roles and functions haven’t changed a jot. It is hard to imagine morale is particularly high in the Bank at present, and we might even sympathise with the more junior of the staff losing their jobs, especially those hired in the last year or two, really on what amounts to false pretences. Even those (probably a minority) doing useless jobs far beyond the scope of the Bank’s actual statutory functions.

You don’t really expect junior hires to a core government agency to have to do due diligence on whether that agency was running spending levels – and hiring plans – far in excess of what had been approved for them by the Minister of Finance. But that is what had happened: Board approved spending last year was 23 per cent higher than what the previous Minister of Finance had approved for 24/25 when he increased the Funding Agreement amounts just before the last election. Treasury didn’t seem to have noticed, or done anything to call it out, so one can only sympathise with new hires now being thrown back onto the job market.

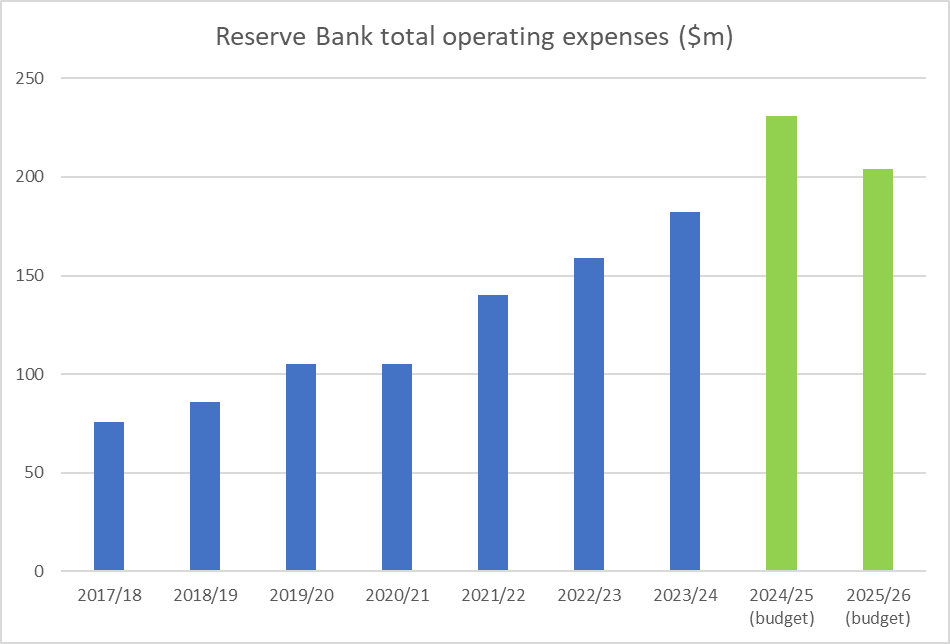

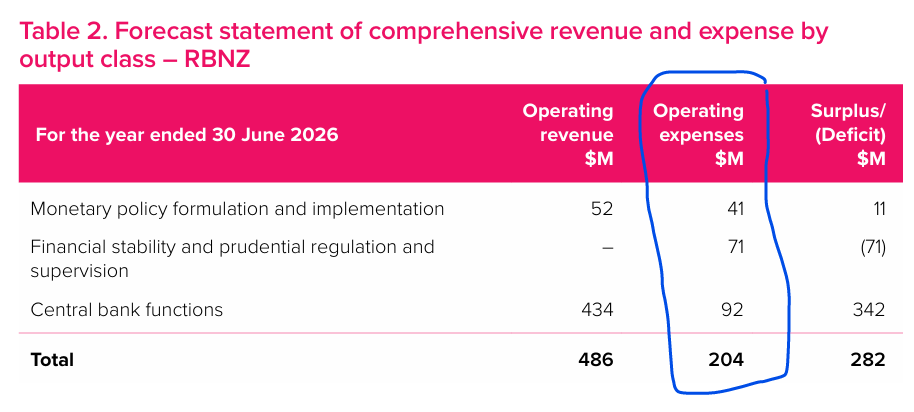

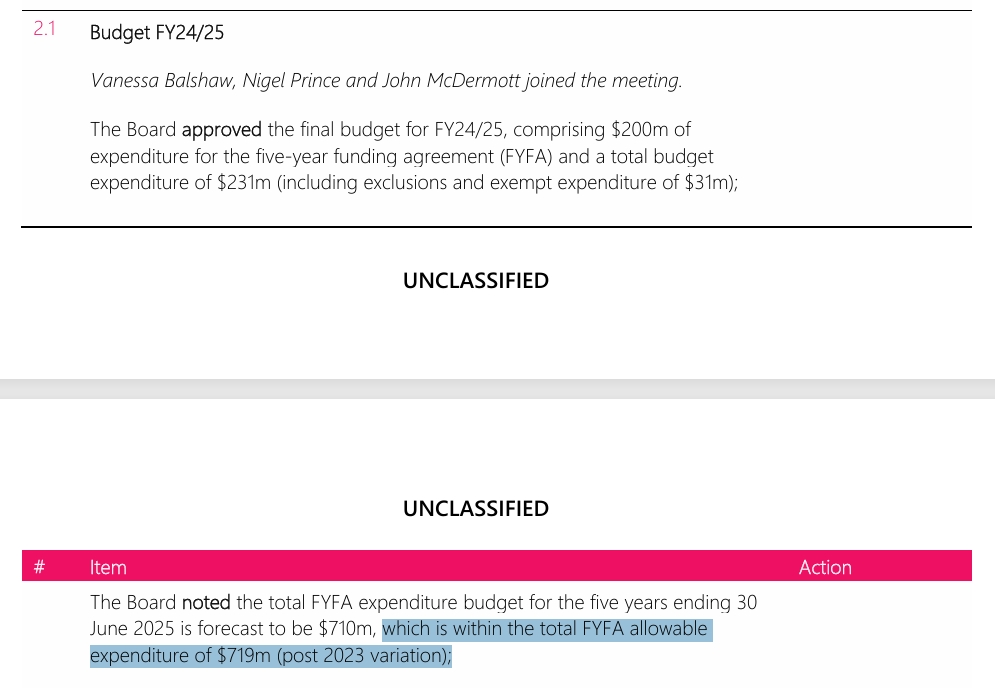

And you can see how last year’s excess created today’s problems. The number of FTEs increased from 601 to 660 between 30 June last year and 31 January this year. Had they not gone on that last hiring binge, adjustment now would be much less painful all round. This table, showing FTE numbers, is from the 2023/24 Annual Report published last September.

It is a reminder of how rapidly Orr and Quigley had been ramping up staff numbers, with no substantial change in functions. Cut FTEs by 20 per cent from that 31 January level (660) and it would take the Bank down to 528 FTEs, at which point it would still be larger than it had been on 30 June 2023, the final balance date under the previous Labour government (under whose term almost all agencies had seen rapid growth in staff numbers). It makes the point that the cuts the current Minister of Finance approved have not been deep at all relative to what was going on (spending allowances, staffing) on Labour’s watch. (I reckon the Bank’s core functions could probably be done professionally with 350 staff, but save that debate for another day.)

One way of seeing this is to look at the Bank’s total operating expenses. In the final budget approved during Labour’s term, the Bank budgeted to spend $212 million in total operating expenses in 2023/24. For 2025/26. the recently published budget for total operating expenses is $204 million, 3.8% lower than in 2023/24. Add in, say, 5 per cent inflation over the two years and you are still looking at a real cut of under 10 per cent. Not easy to adjust to perhaps, but not very different from what a lot of other government agencies have experienced. The wild card of course was the budget for 24/25: $231 million. This year’s budget is about 14 per cent lower than that in real terms. But that 2024/25 budget never had any ministerial authorisation at all.

Another, but murkier, way of looking at it is to look at approvals under the Funding Agreement (which cover a – changing – subset of total operating expenses, but which are where the Minister of Finance is supposed to have control).

In the August 2023 update to the last Funding Agreement, Grant Robertson approved the Bank spending $149.44 million on in-scope operating expenses. In addition, they were explicitly allowed to spend on these items about $5 million of the amount that had been allowed for currency issuance expenses but which wasn’t needed for that purpose. So, say, $154,5m on in-scope operating expenses.

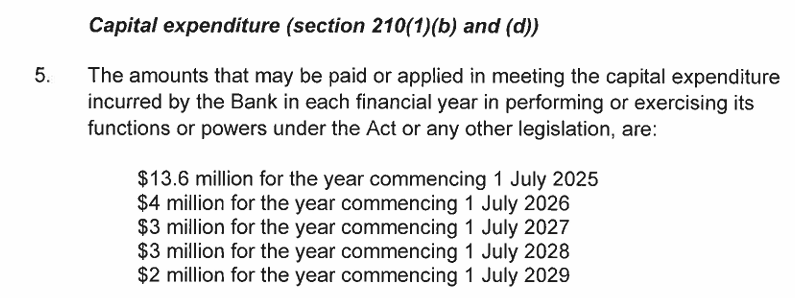

In the new Funding Agreement approved by the Minister in April this year, total in-scope operating expenses allowed for this year is $155 million (dropping away to $145 million next year, for reasons not made clear in the documents published so far, but maybe reflecting upfront restructuring costs – redundancy payments now for all those losing their jobs, already some weeks into 25/26?).

But you can’t just compare and contrast $155 million with $154.5 million because in the new Funding Agreement more spending items have been moved out of scope, not required to be covered within that $155 million limit. There are some smallish items (eg costs associated with the Bank’s legacy superannuation scheme, totalling probably less than half a million this year). But there is also this

Remember, these are business case costs, not some full cost of a project but you’d think they might easily total another million or two (consultants don’t come cheap).

And there is this explicit carveout, with some numbers

ie $5 million a year

Add those three items back in and the appropriate comparison to last year’s Funding Agreement level (the $154.5 million) is perhaps more like $161.5 million ($155 + 5 + 1.25 + 0.25). It drops away next year, but taking $10 million off that total still doesn’t leave them much less than the $154.5 million they were allowed for 24/25. The big problem – for them – is that they simply ignored that 24/25 limit and went for broke, hoping they could trick the Minister into setting them a permanently higher new baseline level of spending. It didn’t work fortunately. In a decent world they’d all (Orr, Quigley, the rest of last year’s board) apologise to the Minister, to the public, and to their own staff. In our world, staff lose their jobs and Quigley and the board keep theirs.

It is still interesting that they are needing to make such deep staff cuts to meet the budget and stay within the new Funding Agreement limits. Perhaps one partial reason might be the big new commitment they made to office space in Auckland – in what is apparently one of the fanciest new buildings in Auckland, with a five star green rating as well – on a scale which to have been anything like justified would have required even more growth in staff numbers. They signed up to that 4800 square metres last November, with no idea where the Funding Agreement would land and knowing they’d already well-overreached the previous Funding Agreement limits. According to last year’s Annual Report they spent $1 million on Rental and Lease Expenses (presumably mostly/wholly on their existing office space in a 40 year old building in Queen St). Not exactly a source I’d rely on for much but Google’s AI overview suggested that annual lease costs on the space in the new building could be $3.5 million (and their lease there runs from 1 August, while the existing lease doesn’t expire until 31 December).

In concluding I want to come back very briefly to the Post article. It is right to say that the Bank got much less than it had had the gall to ask for (unlike Oliver Twist, in asking for more they were already bloated), but what they are allowed to spend this year and next isn’t much different in real terms than what Grant Robertson had allowed them when he’d set the spending limit for 24/25. It is just a shame – actually, it should be scandalous – that they chose to ignore that limit so egregiously. Taxpayers and their own staff now pay the price.

Various bits and pieces have emerged from the Reserve Bank in the last couple of days; two in the form of other people’s OIA requests, and one in a partial response from the Bank to one of mine lodged with Treasury.

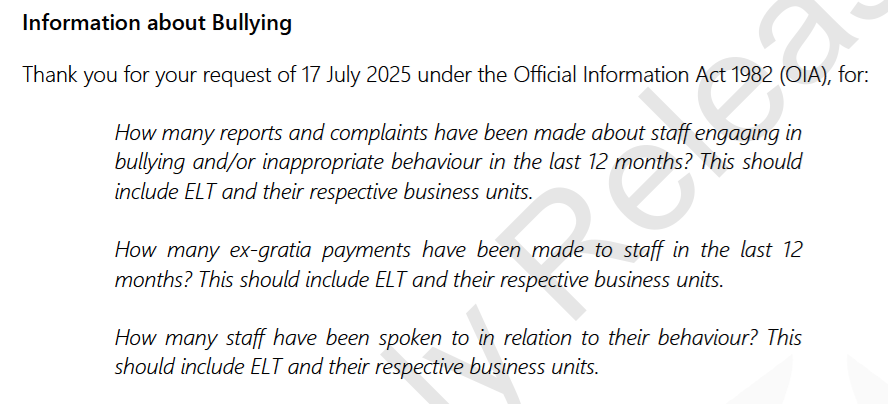

First, bullying. Someone, who must have had some knowledge of what was going on, had lodged a request for this information

Perhaps the Bank is turning over a new leaf on OIAs, as the request had only been lodged on 17 July and not only did the response go back to the requester on Monday (4 August) but they put it on their website that day (the Bank is quite selective about which responses they post, and there are often quite long lags). In fact, I just noticed there is another response – to a request lodged on 24 July – sent today and posted on the website today. If this really is a change of heart it is excellent news.

Anyway, the answers were interesting, to say the least

In the words of one former colleague, those payouts were “startling”. The 20 staff being spoken to seems a lot too, but who knows quite what standard they were using. Perhaps someone had spoken disrespectfully of the tree god, or suggested that the Bank really should have stayed within its allowed Funding Agreement spending limits? But to actually write cheques, hand over money, things must have been quite serious, even in an organisation not recently known for its budgetary discipline.

We know nothing more at this stage (amounts, specific reasons, who was responsible for the behaviour for which the ex gratia payments were made). To be entirely literal it isn’t 100 per cent clear that all the payouts were for bullying (the request covers any ex gratia payments to staff), but they probably were, given that the Bank headlines the entire response “Information about Bullying” and would have had an incentive to minimise the bullying dimension if there really were other reasons for some of the payments. Were the payments made before or after Orr left, and were any of them on account of his behaviour? I gather from Twitter that someone has lodged a further OIA so perhaps we will learn a bit more in time. But it doesn’t look good – and cases rising to level of payout must only be the tip of an iceberg, as some people are likely to be reluctant to lodge complaints, and others may simply have left the organisation.

The second OIA was about the new Auckland office (also only lodged on 24 July). You may recall that my source had indicated that the Bank had signed up to a fancy new Auckland office of a size probably inconsistent with the looming budget cuts. The Bank’s response seems to broadly back that story. The new lease agreement was signed on 4 November 2024. By that time (and as far as we can tell at present) the Bank did not know that its approved spending levels would be cut a long way back from what they had bid for when they lodged their next five year Funding Agreement bid in September. However, they were well aware that they had gone out on a limb, adopting a budget for 24/25 that was 23 per cent in excess of what they were allowed by Grant Robertson for that year under the Funding Agreement then in place, and had sought to persuade the Minister and Treasury that any (modest) cuts should be only from that unauthorised high “baseline”.

And while they may have needed a new Auckland office, this was the new space

and this was what it was to replace

In other words, they committed to more than twice the floorspace, in a more up-market building, at a time of general fiscal stringency and when they had no particular reason to suppose that they’d be allowed to keep growing. I’m not a property person but it seems that 10-15 square metres per head is about normal for typical open plan office

So it looks as though the Bank had gone lavish on the per capita floor space even if the new office was to be fully occupied at some point in future (which would have been a lot larger scale than the 164 staff and contractors they had in the Auckland office as at 30 June).

It seems a lot like a cavalier use of public money, made even worse (than their general budget excess) by the no-doubt multi-year nature of the property lease. But perhaps they’ll be able to sublet some of it?

And that spilled over into the third OIA response, that turned up this afternoon. It was part of a request I’d lodged with Treasury a couple of months ago which they’d transferred (that part of) to the Bank, and covers some late-in-the-piece material from the Bank to and from the Minister on Funding Agreement matters, after Orr had left. To be honest, I didn’t even think this material was in scope, as I’d been looking for Treasury material. As it happens, when I read what came in, parts seemed familiar, and I realised they’d already released these particular documents to someone else a month or so ago and I’d used a couple of bits of it last month (end of that post). But I hadn’t looked that closely then, and the significance of other aspects is also more apparent now.

First, last Friday I highlighted the way the temporary Governor Christian Hawkesby appeared to have actively misled FEC on where the initiative lay for the review the Bank now has underway of bank capital requirements. He played down any ministerial involvement claiming it had been just a Bank decision to do the review. That it clearly wasn’t was pretty evident from the Treasury filenote of that 24 February meeting between the Bank, Treasury and the Minister.

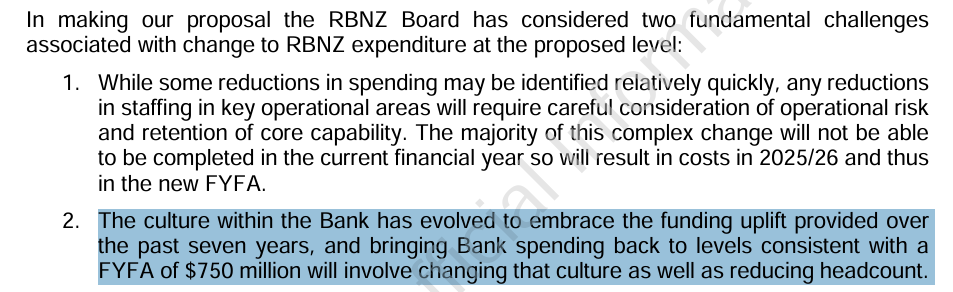

But to reinforce the point, here is Neil Quigley writing to the Minister on 16 March basically pleading (successfully) that she not accept Treasury’s view of how deep the cuts to operating expenses should be. This was the paper in which he pleaded that the Bank’s “culture” had evolved in light of the fiscal excess of recent years and that it would take time to change the culture and save lots of money. But he also said this

Hawkesby actively misled FEC. Once upon a time that sort of thing mattered.

Where Quigley was largely unsuccessful at this stage was around the capital budget (not something I’d previously paid any attention to). The initial bid last September had been for $50 million over five years. At this point Treasury was proposing $26 million (which, assuming the numbers in the Minister’s Cabinet paper are comparable, was 12 per cent less than total expected capex for 2020-2025). Here was Quigley’s plea

Note that first item. If you’ve just rashly signed up to big new offices in a fancy building the fit out costs (for a lease that commenced on 1 August 2025) were likely to be large.

Quigley’s capex plea failed, and the Minister ended up agreeing to allow them only $26.3 million of capex over the full five year period. This is the annual phasing.

Which might suggest that they will be spending something close to $10 million on the fit-out of a new office that they simply shouldn’t have signed up to before they had any clear steer about the future. The 25/26 number ended up a bit higher even than the $13m Quigley had sought on 16 March – new estimates of fit out costs? – with the capex allowances for future years being slashed. (If Quigley’s plea is even roughly accurate you might wonder how sustainable all this proves – presumably the Bank will spend all its opex allowance, and perhaps they reckon they’ll come back cap in hand in a few years’ time, or degrade the existing capital and wait for the next Funding Agreement negotiations. Or Treasury might be right about what they need.)

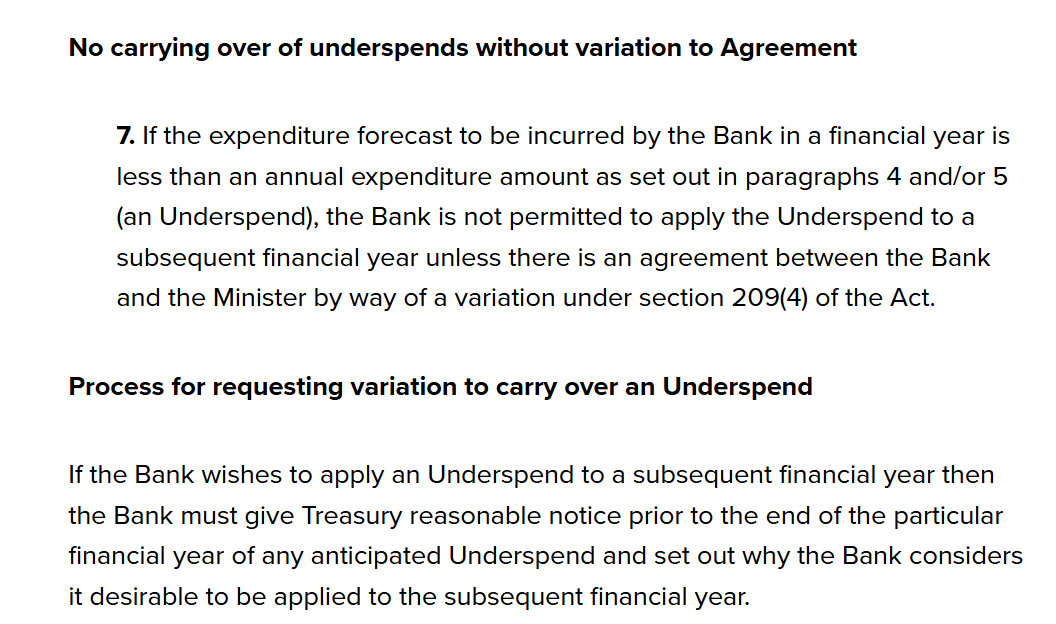

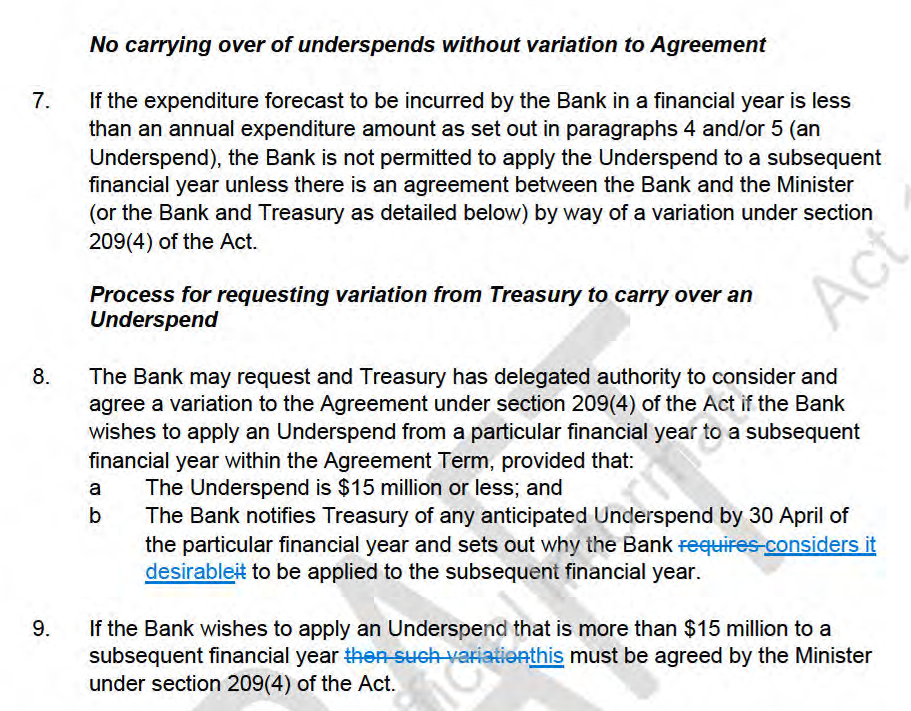

The final observation from these papers is perhaps not of any great moment, but it is puzzling nonetheless. You’ll recall that the Bank had gone ahead and set a budget for 24/25 far in excess of what the Funding Agreement had allowed. There was never any serious suggestion that the Bank was allowed to carry forward earlier year underspends, use it all for a last year splurge, and then try to use that new level as a baseline against which any modest cuts should be set. But that is how Orr, Quigley and the rest of the board had operated (quite explicitly – it is in the Board minutes and the September 2024 Funding Agreement bid).

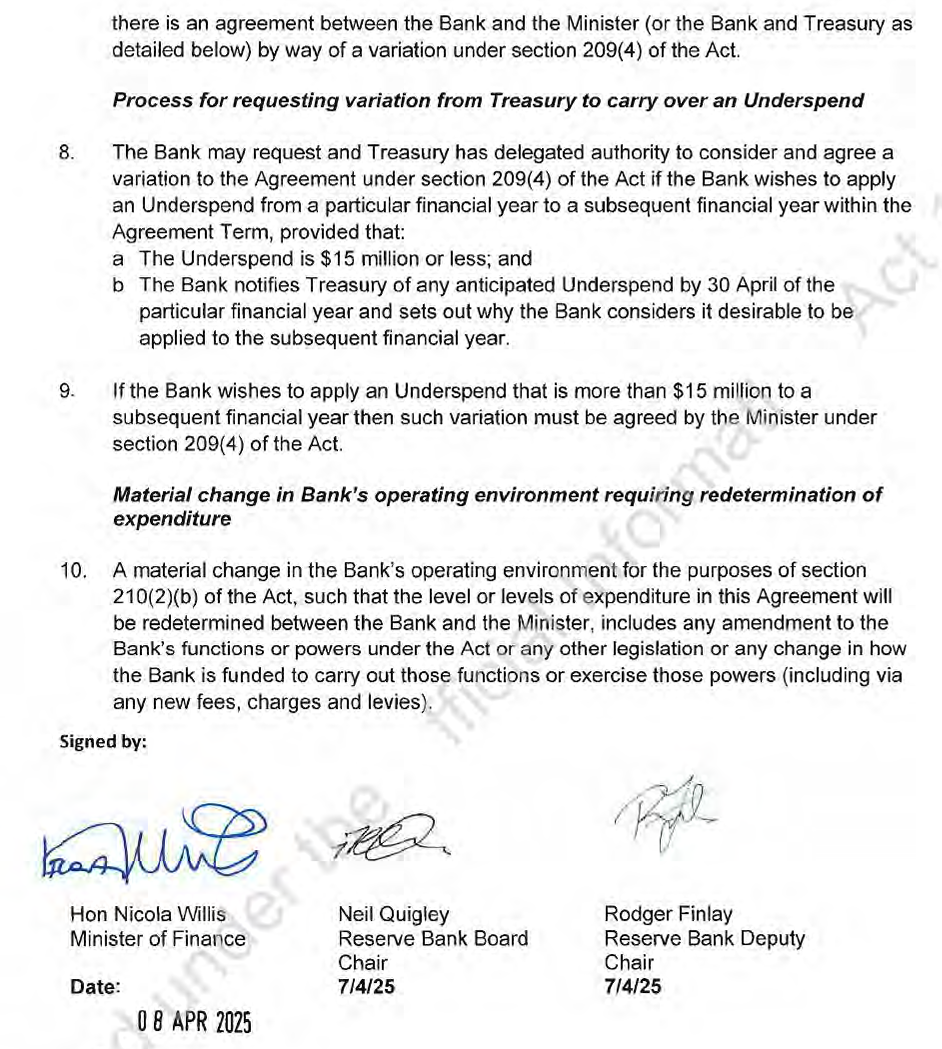

There are problems with the Funding Agreement model, which involves setting annual spending limits five years ahead. Sometimes it is hard to know when a particular cost might arise. So it probably does make sense – if this model is stuck to – to allow scope for some flexibility. It is there anyway – no one gets fired for going a bit under or over in any year (and isn’t formalised like a parliamentary appropriation), and there is always scope for a renegotiation mid-stream (as there’d been in 2023). But the Bank was keen to formalise something. I noted in a post last month that in that 16 March paper the version of the draft agreement the Bank submitted involved a model in which Treasury could agree to modest variations (up to about 10 per cent) and anything more required the Minister.

I included the signature block because what I hadn’t noticed before – hadn’t read to the end of the set of documents, which looked like they were just repetitions and admin paperwork – is that she seemed to agree to this only after she’d already signed up to something like what the Bank wanted.

In that OIA response there was this

All signed and dated and a scanned version sent back to Bank by one of the advisers in the Minister’s office, in a email of 10:14am on 8 April.

We are left wondering what happened. Quigley’s memo of 16 March did not touch on the variation issue at all. Was the Minister not made aware of it, including by Treasury, until the very last minute, or was she aware all along and very belatedly chose to take a harder line? Fortunately she did finally land on the best approach, but how? The original OIA to Treasury, lodged back in June but due shortly, may shed some light, but it just doesn’t look like a particularly smooth or adept end to the Funding Agreement process. And I wonder what Quigley, Finlay, and Hawkesby made of the latest, last, loss………..which couldn’t have happened to a more deserving bunch given their egregious bid six months earlier.

As for me, I guess I should read OIA responses – even other people’s – a bit more closely.

There are still lots of outstanding questions around the sudden departure of the Reserve Bank Governor, and the handling of those events by the board and the Minister. But, even amid ongoing OIA obstructionism – the Bank simply ignoring the substance of specific requests, in a flagrantly illegal way – some more bits and pieces have emerged.

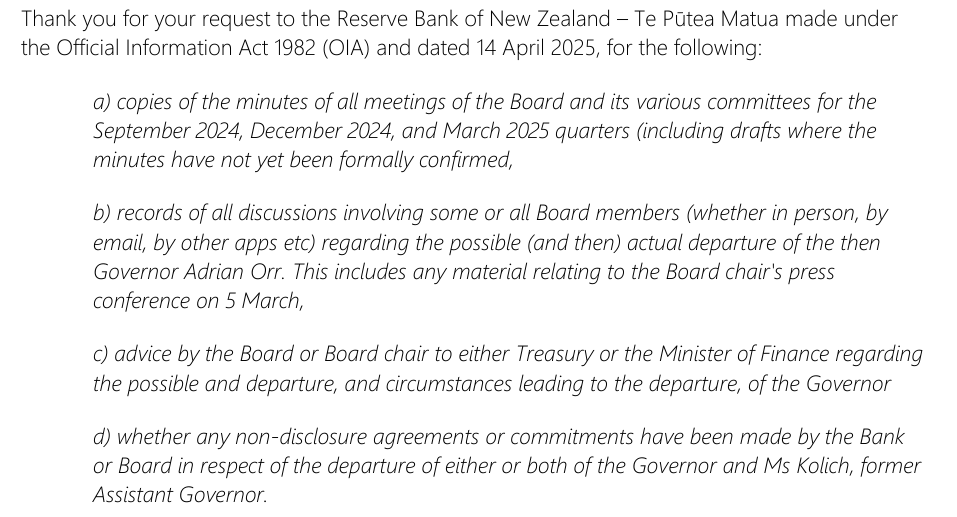

Back in April I lodged these requests

The Bank finally got round to responding on 30 June.

Of those, item a) wasn’t primarily about Orr’s departure (for unrelated reasons I wanted to see how their board committees work). Nonetheless, the response was interesting because although they sent me the committee minutes (with redactions), they didn’t even address the request for the minutes of actual Board meetings. As it happens, the Bank periodically (normally quarterly) releases rather limited and selective minutes of regularly scheduled Board meetings (you can find them here) and I’d lodged the request mostly because by 14 April they hadn’t released any for six months). They’ve since put up more recent ones. The Bank’s usual approach when someone requests something that is already on a website by the time the reply goes out is to point requesters to a link to those documents and then decline the specific request because the document is already publicly available (legitimate grounds for denial). This time, however, there is no mention in the response of the board minutes at all (only a mention that the committee minutes were attached, as they were).

This suggests an (illegal) effort to avoid addressing the specific request. One possible reason might be because it is almost certain that there will have been short-notice board meetings in and immediately around Orr’s resignation, which they don’t want to either acknowledge or disclose the records of. How could it have been otherwise? The Governor tells the board chair he’s thinking of resigning, and the Board does nothing, never meets, never authorises an exit package with gag agreements? Even for an apparently supine board like that of the Reserve Bank it seems very very unlikely. And when the Governor actually resigns – recall it was brought forward at the last minute by several days – there is no short notice Zoom board meeting to discuss what next? Yeah, right. (I’ll come back later to some interesting points in the minutes of the scheduled board meetings).

Another reason to believe that might be the explanation is the Bank’s response to my second item (above). This was it

That is a reference to the belated bulk release (available here), apparently designed to shape how we should think about Orr’s departure. But…..that response to my request by the Bank simply does not address my specific request, because the 11 June release contained precisely nothing about discussions among board members and nothing about the chair’s press conference later on the afternoon of Orr’s resignation (and nothing about any short-notice board meetings). Of course there will have been discussion among board members, and there might be even be some OIA grounds to withhold some of that specifically (in which cases such withholding needs to be justified specifically, item by item), but this response seeks to pretend answers have been provided when in fact the whole issue has been avoided.

Item d) of my request was overtaken by events. I was no longer particularly interested in Kolich’s departure (and the 11 June release suggested it was in train before Orr left), and the 11 June release did tell us there was an NDA with Orr (although we still have no idea what the nature of the gagging provisions were, or why they were imposed or accepted by the Board, or the Minister – you’ll recall from previous posts that a Governor’s resignation is addressed to the Minister not the Board).

But then there was item c) (above). There is a typo in the request, but the Bank seems to have understood it as intended (about possible and actual departure). This was their response

It is quite extraordinary really. Things had run so far off the rails that the Governor was first talking of resigning then actually planning to resign – partly, the 11 June release tells us, because effective future working relations were so impaired, in the context of the funding agreement disagreements – and neither the Board nor the Board chair initiated any (direct) contact with the Minister of Finance at all; no meetings, no texts, no calls, no written advice, no nothing. If true, and I guess we must assume it is so, it is extraordinary, and something of a dereliction of duty, given that the Board governs the Bank, monitors the Governor etc all on behalf of the Minister, who not only has general responsibility for the Bank but specific responsibility for hiring, firing, and (in this case) receiving a Governor’s resignation. (Other releases show that Quigley had alerted Iain Rennie to what was going on, who’d mentioned it to the Minister). I usually word such requests quite carefully to specifically include “or the minister’s office” and failed to do so this time. I guess it is possible they are hiding behind that and there was contact by Quigley and the Board with senior advisers to the Minister, but on this occasion I doubt that is so because of the final two sentences in that response. It was nice of them to tell me about that but since it was from the Minister, conveyed via her office, it wasn’t specifically within the scope of my request (but one is left wondering why it wasn’t disclosed in the 11 June release).

It just seems astonishing. And not least because of how the Board just seems to assume the freedom to negotiate gag orders with Orr, when a) his resignation had to be made to the Minister not to them, and b) when there would inevitably be intense public questioning and scrutiny of what was going on, and they were proposing even to tie the Minister’s hand without consulting her.

And then the only contact is the ill-judged (as it turned out) request from the Minister’s office for the Board chair to do a press conference. I don’t disagree that both the Board chair and the Minister owed us answers (which we still don’t have) but Quigley is singularly bad at fronting when dealing with challenging questions, and his responses in that press conference ended up raising more questions than answers, at times apparently actively misleading journalists and the public, all while there were no evident market ructions to calm. More questions for the Minister I guess: does she even now know the terms of the gagging agreements entered into? If not, why not? If so, how and why does she defend or justify them?

I noted earlier that the March quarter Board minutes (released on 18 June, conveniently after the 11 June release) had some interesting content (and some telling omissions).

There were records of two meetings. The first was on 27 February (which reports the Board approved minutes of a 14 February special meeting, minutes of which – not disclosed – were clearly within scope of my request). This was the meeting – we were told in the 11 June release – where things crystallised

with the Board taking one view on the future Funding Agreement (bowing to reality) and the Governor refusing to do so. You have to imagine there was quite an extensive and tense discussion. But here is what the Board minutes have to say about discussion of the Funding Agreement and associated negotiations.

That’s right. Precisely nothing. And it is not as if some very sensitive material has been withheld on legitimate OIA grounds (hard to see what now that so much is a) finalised and b) in the public domain). It is just that there is no mention of the Funding Agreement in the 10 pages of minutes of a seven hour meeting.

It is extremely dubious, because it appears like an active effort to mislead readers (of these proactively released documents) and, unless there are secret shadow minutes, a breach of the Public Records Act, which requires public agencies to maintain proper records, including of such consequential meetings and discussions. It seems likely that much of the discussion will have occurred in item 6.2 “Board Only Time”, where nothing is disclosed (or withheld), although even then how plausible is it that all the discussion of the Funding Agreement, where there were major differences, occurred without any other senior management present (CFO or that person’s boss, or the Deputy Governor)? It really is a classic example of minutes theatre: it is good that the Board releases proactively what they do, but this example illustrates again just how selective (and thus dishonest) their approach is.